|

Related Topics |

|

This page will provide readers with more details regarding South Africa's Food and Beverages Sector. We will take a more detailed look at the various income sources for Restaurants and Coffee Shops, Fast Food and Take-Away outlets, and Catering services (which includes pubs and canteens). The image below provides a taster of the type of information available on this page using the interactive graphics.

|

Note the page will be updated on an ad hoc basis as more information with regards to the food and beverages sector in South Africa becomes available.

|

23 March 2020: Impact on Coronavirus on South Africa's Food and Beverages Industry

In coming days we will publish our estimates of the potential impact the Coronavirus and the strict government restrictions on number of clients allowed in restaurants and bars will have the industry. And from initial trade we observed over the weekend the impact will be significant and we predict that a large number of smaller bars and restaurants will close their doors permanently after this is all over as they wont have enough cash reserves to ride out the troubled times ahead.

Government is set to release the rules pertaining to the lockdown and who is allowed to operate and work, and how this is scheduled to take place. If fast food companies and restaurants cannot operate during during this time period we predict that a large number of smaller take-away, fast foods and restaurants will have to permanently close their doors after the lockdown period is over.

Government is set to release the rules pertaining to the lockdown and who is allowed to operate and work, and how this is scheduled to take place. If fast food companies and restaurants cannot operate during during this time period we predict that a large number of smaller take-away, fast foods and restaurants will have to permanently close their doors after the lockdown period is over.

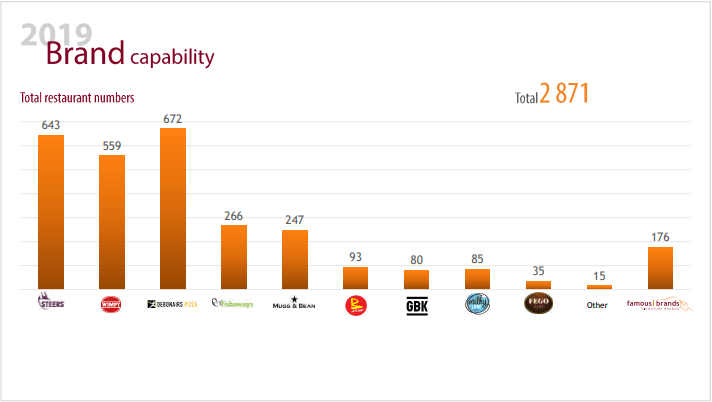

30 May 2019: Famous Brands latest results shows they have 2402 stores in SA

Famous Brands, which owns fast food and casual dining brands such as Steers, Wimpy, Debonairs, Mugg & Bean, FishAways etc, latest financial results showed they they have 2402 outlets open in South Africa as at end of February 2019. The largest contributor to their 2 402 stores is Debonairs, with the pizza brand having 672 stores (not all necessarily in South Africa though as some might be outside the borders of South Africa). The image below shows the number of stores Famous Brands have open for the bulk of their brands (note it includes all stores across the world and not only the 2 402 stores in South Africa).

In total the group has the following number of stores open for their various brands as at end February 2019:

- Steers: 643

- Wimpy: 559

- Debonairs: 672

- FishAways: 266

- Mugg & Bean: 247

- Gourmet Burger Kitchen (UK): 80

- Fego: 35

27 May 2019: Pondering National Wine Day

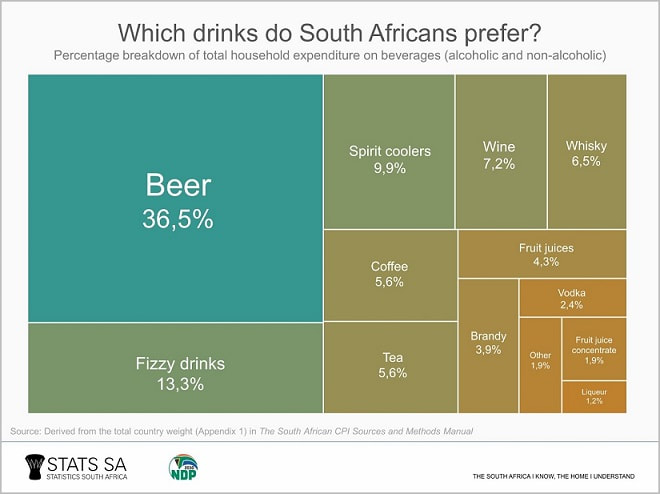

We take a look at an article published on Statistics South Africa (Stats SA) website in which they take a look at a few fun facts regarding South Africa's beverages spending (this includes alcoholic and non-alcoholic beverages spending). A

Article Starts

25 May is National Wine Day! Here are a few fun facts to muse over if you’re planning to enjoy a glass or three.

SA households spend more on wine than on coffee

South Africans have clear priorities when it comes to drink. Wine takes up 7,2% of total household expenditure on alcoholic and non-alcoholic beverages, according to Stats SA’s inflation basket. This places wine in fourth place as the most popular beverage that households spend money on. Beer is the clear winner, taking up over a third of household spending on beverages, followed by fizzy drinks and spirit coolers. Whisky follows wine in fifth place (see image below):

Article Starts

25 May is National Wine Day! Here are a few fun facts to muse over if you’re planning to enjoy a glass or three.

SA households spend more on wine than on coffee

South Africans have clear priorities when it comes to drink. Wine takes up 7,2% of total household expenditure on alcoholic and non-alcoholic beverages, according to Stats SA’s inflation basket. This places wine in fourth place as the most popular beverage that households spend money on. Beer is the clear winner, taking up over a third of household spending on beverages, followed by fizzy drinks and spirit coolers. Whisky follows wine in fifth place (see image below):

Coffee,, the darling of beverage-related internet memes, is tie with tea, taking up 5,6% of household spending on drinks. That’s in sixth place. Siestog. Wine’s 7,2% can be further broken down into red (3,9%) and white (3,2%). As a nation, it seems we are slightly more partial to red wine over white.2

