|

Related Topics |

|

We take a look at the latest financial results from listed Telecoms operator MTN for the period ending June 2019. The mobile operator has been struggling for years largely due to issues in some of their biggest markets such as Iran and Nigeria. Can the group lessen their dependence on these markets by growing market shares in their other markets? Lets see if their results hint towards growing market share elsewhere

|

|

About MTN

For those who dont know anything about MTN. Below a brief description of what the group is about.

MTN is a leading emerging market mobile operator, serving 233 million subscribers in 21 countries across Africa and the Middle East. MTN Group Ltd. is a pure-play emerging markets mobile telco operator at the forefront of technological and digital changes. The Group offers voice, data and digital services to retail customers in the 21 countries in which its operations have telecoms licences.

MTN is a leading emerging market mobile operator, serving 233 million subscribers in 21 countries across Africa and the Middle East. MTN Group Ltd. is a pure-play emerging markets mobile telco operator at the forefront of technological and digital changes. The Group offers voice, data and digital services to retail customers in the 21 countries in which its operations have telecoms licences.

Financial Results Overview

Firstly we take a look at the financial highlights as stated by MTN's management

- Subscribers increased by 7,7 million to 240 million from 31 December 2018

- Service revenue grew by 9,7%*

- EBITDA margin improved to 35,2%* (43,1%**)

- EBITDA˜ (before once-off items) increased by 10,2%* (34,7%**)

- Reported group EPS at 247 cps**, up 17,2%^ (1,2%**)

- Reported group HEPS at 195 cps**, up 8,8%^ (down 9,3%**)

- Non-operational impacts, including IFRS 16 (39 cents), lowered HEPS by 102 cps

- Holding company leverage stable at 2,3x

- Interim dividend of 195 cents per share in line with guidance, up 11,4%

Now for the numbers we are interested in:

- Subscribers increased by 7,7 million to 240 million from 31 December 2018

- Service revenue grew by 9,7%*

- EBITDA margin improved to 35,2%* (43,1%**)

- EBITDA˜ (before once-off items) increased by 10,2%* (34,7%**)

- Reported group EPS at 247 cps**, up 17,2%^ (1,2%**)

- Reported group HEPS at 195 cps**, up 8,8%^ (down 9,3%**)

- Non-operational impacts, including IFRS 16 (39 cents), lowered HEPS by 102 cps

- Holding company leverage stable at 2,3x

- Interim dividend of 195 cents per share in line with guidance, up 11,4%

Now for the numbers we are interested in:

- Revenue: R72.505 billion

- Profit for the period: R4.328 billion

- Net profit margin: 5.96% (down from 6.46% as at year end December 2018)

- Diluted Headline Earnings per share: R1.95

- PE ratio: 28 (when using the more realistic headline earnings per share number)

- Dividend declared for period: R1.95 per share

- Dividend yield: 3.48%

- Cash generated from operations: R20.9 billion

- Cash generated from operations per share: R11.09 per share

- Net asset value per share: R45.15

- So trading at about2.48 times its stated net asset value

- Cash on balance sheet: R13.338 billion

- Cash on balance sheet per share: R7.09 or 6.3% of the current share price

Management commentary on the results

Group president and CEO, Rob Shuter comments:

"We delivered encouraging results for the period, against the backdrop of difficult trading conditions. South Africa in particular was impacted by a weak economy as well as the implementation of lower out-of-bundle pricing and the new ICASA subscriber regulations in the first quarter of the year. Despite these headwinds, we progressed with our plans to build a digital operator, growing service revenue by 9,7%* and EBITDA by 10,2%*, which supported solid growth in operational earnings. Our holding company leverage ratio remained stable at 2,3x and we reduced our capex intensity to 16,9%^. Commercial momentum continued, with growth in our subscriber base of 7,7 million, in our active data users of 3,5 million, and in our Mobile Money users of 2,4 million. We now have leading network NPS in more than half of our markets, supported by the continued expansion and quality of our data networks. We delivered on several strategic projects including the listings of MTN Nigeria on the Nigerian Stock Exchange and Jumia, our e-commerce venture, on the New York Stock Exchange. The asset realisation programme delivered R2,1 billion to the group in the second quarter, we launched our Ayoba messaging platform in 3 markets and we were awarded a super-agent licence in Nigeria, enabling the expansion of our fintech business. We remain focused on building our digital operator strategy, focusing on being a scale player in both our evolving telco services as well as digital and fintech and delivering on our medium-term targets."

