|

|

Related Topics

|

About Italtile

Italtile limited is a leading retailer and manufacturer of tiles, bathroomware and related products. The Group operates as a national franchisor of its three high profile retail brands, Italtile Retail, CTM and TopT. The retail operations are underpinned by an extensive property portfolio and a vertically integrated supply chain comprising International Tap Distributors (an importer and distributor of brassware and accessories), and Cedar Point, (an importer of shower enclosures, laminated boards, cabinets, sanitaryware, décor and tiling tools). The Group holds controlling interests in both businesses. The Group’s Distribution Centre sources imported products and provides warehousing and distribution facilities to the retail brands. Effective 2 October 2017, the Group acquired controlling stakes in its key suppliers, tile and sanitaryware manufacturer, Ceramic Industries (Pty) Ltd and adhesives and related products manufacturer, Ezee Tile.

Italtile showroom

Trading Statement

Italtile is currently finalising its results for the six months ended 31 December 2019 (“the review period”). This trading statement includes the contribution of Ceramic Industries Proprietary Limited (“Ceramic”), in which the Group holds a 95.47% stake, and Ezee Tile Adhesive Manufacturers Proprietary Limited (“Ezee Tile”), in which the Group holds an effective 71.54% stake. Sales related to Ceramic and Ezee Tile are referred to as “manufacturing” sales to distinguish them from “retail” sales reported by Italtile’s retail brands, namely CTM, Italtile Retail, TopT and U-Light.

OPERATING ENVIRONMENT

Lacklustre trading conditions persisted over the review period. Consumer confidence and investment sentiment remained subdued in the absence of transformational economic and socio-political reforms, continued policy uncertainty and an increasingly unstable power supply, while household discretionary spend remained severely constrained in the context of escalating living costs, limited wage inflation, high levels of personal debt, retrenchments and unprecedented unemployment rates. RESULTS Despite the challenging operating environment, the Group reported solid results for the review period, reflecting the strength of its strategically structured resilient business model. System-wide turnover for the review period was R5.4 billion, 1.4% higher than the prior corresponding period (2018: R5.3 billion). System-wide turnover is defined as the aggregate of the Group’s consolidated turnover (total sales by Group-owned entities and corporate stores, excluding sales from owned supply chain businesses to corporate stores) and the retail turnover of franchisees of the Group. Retail In the weak demand environment, creditable retail turnover growth was achieved, attributable to management’s unwavering focus on improving the customer experience and driving sales through investment in people, technology, store layouts, merchandising and range. Total retail store turnover rose 4.5% for the review period compared to the previous corresponding period, with average selling price inflation estimated at 1.5%. Like-for-like retail store turnover growth of 1.7% was below management’s benchmark. Retail store turnover is defined as the aggregate turnover of all stores, both corporate and franchised, in the Group’s retail network. Manufacturing Generally softer consumer demand and the overstock position of tile wholesalers in the industry impacted negatively on Ceramic’s sales, which were flat compared to the previous corresponding period. However, as remedial measures took effect Ezee Tile succeeded in reversing the disappointing performance reported in the prior year. This business delivered good sales growth of 7.3%, which contributed to the manufacturing division’s total sales growth of 1.3%. Estimated average selling price inflation in the manufacturing division was 1.0% for the review period.

EARNINGS

During the review period, the Group incurred a once-off charge of R39.0 million related to the Broad- Based Black Economic Empowerment (“BBBEE”) transaction concluded with Yard Investment Holdings Proprietary Limited, (“Yard”), as announced on SENS on 10 September 2019. Accordingly, the guidance below illustrates the Group’s BBBEE transaction impact on earnings per share (“EPS”) and headline earnings per share (“HEPS”) for the review period.