Wait for it … wine is the most expensive in Western Cape

Maybe it’s not that much of a surprise, as Western Cape is the hub of the wine industry in South Africa. The most recent data show that the average price of a 750 ml bottle of red wine will set you back R88,50 in that province, higher than the national average of R64,38.3

Wait for it … wine is the most expensive in Western Cape

Maybe it’s not that much of a surprise, as Western Cape is the hub of the wine industry in South Africa. The most recent data show that the average price of a 750 ml bottle of red wine will set you back R88,50 in that province, higher than the national average of R64,38.3

If you’re feeling a little contrarian to the popularity of red wine and choose to drink the alternative, Western Cape is also the most expensive in terms of white wine (R70,44 for a bottle). KwaZulu-Natal is the second most expensive province for both red and white varieties. Wine is notably cheaper in other provinces. As you work down the price lists above, you can’t help wondering whether other provinces prefer the “cardboardeaux” over the bottled variety. But we’re not judging…

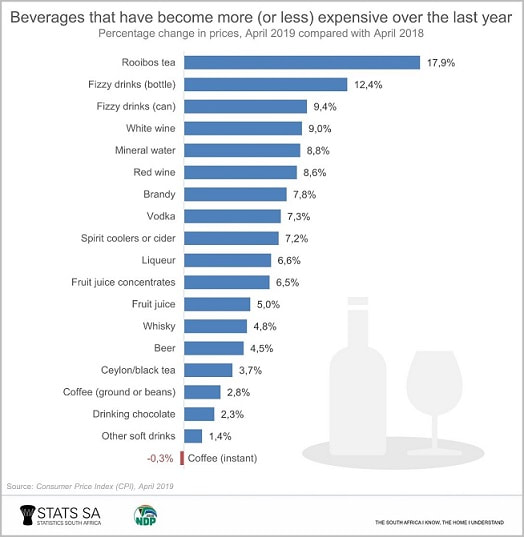

Wine prices have risen over the last year, but not as quickly as rooibos

Inflation data show that red and white wine prices have risen over the last 12 months, but not as much as fizzy drinks and rooibos tea. You are paying, on average, 8,6% more for a bottle of red wine than you did a year ago. White wine prices have risen by 9,0%.. Rooibos drinkers in particular have had a rough time, with prices for the tea jumping by 17,9% in the twelve months to April. The rooibos industry is currently recovering from a four-year drought that has constrained supply, contributing to the rise in prices.

Wine prices have risen over the last year, but not as quickly as rooibos

Inflation data show that red and white wine prices have risen over the last 12 months, but not as much as fizzy drinks and rooibos tea. You are paying, on average, 8,6% more for a bottle of red wine than you did a year ago. White wine prices have risen by 9,0%.. Rooibos drinkers in particular have had a rough time, with prices for the tea jumping by 17,9% in the twelve months to April. The rooibos industry is currently recovering from a four-year drought that has constrained supply, contributing to the rise in prices.

Wine prices have risen faster than the prices of other alcoholic beverages such as brandy, vodka, whisky and beer. At the end of the day, the price may be a secondary consideration if you’re a fan of wine. National Wine Day presents an opportunity for you to join all other wine fanciers to celebrate this culturally important drink. Enjoy responsibly!

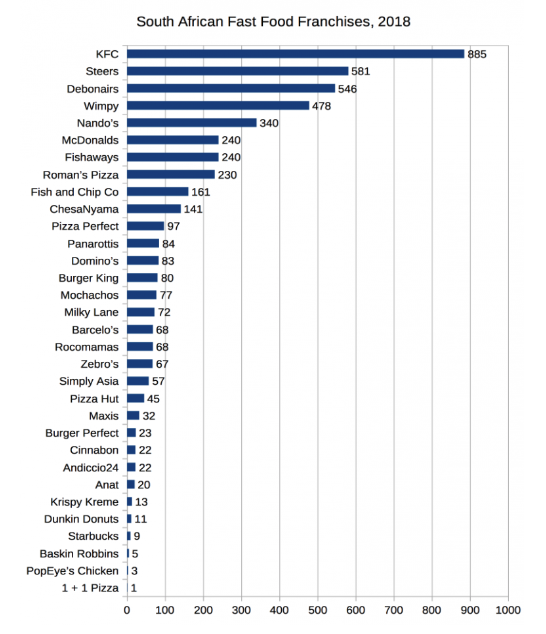

7 May 2019: Most popular fast food franchises in South Africa

So have you ever wondered what the most popular fast food franchise in South Africa is? Or how many KFC shops there are in South Africa? Or how many Steers, Rocomamas or Wimpy's there are in South Africa? Well this type of information is hard to come by and to collect, but according to an article in BusinessTech which was published in July 2018 the most popular fast food franchise in South Africa by far is KFC, with it having 300 more stores open than Steers for example. The image below as published by BusinessTech shows the number of outlets as at July 2018 according to the information they collected.

So based on the bar chart above the summary below shows the number of fast food outlets per brand in South Africa:

The original article can be found here.

- KFC: 885

- Steers: 581

- Debonairs: 546

- Wimpy: 478

- Nando's: 340

- Mcdonalds: 240

- Fishaways: 240

- Romans's Pizza: 230

- Fish and Chips co: 161

- ChesaNyama: 141

The original article can be found here.

25 March 2019: Income earned per outlet type per income category for January 2019

The bar chart below takes a look at the latest numbers published by Statistics South Africa (Stats SA) regarding South Africa's food and beverages sector. It breaks income earned in January 2019 down per outlet type and for the various income categories such as: Food sales, bar sales (includes non-alcoholic and alcoholic beverages) and other income (such as cigarette and other vending machines, any other items not classified under food or bar sales.

So restaurants and coffee shops earned more income from food sales for the month of January 2019 than Take-away and fast food outlets, with the former earning R2.684 billion and the latter coming in with R2,1 billion in income earned from Food sales. It is no real surprise that Catering services (which includes pubs, bars and taverns) earn the most under "Other income" as people are more likely to be buying cigarettes or other items such as shirts for example from bars, pubs and taverns than what they are buying it from restaurants and take-away establishments.