Overview

MTN reported encouraging operational results for the 6 months as we remained focused on executing our BRIGHT strategy. We continued to grow service revenue ahead of inflation, to increase our margin on earnings before interest, taxation, depreciation and amortisation (EBITDA) slightly and to reduce capital expenditure (capex) intensity. Macroeconomic conditions were challenging, particularly in South Africa, with the economy contracting in the first quarter and the rand weakening against the US dollar.

Group service revenue increased by 9,7%* in constant currency terms. This was led by growth of 12,2%* by MTN Nigeria, 18,7%* by MTN Ghana and 3,3% by MTN South Africa. The performance of MTN South Africa was impacted by changes to out-of-bundle (OOB) tariffs and a reassessment of revenue recognition criteria and adjustments required due to delayed payments under the network roaming agreement with Cell C. As a result of the reassessment and in compliance with IFRS 15 Revenue from Contracts with Customers, we have not recognised revenue amounting to R393 million for network roaming services provided to Cell C during the period. We are evaluating a sustainable solution to the agreement with Cell C.

Voice revenue increased by 4,5%*. This was underpinned by customer growth, the benefits of our customer value management (CVM) initiatives and our focus on segmented offers. Group subscribers increased by 7,7 million to 240 million and we rolled out our Pulse youth offer in 16 markets.

Group data revenue expanded by 19,8%*, supported by healthy growth in active data users to 82 million as we improved the coverage and quality of our data networks. Across our markets, we increased 3G and 4G population coverage by 24,4 million and 32,5 million people respectively. The effective rate per megabyte across our markets declined by 26,1%, with average usage up 24,6% at 2,7GB per month.

Digital revenue decreased by 42,5%*. This was largely the result of the continued optimisation of traditional value-added services. In June, we recorded an increase in digital revenue month-on-month. We are focused on growing our modern digital offerings through our music, instant messaging and advertising platforms. We continued to expand MusicTime!, focusing on customer awareness and refining our go-to-market strategy. Following the launch of Ayoba in 3 markets, we recorded 300 000 monthly active users at the end of the period.

Fintech revenue increased by 30,7%*, supported by customer growth of 8,9% to 30 million active Mobile Money (MoMo) users with a monthly ARPU of US$1,30. The total value of transactions in the six months to June was US$44,1 billion, and we processed 9 193 transactions per minute. In May, we launched Africa's first MoMo artificial intelligence service or chatbot in Ivory Coast. Our aYo joint venture insurance business recorded almost 4,2 million registered policy holders across our African footprint in the first half, as we launched the offering in Ghana.

Operational review

MTN South Africa

- Service revenue increased by 3,3%

-Data revenue increased by 5,6%

- Fintech revenue increased by 21,6%

- Digital revenue decreased by 34,5%

- EBITDA increased by 0,2%* to R7 462 million

- EBITDA margin decreased by 1,9 pp* to 33,3%*

- Capex decreased by 13,8%* MTN

South Africa reported improved service revenue in the period. Growth in wholesale and consumer postpaid revenue supported service revenue growth but was offset by a 5,5% reduction in prepaid service revenue coupled by the Cell C adjustments made.

MTN Nigeria

- Service revenue increased by 12,2%*

- Data revenue increased by 31,8%*

- Fintech revenue increased by 21,2%*

- Digital revenue decreased by 64,3%*

- EBITDA grew by 16,1%* to R8 623 million*

- EBITDA margin increased by 1,5 pp* to 44,6%*

- Capex increased by 37,5%*

MTN Nigeria delivered a solid performance, with strong voice (+11,4%) and data revenue (+31,8%) driving double-digit service revenue growth and further improving the EBITDA margin.

