|

Related Topics |

|

On this page we will update the daily performance of the JSE All Share Index on our calendar graphic. We will also add the latest market related news on this page as and when it happens. If you want to keep up to date with the JSE All Share Index performance this is the page to keep an eye on

|

|

8 June: The summary below covers quick facts about Carnival Corporation, the worlds biggest cruise ship company. Our sister website covered Carnival Corporation as part of their More About series

Read the full article here

27 May 2020: Our sister website started a series on providing more interesting information on US listed stocks. Below a few quick facts on two stocks looked at recently. They are The Home Depot and Constellation Brands

The Home Depot

The data below refers to the full fiscal 2019:

Read the More About The Home Depot article here

Constellation Brands

Read the More About Constellation Brands here

21 May 2020: Earlier in the week we covered the latest JSE trading statistics for the trading week ended 15 May 2020. Below an extract of that article.

Number of trades:

Number of trades (2020): 1 686 349

Number of trades (2019): 1 635 856

% change year on year: 3.09%

Volume traded:

Volume traded (2020): 2 192 566 000

Volume of traded (2019): 1 448 466 000

% change year on year: 51.37%

Value of trades:

Value of trades (2020): R105 209 137 000

Value of trades (2019): R105 477 824 000

% change year on year: -0.25%

Foreign purchase/selling:

Net sales/Purchases (2020): -R 2 166 591 000

Net sales/Purchases (2019): -R454 868 000

So year to date (YTD) foreigners have been net seller/buyers:

Net sales/Purchases (2020): -R30.098 billion

Net sales/Purchases (2019): -R29.222 billion

Read the full article here

6 May 2020: Yesterday we covered the latest PE ratio of the JSE All Share Index as at the end of April 2020. The overall price to earnings ratio of the JSE All Share Index increased sharply as markets recovered from the strong sell off the month before. Below a short extract from that article

So since January 2011, the JSE All Share average PE ratio is sitting at 16 . As at the end of April 2020, the JSE All Share PE ratio was sitting at 14.20 (so well below above the average levels since the start of 2011). And the longer term PE ratio as measured by the 13 month moving average (which has been in constant decline for some time now), came in at 16.00, which is above the current PE ratio of the market as a whole.

Read the full article here

22 April 2020: Yesterday the South African President Announced a massive relief package totalling R500 billion to address the impact of Covid-19 on South African citizens, and businesses. In the announcement he mentioned that is is roughly 10% of South Africa's economy. We checked the numbers on our South Africa's GDP page. See an extract from that page below

Today President Ramaphosa announced a comprehensive social and economic relief package for South Africans to fight off the effects of Covid-19 is having on citizens, businesses and South Africa's economy. The president stated that the R500 billion relief package is about 10% of South Africa's GDP. In 2019 the total worth of South Africa's economy, in current prices amounted to R5.077 trillion according to data from Statistics South Africa. So the relief package is as the president said, about 10% of the size of South Africa's economy in current prices.

17 April 2020: The South African Reserve Bank cut the South African REPO rate by 100 basis points for the second time in less than a month as it looks to provide consumers with financial relief during the tough economic times brought on by the Covid-19 lockdown in South Africa. Below an extract from the monetary policy statement

Against this backdrop, the MPC decided to cut the repo rate by 100 basis points. This takes the repo rate to 4.25% per annum, with effect from 15 April 2020. The decision was unanimous. The implied path of policy rates over the forecast period generated by the Quarterly Projection Model indicates five repo rate cuts of 25 basis points extending into the first quarter of 2021. Monetary policy can ease financial conditions and improve the resilience of households and firms to the economic implications of Covid-19. In addition to continued easing of interest rates, the Bank has taken steps to ensure adequate liquidity in money and government bond markets and to ease capital requirements to free capital for onlending by financial institutions.

Each of these steps make more capital available to households and firms. Monetary policy however cannot on its own improve the potential growth rate of the economy or reduce fiscal risks. These should be addressed by implementing prudent macroeconomic policies and structural reforms that lower costs generally, and increase investment opportunities, potential growth and job creation. Such steps will further reduce existing constraints on monetary policy and its transmission to lending.

Global economic and financial conditions are expected to remain highly volatile for the foreseeable future. In this highly uncertain environment, future decisions will continue to be highly data dependent, sensitive to the balance of risks to the outlook and will seeks to look through temporary price shocks. As usual, the repo rate projection from the QPM remains a broad policy guide which can change from meeting to meeting in response to changing data and risks.

Lesetja Kganyago

GOVERNOR

The next statement of the Monetary Policy Committee will be released on 21 May 2020

Read the full article here

8 April 2020: Yesterday we covered the latest JSE trading statistics for the week ended 3 April 2020. Below an extract from that article.