The summary below shows the income earned per income category per outlet type:

The summary below shows the income earned per income category per outlet type:

- Income from food sales : Restaurants and coffee shops: R 2 684 200 000

- Income from food sales : Take-away and fast food outlets: R 2 101 800 000

- Income from food sales : Catering services: R 660 200 000

- Income from bar sales : Restaurants and coffee shops: R 259 800 000

- Income from bar sales : Take-away and fast food outlets: R 7 600 000

- Income from bar sales : Catering services: R 42 900 000

- Other income : Restaurants and coffee shops: R 12 000 000

- Other income : Take-away and fast food outlets: R 700 000

- Other income : Catering services: R 63 300 000

22 January 2019: Income earned over time per outlet type

Is it starting to feel like you don't actually go out and have a few drinks at the local pub after a long work week like you used to do in the past? Well based on the income earned by the various food and beverages outlet types it looks like the catering services category (which includes bars and pubs) is earning less and less income over time.

The line graph below shows the monthly total income earned by the various food and beverages outlet type on a monthly basis. Note the numbers in the graphic below has been adjusted for inflation.

The line graph below shows the monthly total income earned by the various food and beverages outlet type on a monthly basis. Note the numbers in the graphic below has been adjusted for inflation.

In January 2008, catering services contributed 17.91% of the total income earned by the industry. Based on the numbers for November 2018, catering services now contribute only 13.23% of total income earned by the industry. A clear sign that bars and pubs are frequented less often than it used to be in the past. Is it because consumers are under continued financial pressure and dont have the money to go out for drinks? Perhaps. But in today's world most restaurants offer a wide variety of beers, gins and wines, so instead of going for drinks and then going out for supper, people combine the two into one.

In January 2008, restaurants and coffee shops contributed 56.5% of total income earned by the industry. By November 208 they contributed just under 50% of total income earned by the industry. Fast food and take-aways contributed 25.6% of total income earned by the industry in January 2008. By November 2018 the Fast food and take-away outlets contributed 36.0% of total income earned by the industry. So in summary, people tend to go to bars and pubs less while they spend more on take-aways.

In January 2008, restaurants and coffee shops contributed 56.5% of total income earned by the industry. By November 208 they contributed just under 50% of total income earned by the industry. Fast food and take-aways contributed 25.6% of total income earned by the industry in January 2008. By November 2018 the Fast food and take-away outlets contributed 36.0% of total income earned by the industry. So in summary, people tend to go to bars and pubs less while they spend more on take-aways.

9 January 2019: Employment in the Hotels and Restaurants industry in South Africa

In today's update we take a look at the formal employment numbers in the Hotels and Restaurants industry as estimated by Statistics South Africa's quarterly employment statistics survey. Sadly it groups Hotels and Restaurants together so a more detailed breakdown of employment per food outlet type does not exist, or as not being published at least.

The line chart below shows the total number of formal employees in the hotels and restaurants industry in South Africa per quarter since September 2009.

The line chart below shows the total number of formal employees in the hotels and restaurants industry in South Africa per quarter since September 2009.

As at September 2018 there were 268 299 people working in the Hotels and restaurants industry in South Africa, up from 189 925 people working in the industry 9 years ago. That is total growth in employment in this industry of 78 374 employees,or growth of 41.27% in employment in the industry in the last 9 years. No wonder government keeps punting and pushing the Tourism industry as a major source and driver of future employment in South Africa.

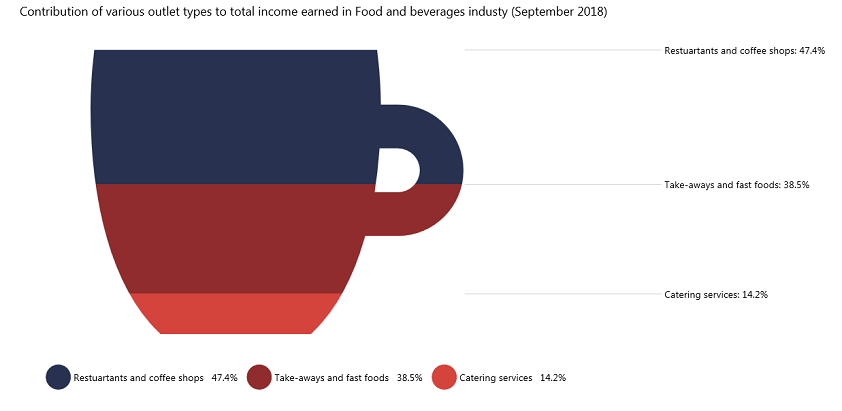

27 November 2018: Contribution of the various outlet types to total income earned in September 2018

The image below shows the relative contribution of the major food and beverage outlet types to total income earned by the industry during September 2018 (At 2015 constant prices, I.e adjusted for inflation)

Restaurants and coffee shops were clearly the biggest contributors to total income during September 2018. We suspect that this contribution might decline during the holiday period as more people make use of take aways and enjoy a few drinks at a bar or pub (which falls under catering services). It will be interesting to see what impact the holiday season has on the relative contribution of the outlet types to total income: Below a summary of the relative contribution to income earned in September 2018:

- Restaurants and coffee shops: 47.4%

- Take-aways and fast foods: 38.5%

- Catering services: 14.2%

20 November 2018: The year on year growth in income earned by various food and beverages outlet types

In today's update we take a look at the year on year growth rates of income earned (after adjusting for inflation and seasonal effects) of the various food and beverages outlet types as well as for the industry as a whole.