West and Central Africa (WECA)

- Service revenue increased by 0,5%*

- Data revenue increased by 24,9%*

- Fintech revenue increased by 35,5%*

- Digital revenue declined by 58,8%*

Middle East and North Africa (MENA) (excluding Iran)

- Service revenue increased by 19,8%*

- Data revenue increased by 45,6%*

- Fintech revenue increased by 80,8%*

- Digital revenue increased by 26,1%*

Despite the geopolitical challenges across the region, MTN operations in MENA delivered a strong performance, largely driven by MTN Syria and MTN Sudan, delivering service revenue growth of 14,0%* and 49,4%* respectively. This was supported by the solid growth in data and voice revenue

Associates, joint ventures and investments

Telecoms operations

MTN Irancell recorded a pleasing result given the challenges the business faced following the re-introduction of US sanctions, the depreciation of the currency and high inflation rates. Service revenue grew by 17,9%*, with voice up by 24,4%* and data revenue up by 22,4%*. The reported results from Iran were however negatively impacted on translation following the move to report exchange rates at the Sana rate as of August 2018. The average Sana rate in the reporting period was 51,3% weaker relative to the prior period. This added to the additional forex losses against the Iranian receivable of R1 295 million at the end of the period. The value of the Irancell receivable as at 30 June 2019 was R3,0 billion.

Prospects and guidance

Well positioned to deliver growth Guided by our BRIGHT strategy, we are well positioned to grow by leveraging our scale and enhancing our competitive position. Our markets are characterised by significant population growth, youthful demographics, low levels of smartphone penetration and data and digital adoption, as well as large unbanked populations.

The enterprise and wholesale sectors are relatively undeveloped and growing fast. The combination of our large customer base, extensive networks and deep distribution gives us access to large pools of revenue. We are committed to building a digital operator, being a scale player in both the evolving telco and fintech and digital services spaces. Following data price reductions in South Africa and Nigeria, we expect price elasticity in the second half of the year to improve data revenue growth.

We expect lower wholesale revenue in MTN South Africa to be a drag on service revenue following the end of the national wholesale deal with Telkom on 28 June 2019. We plan to launch MoMo in South Africa in the second half of the year. On the back of the award of the super-agent licence in Nigeria, we will accelerate our fintech ambitions and now fully leverage the extensive distribution we have across the country to offer a range of transfer and payment services to our GSM customer base. We will continue to work towards obtaining a payment service banking licence in Nigeria. We will roll out our MTN Homeland offering, allowing money to be sent to MoMo recipients in Africa from Europe quickly and affordably.

We will continue to expand our insurance business and leverage the partnership with Sanlam that we announced in July 2019. We plan to roll out Ayoba in Nigeria, South Africa, Uganda and Liberia in the second half of the year. We will also integrate payments into the Ayoba service as part of our broadening of the fintech business, as well as integrate Ayoba into MTN segmented offers. After launching our time-based music streaming service MusicTime! in South Africa in December 2018, we plan to launch this next in Nigeria and Ghana.

Medium-term guidance

We reiterate our guidance for the medium term (3 to 5 years) of double-digit growth in group service revenue in constant currency terms, double-digit growth in MTN Nigeria's service revenue and mid-single-digit growth in service revenue from MTN South Africa. Over this period, we expect to continue to increase our group EBITDA margin. By leveraging historical investments, improved procurement processes and an increasing revenue contribution from our digital businesses, we expect the group capex intensity to steadily improve over the medium term. Our improving revenue growth, margins and capex intensity are anticipated to drive significant improvements in group returns and cash flow. The board remains committed to targeting growth of 10% to 20% in the dividend

