|

|

Category: Stock Market and SASOL

Share Price: R205.22 (down 4.4% for the day) Date: 24 February 2020 We take a look at SASOL's interim financial results for the period ending December 2019. And it a horrible set of financial numbers yet again for the petrochemicals giant. The stock is down -48.35% over the last 12 months and down -19.1% in the last month. Mr Market is not liking SASOL right now.

|

|

Related Topics

About SASOL

Sasol is an international integrated chemicals and energy company that leverages technologies and the expertise of our 31 270 people working in 32 countries. We develop and commercialise technologies, and build and operate world-scale facilities to produce a range of high-value product stream, including liquid fuels, chemicals and low-carbon electricity.

Sasol’s new value chain-based operating model came into effect in 2014. Towards this end, the Sasol Group is now organised into two upstream business units, three regional operating hubs, and four customer-facing strategic business units, supported by fit-for-purpose functions as reflected in our new Sasol website.

By combining the talent of our people and our technological advantage, Sasol has been a pioneer in innovation for over six decades. As market needs and stakeholder expectations have changed, so too have our methods, facilities and products, driving progress to deliver long-term shareholder value sustainably. The growth and enhancement of our foundation businesses in Southern Africa is complemented by the significant chapter of growth, Sasol has entered in its history.

At Sasol, we recognise the growing need for countries to secure supply of energy and chemicals. For many countries, specifically those with abundant hydrocarbons, in-country conversion of these resources into liquid fuels and chemicals goes a long way to boost national economies. Sasol’s focused and strong project pipeline means we are actively capitalising on the growth opportunities that play to our strengths in Southern Africa and North America. Our focus is creating value sustainably and we are proud to be taking this company, to new frontiers.

Sasol was established in 1950 in South Africa and we remain one of the country’s largest investors in capital projects, skills development and technological research and development. The company is listed on the JSE in South Africa and on the New York Stock Exchange in the United States.

Sasol’s new value chain-based operating model came into effect in 2014. Towards this end, the Sasol Group is now organised into two upstream business units, three regional operating hubs, and four customer-facing strategic business units, supported by fit-for-purpose functions as reflected in our new Sasol website.

By combining the talent of our people and our technological advantage, Sasol has been a pioneer in innovation for over six decades. As market needs and stakeholder expectations have changed, so too have our methods, facilities and products, driving progress to deliver long-term shareholder value sustainably. The growth and enhancement of our foundation businesses in Southern Africa is complemented by the significant chapter of growth, Sasol has entered in its history.

At Sasol, we recognise the growing need for countries to secure supply of energy and chemicals. For many countries, specifically those with abundant hydrocarbons, in-country conversion of these resources into liquid fuels and chemicals goes a long way to boost national economies. Sasol’s focused and strong project pipeline means we are actively capitalising on the growth opportunities that play to our strengths in Southern Africa and North America. Our focus is creating value sustainably and we are proud to be taking this company, to new frontiers.

Sasol was established in 1950 in South Africa and we remain one of the country’s largest investors in capital projects, skills development and technological research and development. The company is listed on the JSE in South Africa and on the New York Stock Exchange in the United States.

SASOL's commentary on their interim financial results for period ending December 2019

Reviewed interim financial results for the six months ended 31 December 2019

Earnings performance

We delivered a satisfactory set of business results for the six months ended 31 December 2019, with increased volumes while cost and working capital tracked our internal targets contributing to the balance sheet covenant levels being maintained within market guidance. The financial results were impacted mostly by a weak macroeconomic environment, which resulted in lower margins, and the LCCP being in a ramp-up phase.

Earnings decreased by 72% to R4,5 billion compared to the prior period. This resulted from a 9% decrease in the rand per barrel price of Brent crude oil, softer global chemical prices and refining margins, lower productivity at our Mining operations and a negative contribution from the LCCP. Our gross margin percentage decreased by 2% compared to the prior period driven by a softer macroeconomic environment negatively impacting supply-demand dynamics especially in our chemicals businesses. We anticipate softer chemical prices over the next 12 to 24 months and expect structural recovery over the medium to long-term. Our Energy business was impacted by lower crude oil prices as well as lower refining margins due to weaker demand.

