|

Related Topics |

|

We take a look at the latest financial results of clothing and fashion giant Truworths International. With South Africa's economy struggling and world growth slowing down has the group been able to weather the tough economic times its operating in?

|

|

About Truworths International (TRU)

OUR BUSINESS

Welcome to Truworths, one of South Africa's leading fashion retailers, with over 728 stores in South Africa and 49 in the rest of Africa.Truworths forms part of Truworths International, an investment holding company listed on the JSE, whose companies are engaged in the retailing of fashion apparel and accessories. The Truworths International Retail Group incorporates Identity, YDE and Uzzi.

OUR PHILOSOPHY

The Truworths business model is driven by a philosophy that has been developed and refined over many years in pursuit of a unique approach to achieve sustainable growth in the complex and fast-moving retail fashion environment.

A major asset in this pursuit has been the strength of the Truworths brand, which represents an innovative, South African interpretation of fashion trends and attractive styling, competitive with the highest international standards, to youthful, fashionable consumers. MORE

We strive to:

INTERNATIONAL

Truworths International currently comprises Truworths Limited and the international franchise operations.

Truworths Limited is a leading South African retailer of fashion merchandise. The operation has developed a range of specialised retail formats including Truworths Woman, Truworths Man, Daniel Hechter, Inwear and LTD. Key to Truworths' success has been the development of stores as brands and brands as stores. Truworths has become the destination of choice for fashionable individuals in search of quality fashion that makes them look attractive and successful, and feel enthused with confidence.

RETAIL OPERATIONS

We strive to provide an enticing, exciting and visually appealing fashion retail environment where our customers can shop effortlessly, assisted by energetic, committed people. It is essential that store ambience reflects and enhances customer confidence in our offering of an innovative and adventurous blend of colour, fabric and fashion styling of international standards.

Regular market surveys indicate that excellent standards of service and visual merchandise presentation have been maintained. This has been achieved in conjunction with an improvement in productivity and profitability.

BRANDS

Below a few of Truworths brands that they own and sell at their stores.

Welcome to Truworths, one of South Africa's leading fashion retailers, with over 728 stores in South Africa and 49 in the rest of Africa.Truworths forms part of Truworths International, an investment holding company listed on the JSE, whose companies are engaged in the retailing of fashion apparel and accessories. The Truworths International Retail Group incorporates Identity, YDE and Uzzi.

OUR PHILOSOPHY

The Truworths business model is driven by a philosophy that has been developed and refined over many years in pursuit of a unique approach to achieve sustainable growth in the complex and fast-moving retail fashion environment.

A major asset in this pursuit has been the strength of the Truworths brand, which represents an innovative, South African interpretation of fashion trends and attractive styling, competitive with the highest international standards, to youthful, fashionable consumers. MORE

We strive to:

- Make the Truworths brand of fashion merchandise the most aspirational, innovative and adventurous blend of colour, fabric, value and fashion styling

- Make the Truworths store - the brand destination - the most enticing, visually appealing and effortless retail shopping environment

- Engage and energise our people, who personify the brand

- Lead and motivate our staff to deliver consistently in the context of our value system, so that we continue to build brand integrity.

INTERNATIONAL

Truworths International currently comprises Truworths Limited and the international franchise operations.

Truworths Limited is a leading South African retailer of fashion merchandise. The operation has developed a range of specialised retail formats including Truworths Woman, Truworths Man, Daniel Hechter, Inwear and LTD. Key to Truworths' success has been the development of stores as brands and brands as stores. Truworths has become the destination of choice for fashionable individuals in search of quality fashion that makes them look attractive and successful, and feel enthused with confidence.

RETAIL OPERATIONS

We strive to provide an enticing, exciting and visually appealing fashion retail environment where our customers can shop effortlessly, assisted by energetic, committed people. It is essential that store ambience reflects and enhances customer confidence in our offering of an innovative and adventurous blend of colour, fabric and fashion styling of international standards.

Regular market surveys indicate that excellent standards of service and visual merchandise presentation have been maintained. This has been achieved in conjunction with an improvement in productivity and profitability.

BRANDS

Below a few of Truworths brands that they own and sell at their stores.