Number of trades:

Number of trades (2020): 2 229 397

Number of trades (2019): 1 488 515

% change year on year: 49.77%

Volume traded:

Volume traded (2020): 2 480 915 000

Volume of traded (2019): 1 452 713 000

% change year on year: 70.78%

Value of trades:

Value of trades (2020): R115 663 108 000

Value of trades (2019): R98 170 521 000

% change year on year: 17.82%

Foreign purchase/selling:

Net sales/Purchases (2020): -R3 442 722 000

Net sales/Purchases (2019): -R1 563 029 000

So year to date (YTD) foreigners have been net seller/buyers:

Net sales/Purchases (2020): -R29.433 billion

Net sales/Purchases (2019): -R26.227 billion

Read the full article here

2 April 2020: Yesterday we covered the latest formal sector employment numbers for South Africa for the quarter ending December 2019

The summary below shows the number of employees per industry as at December 2019

Read the full article here

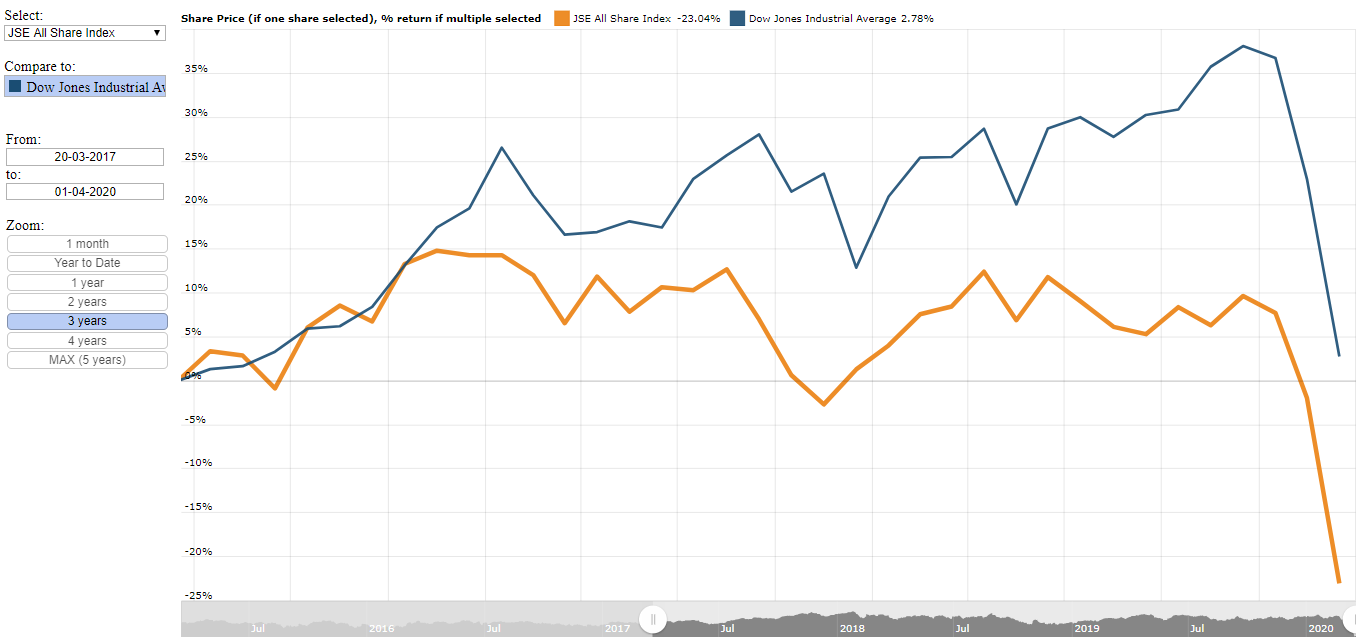

19 March 2020: Yesterday we compared the performance of the Dow Jones Industrial Average to that of the JSE All Share Index over various time periods. Below a short extract from that article.

The summary below shows the returns provided by the JSE All Share Index and the Dow Jones Industrial Average over the last 3 years

So over the last 3 years the Dow Jones Industrial Average is better off by roughly 26%, while over a year period it was better off by about 13% and for the 2020 year to date it was better off by about 3.5%. So the longer the time period the bigger the difference in the performance between the JSE All Share Index and the Dow Jones.

This certainly makes the case for South Africans to invest off shore and to get exposure to foreign markets and indices such as the Dow Jones Industrial Average of the S&P 500.