As the LCCP units progress through the sequential beneficial operation schedule, our revenues do not yet match the costs expensed. We do expect that for the second half of FY20 revenue will match the costs expensed better and that the LCCP will generate positive earnings before interest, tax, depreciation and amortisation (EBITDA). The LCCP negatively impacted earnings by R2,8 billion (EBITDA of R1,1 billion and R1,7 billion in additional depreciation charges). Earnings were further impacted by approximately R2,0 billion in finance charges for the period as the LCCP units reach beneficial operation.

As a result of the aforementioned factors our key financial metrics were impacted as follows:

Net asset value Half Year December 2019 Half Year December 2019 % change

Total assets (R million) 486 345 472 461 3

Total liabilities (R million) 257 699 230 223 12

Total equity (R million) 228 646 242 238 -6

Dividend

After careful consideration of our current leverage and the volatility in the macroeconomic environment, the Board of directors (Board) decided to pass the interim dividend to protect and strengthen our balance sheet. This is a decision that was not taken lightly as we remain committed to delivering shareholder value, however, given the current position of our balance sheet, the Board made this decision in the long-term interest of our shareholders. We continue to ensure that we deliver the key elements of our strategy, particularly the completion of the LCCP.

Earnings performance

We delivered a satisfactory set of business results for the six months ended 31 December 2019, with increased volumes while cost and working capital tracked our internal targets contributing to the balance sheet covenant levels being maintained within market guidance. The financial results were impacted mostly by a weak macroeconomic environment, which resulted in lower margins, and the LCCP being in a ramp-up phase.

Earnings decreased by 72% to R4,5 billion compared to the prior period. This resulted from a 9% decrease in the rand per barrel price of Brent crude oil, softer global chemical prices and refining margins, lower productivity at our Mining operations and a negative contribution from the LCCP. Our gross margin percentage decreased by 2% compared to the prior period driven by a softer macroeconomic environment negatively impacting supply-demand dynamics especially in our chemicals businesses. We anticipate softer chemical prices over the next 12 to 24 months and expect structural recovery over the medium to long-term. Our Energy business was impacted by lower crude oil prices as well as lower refining margins due to weaker demand.

As the LCCP units progress through the sequential beneficial operation schedule, our revenues do not yet match the costs expensed. We do expect that for the second half of FY20 revenue will match the costs expensed better and that the LCCP will generate positive earnings before interest, tax, depreciation and amortisation (EBITDA). The LCCP negatively impacted earnings by R2,8 billion (EBITDA of R1,1 billion and R1,7 billion in additional depreciation charges). Earnings were further impacted by approximately R2,0 billion in finance charges for the period as the LCCP units reach beneficial operation.

As a result of the aforementioned factors our key financial metrics were impacted as follows:

- Earnings before interest and tax (EBIT) decreased by 53% to R9,9 billion compared to the prior period;

- Adjusted EBITDA(1) declined by 27% from R26,8 billion in the prior period to R19,6 billion;

- Basic earnings per share (EPS) decreased by 73% to R6,56 per share compared to the prior period;

- Headline earnings per share (HEPS) decreased by 74% to R5,94 per share compared to the prior period; and

- Core headline earnings per share(2) (CHEPS) decreased by 57% to R9,20 compared to the prior period.

Net asset value Half Year December 2019 Half Year December 2019 % change

Total assets (R million) 486 345 472 461 3

Total liabilities (R million) 257 699 230 223 12

Total equity (R million) 228 646 242 238 -6

Dividend

After careful consideration of our current leverage and the volatility in the macroeconomic environment, the Board of directors (Board) decided to pass the interim dividend to protect and strengthen our balance sheet. This is a decision that was not taken lightly as we remain committed to delivering shareholder value, however, given the current position of our balance sheet, the Board made this decision in the long-term interest of our shareholders. We continue to ensure that we deliver the key elements of our strategy, particularly the completion of the LCCP.

Advertisement

Update on SASOL's disastrous Lake Charles Chemicals Project

Update on the Lake Charles Chemicals Project (LCCP)

Ongoing focus as we ramp up plants to beneficial operation At the LCCP, we maintain our focus on safely improving productivity in the field and bringing the plants into beneficial operation. The project continued with its exceptional safety record with a recordable case rate (RCR) of 0,10. At the end of December 2019, engineering and procurement activities were substantially complete and construction progress was at 98%, with overall project completion at 99%. The investigation into the incident which occurred at the LDPE unit in January 2020 is complete.

