|

Related topics |

|

While one can look at the financial results of individual companies in order to determine whether to buy into a company's shares, hardly any work is done on looking at the overall financial well-being of companies within South Africa. Do foreign and/or local investors understand the company dynamics and industries in which South African companies operate? We aim to shed some light on the financial well-being of companies in South Africa.

Page was created on 31 August 2017, for Annual Financial Statistics (2015), published at the end of 2016. Please read the data disclaimer at the bottom of this page. |

We will look at a few of the more common financial ratios out there such as net profit margin, current ratio, debt to assets, debt to equity etc., and then a few we at South African Market Insights feel will provide an interesting perspective and view of the financial well-being of companies operating in South Africa. Note the charts are interactive. Click on a slice of the pie chart to update the bar chart below the pie chart. (Best viewed on Tablet, Laptop or Desktop PC).

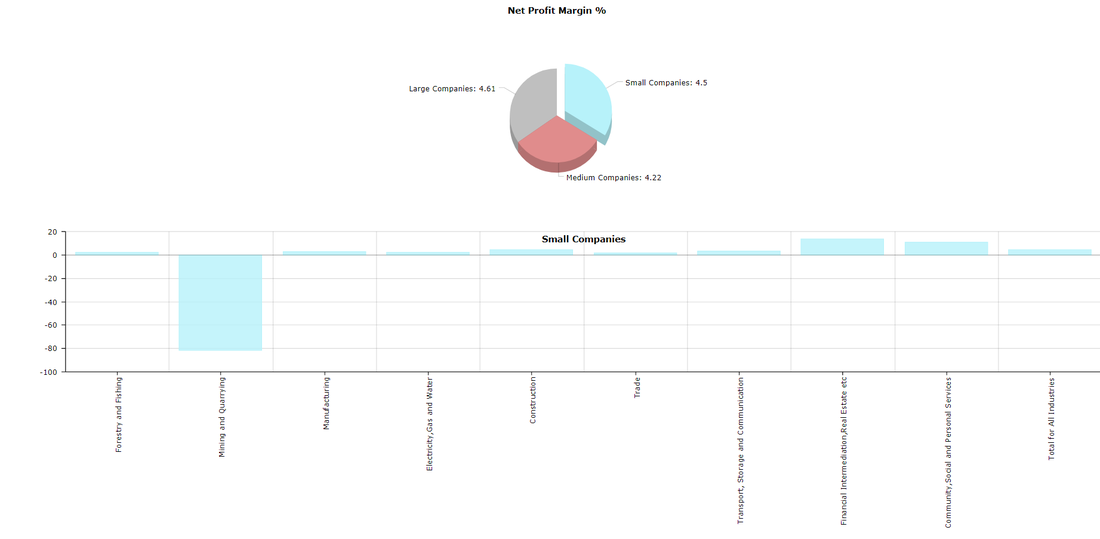

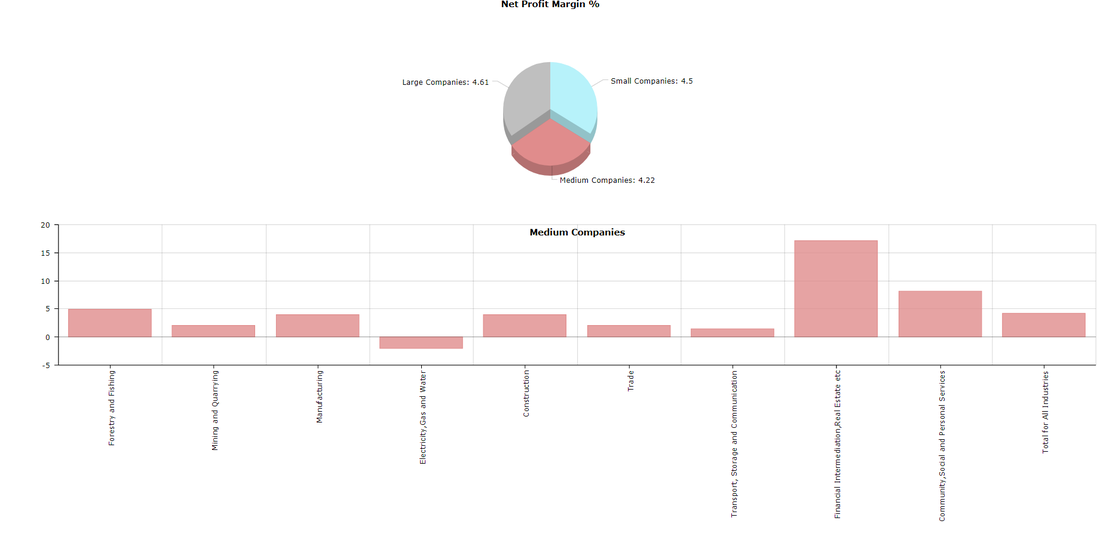

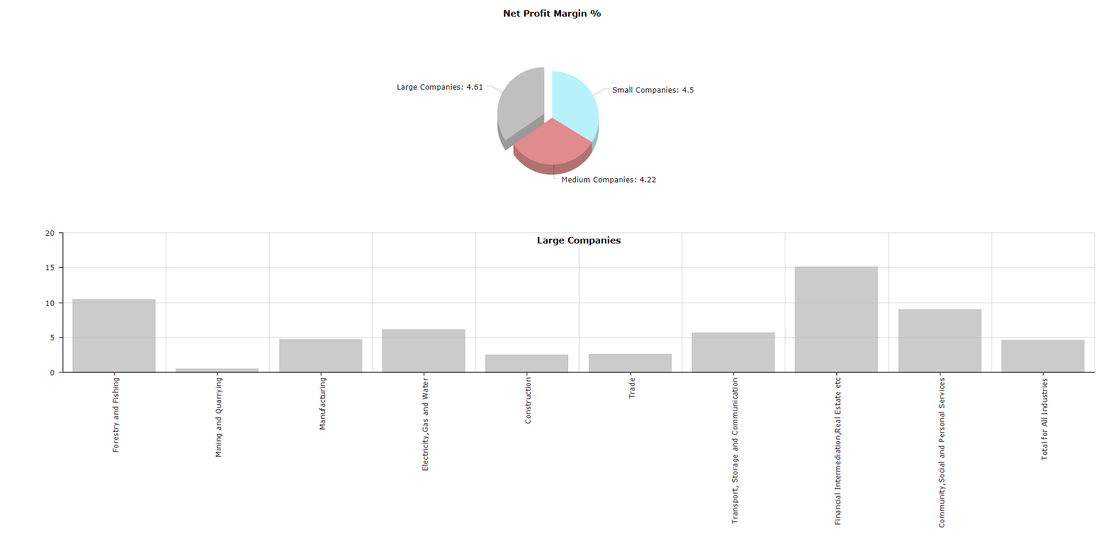

Net profit margin:

The first ratio we will look at is the net profit margin achieved by companies. Net profit margin in this case is calculated as (Net profit after taxes)/Turnover and is expressed as a percentage. The margins will be calculated for both the size of the company and the industry in which the company operates in. The pie chart shows the net profit margin achieved by firm size. Click on the pie chart and the bar chart below will show the net profit margin achieved for that specific company size operating in a various sectors of the economy. The images below shows the different profit margins per industry, depending on the company size selected in the pie chart.

Net profit margin for small companies per industry type.

|

Net profit margin for medium companies per industry type.

|

Net profit margin for large companies per industry type.

|

Large companies achieved the highest net profit margins coming in at an average of 4.6% while medium sized companies achieved the lowest net profit margin averaging 4.22%. From the graphics above its clear the most profitable industry to operate in is the financial intermediation, real estate industry, with average profit margins across the various company sizes coming in at at 15.37%

The mining and quarrying industry seems to be one of the tougher industries to operate in (with net profit margin sitting at -26% across all company sizes in this industry) but smaller companies in particular struggling showing net profit margins of -81.4% for the period in question. The medium and large sized companies barely scraped through with a profit in this industry too (with them taking away net profits of 2.07% and 0.47% respectively).

One of the bigger industries in South Africa, the Trade industry (wholesale, retail and motor trade), showed very similar net profit margins across company sizes. Net profit margin varied from 1,9% to 2.56%

The mining and quarrying industry seems to be one of the tougher industries to operate in (with net profit margin sitting at -26% across all company sizes in this industry) but smaller companies in particular struggling showing net profit margins of -81.4% for the period in question. The medium and large sized companies barely scraped through with a profit in this industry too (with them taking away net profits of 2.07% and 0.47% respectively).