Read the full article here

- Carnival Corporation is listed on the New York Stock Exchange under share code ticker: CCL

- Number of employees: 150 000

- Passengers Carried (in thousands) :12,900

- Passenger Capacity :249,000 lower births

- Number of Ships: 104

- Revenues in 2019: $20.825 billion

- Earnings per share in 2019: $4.32

- Shares in issue: 692 million

- Dividends paid per share in 2019: $2.00

- Stockholders equity in Carnival Corporation: $25.365 billion

- Stockholders equity per share: $36.65

Read the full article here

27 May 2020: Our sister website started a series on providing more interesting information on US listed stocks. Below a few quick facts on two stocks looked at recently. They are The Home Depot and Constellation Brands

The Home Depot

- The Home Depot is listed on the New York Stock Exchange under stock code ticker: HD

- Total revenues for 2019 fiscal year : $110.225 billion

- Number of Home Depot Stores: 2 291

- Average Home Depot store size: 104 000 square feet plus an average of 24 000 square feet for the outdoor and garden section

The data below refers to the full fiscal 2019:

- Comparable sales increase: 3.5%

- Comparable customer transactions increase: 1.1%

- Comparable average ticket increase:2.5%

- Customer transactions (in millions): 1,616.0

- Average ticket: $ 67.30

- Sales per retail square foot: $454.82

- Diluted earnings per share $ 10.25

Read the More About The Home Depot article here

Constellation Brands

- Main brands of Constellation include: Corona, Modelo and Casa Noble Tequila

- 9,800 employees. Approximately 4,900 employees were in the U.S. and approximately 4,900 employees were outside of the U.S., primarily in Mexico

- Annual net sales in 2019: $8.116 billion

- Beer sales makes up 64.1% of the group's total sales

- Number 3 beer company in the U.S

- Total assets: $29.231 billion

- Stockholders equity: $12.83 billion

- Shares in issue: 167.249 million shares

- Dividend declared during 2019 fiscal year: $2.96

Read the More About Constellation Brands here

21 May 2020: Earlier in the week we covered the latest JSE trading statistics for the trading week ended 15 May 2020. Below an extract of that article.

Number of trades:

Number of trades (2020): 1 686 349

Number of trades (2019): 1 635 856

% change year on year: 3.09%

Volume traded:

Volume traded (2020): 2 192 566 000

Volume of traded (2019): 1 448 466 000

% change year on year: 51.37%

Value of trades:

Value of trades (2020): R105 209 137 000

Value of trades (2019): R105 477 824 000

% change year on year: -0.25%

Foreign purchase/selling:

Net sales/Purchases (2020): -R 2 166 591 000

Net sales/Purchases (2019): -R454 868 000

So year to date (YTD) foreigners have been net seller/buyers:

Net sales/Purchases (2020): -R30.098 billion

Net sales/Purchases (2019): -R29.222 billion

Read the full article here

6 May 2020: Yesterday we covered the latest PE ratio of the JSE All Share Index as at the end of April 2020. The overall price to earnings ratio of the JSE All Share Index increased sharply as markets recovered from the strong sell off the month before. Below a short extract from that article

So since January 2011, the JSE All Share average PE ratio is sitting at 16 . As at the end of April 2020, the JSE All Share PE ratio was sitting at 14.20 (so well below above the average levels since the start of 2011). And the longer term PE ratio as measured by the 13 month moving average (which has been in constant decline for some time now), came in at 16.00, which is above the current PE ratio of the market as a whole.

Read the full article here

22 April 2020: Yesterday the South African President Announced a massive relief package totalling R500 billion to address the impact of Covid-19 on South African citizens, and businesses. In the announcement he mentioned that is is roughly 10% of South Africa's economy. We checked the numbers on our South Africa's GDP page. See an extract from that page below

Today President Ramaphosa announced a comprehensive social and economic relief package for South Africans to fight off the effects of Covid-19 is having on citizens, businesses and South Africa's economy. The president stated that the R500 billion relief package is about 10% of South Africa's GDP. In 2019 the total worth of South Africa's economy, in current prices amounted to R5.077 trillion according to data from Statistics South Africa. So the relief package is as the president said, about 10% of the size of South Africa's economy in current prices.

17 April 2020: The South African Reserve Bank cut the South African REPO rate by 100 basis points for the second time in less than a month as it looks to provide consumers with financial relief during the tough economic times brought on by the Covid-19 lockdown in South Africa. Below an extract from the monetary policy statement

Against this backdrop, the MPC decided to cut the repo rate by 100 basis points. This takes the repo rate to 4.25% per annum, with effect from 15 April 2020. The decision was unanimous. The implied path of policy rates over the forecast period generated by the Quarterly Projection Model indicates five repo rate cuts of 25 basis points extending into the first quarter of 2021. Monetary policy can ease financial conditions and improve the resilience of households and firms to the economic implications of Covid-19. In addition to continued easing of interest rates, the Bank has taken steps to ensure adequate liquidity in money and government bond markets and to ease capital requirements to free capital for onlending by financial institutions.

Each of these steps make more capital available to households and firms. Monetary policy however cannot on its own improve the potential growth rate of the economy or reduce fiscal risks. These should be addressed by implementing prudent macroeconomic policies and structural reforms that lower costs generally, and increase investment opportunities, potential growth and job creation. Such steps will further reduce existing constraints on monetary policy and its transmission to lending.

Global economic and financial conditions are expected to remain highly volatile for the foreseeable future. In this highly uncertain environment, future decisions will continue to be highly data dependent, sensitive to the balance of risks to the outlook and will seeks to look through temporary price shocks. As usual, the repo rate projection from the QPM remains a broad policy guide which can change from meeting to meeting in response to changing data and risks.