From the graphic above it is clear that the catering services category (which includes bars and pubs) has been struggling for a while now, with their year on year growth rates being negative for most months since the start of 2017. Other than that it has been a relatively mixed bag for Restaurants and coffee shops, Take-away and fast food outlets as well as the total industry. Since the start of 2017, the average year on year growth achieved by the various outlet types are as follows:

- Restaurants and coffee shops: 1.5%

- Take-away and fast food outlets: 2.5%

- Catering services: -3%

- Total Food and Beverages Industry: 1.2%

21 August 2018: Total income from food and beverages sector since 2008

The line graph below shows the total income earned by the Food and Beverages industry per month, since the start of 2008. And readers can see that the income earned (after income has been adjusted for inflation) has been pretty flat over the last 10 years. It is no real surprise then that the shares of listed food and beverages stocks such as Spur and Famous Brands have been struggling over the last couple of years. As after inflation there is no real growth in the industry. Its just spinning its wheels, just like South Africa's economy. As South African consumers do not have the means to spend more money on dining at restaurants or eating fast foods and take-aways.

Our prediction is that the industry will continue to plot along at the current trend for years to come, until South Africa's economy finds a way to create jobs, increase the overall level of wealth of South Africans and South African consumers have more free cash available to spend on "luxuries" such as eating out and getting regular fast foods. With South Africans being heavily indebted this might take a very long time. The average income earned by the industry per year is shown below:

Currently the monthly income by the food and beverages sector amounts to R4.56 billion a month. A far cryfrom the R4.76 billion a month it earned in 2008 before the financial crisis hit.

- 2008: R 4 755 725 000

- 2009: R 4 348 725 000

- 2010: R 4 371 450 000

- 2011: R 4 337 333 333

- 2012: R 4 381 275 000

- 2013: R 4 405 658 333

- 2014: R 4 347 400 000

- 2015: R 4 400 100 000

- 2016: R 4 444 191 667

- 2017: R 4 476 991 667

- 2018: R 4 559 416 667

Currently the monthly income by the food and beverages sector amounts to R4.56 billion a month. A far cryfrom the R4.76 billion a month it earned in 2008 before the financial crisis hit.

21 May 2018: Income from bar sales for Food and Beverages Sector relatively flat

In today's update we look at the total income earned by the Food and beverages from bar sales. This includes the sales of coffee and tea, cold drinks, and of course alcohol. Note we are looking at the total industry growth (so figures from bars, pubs and taverns are included in the graphic below.

The graphic above represents the year on year growth in constant prices (after sales figures have been adjusted for inflation) and after we applied a 12 month moving average to the growth rate to best identify the underlying trend in the monthly sales data, which even after seasonal adjustment remained relatively volatile.

As the graphic above shows the growth from bar sales in recent months has been flat for basically the last two years, with no significant upward momentum in the income from bar sales to speak of. Again just showing how hard it has been for the industry, in particular small coffee shops and pubs, with a large number of them closing down in the recent past. Even big franchise brands such as Famous Brands (which owns Mugg and Bean, Steers, Fishaways, Tashas, Turn 'n Tender, Keg etc) has been under significant pressure for the last couple of years, as their profit margins drop due to declining consumer spending, increased competition from a smaller target market and increasing costs.

This is not a time to be opening a pub or coffee shop, unless its concept is strong and unique enough to set it apart from the competition.

As the graphic above shows the growth from bar sales in recent months has been flat for basically the last two years, with no significant upward momentum in the income from bar sales to speak of. Again just showing how hard it has been for the industry, in particular small coffee shops and pubs, with a large number of them closing down in the recent past. Even big franchise brands such as Famous Brands (which owns Mugg and Bean, Steers, Fishaways, Tashas, Turn 'n Tender, Keg etc) has been under significant pressure for the last couple of years, as their profit margins drop due to declining consumer spending, increased competition from a smaller target market and increasing costs.

This is not a time to be opening a pub or coffee shop, unless its concept is strong and unique enough to set it apart from the competition.

24 April 2018: Contributions to Food and Beverages Sector Income for Feb 2018

The pie chart below takes a look at the contribution of the various outlet types (Restaurants and Coffee shops, Take-aways and fast food and lastly catering services (including bars and pubs) and their various income streams (food sales, bar sales and other income, such as cigarette sales) and each's outlet/income stream types contribution to income earned in the Food and Beverages sector in February 2018

As the pie chart above shows, income earned in the food and beverages sector in South Africa is dominated by Income from food sales of Restaurants and coffee shops, with it making up almost 45% of all income earned in the sector. The second biggest income generator is income earned from food sales from Take-away and Fast food outlets, with it generating just over 35% of income earned in the industry in February 2018. Catering services food sales came in a distant 3rd place in terms of income generated in this sector with it earning just under 11% of the income in the food and beverages sector in February 2018.

When looking at the income earned for the industry as a whole the below provides a a summary of the growth in income earned for February 2018, compared to that of February 2017:

The above shows that the industry is clearly under significant pressure, with income earned in the sector in total only growing by 1.2% compared to the figures of a year ago. While bar sales (alcoholic and non alcoholic drinks) showed stronger growth, of 2.6% compared to the year before, it remains a very weak number considering inflation for the period was sitting at 4.4%. This income earned in this sector is well below inflation, suggesting profit margins are being eaten into in this industry, making stocks such as Famous Brands (FBR), Spur (SUR) and Taste (TAS) less attractive investments on the JSE.

From these numbers, we suspect more people are choosing to rather eat in at home and make their own food instead of going out to grab something to eat. A clear sign of struggling times for South African consumers.

When looking at the income earned for the industry as a whole the below provides a a summary of the growth in income earned for February 2018, compared to that of February 2017:

- Income from food sales: 1.2%

- Income from bar sales : 2.6%

- Other income : -7.5%

- Total income : 1.2%

The above shows that the industry is clearly under significant pressure, with income earned in the sector in total only growing by 1.2% compared to the figures of a year ago. While bar sales (alcoholic and non alcoholic drinks) showed stronger growth, of 2.6% compared to the year before, it remains a very weak number considering inflation for the period was sitting at 4.4%. This income earned in this sector is well below inflation, suggesting profit margins are being eaten into in this industry, making stocks such as Famous Brands (FBR), Spur (SUR) and Taste (TAS) less attractive investments on the JSE.

From these numbers, we suspect more people are choosing to rather eat in at home and make their own food instead of going out to grab something to eat. A clear sign of struggling times for South African consumers.

