|

Related Topics |

|

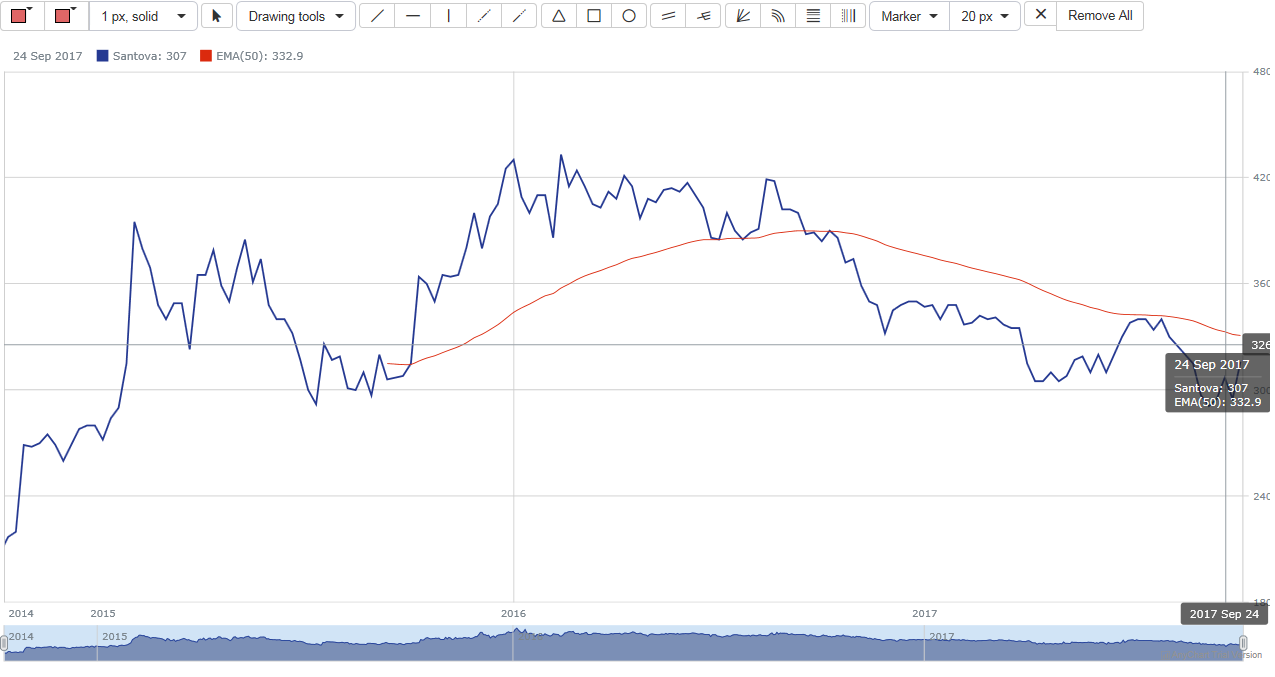

In today's blog we taking a quick look at Santova shipping while at the same time piloting our new interactive technical analysis chart (thanks to www.anychart.com) for the assitance in getting it into a workable format onto our site.

|

|

So what is Santova (SNV)?

Santova is a specialist international trade solutions business listed on the South Africa stock exchange with offices throughout South Africa, Ghana, Mauritius, Australia, Germany, Netherlands, United Kingdom, Hong Kong and Mainland China.

The Groups strategy is to continually develop and invest in key differentiators that set it apart from its competitors. This is achieved by offering select clients comprehensive supply chain solutions that enable them to achieve competitive advantage through multi-dimensional innovative global supply chain solutions.

As companies continue seeking worldwide sourcing and distributing products in multiple markets, they require extensive sophisticated operational and logistics solutions across geographies. Through being extremely client-centric in its approach, Santova is able to capitalise on its international offices, systems and processes and leverage off a borderless and integrated world economy which is driven by globalisation and technological advancements.

See their interactive chart below. Please feel free to play around with it

The Groups strategy is to continually develop and invest in key differentiators that set it apart from its competitors. This is achieved by offering select clients comprehensive supply chain solutions that enable them to achieve competitive advantage through multi-dimensional innovative global supply chain solutions.