Lesetja Kganyago

GOVERNOR

The next statement of the Monetary Policy Committee will be released on 21 May 2020

Read the full article here

8 April 2020: Yesterday we covered the latest JSE trading statistics for the week ended 3 April 2020. Below an extract from that article.

Number of trades:

Number of trades (2020): 2 229 397

Number of trades (2019): 1 488 515

% change year on year: 49.77%

Volume traded:

Volume traded (2020): 2 480 915 000

Volume of traded (2019): 1 452 713 000

% change year on year: 70.78%

Value of trades:

Value of trades (2020): R115 663 108 000

Value of trades (2019): R98 170 521 000

% change year on year: 17.82%

Foreign purchase/selling:

Net sales/Purchases (2020): -R3 442 722 000

Net sales/Purchases (2019): -R1 563 029 000

So year to date (YTD) foreigners have been net seller/buyers:

Net sales/Purchases (2020): -R29.433 billion

Net sales/Purchases (2019): -R26.227 billion

Read the full article here

2 April 2020: Yesterday we covered the latest formal sector employment numbers for South Africa for the quarter ending December 2019

The summary below shows the number of employees per industry as at December 2019

- Mining and quarrying: 448 492

- Manufacturing: 1 209 342

- Electricity, gas and water supply: 61 225

- Construction: 575 423

- Wholesale, retail and motor trade; hotels and restaurants: 2 305 822

- Transport, storage and communication: 495 486

- Financial intermediation, insurance, real estate and business services: 2 348 270

- Community, social and personal services: 2 771 182

Read the full article here

19 March 2020: Yesterday we compared the performance of the Dow Jones Industrial Average to that of the JSE All Share Index over various time periods. Below a short extract from that article.

The summary below shows the returns provided by the JSE All Share Index and the Dow Jones Industrial Average over the last 3 years

- Dow Jones: 2.78%

- JSE All Share Index: -23.04%

So over the last 3 years the Dow Jones Industrial Average is better off by roughly 26%, while over a year period it was better off by about 13% and for the 2020 year to date it was better off by about 3.5%. So the longer the time period the bigger the difference in the performance between the JSE All Share Index and the Dow Jones.

This certainly makes the case for South Africans to invest off shore and to get exposure to foreign markets and indices such as the Dow Jones Industrial Average of the S&P 500.

Read the full article here

17 March 2020: Yesterday we covered the latest trading statistics for the JSE for the week ending 13 March 2020. One of the most brutal trading weeks in the stock exchanges history

Number of trades:

Number of trades (2020): 3 275 462

Number of trades (2019): 1 579 229

% change year on year: 107.4%

Volume traded:

Volume traded (2020): 2 997 932 000

Volume of traded (2019): 1 809 382 000

% change year on year: 65.70%

Value of trades:

Value of trades (2020): R181 036 168 000

Value of trades (2019): R122 758 890 000

% change year on year: 47.47%

Foreign purchase/selling:

Net sales/Purchases (2020): -R5 439 345 000

Net sales/Purchases (2019): -R5 508 578 000

So year to date (YTD) foreigners have been net seller/buyers:

Net sales/Purchases (2020): -R20.455 billion

Net sales/Purchases (2019): -R27. 448 billion

Read the full article here

11 March 2020: Our latest valuation on MTN following the release of their year end results for December 2019

So what do we value MTN shares at based on their latest financial results? Based on their results, the markets they operate in and the strong balance sheet, low PE ratio and very high dividend yield our valuation model provides a full value price (target price) of R106.60 per MTN share (up from our interim period 2019 valuation of MTN).

We usually recommend that long term fundamental or value investors look to enter a stock at least 10% below our full value price which in this case is R106.60. A good entry point into the shares of MTN would therefore be at R95.90 or below.

Since the stock of MTN is trading at well below our suggested entry point into the share we rate the shares of MTN as a buy

Read the full article here

6 March 2020: The extract below covers the latest JSE All Share PE ratio up to end of February 2020

So since January 2011, the JSE All Share average PE ratio is sitting at 17.66. As at the end of February 2020, the JSE All Share PE ratio was sitting at 14.62 (so well below above the average levels since the start of 2011). And the longer term PE ratio as measured by the 13 month moving average (which has been in constant decline for some time now), came in at 16.68, which is above the current PE ratio of the market as a whole.

So what does it tell us about the markets and its valuation? Well market valuations have certainly come down strongly since late 2016 when the market PE ratio was around the 23 mark. Since then company profits and earnings have been disappointing sending share prices tumbling down and dragging down PE ratios with them. The month of February 2020 was a particularly brutal months for the markets, with Coronavirus fears spreading across world financial markets and which saw the JSE All Share Index lose more than 10% of its value so far in 2020, and the last trading day of February seeing a decline of almost 5% in the JSE All Share Index.