Six months to December 2018 Six months to December 2019 Percentage change

Excluding BBBEE charge

- Earnings per share 55.4 cents 57.6 cents to 59.3 cents 4% to 7%

- Headline earnings per share 54.7 cents 58.0 cents to 59.1 cents 6% to 8%

Including BBBEE charge

- Earnings per share 55.4 cents 54.3 cents to 56.5 cents -2% to 2%

- Headline earnings per share 54.7 cents 54.7 cents to 55.8 cents 0% to 2%

OUTLOOK

While the weak macro-economic conditions are extremely challenging and expected to persist for the foreseeable future, management remains optimistic that the Group will deliver growth for the full financial year. In the Group’s reviewed results for the year ended 30 June 2019 published on SENS on 22 August 2019, management projected that due to the high base effect, growth in the first six months of the year would likely be lower than the second six months. However, given the continuing deterioration of the economy - and the retail and construction sectors specifically - growth in the second half of the year is now anticipated to be less robust than envisaged, and more likely in line with the current review period. Notwithstanding the discouraging external environment, management remains committed to optimising on the opportunities within its control in the business to drive continued growth.

REVIEW OF RESULTS

The information on which this announcement is based has not been reviewed or reported on by Italtile's auditors.

PUBLICATION OF RESULTS

The Group's results for the six months ended 31 December 2019 are expected to be published on SENS on or about 13 February 2020.

Johannesburg 7 February 2020

Sponsor Merchantec Capital

OPERATING ENVIRONMENT

Lacklustre trading conditions persisted over the review period. Consumer confidence and investment sentiment remained subdued in the absence of transformational economic and socio-political reforms, continued policy uncertainty and an increasingly unstable power supply, while household discretionary spend remained severely constrained in the context of escalating living costs, limited wage inflation, high levels of personal debt, retrenchments and unprecedented unemployment rates. RESULTS Despite the challenging operating environment, the Group reported solid results for the review period, reflecting the strength of its strategically structured resilient business model. System-wide turnover for the review period was R5.4 billion, 1.4% higher than the prior corresponding period (2018: R5.3 billion). System-wide turnover is defined as the aggregate of the Group’s consolidated turnover (total sales by Group-owned entities and corporate stores, excluding sales from owned supply chain businesses to corporate stores) and the retail turnover of franchisees of the Group. Retail In the weak demand environment, creditable retail turnover growth was achieved, attributable to management’s unwavering focus on improving the customer experience and driving sales through investment in people, technology, store layouts, merchandising and range. Total retail store turnover rose 4.5% for the review period compared to the previous corresponding period, with average selling price inflation estimated at 1.5%. Like-for-like retail store turnover growth of 1.7% was below management’s benchmark. Retail store turnover is defined as the aggregate turnover of all stores, both corporate and franchised, in the Group’s retail network. Manufacturing Generally softer consumer demand and the overstock position of tile wholesalers in the industry impacted negatively on Ceramic’s sales, which were flat compared to the previous corresponding period. However, as remedial measures took effect Ezee Tile succeeded in reversing the disappointing performance reported in the prior year. This business delivered good sales growth of 7.3%, which contributed to the manufacturing division’s total sales growth of 1.3%. Estimated average selling price inflation in the manufacturing division was 1.0% for the review period.

EARNINGS

During the review period, the Group incurred a once-off charge of R39.0 million related to the Broad- Based Black Economic Empowerment (“BBBEE”) transaction concluded with Yard Investment Holdings Proprietary Limited, (“Yard”), as announced on SENS on 10 September 2019. Accordingly, the guidance below illustrates the Group’s BBBEE transaction impact on earnings per share (“EPS”) and headline earnings per share (“HEPS”) for the review period.