20 November: Numbers on the Food and Beverages Sector from AFS2016

In the latest Annual Financial Statistics (AFS) published by Statistics South Africa the following numbers pertain to the Food and Beverages Industry in South Africa.

Income Items:

Turnover: R60.9billion

Royalties, Franchise Fees, copyrights and trademarks: R346million

Interest: R171million

Total Income: R61.95billion

Expenditure Items:

Purchases: R31.3billion

Advertising: R585million

Employment Costs: R12.46billion

Income Tax: R409million

Royalties, franchise fees, copyright, trade names, trademarks and patent rights: R1.635billion

Containers and packaging materials : R358million

Total Expenditure: R60.29billion

From the above it is clear that Total Income of R61.95billion is not a lot more than total expenditure of R60.3billion, signalling very thin profit margins in the industry. This might be due to strong competition in the market or depressed consumer spending in the current economic climate.

Income Items:

Turnover: R60.9billion

Royalties, Franchise Fees, copyrights and trademarks: R346million

Interest: R171million

Total Income: R61.95billion

Expenditure Items:

Purchases: R31.3billion

Advertising: R585million

Employment Costs: R12.46billion

Income Tax: R409million

Royalties, franchise fees, copyright, trade names, trademarks and patent rights: R1.635billion

Containers and packaging materials : R358million

Total Expenditure: R60.29billion

From the above it is clear that Total Income of R61.95billion is not a lot more than total expenditure of R60.3billion, signalling very thin profit margins in the industry. This might be due to strong competition in the market or depressed consumer spending in the current economic climate.

2 November 2017: Income per outlet type per category

The bar chart below shows the amount of income earner per category, per Food and Beverages outlet type for the full year of 2015. Data obtained from Statistics South Africa.

It is clear that in 2015, restaurants and coffee shops earned more income from Food and Snacks sales as well as the sales of non-alcoholic beverages than takeaway and fast-food outlets. Interesting to note that when it comes to alcoholic beverages the takeaway and fast-food outlets earned hardly any income from it, while restaurants and coffee shops as well as canteens (which includes pubs and bars earned a fair amount of their income from the sale of alcoholic beverages). The above shows that while takeaway and fast-food outlets are extremely popular, sit down restaurants and coffee shops is still a bigger contributor to the South African food and beverages industry.

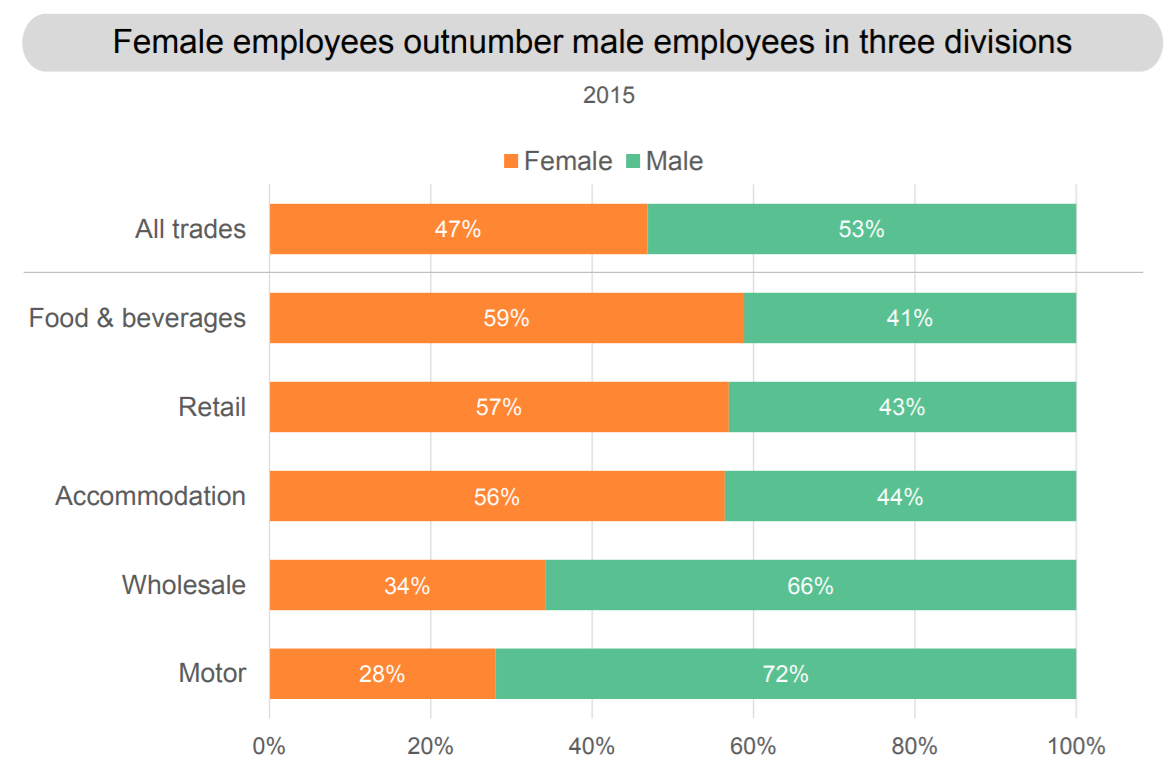

1 November 2017: Employment per gender in Food and Beverages Industry?

The image below shows the distribution of employment per gender in all the major trade industries within South Africa. And according to the graphic obtained from Statistics South Africa, almost 60% of the employees in the Food and Beverages industry are females, while only 40% are males.