Read the full article here

28 February 2020: Below an extract from our latest article regarding struggling petrochemicals giant, SASOL

So in summary one can say the following about SASOL's interim financial results. They are not paying an interim dividend, their core headline earnings per share declined from R21.45 a year ago to R9.20 now. Their total assets increased by 3% while their liabilities increased by a whopping 12%. In addition to that their total equity declined by 6% from R242.238 bilion down R14 billion to R228.646 billion.

Based on the group's prospects and the group's latest earnings and stopping the interim dividend we value the stock of SASOL at R167.90 a share. We therefore believe the stock of SASOL is overvalued and expect it to pull back from current levels to closer to our target price (full value price) in coming weeks and months.

Read the full article here

Number of trades:

Number of trades (2020): 3 275 462

Number of trades (2019): 1 579 229

% change year on year: 107.4%

Volume traded:

Volume traded (2020): 2 997 932 000

Volume of traded (2019): 1 809 382 000

% change year on year: 65.70%

Value of trades:

Value of trades (2020): R181 036 168 000

Value of trades (2019): R122 758 890 000

% change year on year: 47.47%

Foreign purchase/selling:

Net sales/Purchases (2020): -R5 439 345 000

Net sales/Purchases (2019): -R5 508 578 000

So year to date (YTD) foreigners have been net seller/buyers:

Net sales/Purchases (2020): -R20.455 billion

Net sales/Purchases (2019): -R27. 448 billion

Read the full article here

11 March 2020: Our latest valuation on MTN following the release of their year end results for December 2019

So what do we value MTN shares at based on their latest financial results? Based on their results, the markets they operate in and the strong balance sheet, low PE ratio and very high dividend yield our valuation model provides a full value price (target price) of R106.60 per MTN share (up from our interim period 2019 valuation of MTN).

We usually recommend that long term fundamental or value investors look to enter a stock at least 10% below our full value price which in this case is R106.60. A good entry point into the shares of MTN would therefore be at R95.90 or below.

Since the stock of MTN is trading at well below our suggested entry point into the share we rate the shares of MTN as a buy

Read the full article here

6 March 2020: The extract below covers the latest JSE All Share PE ratio up to end of February 2020

So since January 2011, the JSE All Share average PE ratio is sitting at 17.66. As at the end of February 2020, the JSE All Share PE ratio was sitting at 14.62 (so well below above the average levels since the start of 2011). And the longer term PE ratio as measured by the 13 month moving average (which has been in constant decline for some time now), came in at 16.68, which is above the current PE ratio of the market as a whole.

So what does it tell us about the markets and its valuation? Well market valuations have certainly come down strongly since late 2016 when the market PE ratio was around the 23 mark. Since then company profits and earnings have been disappointing sending share prices tumbling down and dragging down PE ratios with them. The month of February 2020 was a particularly brutal months for the markets, with Coronavirus fears spreading across world financial markets and which saw the JSE All Share Index lose more than 10% of its value so far in 2020, and the last trading day of February seeing a decline of almost 5% in the JSE All Share Index.

Read the full article here

28 February 2020: Below an extract from our latest article regarding struggling petrochemicals giant, SASOL

So in summary one can say the following about SASOL's interim financial results. They are not paying an interim dividend, their core headline earnings per share declined from R21.45 a year ago to R9.20 now. Their total assets increased by 3% while their liabilities increased by a whopping 12%. In addition to that their total equity declined by 6% from R242.238 bilion down R14 billion to R228.646 billion.

Based on the group's prospects and the group's latest earnings and stopping the interim dividend we value the stock of SASOL at R167.90 a share. We therefore believe the stock of SASOL is overvalued and expect it to pull back from current levels to closer to our target price (full value price) in coming weeks and months.

Read the full article here

10 February 2020: Towards the end of last week we covered the latest trading statement from Italtile. Below an extract from that article

EARNINGS

During the review period, the Group incurred a once-off charge of R39.0 million related to the Broad- Based Black Economic Empowerment (“BBBEE”) transaction concluded with Yard Investment Holdings Proprietary Limited, (“Yard”), as announced on SENS on 10 September 2019. Accordingly, the guidance below illustrates the Group’s BBBEE transaction impact on earnings per share (“EPS”) and headline earnings per share (“HEPS”) for the review period.

Six months to December 2018 Six months to December 2019 Percentage change

Excluding BBBEE charge

- Earnings per share 55.4 cents 57.6 cents to 59.3 cents 4% to 7%

- Headline earnings per share 54.7 cents 58.0 cents to 59.1 cents 6% to 8%

Including BBBEE charge

- Earnings per share 55.4 cents 54.3 cents to 56.5 cents -2% to 2%

- Headline earnings per share 54.7 cents 54.7 cents to 55.8 cents 0% to 2%

OUTLOOK

While the weak macro-economic conditions are extremely challenging and expected to persist for the foreseeable future, management remains optimistic that the Group will deliver growth for the full financial year. In the Group’s reviewed results for the year ended 30 June 2019 published on SENS on 22 August 2019, management projected that due to the high base effect, growth in the first six months of the year would likely be lower than the second six months. However, given the continuing deterioration of the economy - and the retail and construction sectors specifically - growth in the second half of the year is now anticipated to be less robust than envisaged, and more likely in line with the current review period. Notwithstanding the discouraging external environment, management remains committed to optimising on the opportunities within its control in the business to drive continued growth.