One of the bigger industries in South Africa, the Trade industry (wholesale, retail and motor trade), showed very similar net profit margins across company sizes. Net profit margin varied from 1,9% to 2.56%

Turnover to Assets Ratio:

This ratio is calculated as Turnover/Total Assets and is used as a measure to show how efficiently companies are deploying assets to generate revenue. This ratio is known for varying vastly across various sectors so care should be taken when comparing industries.

Medium sized companies achieved the highest turnover to assets ratio with turnover coming in at 148.56% of total assets whereas the large companies had the lowest turnover to assets ratio, with turnover coming in at 91.73% of total assets. The Trade industry achieved by far the best turnover to assets ratio across all company sizes, but this is not surprising as retail tend to have high turnover to assets ratios. They have small asset bases yet high turnover. The turnover to assets ratio for the Trade industry averaged between 227% and 292%.

The finance, real estate etc. sector showed some of the lowest turnover to assets ratios across the various company sizes (from 29% to 48%). Reason for this is the fact that companies in this industry have a very large asset base, and therefore turnover to assets ratios are relatively small.

The finance, real estate etc. sector showed some of the lowest turnover to assets ratios across the various company sizes (from 29% to 48%). Reason for this is the fact that companies in this industry have a very large asset base, and therefore turnover to assets ratios are relatively small.

Debt to Equity Ratio:

Debt to Equity ratio is calculated as Total Liabilities/Total Equity. Debt to equity ratio is commonly used to show how leveraged/geared a company is. Essentially it shows how much suppliers, lenders and creditors have committed to the company compared to what shareholders have committed. The debt to equity ratios are usually higher (above 2) for capital intensive companies and lower (around 0.5) for less capital intensive companies. So care should be taken when comparing these ratios across industries.

From the above graphic its pretty clear that most companies are leveraged to a some extent. The smaller companies less so than the medium to large companies. The smaller companies showed an overall debt to equity ratio of 1.42, while the medium sized companies had a debt to equity ratio of 2.42 and the large companies had a debt to equity ratio of 1.98. One can think of several possible reasons why the smaller companies had the lowest debt to equity ratio and the largest firms having a lower debt to equity ratio than the medium sized firms.

The electricity,gas and water supply as well as the transport, storage and communication companies seem to be highly leveraged. The negative debt to equity ratio shown by small and medium sized mining and quarrying companies basically implies the value of their assets is worth less than what shareholders put into the company. Small forestry and fishing companies have extremely high debt to equity ratios with it hovering around 15. For medium sized companies, its the companies operating in the electricity, gas and water supply industry that has the highest debt to equity ratios, with it sitting at around 8.6

- Smaller companies do not have access to as much debt as the bigger firms (banks unwilling to borrow more to smaller firms)

- Large companies (in most cases will probably be listed on the JSE, and therefore have easy access to more equity commitments from shareholders). This is a cheap and quick way to obtain additional funding.

- The medium sized companies fall between the two scenarios mentioned above. Probably have easy access to more debt, and a smaller likelihood of being listed than the large companies and therefore not as easy access to shareholder's equity. So the easier route for these guys would be to take on more debt.

The electricity,gas and water supply as well as the transport, storage and communication companies seem to be highly leveraged. The negative debt to equity ratio shown by small and medium sized mining and quarrying companies basically implies the value of their assets is worth less than what shareholders put into the company. Small forestry and fishing companies have extremely high debt to equity ratios with it hovering around 15. For medium sized companies, its the companies operating in the electricity, gas and water supply industry that has the highest debt to equity ratios, with it sitting at around 8.6

Debt to Assets Ratio:

Debt to Assets ratio is calculated as Total liabilities/Total Assets. This, as the debt to equity ratio shows how leveraged a company is. It expresses total debt as a percentage of total assets. Basically showing the portion of assets of a company that is financed with debt. As a benchmark this value should be lower than one. The lower the ratio the better as it shows companies assets far outstrips its liabilities.

Overall the debt to assets ratio shows that for small companies close to 59% of assets is financed with debt, for medium companies their debt: assets ratio shows that almost 70% of their assets are financed with debt, and large companies debt to assets ratio shows that around 67% of large company assets are financed via debt.