As companies continue seeking worldwide sourcing and distributing products in multiple markets, they require extensive sophisticated operational and logistics solutions across geographies. Through being extremely client-centric in its approach, Santova is able to capitalise on its international offices, systems and processes and leverage off a borderless and integrated world economy which is driven by globalisation and technological advancements.

See their interactive chart below. Please feel free to play around with it

While we will be doing an updated valuation on Santova (SNV) soon below the comments from well known small caps website www.Smallcaps.co.za

Santova (SNV) is a non-asset based supply chain manager with more than 65% of its earnings coming from outside of South Africa, including the majority of hard currency in this.

For some background to the Group and my views on it, see my old articles over here (in reverse chronological order): Santova put out a H1:18 trading statement yesterday that can be summarised as follows:

Ignoring the recession’s impact, if we assume that Santova’s 65% offshore earnings would have added a further 10% from flat ZAR in H1:18 (i.e. constant currency), I arrive a HEPS growth of between 16% to 21%. Now imagine these results during a period of ZAR weakness…

Also, Santova achieved these results organically. This is always much higher quality than acquisitive growth. The latter comes with material risk and tends to once-off in nature too.

Subsequent to H1:18 and during H2:18, Santova has acquired the minorities out their profitable Australian business and the ZAR has weakened by about 7% against various hard currencies… Oh, and did I mention that South Africa is no longer in a recession?

In other words, despite Santova having a superb H1:18, I think they are actually going to have a better H2:18!

And, with all the boxes being ticked from profitability, growth and geographic diversification, Santova is also trading on a very low 7.9x Price Earnings (PE).

I hold Santova in the AWSM Fund and, personally, I wish various rules did not prohibit me from holding more of it at these levels (not my personal rules, but those of the CIS Act). I won’t state my fair valuation here, it just sounds ridiculous against the share price, but needless to say that I see it as worth materially more than where it is trading.

It is quite simple: Santova is proving its quality in this market, but the market has not yet responded by re-rating its share price. I am biased, but this is probably the cheapest stock on the JSE at this point.

Santova (SNV) is a non-asset based supply chain manager with more than 65% of its earnings coming from outside of South Africa, including the majority of hard currency in this.

For some background to the Group and my views on it, see my old articles over here (in reverse chronological order): Santova put out a H1:18 trading statement yesterday that can be summarised as follows:

- H1:18 EPS and HEPS expected to between +10% y/y to +15% y/y.

- This performance was underpinned by organic growth.

- The strong ZAR during this period actually saw the Group’s c.65% offshore earnings translated in less ZAR than they would have been in constant currency (and a mile worse than they would have been with a depreciating ZAR).

Ignoring the recession’s impact, if we assume that Santova’s 65% offshore earnings would have added a further 10% from flat ZAR in H1:18 (i.e. constant currency), I arrive a HEPS growth of between 16% to 21%. Now imagine these results during a period of ZAR weakness…

Also, Santova achieved these results organically. This is always much higher quality than acquisitive growth. The latter comes with material risk and tends to once-off in nature too.

Subsequent to H1:18 and during H2:18, Santova has acquired the minorities out their profitable Australian business and the ZAR has weakened by about 7% against various hard currencies… Oh, and did I mention that South Africa is no longer in a recession?

In other words, despite Santova having a superb H1:18, I think they are actually going to have a better H2:18!

And, with all the boxes being ticked from profitability, growth and geographic diversification, Santova is also trading on a very low 7.9x Price Earnings (PE).

I hold Santova in the AWSM Fund and, personally, I wish various rules did not prohibit me from holding more of it at these levels (not my personal rules, but those of the CIS Act). I won’t state my fair valuation here, it just sounds ridiculous against the share price, but needless to say that I see it as worth materially more than where it is trading.

It is quite simple: Santova is proving its quality in this market, but the market has not yet responded by re-rating its share price. I am biased, but this is probably the cheapest stock on the JSE at this point.