Read the full article here

27 January 2020:

Earlier today Woolworths Holdings released a sales update and voluntary trading statement for the period ending December 201. Below part of their trading statement.

VOLUNTARY TRADING STATEMENT

This voluntary trading statement is issued in terms of Section 3.4 (b) of the JSE Listings Requirements. Shareholders are advised that earnings per share (‘EPS’), headline earnings per share (‘HEPS’) and adjusted diluted HEPS for the current period are impacted by the adoption of IFRS 16. EPS and HEPS are unlikely to differ by 20% or more than the previous corresponding period. The Group will be reporting on IFRS 16 for the first time in the interim financial results of the 2020 financial year on a modified retrospective approach, with no restatement of the reported comparative prior period results. Excluding the impact of IFRS 16, in both the current and prior periods, EPS, HEPS and adjusted diluted HEPS are expected to be within the ranges reflected in the table below:

December 2018 December 2019 December 2019

reported (cents) expected range (%) expected range (cents)

EPS 197.5 -7.5% to -12.5% 172.8 to 182.7

HEPS 200.4 -7.5% to -12.5% 175.4 to 185.4

Adjusted diluted HEPS 202.9 -9.0% to -14.0% 174.5 to 184.6

Including the impact of IFRS 16 in the current period, EPS, HEPS and adjusted diluted HEPS are expected to be within the ranges reflected in the table below:

December 2018 December 2019 December 2019

reported (cents) expected range (%) expected range (cents)

EPS 197.5 -15.0% to -20.0% 158.0 to 167.9

HEPS 200.4 -15.0% to -20.0% 160.3 to 170.3

Adjusted diluted HEPS 202.9 -17.5% to -22.5% 157.2 to 167.4

CONSTANT CURRENCY INFORMATION

The constant currency information contained in this announcement has been presented to illustrate the impact of changes in the Group’s major foreign currency, the Australian dollar. In determining the constant currency turnover and concession sales growth rate, turnover and concession sales denominated in Australian dollars for the current period have been adjusted by application of the aggregated monthly average Australian dollar exchange rate for the prior period. The foreign currency fluctuations of our rest of Africa operations are not considered material, and have therefore not been applied in determining the constant currency turnover and concession sales growth rate. The aggregated monthly average Australian dollar exchange rate is R10.05 for the current period and R10.26 for the prior period.

Read the full article here

23 January 2020: Below we take a look at the latest Johannesburg Stock Exchange (JSE) trading statistics for the week ended 17 January 2020

Number of trades:

Number of trades (2020): 1 391 255

Number of trades (2019): 1 284 384

% change year on year: 8.32%

Volume traded:

Volume traded (2020): 1 659 811 000

Volume of traded (2019): 1 238 277 000

% change year on year: 34.04%

Value of trades:

Value of trades (2020): R94 273 869 000

Value of trades (2019): R81 096 030 000

% change year on year: 16.25%

Foreign purchase/selling:

Net sales/Purchases (2020): -R1 042 762 000

Net sales/Purchases (2019): -R3 650 777 000

So year to date (YTD) foreigners have been net seller/buyers:

Net sales/Purchases (2020): -R4.379 billion

Net sales/Purchases (2019): -R10.112 billion

So a year ago foreigners were net sellers of SA listed shares to the value of -R10.112 billion for the YTD while this year they have been net sellers to the tune of -R4.379 billion in the year to date (YTD). While the numbers for this is year is a lot better than the previous year the fact is that foreigners remain net sellers of SA listed stocks and they have been for most of 2019, 2018 and 2017.

Read the full article here

14 January 2020: Below we take a look at the latest Johannesburg Stock Exchange (JSE) trading statistics for the week ended 10 January 2020

Number of trades:

Number of trades (2020): 1 139 462

Number of trades (2019): 1 186 326

% change year on year: -3.95%

Volume traded:

Volume traded (2020): 1 150 825 000

Volume of traded (2019): 1 105 833 000

% change year on year: 4.07%

Value of trades:

Value of trades (2020): R68 170 319 000

Value of trades (2019): R75 162 499000

% change year on year: -9.3%

Foreign purchase/selling:

Net sales/Purchases (2020): -R3 763 134 000

Net sales/Purchases (2019): -R4 930 093 000

So year to date (YTD) foreigners have been net seller/buyers:

Net sales/Purchases (2020): -R3.630 billion

Net sales/Purchases (2020): -R6.461 billion

So a year ago foreigners were net sellers of SA listed shares to the value of -R6.461 billion for the YTD while this year they have been net sellers to the tune of -R3.630 billion in the year to date (YTD). While the numbers for this is year is a lot better than the previous year the fact is that foreigners remain net sellers of SA listed stocks and they have been for most of 2019, 2018 and 2017.