"We delivered encouraging results for the period, against the backdrop of difficult trading conditions. South Africa in particular was impacted by a weak economy as well as the implementation of lower out-of-bundle pricing and the new ICASA subscriber regulations in the first quarter of the year. Despite these headwinds, we progressed with our plans to build a digital operator, growing service revenue by 9,7%* and EBITDA by 10,2%*, which supported solid growth in operational earnings. Our holding company leverage ratio remained stable at 2,3x and we reduced our capex intensity to 16,9%^. Commercial momentum continued, with growth in our subscriber base of 7,7 million, in our active data users of 3,5 million, and in our Mobile Money users of 2,4 million. We now have leading network NPS in more than half of our markets, supported by the continued expansion and quality of our data networks. We delivered on several strategic projects including the listings of MTN Nigeria on the Nigerian Stock Exchange and Jumia, our e-commerce venture, on the New York Stock Exchange. The asset realisation programme delivered R2,1 billion to the group in the second quarter, we launched our Ayoba messaging platform in 3 markets and we were awarded a super-agent licence in Nigeria, enabling the expansion of our fintech business. We remain focused on building our digital operator strategy, focusing on being a scale player in both our evolving telco services as well as digital and fintech and delivering on our medium-term targets."

Overview

MTN reported encouraging operational results for the 6 months as we remained focused on executing our BRIGHT strategy. We continued to grow service revenue ahead of inflation, to increase our margin on earnings before interest, taxation, depreciation and amortisation (EBITDA) slightly and to reduce capital expenditure (capex) intensity. Macroeconomic conditions were challenging, particularly in South Africa, with the economy contracting in the first quarter and the rand weakening against the US dollar.

Group service revenue increased by 9,7%* in constant currency terms. This was led by growth of 12,2%* by MTN Nigeria, 18,7%* by MTN Ghana and 3,3% by MTN South Africa. The performance of MTN South Africa was impacted by changes to out-of-bundle (OOB) tariffs and a reassessment of revenue recognition criteria and adjustments required due to delayed payments under the network roaming agreement with Cell C. As a result of the reassessment and in compliance with IFRS 15 Revenue from Contracts with Customers, we have not recognised revenue amounting to R393 million for network roaming services provided to Cell C during the period. We are evaluating a sustainable solution to the agreement with Cell C.

Voice revenue increased by 4,5%*. This was underpinned by customer growth, the benefits of our customer value management (CVM) initiatives and our focus on segmented offers. Group subscribers increased by 7,7 million to 240 million and we rolled out our Pulse youth offer in 16 markets.

Group data revenue expanded by 19,8%*, supported by healthy growth in active data users to 82 million as we improved the coverage and quality of our data networks. Across our markets, we increased 3G and 4G population coverage by 24,4 million and 32,5 million people respectively. The effective rate per megabyte across our markets declined by 26,1%, with average usage up 24,6% at 2,7GB per month.

Digital revenue decreased by 42,5%*. This was largely the result of the continued optimisation of traditional value-added services. In June, we recorded an increase in digital revenue month-on-month. We are focused on growing our modern digital offerings through our music, instant messaging and advertising platforms. We continued to expand MusicTime!, focusing on customer awareness and refining our go-to-market strategy. Following the launch of Ayoba in 3 markets, we recorded 300 000 monthly active users at the end of the period.

Fintech revenue increased by 30,7%*, supported by customer growth of 8,9% to 30 million active Mobile Money (MoMo) users with a monthly ARPU of US$1,30. The total value of transactions in the six months to June was US$44,1 billion, and we processed 9 193 transactions per minute. In May, we launched Africa's first MoMo artificial intelligence service or chatbot in Ivory Coast. Our aYo joint venture insurance business recorded almost 4,2 million registered policy holders across our African footprint in the first half, as we launched the offering in Ghana.

Operational review

MTN South Africa

- Service revenue increased by 3,3%

-Data revenue increased by 5,6%

- Fintech revenue increased by 21,6%

- Digital revenue decreased by 34,5%

- EBITDA increased by 0,2%* to R7 462 million

- EBITDA margin decreased by 1,9 pp* to 33,3%*

- Capex decreased by 13,8%* MTN

South Africa reported improved service revenue in the period. Growth in wholesale and consumer postpaid revenue supported service revenue growth but was offset by a 5,5% reduction in prepaid service revenue coupled by the Cell C adjustments made.