The root cause analysis determined that a piping support structure, within the LDPE emergency vent system, failed during commissioning causing a pipe to dislodge. No major equipment was damaged, and the incident was isolated. Remediation has commenced, however, the replacement of the high pressure piping material components have long lead times. We expect beneficial operation of the LDPE unit to be delayed to the second half of calendar year 2020. Parallel commissioning activities on the remainder of the LDPE unit continue during remediation and every effort will be made to expedite the restoration project. The overall LCCP cost estimate is tracking US$12,8 billion, within our previous guidance of US$12,6 billion to US$12,9 billion, and our EBITDA estimate of US$50 million to US$100 million for FY20 remains. During the time of the delay in the LDPE unit startup, the ethylene produced by the cracker and destined for the unit is sold externally. All previously commissioned units were unaffected and are operating to plan.

The ETO unit, the fourth of seven units, achieved beneficial operation on 30 January 2020. The unit has a nameplate capacity of 100 kilo tons (kt) per year, forms part of our ethylene oxide value chain and adds to the capacity of our Performance Chemicals product volumes already produced and sold on both a regional and global scale. The ETO unit follows the linear low- density polyethylene (LLDPE), world-scale ethane cracker and ethylene oxide/ethylene glycol (EO/EG) facilities, which all reached beneficial operation last year and are operating to plan. This provides additional flexibility to our ethylene oxide value chain and will enable us to divert some volume away from the mono-ethylene glycol (MEG) product line and support increased margins. As previously communicated, we still expect the Ziegler and Guerbet plants to achieve beneficial operation in the last quarter of FY20.

The ethane cracker is ramping up following the successful replacement of the acetylene reactor catalyst in December 2019. The plant is expected to operate according to plan for the remainder of the year. The LLDPE plant and the EO value chain are ramping up to plan with our learnings to be carried over to the LDPE ramp-up. The LCCP remains a world-scale, first quartile feedstock-advantaged plant, highly integrated across a diverse product slate with high margin products and world class logistics and infrastructure. The short-term market outlook for ethane and product pricing remains volatile and estimates will be updated periodically. We expect EBITDA in the range of US$600 million to US$750 million for FY21.

Ongoing focus as we ramp up plants to beneficial operation At the LCCP, we maintain our focus on safely improving productivity in the field and bringing the plants into beneficial operation. The project continued with its exceptional safety record with a recordable case rate (RCR) of 0,10. At the end of December 2019, engineering and procurement activities were substantially complete and construction progress was at 98%, with overall project completion at 99%. The investigation into the incident which occurred at the LDPE unit in January 2020 is complete.

The root cause analysis determined that a piping support structure, within the LDPE emergency vent system, failed during commissioning causing a pipe to dislodge. No major equipment was damaged, and the incident was isolated. Remediation has commenced, however, the replacement of the high pressure piping material components have long lead times. We expect beneficial operation of the LDPE unit to be delayed to the second half of calendar year 2020. Parallel commissioning activities on the remainder of the LDPE unit continue during remediation and every effort will be made to expedite the restoration project. The overall LCCP cost estimate is tracking US$12,8 billion, within our previous guidance of US$12,6 billion to US$12,9 billion, and our EBITDA estimate of US$50 million to US$100 million for FY20 remains. During the time of the delay in the LDPE unit startup, the ethylene produced by the cracker and destined for the unit is sold externally. All previously commissioned units were unaffected and are operating to plan.

The ETO unit, the fourth of seven units, achieved beneficial operation on 30 January 2020. The unit has a nameplate capacity of 100 kilo tons (kt) per year, forms part of our ethylene oxide value chain and adds to the capacity of our Performance Chemicals product volumes already produced and sold on both a regional and global scale. The ETO unit follows the linear low- density polyethylene (LLDPE), world-scale ethane cracker and ethylene oxide/ethylene glycol (EO/EG) facilities, which all reached beneficial operation last year and are operating to plan. This provides additional flexibility to our ethylene oxide value chain and will enable us to divert some volume away from the mono-ethylene glycol (MEG) product line and support increased margins. As previously communicated, we still expect the Ziegler and Guerbet plants to achieve beneficial operation in the last quarter of FY20.