A clear sign that foreign capital is still leaving South African equities in vast amounts. This while the South African government continues to try and convince investors that South Africa is open for business. But the large scale corruption, poor government service delivery, slow economic growth, restrictive labour laws, worries about property rights, crime and general public disorder in the forms of strikes and looting are keeping potential investors away from South Africa.

JSE total market capitalisation:

Market Cap (2019): R17.770 trillion

Market Cap (2018): R12.811 trillion

% change year on year: 38.71%

So as shown in the JSE total market capitalisation above, the value of the overall market capitalisation of the stocks listed on the JSE has increased significantly over the course of the last 12 months.

Read more about the latest JSE trading statistics here

2 January 2020: We wish all our readers a very happy and prosperous new year and we hope that returns offered by the market in 2020 puts a smile on all our readers faces.

Latest trade statistics numbers released by the South African Revenue Service (SARS) shows the following.

South Africa's top 5 export destinations for November 2019:

South Africa's top 5 import origins for November 2019:

Total value of imports into and exports from South Africa for November 2019:

So for the month of November 2019, South Africa exports R6.097 billion more in goods to the rest of the world than what it imported from the rest of the world. While the economic theory dictates that a stronger local currency will hurt a country's trade balance as exports become more expensive and imports cheaper, for South Africa this is not really the case and this is partly due to the impact international commodity prices has on the value of South Africa's exports especially as a large amount of commodities is exported by South Africa. And a stronger local currency makes one of South Africa's biggest imports (crude a lot cheaper, assuming a stable crude oil price).

EARNINGS

During the review period, the Group incurred a once-off charge of R39.0 million related to the Broad- Based Black Economic Empowerment (“BBBEE”) transaction concluded with Yard Investment Holdings Proprietary Limited, (“Yard”), as announced on SENS on 10 September 2019. Accordingly, the guidance below illustrates the Group’s BBBEE transaction impact on earnings per share (“EPS”) and headline earnings per share (“HEPS”) for the review period.

Six months to December 2018 Six months to December 2019 Percentage change

Excluding BBBEE charge

- Earnings per share 55.4 cents 57.6 cents to 59.3 cents 4% to 7%

- Headline earnings per share 54.7 cents 58.0 cents to 59.1 cents 6% to 8%

Including BBBEE charge

- Earnings per share 55.4 cents 54.3 cents to 56.5 cents -2% to 2%

- Headline earnings per share 54.7 cents 54.7 cents to 55.8 cents 0% to 2%

OUTLOOK

While the weak macro-economic conditions are extremely challenging and expected to persist for the foreseeable future, management remains optimistic that the Group will deliver growth for the full financial year. In the Group’s reviewed results for the year ended 30 June 2019 published on SENS on 22 August 2019, management projected that due to the high base effect, growth in the first six months of the year would likely be lower than the second six months. However, given the continuing deterioration of the economy - and the retail and construction sectors specifically - growth in the second half of the year is now anticipated to be less robust than envisaged, and more likely in line with the current review period. Notwithstanding the discouraging external environment, management remains committed to optimising on the opportunities within its control in the business to drive continued growth.

Read the full article here

27 January 2020:

Earlier today Woolworths Holdings released a sales update and voluntary trading statement for the period ending December 201. Below part of their trading statement.

VOLUNTARY TRADING STATEMENT

This voluntary trading statement is issued in terms of Section 3.4 (b) of the JSE Listings Requirements. Shareholders are advised that earnings per share (‘EPS’), headline earnings per share (‘HEPS’) and adjusted diluted HEPS for the current period are impacted by the adoption of IFRS 16. EPS and HEPS are unlikely to differ by 20% or more than the previous corresponding period. The Group will be reporting on IFRS 16 for the first time in the interim financial results of the 2020 financial year on a modified retrospective approach, with no restatement of the reported comparative prior period results. Excluding the impact of IFRS 16, in both the current and prior periods, EPS, HEPS and adjusted diluted HEPS are expected to be within the ranges reflected in the table below:

December 2018 December 2019 December 2019

reported (cents) expected range (%) expected range (cents)

EPS 197.5 -7.5% to -12.5% 172.8 to 182.7

HEPS 200.4 -7.5% to -12.5% 175.4 to 185.4

Adjusted diluted HEPS 202.9 -9.0% to -14.0% 174.5 to 184.6

Including the impact of IFRS 16 in the current period, EPS, HEPS and adjusted diluted HEPS are expected to be within the ranges reflected in the table below:

December 2018 December 2019 December 2019

reported (cents) expected range (%) expected range (cents)

EPS 197.5 -15.0% to -20.0% 158.0 to 167.9

HEPS 200.4 -15.0% to -20.0% 160.3 to 170.3

Adjusted diluted HEPS 202.9 -17.5% to -22.5% 157.2 to 167.4

CONSTANT CURRENCY INFORMATION

The constant currency information contained in this announcement has been presented to illustrate the impact of changes in the Group’s major foreign currency, the Australian dollar. In determining the constant currency turnover and concession sales growth rate, turnover and concession sales denominated in Australian dollars for the current period have been adjusted by application of the aggregated monthly average Australian dollar exchange rate for the prior period. The foreign currency fluctuations of our rest of Africa operations are not considered material, and have therefore not been applied in determining the constant currency turnover and concession sales growth rate. The aggregated monthly average Australian dollar exchange rate is R10.05 for the current period and R10.26 for the prior period.