MTN Nigeria

- Service revenue increased by 12,2%*

- Data revenue increased by 31,8%*

- Fintech revenue increased by 21,2%*

- Digital revenue decreased by 64,3%*

- EBITDA grew by 16,1%* to R8 623 million*

- EBITDA margin increased by 1,5 pp* to 44,6%*

- Capex increased by 37,5%*

MTN Nigeria delivered a solid performance, with strong voice (+11,4%) and data revenue (+31,8%) driving double-digit service revenue growth and further improving the EBITDA margin.

West and Central Africa (WECA)

- Service revenue increased by 0,5%*

- Data revenue increased by 24,9%*

- Fintech revenue increased by 35,5%*

- Digital revenue declined by 58,8%*

Middle East and North Africa (MENA) (excluding Iran)

- Service revenue increased by 19,8%*

- Data revenue increased by 45,6%*

- Fintech revenue increased by 80,8%*

- Digital revenue increased by 26,1%*

Despite the geopolitical challenges across the region, MTN operations in MENA delivered a strong performance, largely driven by MTN Syria and MTN Sudan, delivering service revenue growth of 14,0%* and 49,4%* respectively. This was supported by the solid growth in data and voice revenue

Associates, joint ventures and investments

Telecoms operations

MTN Irancell recorded a pleasing result given the challenges the business faced following the re-introduction of US sanctions, the depreciation of the currency and high inflation rates. Service revenue grew by 17,9%*, with voice up by 24,4%* and data revenue up by 22,4%*. The reported results from Iran were however negatively impacted on translation following the move to report exchange rates at the Sana rate as of August 2018. The average Sana rate in the reporting period was 51,3% weaker relative to the prior period. This added to the additional forex losses against the Iranian receivable of R1 295 million at the end of the period. The value of the Irancell receivable as at 30 June 2019 was R3,0 billion.

Prospects and guidance

Well positioned to deliver growth Guided by our BRIGHT strategy, we are well positioned to grow by leveraging our scale and enhancing our competitive position. Our markets are characterised by significant population growth, youthful demographics, low levels of smartphone penetration and data and digital adoption, as well as large unbanked populations.

The enterprise and wholesale sectors are relatively undeveloped and growing fast. The combination of our large customer base, extensive networks and deep distribution gives us access to large pools of revenue. We are committed to building a digital operator, being a scale player in both the evolving telco and fintech and digital services spaces. Following data price reductions in South Africa and Nigeria, we expect price elasticity in the second half of the year to improve data revenue growth.

We expect lower wholesale revenue in MTN South Africa to be a drag on service revenue following the end of the national wholesale deal with Telkom on 28 June 2019. We plan to launch MoMo in South Africa in the second half of the year. On the back of the award of the super-agent licence in Nigeria, we will accelerate our fintech ambitions and now fully leverage the extensive distribution we have across the country to offer a range of transfer and payment services to our GSM customer base. We will continue to work towards obtaining a payment service banking licence in Nigeria. We will roll out our MTN Homeland offering, allowing money to be sent to MoMo recipients in Africa from Europe quickly and affordably.

We will continue to expand our insurance business and leverage the partnership with Sanlam that we announced in July 2019. We plan to roll out Ayoba in Nigeria, South Africa, Uganda and Liberia in the second half of the year. We will also integrate payments into the Ayoba service as part of our broadening of the fintech business, as well as integrate Ayoba into MTN segmented offers. After launching our time-based music streaming service MusicTime! in South Africa in December 2018, we plan to launch this next in Nigeria and Ghana.