As mentioned in the debt to equity analysis, there is a chance that small and medium sized mining and quarrying firms' liabilities are worth more than their assets (due to the negative debt to equity ratio), and in the case of debt to assets above it's clear that these companies liabilities are in fact worth more than their assets, to the tune of about 23% for small companies and 16% for medium sized firms. And with paper thin profit margins, liabilities outstripping their total assets, the future does look pretty bleak for small and medium sized companies involved in mining and quarrying space. Perhaps these smaller (and loss making) operations will be bought up by the bigger and financially healthier firms in the industry?

In a similar trend to the debt to equity ratio, the smallest companies had the lowest debt to assets ratio (again likely due to the fact that these companies would find it harder to obtain access to credit than larger companies), and the large companies the second lowest ratio and medium sized companies the highest debt to assets ratio. Confirm what debt to equity ratio suggested, that the smallest firms are least geared and the medium sized firms being the highest geared.

As mentioned in the debt to equity analysis, there is a chance that small and medium sized mining and quarrying firms' liabilities are worth more than their assets (due to the negative debt to equity ratio), and in the case of debt to assets above it's clear that these companies liabilities are in fact worth more than their assets, to the tune of about 23% for small companies and 16% for medium sized firms. And with paper thin profit margins, liabilities outstripping their total assets, the future does look pretty bleak for small and medium sized companies involved in mining and quarrying space. Perhaps these smaller (and loss making) operations will be bought up by the bigger and financially healthier firms in the industry?

In a similar trend to the debt to equity ratio, the smallest companies had the lowest debt to assets ratio (again likely due to the fact that these companies would find it harder to obtain access to credit than larger companies), and the large companies the second lowest ratio and medium sized companies the highest debt to assets ratio. Confirm what debt to equity ratio suggested, that the smallest firms are least geared and the medium sized firms being the highest geared.

Current Ratio:

The current ratio is calculated as current assets/current liabilities. This ratio is a liquidity measure that shows how easily companies can service their current debts with their current assets. A current ratio of less than one shows a company's current liabilities is greater than its current assets. I.e it would be unable to pay off all of its obligations with its current assets, if things were to come to that point. As a bare minimum this value should be greater than one.

Small companies have the highest current ratio (coming in at an average of 1.54), with the large companies having the lowest current ratio (coming in at 1.03). The mining and quarrying industry as well as the transport and storage industries has a current ratio of less than 1 for all company sizes. Showing that they will not be able to meet their current obligations with their available current assets. Which basically implies these companies will need cash injections from shareholders (as we have seen recently mining companies have issued a number of rights offers to try and get money from shareholders, or start selling off long term assets to service current debts).

They need to do this as the chances of banks borrowing them more money is very slim as they can't even meet their current debts, so taking on more debt is not an option. This just highlights the financial state these companies are in.

The manufacturing, construction and trade industries all have pretty healthy current ratios across all company sizes.

They need to do this as the chances of banks borrowing them more money is very slim as they can't even meet their current debts, so taking on more debt is not an option. This just highlights the financial state these companies are in.

The manufacturing, construction and trade industries all have pretty healthy current ratios across all company sizes.

Return on Equity (ROE):

Return on equity is calculated as net profit/total equity. This is expressed as a percentage and shows the percentage of net income generated with money shareholders have invested. (I.e how much Rand profits are generated for every x amount invested by shareholders). For example if ROE is 16, then the company generates R16 net profits for every R100 invested by shareholders. As benchmark the ROE value should be at least 3% higher than the money market interest rate (to compensate investors for the risk of investing in a company instead of just keeping his money in the money market.

Highest ROE is achieved by the small companies with their average ROE sitting at 15.06% while large firms had the lowest ROE, with it averaging just 6%. Readers should ignore the strong ROE showed for mining and manufacturing. Reason for it's strong numbers is the fact that both the net profits and equity were negative, and mathematics negative divided by negative makes a positive.

Forestry and fishing as well as community, social and personal services showed strong ROE numbers. With the ROE numbers for forestry and fishing amounting to the following:

Small: 43.06%

Medium: 20.09%

Large: 10:55%

And for community, social and personal services the ROE numbers are as follows:

Small: 30.6%

Medium: 27.4%

Large: 23.6%

Forestry and fishing as well as community, social and personal services showed strong ROE numbers. With the ROE numbers for forestry and fishing amounting to the following:

Small: 43.06%

Medium: 20.09%

Large: 10:55%

And for community, social and personal services the ROE numbers are as follows:

Small: 30.6%

Medium: 27.4%

Large: 23.6%

Return on Assets (ROA):

Return on assets is calculated as net profit/total assets. This is expressed as a percentage and shows the percentage of net income generated by their total assets. (I.e how much Rand profits are generated for every x amount held in assets). For example if ROA is 10, then the company generates R10 net profits for every R100 in assets its holds.