Six months to December 2018 Six months to December 2019 Percentage change

Excluding BBBEE charge

- Earnings per share 55.4 cents 57.6 cents to 59.3 cents 4% to 7%

- Headline earnings per share 54.7 cents 58.0 cents to 59.1 cents 6% to 8%

Including BBBEE charge

- Earnings per share 55.4 cents 54.3 cents to 56.5 cents -2% to 2%

- Headline earnings per share 54.7 cents 54.7 cents to 55.8 cents 0% to 2%

OUTLOOK

While the weak macro-economic conditions are extremely challenging and expected to persist for the foreseeable future, management remains optimistic that the Group will deliver growth for the full financial year. In the Group’s reviewed results for the year ended 30 June 2019 published on SENS on 22 August 2019, management projected that due to the high base effect, growth in the first six months of the year would likely be lower than the second six months. However, given the continuing deterioration of the economy - and the retail and construction sectors specifically - growth in the second half of the year is now anticipated to be less robust than envisaged, and more likely in line with the current review period. Notwithstanding the discouraging external environment, management remains committed to optimising on the opportunities within its control in the business to drive continued growth.

REVIEW OF RESULTS

The information on which this announcement is based has not been reviewed or reported on by Italtile's auditors.

PUBLICATION OF RESULTS

The Group's results for the six months ended 31 December 2019 are expected to be published on SENS on or about 13 February 2020.

Johannesburg 7 February 2020

Sponsor Merchantec Capital

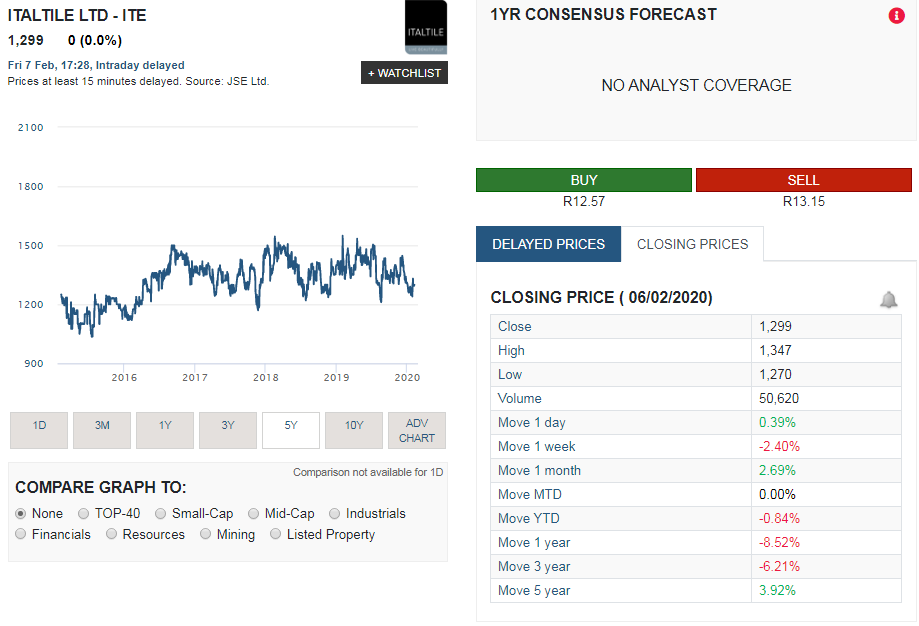

Italtile (ITE) share price performance over last 5 years

The image below, taken from Sharenet shows Italtile's share price performance over the last 5 years. and we must say the share price has held up pretty well considering the industry they operate in.

The summary below shows the share price returns of Italtile over various time periods:

The above shows that over the very short term Italtile has been struggling but when taking a long term view such as the last 5 years, the group actually provided shareholders with pretty decent returns. It should be noted that it is not the most liquid stock around so it doesn't change hands to often, and this might have been providing some protection for the group's share price over the years.

- 1 week: -1.52%

- 1 month: -12.16%

- Year to date (YTD): -7.14%

- 1 year: 1.88%

- 3 years: -3.70%

- 5 years: 46.07%

The above shows that over the very short term Italtile has been struggling but when taking a long term view such as the last 5 years, the group actually provided shareholders with pretty decent returns. It should be noted that it is not the most liquid stock around so it doesn't change hands to often, and this might have been providing some protection for the group's share price over the years.