Read the full article here

23 January 2020: Below we take a look at the latest Johannesburg Stock Exchange (JSE) trading statistics for the week ended 17 January 2020

Number of trades:

Number of trades (2020): 1 391 255

Number of trades (2019): 1 284 384

% change year on year: 8.32%

Volume traded:

Volume traded (2020): 1 659 811 000

Volume of traded (2019): 1 238 277 000

% change year on year: 34.04%

Value of trades:

Value of trades (2020): R94 273 869 000

Value of trades (2019): R81 096 030 000

% change year on year: 16.25%

Foreign purchase/selling:

Net sales/Purchases (2020): -R1 042 762 000

Net sales/Purchases (2019): -R3 650 777 000

So year to date (YTD) foreigners have been net seller/buyers:

Net sales/Purchases (2020): -R4.379 billion

Net sales/Purchases (2019): -R10.112 billion

So a year ago foreigners were net sellers of SA listed shares to the value of -R10.112 billion for the YTD while this year they have been net sellers to the tune of -R4.379 billion in the year to date (YTD). While the numbers for this is year is a lot better than the previous year the fact is that foreigners remain net sellers of SA listed stocks and they have been for most of 2019, 2018 and 2017.

Read the full article here

14 January 2020: Below we take a look at the latest Johannesburg Stock Exchange (JSE) trading statistics for the week ended 10 January 2020

Number of trades:

Number of trades (2020): 1 139 462

Number of trades (2019): 1 186 326

% change year on year: -3.95%

Volume traded:

Volume traded (2020): 1 150 825 000

Volume of traded (2019): 1 105 833 000

% change year on year: 4.07%

Value of trades:

Value of trades (2020): R68 170 319 000

Value of trades (2019): R75 162 499000

% change year on year: -9.3%

Foreign purchase/selling:

Net sales/Purchases (2020): -R3 763 134 000

Net sales/Purchases (2019): -R4 930 093 000

So year to date (YTD) foreigners have been net seller/buyers:

Net sales/Purchases (2020): -R3.630 billion

Net sales/Purchases (2020): -R6.461 billion

So a year ago foreigners were net sellers of SA listed shares to the value of -R6.461 billion for the YTD while this year they have been net sellers to the tune of -R3.630 billion in the year to date (YTD). While the numbers for this is year is a lot better than the previous year the fact is that foreigners remain net sellers of SA listed stocks and they have been for most of 2019, 2018 and 2017.

A clear sign that foreign capital is still leaving South African equities in vast amounts. This while the South African government continues to try and convince investors that South Africa is open for business. But the large scale corruption, poor government service delivery, slow economic growth, restrictive labour laws, worries about property rights, crime and general public disorder in the forms of strikes and looting are keeping potential investors away from South Africa.

JSE total market capitalisation:

Market Cap (2019): R17.770 trillion

Market Cap (2018): R12.811 trillion

% change year on year: 38.71%

So as shown in the JSE total market capitalisation above, the value of the overall market capitalisation of the stocks listed on the JSE has increased significantly over the course of the last 12 months.

Read more about the latest JSE trading statistics here

2 January 2020: We wish all our readers a very happy and prosperous new year and we hope that returns offered by the market in 2020 puts a smile on all our readers faces.

Latest trade statistics numbers released by the South African Revenue Service (SARS) shows the following.

South Africa's top 5 export destinations for November 2019:

- China (10.1%)

- Germany (8.6%)

- United States (7.3%)

- United Kingdom (5.5%)

- India (5.1%)

South Africa's top 5 import origins for November 2019:

- China (19.2%)

- Germany (7.8%)

- United States (6.5%

- India (5.5%)

- Nigeria (5.0%)

Total value of imports into and exports from South Africa for November 2019:

- Exports: R116,902,027,397

- Imports: R110,804,693,420

- Trade Surplus/ Positive Trade Balance: R6,097,333,977

So for the month of November 2019, South Africa exports R6.097 billion more in goods to the rest of the world than what it imported from the rest of the world. While the economic theory dictates that a stronger local currency will hurt a country's trade balance as exports become more expensive and imports cheaper, for South Africa this is not really the case and this is partly due to the impact international commodity prices has on the value of South Africa's exports especially as a large amount of commodities is exported by South Africa. And a stronger local currency makes one of South Africa's biggest imports (crude a lot cheaper, assuming a stable crude oil price).