Medium-term guidance

We reiterate our guidance for the medium term (3 to 5 years) of double-digit growth in group service revenue in constant currency terms, double-digit growth in MTN Nigeria's service revenue and mid-single-digit growth in service revenue from MTN South Africa. Over this period, we expect to continue to increase our group EBITDA margin. By leveraging historical investments, improved procurement processes and an increasing revenue contribution from our digital businesses, we expect the group capex intensity to steadily improve over the medium term. Our improving revenue growth, margins and capex intensity are anticipated to drive significant improvements in group returns and cash flow. The board remains committed to targeting growth of 10% to 20% in the dividend

Advertisement

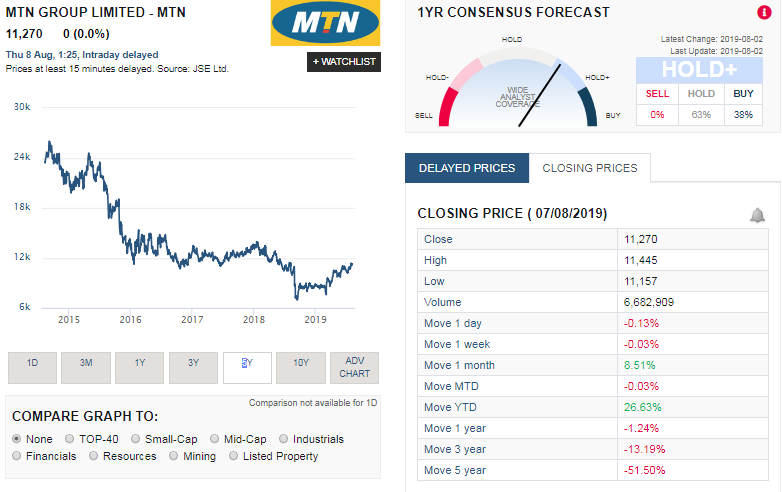

Share Price Performance of MTN

The screenshot below, taken from Sharenet shows the share price performance of MTN over the last 3 years. It also shows the stock's performance over various time frames as well as the sharp increase in the share price today following the release of the financial results

The summary below shows the performance of MTN's share price over various time periods:

So its clear MTN shares have not been performing very well and has left investors pretty bruised and battered. But it has started its slow and steady recovery and we are sure all MTN shareholders will hope that this can continue into the future, so that long term investors can recoup some of their historical losses.

- 1 week:-0.03%

- 1 month: 8.51%

- Year to date (YTD): 26.63%

- 1 year: -1.24%

- 3 years: -13.19%

- 5 years: -51.50%

So its clear MTN shares have not been performing very well and has left investors pretty bruised and battered. But it has started its slow and steady recovery and we are sure all MTN shareholders will hope that this can continue into the future, so that long term investors can recoup some of their historical losses.

MTN shares valuation

In our March 2019 valuation of MTN we valued the group's shares at R94.52 a share. This was at a time when they were trading in the mid R80's per share. So the MTN share price has certainly recovered strongly since then. The question is has it gone up to fast? And does their current financial results warrant a share price of R112.70 that it is trading at now?

Well their balance sheet is strong, they have a decent net profit margin. They do however continue to have regular clashes with the Nigerian authorities regarding penalties they need to pay and cash being repatriated out of the country, In addition to this they have a big market in Iran, from which they struggle to repatriate cash too since sanctions are often imposed on the country.

But with this all being said, their tougher markets are the more lucarative and their biggest markets so should there be no issues in these markets over the next couple of years MTN could see bumper profits coming from these countries which should be good for its share price. Based on current financials and future prospects our valuation model places a target price of R101.50 on MTN based on their latest set of financial results. While it is an increase on our valuation done in March 2019, its still lower than their current share price by about 10%, so we believe MTN is currently overvalued around 10%

Well their balance sheet is strong, they have a decent net profit margin. They do however continue to have regular clashes with the Nigerian authorities regarding penalties they need to pay and cash being repatriated out of the country, In addition to this they have a big market in Iran, from which they struggle to repatriate cash too since sanctions are often imposed on the country.

But with this all being said, their tougher markets are the more lucarative and their biggest markets so should there be no issues in these markets over the next couple of years MTN could see bumper profits coming from these countries which should be good for its share price. Based on current financials and future prospects our valuation model places a target price of R101.50 on MTN based on their latest set of financial results. While it is an increase on our valuation done in March 2019, its still lower than their current share price by about 10%, so we believe MTN is currently overvalued around 10%