The ROA is substantially lower than the ROE, basically showing that company assets are far larger than shareholder equity. The highest ROA is achieved by small companies. With small company ROA averaging 6.23%, while the lowest ROA is achieved by the large companies, with their ROA only averaging 2.01%.

Forestry and fishing and Trade industries showed very similar ROA's across the various company sizes. Trade sector ROA's achieved across company sizes shown below.

Small: 5.24%

Medium: 6.24%

Large: 3.68%

ROA for companies active in the community, social and personal care industries are pretty high (with the exception of medium sized firms) with them showing the following ROA.

Small: 17.16%

Medium: 2.9%

Large: 9.98%

Forestry and fishing and Trade industries showed very similar ROA's across the various company sizes. Trade sector ROA's achieved across company sizes shown below.

Small: 5.24%

Medium: 6.24%

Large: 3.68%

ROA for companies active in the community, social and personal care industries are pretty high (with the exception of medium sized firms) with them showing the following ROA.

Small: 17.16%

Medium: 2.9%

Large: 9.98%

Employee Costs as Percentage of Total Expenditure:

This measure expresses the cost of employees as a percentage of total expenditure. The aim is to show how big a part of total expenditure of the business is made up by its staffing costs. This is a metric that shows just how big a part staff costs makes up of smaller firms total expenditure. And one of the biggest stumbling blocks for smaller businesses, is the fact that staffing is expensive, and if you want good quality staff you have to pay staff what larger firms would offer them.

From the graphics above its clear as the size of the company increases, the lower the employee costs become as percentage of overall expenditure. For small companies, employee costs makes up 19.72% of overall expenditure, for medium sized companies this falls to 13.64% and for large companies the employee costs makes up 11.97% of overall expenditure. The community, social and personal services industry have the highest spending on staffing as percentage of overall expenditure with the percentage spent on staffing looking as follows:

Small: 17.16%

Medium: 30.16%

Large: 37.89%

While the Trade industry's employee cost as percentage of total expenditure is a lot lower and is shown below:

Small: 11.89%

Medium: 8.2%

Large: 7,12%

So when trouble comes knocking at the door of a small company, the easiest way to cut back on spending is letting staff go, as this forms a big part of their overall expenditure, while the large firms might have some room to maneuver and cut spending elsewhere before having to let staff go as their overall spending (in percentage terms) on personal is far lower than that of the small companies.

Small: 17.16%

Medium: 30.16%

Large: 37.89%

While the Trade industry's employee cost as percentage of total expenditure is a lot lower and is shown below:

Small: 11.89%

Medium: 8.2%

Large: 7,12%

So when trouble comes knocking at the door of a small company, the easiest way to cut back on spending is letting staff go, as this forms a big part of their overall expenditure, while the large firms might have some room to maneuver and cut spending elsewhere before having to let staff go as their overall spending (in percentage terms) on personal is far lower than that of the small companies.

Cash as percentage of Total Assets:

Cash as percentage of Total Assets is calculated as Cash/Total Assets, expressed as a percentage. This shows what percentage of a company's assets is held in the form of cash. One would assume the higher the percentage of assets held in cash the more conservative the company is. I.e the company is keeping cash in reserve in case unexpected expenses arise. Or it might show the lack of investment opportunities, or failure of companies management to spot investment opportunities and acquire assets.

Small companies have the highest Cash as percentage of Total Assets with an average of 12.26% of their assets held in cash, medium sized companies hold on average 9.75% of assets in cash, and large companies hold on average of only 5.69% of assets in cash.

Companies active in the Community, social and personal services industry keeps a large amount of their assets in cash (with the percentage ranging from 13.3% to 15.97% (depending on company size). Another industry that has a pretty high percentage of assets in cash is the Construction industry with it ranging from 11.2% to 16.6% (depending on company size).