- Daniel Hetcher

- EARTHADDICT

- EARTHCHILD

- Uzzi

- Hemisphere

- LTD

- LTD kids

- Naartjie

- Hey Betty

- Ginger Mary

Advertisement

So to the numbers we go

Highlights of Truworths International financial results as highlighted by the group

The numbers we are interested in are discussed below:

- Retail sales up 3.7% to R18.6 billion

- Gross margin at 51.6%

- Operating margin at 9.1%

- Profit before tax down 57.5%

- Diluted earnings per share down 66.8%

- Diluted headline earnings per share - Group down 8.5%

- Diluted headline earnings per share - Truworths Africa segment down 2.5%

- Diluted headline earnings per share - Office segment down 60.0%

- Net asset value per share down 10.9%

- Office intangible assets impaired by £97 million

- Cash generated from operations R2.7 billion

- Net debt to equity at 7.2%

- Cash realisation rate of 93%

- Annual dividend per share of 384 cents (2018: 420 cents)

The numbers we are interested in are discussed below:

- Revenue: R19.577 billion (up 1.7%)

- Cost of sales: R8.78 billion (up 3.1%)

- Profit for the period: R691 million

- Basic earnings per share: R2.03

- Headline earnings per share: R5.62

- Diluted headline earnings per share: R5.60

- Cash generated per share: R6.83

- Net asset value per share: R21.38 (so trading at 2.7 times its book value)

- Cash on balance sheet per share: R1.81 (so about3.12% of the company's share price is made up by cash on balance sheet)

- Net debt to equity : 7.2%

- Return on equity: 9%

- Return on assets: 12%

- Dividend yield: 6.6%

So any comments or guidance from management on the results?

The Group continued to experience difficult trading conditions in both its primary markets. Low economic growth, high unemployment, modest increases in negotiated wages and higher average fuel and utility prices contributed to low consumer confidence and constrained spending in South Africa. In the UK, Brexit uncertainty and muted consumer sentiment, combined with the pressure on store-based retailing as consumer spending shifts to online shopping, continue to negatively impact the economy and retail sector in particular. Group retail sales for the current period increased 3.7% to R18.6 billion relative to the R18.0 billion reported for the prior period. Account sales comprised 51% (2018: 50%) of Group retail sales for the current period, with account and cash sales increasing by 4.5% and 2.8% respectively, relative to the prior period.

Retail sales for Truworths Africa (being the Group, excluding the UK-based Office segment and comprising mainly the Truworths businesses in South Africa) increased by 3.1% to R13.5 billion relative to the prior period’s R13.1 billion, with account sales increasing by 4.5% and cash sales decreasing by 0.1%. The improvement in the retail sales performance of Truworths Africa in the second half of the current period is encouraging, with retail sales growing by 3.9% relative to the corresponding prior period (first half: growing 2.4%), mainly driven by account retail sales recording an increase of 5.6% in the second half. Account sales comprised 70% of retail sales (2018: 69%). In Truworths Africa like-forlike store retail sales increased by 0.7%. Product deflation averaged 0.2% for the current period (2018: 1.4% deflation).

Retail sales for the Group’s UK-based Office segment (Office) decreased in Sterling terms by 0.9% to £279 million relative to the prior period’s £281 million. In Rand terms, however, retail sales for Office increased by 5.3% to R5.1 billion. Retail sales in the second half of the current period performed substantially better in Sterling terms, growing at 2.0% (first half: decreasing 3.0%), as a result of an increase in sales of marked-down merchandise. The Office segment continued to show good online performance, with online retail sales growing at 9.8% and comprising 33.8% of retail sales for the current period.

Group sale of merchandise, which comprises Group retail sales, together with wholesale and franchise sales and delivery fee income, less accounting adjustments (refer to note 4 for further information), increased 3.1% to R18.1 billion. Since the prior period-end a net 24 stores were closed across all brands. Truworths Africa opened 23 stores and closed 30, while Office closed 17 stores (of which 16 were concession stores across House of Fraser and Topshop/Topman), resulting in an increase in trading space of 1.3% (Truworths increase of 1.6% and Office decrease of 5.2%). At the end of the current period the Group had 945 stores (including 24 concession outlets) (2018: 969 stores, including 40 concession outlets). The Group’s gross margin reduced to 51.6% (2018: 52.4%).

Truworths Africa’s gross margin was unchanged at 55.5%, while the gross margin in Office declined from 44.4% in the prior period to 42.3%, mainly due to a decline in the full price versus markdown sales mix. The continuingly tough trading environment in the UK has impacted the profitability of the Office segment, necessitating a reassessment by management of the carrying value of the Office segment’s assets. This has resulted in a non-cash impairment charge of £97 million (£102 million excluding the impact of deferred tax in relation to trademarks), hereinafter referred to as the Office impairment, being raised against the Office intangible assets.