Food and beverages sector employment by gender. Statistics South Africa

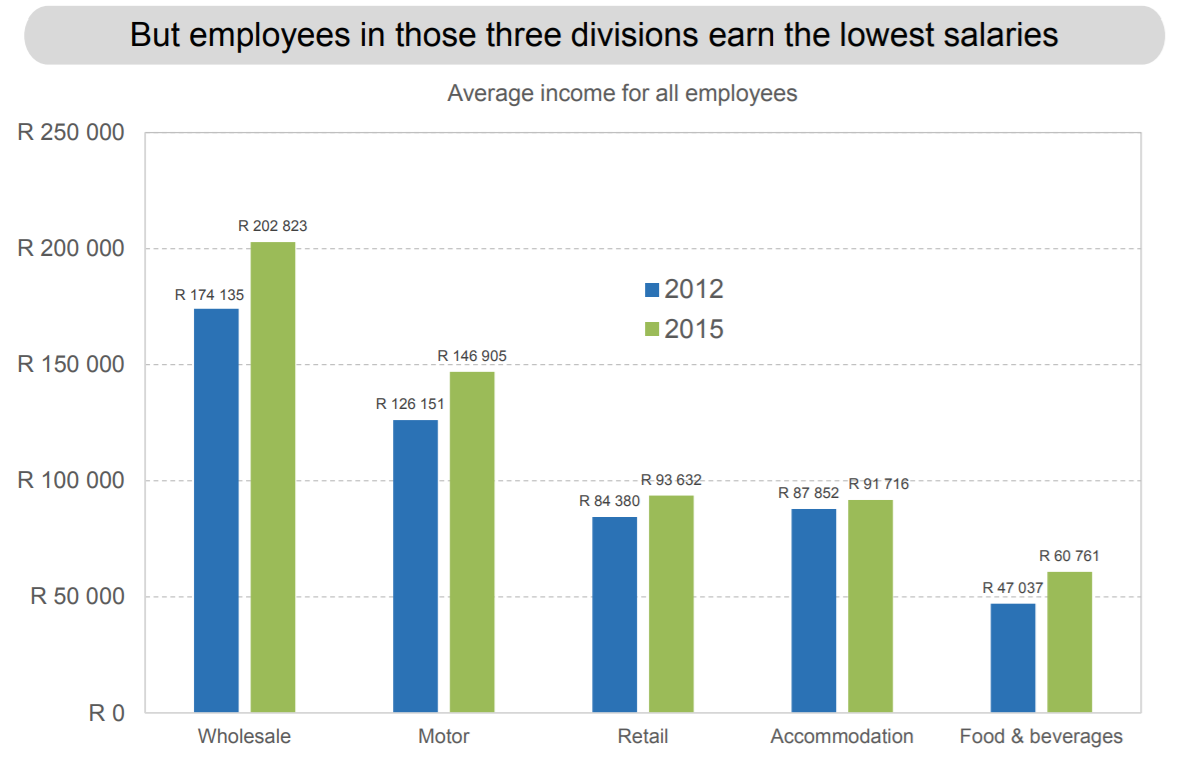

Worrying for the industry (and all the females employed in it) is the fact that the industry has the lowest salary levels out of all the trade industries. Clear proof that females have an uphill battle when it comes to employment and earnings equality, especially in the food and beverages sector of South Africa.

Salaries of the various divisions within the trade industry:

Salary levels for the various divisions within the trade industry in South Africa. Source: Statistics South Africa

While salaries have increased from R47 037 it has gone up to R60 761 (or 9%) a year. And considering inflation averaged roughly 6% showing real wage increases of around 3% per year. Clearly the trade industry one wants to be employed in within the trade industry is the wholesale sector as their salary levels far outstrips the others within the industry.

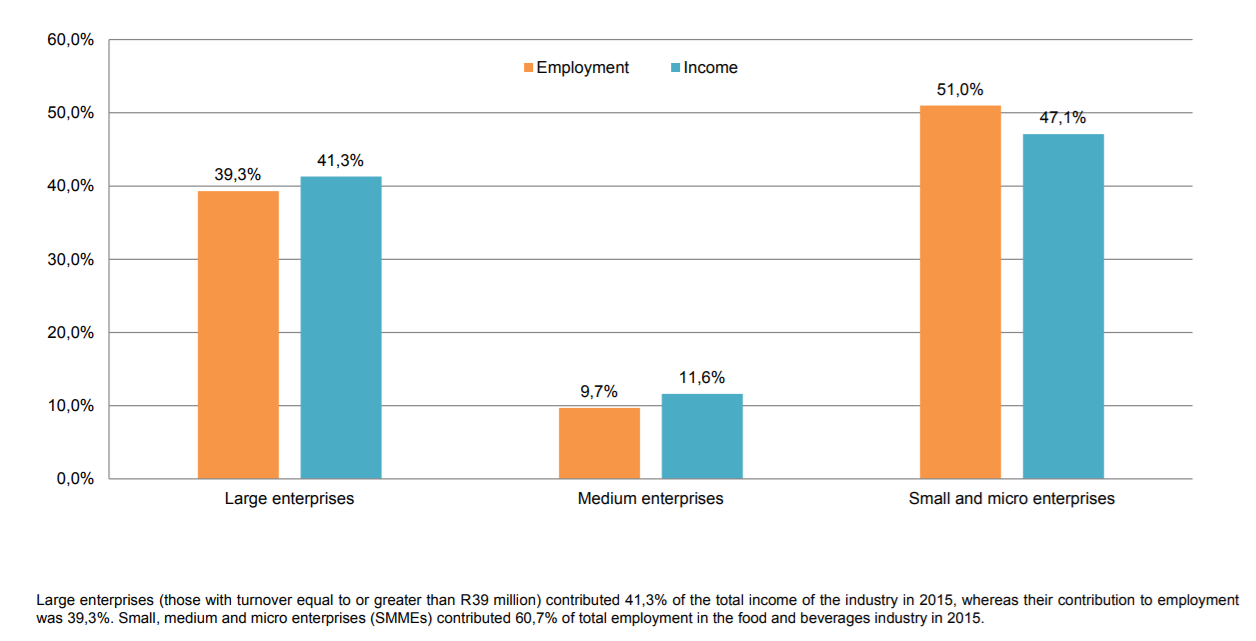

Contribution to income and employment based on company size:

The graphic below shows the contribution various company sizes make to both the income earned and number of employees employed in the food and beverages industry.