While it was mentioned earlier the higher the ratio the more likely it is that the company is being conservative, on the flip side, a very low ratio might indicate that a company does not have a lot of cash reserves as its running out of money trying to stay afloat.

Companies active in the Community, social and personal services industry keeps a large amount of their assets in cash (with the percentage ranging from 13.3% to 15.97% (depending on company size). Another industry that has a pretty high percentage of assets in cash is the Construction industry with it ranging from 11.2% to 16.6% (depending on company size).

While it was mentioned earlier the higher the ratio the more likely it is that the company is being conservative, on the flip side, a very low ratio might indicate that a company does not have a lot of cash reserves as its running out of money trying to stay afloat.

Trade and Other Receivables as Percentage of Total Assets:

Trade and other receivables as percentage of total asset is calculated as Trade and Other receivables /Total assets expressed as a percentage. This metric shows what percentage of a firm's total assets is in the form of money owed to them. The higher this percentage the more concerned one should be as no company would like to have a large portion of their assets sitting in someone else's hands. Could point to clients struggling to pay the company, or that the company's debt collection processes are not very effective.

Large companies have the lowest percentage of assets being held in the form of Trade and Other Receivables with it averaging 12.16%, while medium sized companies average 19.34% and for small companies it's at 16.98%. It must be rather concerning for medium sized companies that a fifth of their total assets is money owed to them. It is not surprising to see large firms have the lowest ratio (in contrast to last year's financial ratios), when times get tough, the tough gets going and we are sure large firms focussed on debt collection over recent years in order to ensure money due to them gets back to them faster than it has in the past.

Companies in the Trade and Manufacturing industries have pretty high percentage of assets held in the form of trade and other receivables across all company sizes. So investors buying shares of companies involved in this industry should keep in mind that a fair chunk of these companies assets are actually money that's owed to them.

Companies in the Trade and Manufacturing industries have pretty high percentage of assets held in the form of trade and other receivables across all company sizes. So investors buying shares of companies involved in this industry should keep in mind that a fair chunk of these companies assets are actually money that's owed to them.

Trade and Other Payable's as Percentage of Total Liabilities:

Trade and Other Payables as percentage of Total Liabilities is calculated as Trade and Other Payables /Total Liabilities expressed as a percentage. This metric shows what percentage of a company's total liabilities is made up by money it owes to suppliers of goods and services

The trade and other payables as percentage of overall liabilities is higher per company size, than the percentage of total assets made up by trade and other receivables.

Large companies have the lowest percentage of liabilities being made up in the form of trade and other payables with it averaging 22.6%, while medium sized companies average 28.24% and small companies 23.23%.

Trade and Manufacturing industries have very high trade and other payables as percentage of total liabilities, across all company sizes. As was the case with their trade and other receivables as percentage of total assets. Clearly the norm of these industries are to have a large percentage of assets made up by money owed to you and one of your largest liabilities is money owed to service providers and suppliers.

Large companies have the lowest percentage of liabilities being made up in the form of trade and other payables with it averaging 22.6%, while medium sized companies average 28.24% and small companies 23.23%.

Trade and Manufacturing industries have very high trade and other payables as percentage of total liabilities, across all company sizes. As was the case with their trade and other receivables as percentage of total assets. Clearly the norm of these industries are to have a large percentage of assets made up by money owed to you and one of your largest liabilities is money owed to service providers and suppliers.

Data disclaimer:

Data used is obtained from the 2015 Annual Financial Statistics (AFS) published by Statistics South Africa. The companies sampled from year to year might differ substantially, therefore care should be taken when trying to compare statistics over time and when making inferences on a specific industry as the companies sampled (though selected to ensure the industry is accurately represented), financial positions might not represent the financial position of all companies in a specific industry. The statistics shown and commented on is based solely on the AFS 2015 data as published by Statistics South Africa.

Data Source: AFS 2015 as published by Statistics South Africa

Data used is obtained from the 2015 Annual Financial Statistics (AFS) published by Statistics South Africa. The companies sampled from year to year might differ substantially, therefore care should be taken when trying to compare statistics over time and when making inferences on a specific industry as the companies sampled (though selected to ensure the industry is accurately represented), financial positions might not represent the financial position of all companies in a specific industry. The statistics shown and commented on is based solely on the AFS 2015 data as published by Statistics South Africa.

Data Source: AFS 2015 as published by Statistics South Africa