The ethane cracker is ramping up following the successful replacement of the acetylene reactor catalyst in December 2019. The plant is expected to operate according to plan for the remainder of the year. The LLDPE plant and the EO value chain are ramping up to plan with our learnings to be carried over to the LDPE ramp-up. The LCCP remains a world-scale, first quartile feedstock-advantaged plant, highly integrated across a diverse product slate with high margin products and world class logistics and infrastructure. The short-term market outlook for ethane and product pricing remains volatile and estimates will be updated periodically. We expect EBITDA in the range of US$600 million to US$750 million for FY21.

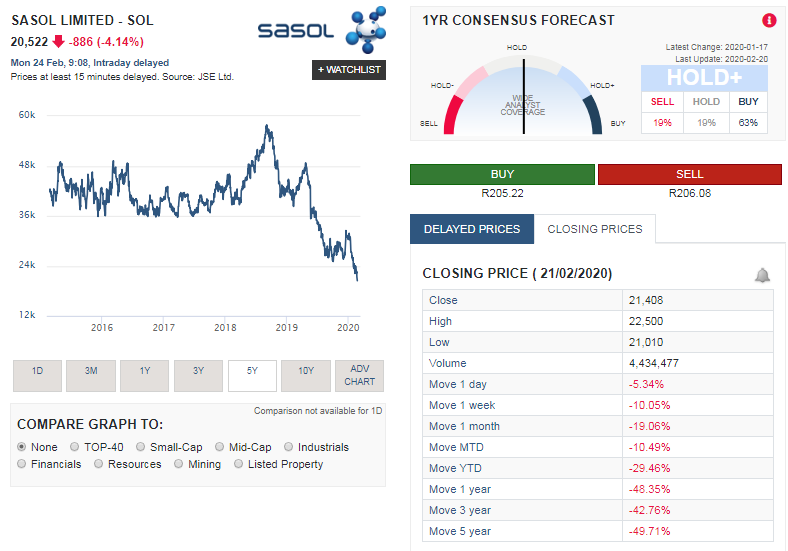

SASOL share price history over the last 5 years

The image below is a screenshot taken from sharenet showing SASOL's share price history over the last 5 years. And its pretty clear that since the start of 2018 its been a very tough time for the group, with the bulk of their issues emanating from the Lake Charles Chemicals Project (LCCP)

SASOL (SOL) share price plunge after it announced it is not paying an interim dividend

The summary below provides an overview of the share price performance of SASOL over various time periods:

The above is the last thing any shareholder would like to see. And based on the market's reaction to SASOL's latest interim financial results and the fact that it is not paying an interim dividend, we can expect more pain for SASOL shareholders in coming weeks and months

- 1 week: -10.05%

- 1 months: -19.06%

- Year to Date (YTD): -29.46%

- 1 year: -48.35%

- 3 years:-42.76%

- 5 years:-49.71%

The above is the last thing any shareholder would like to see. And based on the market's reaction to SASOL's latest interim financial results and the fact that it is not paying an interim dividend, we can expect more pain for SASOL shareholders in coming weeks and months

Summary of SASOL's latest results and share price valuation

So in summary one can say the following about SASOL's interim financial results. They are not paying an interim dividend, their core headline earnings per share declined from R21.45 a year ago to R9.20 now. Their total assets increased by 3% while their liabilities increased by a whopping 12%. In addition to that their total equity declined by 6% from R242.238 bilion down R14 billion to R228.646 billion.

Based on the group's prospects and the group's latest earnings and stopping the interim dividend we value the stock of SASOL at R167.90 a share. We therefore believe the stock of SASOL is overvalued and expect it to pull back from current levels to closer to our target price (full value price) in coming weeks and months.

Based on the group's prospects and the group's latest earnings and stopping the interim dividend we value the stock of SASOL at R167.90 a share. We therefore believe the stock of SASOL is overvalued and expect it to pull back from current levels to closer to our target price (full value price) in coming weeks and months.