Contribution to employment and income by company type. Source: Statistics South Africa

The graphic above shows that small and micro enterprises contribute by fr the most to both employment and income in the food and beverages sector in South Africa. The medium sized companies only contribute around 10% to the total employment level of the industry and close to 12% of the income of the industry.

14 September 2017: Which outlet type earns the most income?

First question we'll answer is which food outlet type brings in the most income? Is it sit down restaurants and coffee shops or Fast food and Take-Away outlets? Or is it Catering services (which includes pubs and canteens)?

From the graphic above it is clear that the income earned from restaurants and coffee shops and those of fast food and take-away outlets are very very similar. In some months restaurants and coffee shops earn more income than fast food and take-aways, and in other months its the reverse that holds true. The breakdown of income earned by food and beverage outlets are roughly as follows:

The graphics below shows per outlet type, the various income sources and its contribution to total income earned per outlet type over time.

- 40% restaurants and coffee shops

- 40% take-aways and fast food outlets

- 20% catering services (includes pubs and canteens)

The graphics below shows per outlet type, the various income sources and its contribution to total income earned per outlet type over time.

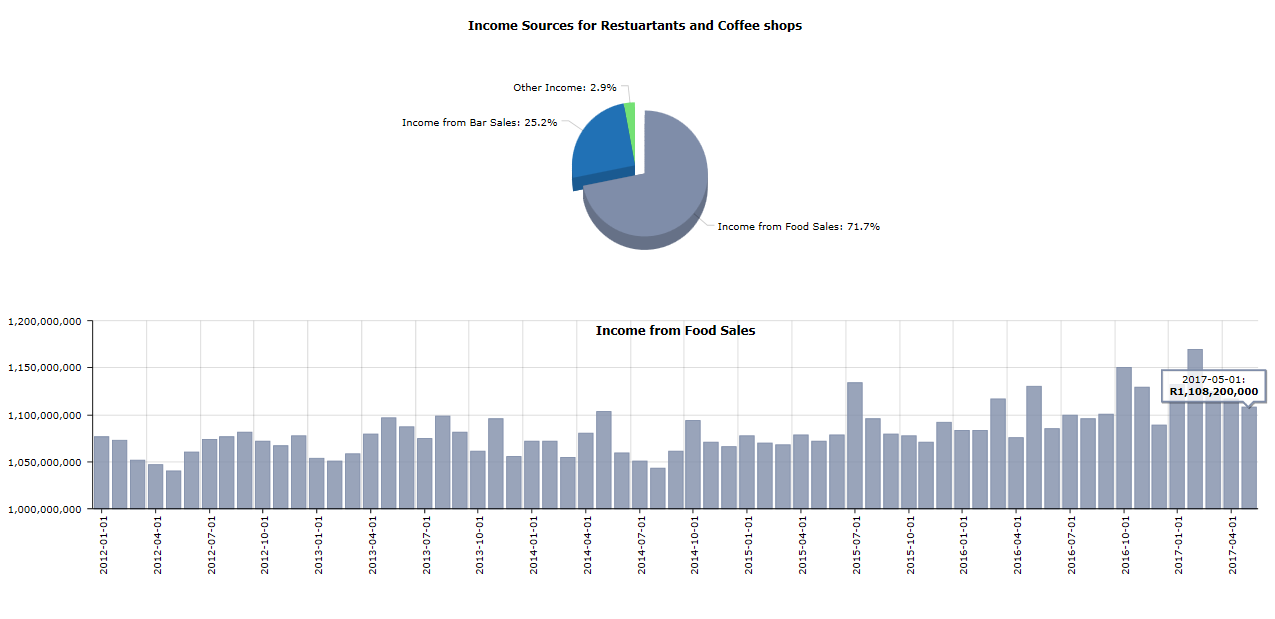

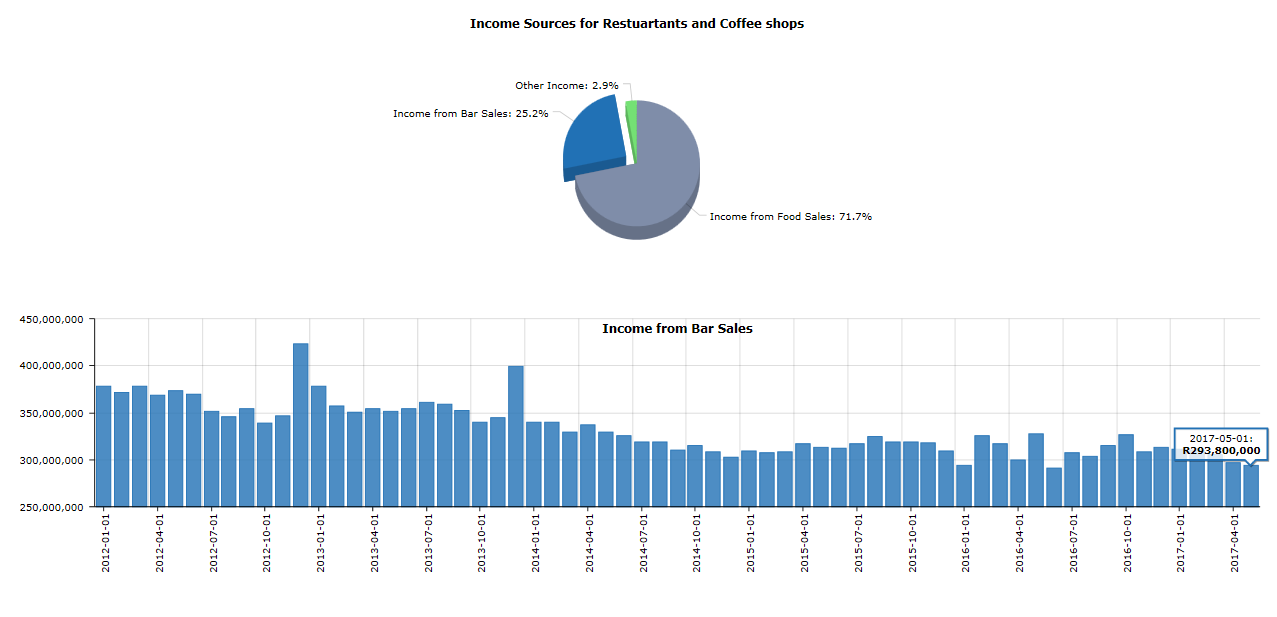

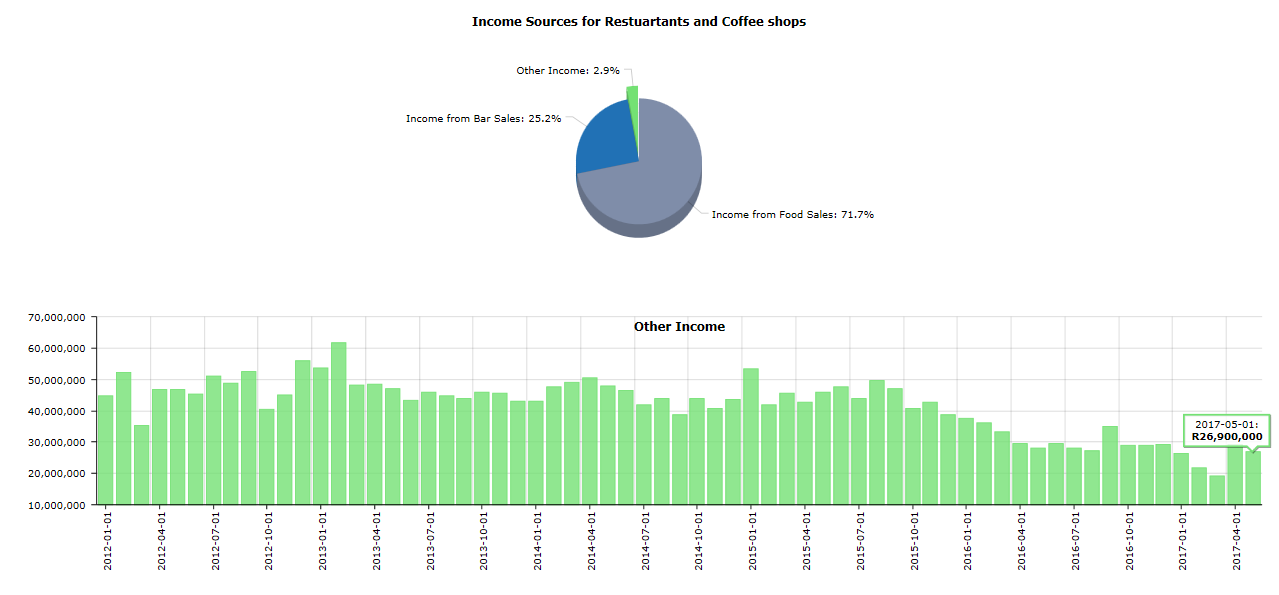

Restaurants and coffee shops

The pie chart of the graphic above clearly shows that the majority of income earned (71.7%) of Total Income is earned from Food Sales, while 25.2% of income for restaurants and coffee shops comes from bar sales (this includes coffee, non-alcoholic and alcoholic beverages), and a mere 2.9% from "other income". This includes cigarettes and other odds and ends sold at restaurants and coffee shops. The bar chart below the pie chart shows the Total Income earned by Restaurants and coffee shops.

Average monthly income for Restaurants and Coffee shops:

Food Sales: R1,05billion

Bar Sales: R310million

Other Income: R30million

If users click on the pie chart (and select say Income from Food sales), the bar chart will show the income earned from food sales for every month. See images below to get an idea of the kind of information the infographic above supplies.

Average monthly income for Restaurants and Coffee shops:

Food Sales: R1,05billion

Bar Sales: R310million