Trading expenses for the current period, inclusive of the Office impairment, increased by 31.9% to R9.2 billion, constituting 50.7% of sale of merchandise. Excluding the Office impairment and other adjustments referred to in note 16, trading expenses increased by 6.3% and constituted 41.0% (2018: 39.8%) of sale of merchandise. Refer to Account Management below for further details on trade receivable costs. Group trading profit for the current period decreased 80.5% to R492 million, primarily due to the Office impairment. On an adjusted basis, Group trading profit decreased 9.8% to R2.2 billion (refer to note 16 for further information). Interest received decreased 18.8% to R1.2 billion (2018: R1.4 billion). Excluding the reclassification of interest received in respect of stage 3 trade receivables in terms of IFRS 9 (R106 million), interest received decreased 11.3%. This decrease was primarily the result of the deployment of cash in the restructuring of the South African funding arrangements in June 2018 (refer to note 11 for further information).

Group operating profit for the current period decreased 58.1% to R1.7 billion, resulting in an operating margin of 9.1%. On an adjusted basis, Group operating profit decreased by 10.3% to R3.5 billion and the operating margin decreased from 22.3% in the prior period to 19.4% (refer to note 16 for further information). The operating margin of Truworths Africa decreased to 26.4% (2018: 29.1%). Finance costs decreased materially by 66.4% from R250 million in the prior period to R84 million, reflecting the benefits of the restructuring of the Group’s South African funding arrangements undertaken in 2018.

Retail sales for Truworths Africa (being the Group, excluding the UK-based Office segment and comprising mainly the Truworths businesses in South Africa) increased by 3.1% to R13.5 billion relative to the prior period’s R13.1 billion, with account sales increasing by 4.5% and cash sales decreasing by 0.1%. The improvement in the retail sales performance of Truworths Africa in the second half of the current period is encouraging, with retail sales growing by 3.9% relative to the corresponding prior period (first half: growing 2.4%), mainly driven by account retail sales recording an increase of 5.6% in the second half. Account sales comprised 70% of retail sales (2018: 69%). In Truworths Africa like-forlike store retail sales increased by 0.7%. Product deflation averaged 0.2% for the current period (2018: 1.4% deflation).

Retail sales for the Group’s UK-based Office segment (Office) decreased in Sterling terms by 0.9% to £279 million relative to the prior period’s £281 million. In Rand terms, however, retail sales for Office increased by 5.3% to R5.1 billion. Retail sales in the second half of the current period performed substantially better in Sterling terms, growing at 2.0% (first half: decreasing 3.0%), as a result of an increase in sales of marked-down merchandise. The Office segment continued to show good online performance, with online retail sales growing at 9.8% and comprising 33.8% of retail sales for the current period.

Group sale of merchandise, which comprises Group retail sales, together with wholesale and franchise sales and delivery fee income, less accounting adjustments (refer to note 4 for further information), increased 3.1% to R18.1 billion. Since the prior period-end a net 24 stores were closed across all brands. Truworths Africa opened 23 stores and closed 30, while Office closed 17 stores (of which 16 were concession stores across House of Fraser and Topshop/Topman), resulting in an increase in trading space of 1.3% (Truworths increase of 1.6% and Office decrease of 5.2%). At the end of the current period the Group had 945 stores (including 24 concession outlets) (2018: 969 stores, including 40 concession outlets). The Group’s gross margin reduced to 51.6% (2018: 52.4%).

Truworths Africa’s gross margin was unchanged at 55.5%, while the gross margin in Office declined from 44.4% in the prior period to 42.3%, mainly due to a decline in the full price versus markdown sales mix. The continuingly tough trading environment in the UK has impacted the profitability of the Office segment, necessitating a reassessment by management of the carrying value of the Office segment’s assets. This has resulted in a non-cash impairment charge of £97 million (£102 million excluding the impact of deferred tax in relation to trademarks), hereinafter referred to as the Office impairment, being raised against the Office intangible assets.