Other Income: R30million

If users click on the pie chart (and select say Income from Food sales), the bar chart will show the income earned from food sales for every month. See images below to get an idea of the kind of information the infographic above supplies.

Food Sales

Income earned from food sales from Restaurants and coffee shops

|

Bar Sales

Income earned from bar sales from Restaurants and coffee shops

|

Other Income

Income earned from "Other sales" from Restaurants and coffee shops

|

Fast Food and Take-away outlets:

As can be seen from the graphic below, the majority of income earned from Fast-food and Take-away outlets come from Food sales (97.3%). It has to be noted combo meals that includes drinks such as fizzy drinks, juices, coffee etc. will be counted under Food sales, which skews the results a little in terms of the bar sales reported by Fast-food and take-away outlets. Almost no income is earned by fast-food and take-away outlets from "Other".

Average monthly income for Fast Food and Take-away outlets:

Food Sales: R1,32billion

Bar Sales: R35million

Other Income: R2illion

Food Sales: R1,32billion

Bar Sales: R35million

Other Income: R2illion

Catering services

As can be seen from the graphic below, the majority of income earned from Catering services comes from Food sales (70.6%). But since Catering services includes pubs, taverns and canteens, a significant chunk of their income is earned from Bar sales (20.8%). While 8.5% of Catering services's income is earned from Other (think cigarettes, limited payout slot machines and other games etc).

Average monthly income for Catering services:

Food Sales: R430million

Bar Sales: R110million

Other Income: R50million

Food Sales: R430million

Bar Sales: R110million

Other Income: R50million

The food and beverages industry in South Africa is a significant one, with a number of companies active in this sector listed on the JSE too. They include Famous Brands, Spur, Taste Holdings. See our Sector Comparison Page to compare the share price performance of these companies over time.

According to Statistics South Africa (Stats SA) Consumer Price Index (CPI), South Africans spend 1.98% of all money spent at restaurants for sit down or take-away, which equates to over R48billion a year spent by South African consumers on this particular industry

According to Statistics South Africa (Stats SA) Consumer Price Index (CPI), South Africans spend 1.98% of all money spent at restaurants for sit down or take-away, which equates to over R48billion a year spent by South African consumers on this particular industry