Trading expenses for the current period, inclusive of the Office impairment, increased by 31.9% to R9.2 billion, constituting 50.7% of sale of merchandise. Excluding the Office impairment and other adjustments referred to in note 16, trading expenses increased by 6.3% and constituted 41.0% (2018: 39.8%) of sale of merchandise. Refer to Account Management below for further details on trade receivable costs. Group trading profit for the current period decreased 80.5% to R492 million, primarily due to the Office impairment. On an adjusted basis, Group trading profit decreased 9.8% to R2.2 billion (refer to note 16 for further information). Interest received decreased 18.8% to R1.2 billion (2018: R1.4 billion). Excluding the reclassification of interest received in respect of stage 3 trade receivables in terms of IFRS 9 (R106 million), interest received decreased 11.3%. This decrease was primarily the result of the deployment of cash in the restructuring of the South African funding arrangements in June 2018 (refer to note 11 for further information).

Group operating profit for the current period decreased 58.1% to R1.7 billion, resulting in an operating margin of 9.1%. On an adjusted basis, Group operating profit decreased by 10.3% to R3.5 billion and the operating margin decreased from 22.3% in the prior period to 19.4% (refer to note 16 for further information). The operating margin of Truworths Africa decreased to 26.4% (2018: 29.1%). Finance costs decreased materially by 66.4% from R250 million in the prior period to R84 million, reflecting the benefits of the restructuring of the Group’s South African funding arrangements undertaken in 2018.

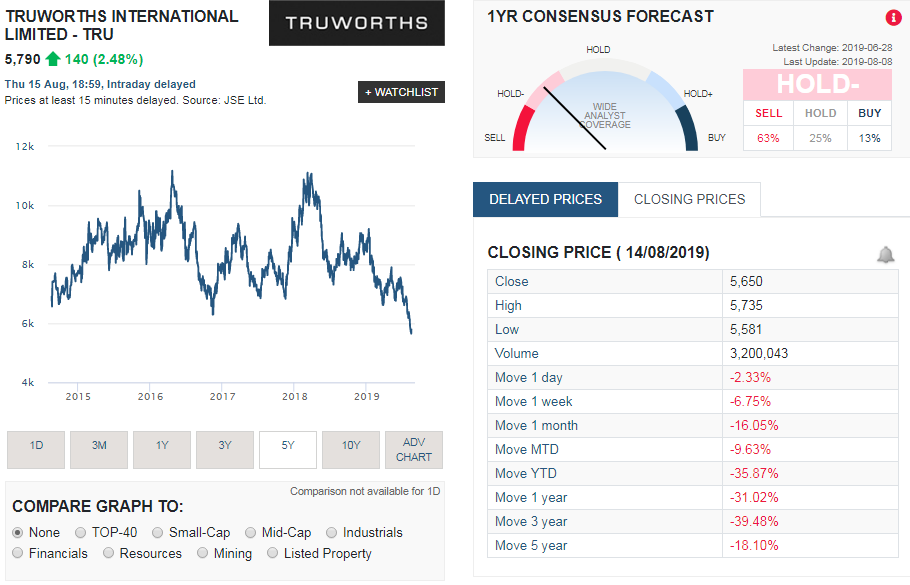

Truworths (TRU) share price history

The image below (taken from Sharenet) shows the share price performance of Truworths over the last 5 years. And as the image shows its been a pretty volatile ride for Truworths investors but the bias has been towards the down side as shown by the negative returns over various time periods to the right of the image.

The summary below shows the share price performance of Truworths (TRU) over various time periods:

- 1 week: -6.75%

- 1 month: -16.05%

- Year to Date (YTD): -35.87%

- 1 year: -31.02%

- 3 years: -39.48%

- 5 years: -18.10%

So should you buy their shares?

Well they do cover a very large chunk of the clothing retail sector in South Africa, so they should be included in any long term portfolio that is looking to spread and cover large sectors of the South African economy. While the sector is prone to very volatile earnings, as fashion products can be a hit or miss with clients and its something one wouldn't know until products hit the shelf, it is very hard to reliably estimate their earnings potential. The other worry for the group recently has been their UK operations (we sound like a broken records with all the SA companies struggling to make it in the UK). Think of Famous Brands for example.

Truworths International valuation

Based on Truworths financial results, their issues in the UK, their strong balance sheet and cash generation capacity and the healthy dividend yield of 6.6% all things considered we value Truworths International (TRU) at R80.68 a share. So at the current price we do believe the group offers value. Its recent decline due to the news about their problems in the UK has created a great buying opportunity for long term investors. The group's share price has declined almost as much in the last month as it has over the last 5 years. We think there is strong long term gains to be made if the shares are bought and the current price and the fat divided yield doesn't hurt either.