|

Related Topics |

|

We take a look at the final financial results of Woolworths, one of South Africa's largest retailers. They are active in the fashion and beauty and food space, and also hold significant stakes in Australian clothing retailers David Jones and Country Road. But Woolies Foods is the crown jewel of the group.

|

|

About Woolworths

The first Woolworths store opened its doors to the public in Cape Town in October 1931. And it was founder Max Sonnenberg who captured the public’s imagination with dynamic store policies that set Woolworths apart from its competitors. Three years later, a second branch opened in Durban, with another two in Port Elizabeth and Johannesburg a year later. And since then we’ve been building on our reputation for superior quality, exciting innovation and excellent value.

At Woolworths we take our business values seriously. They aren’t just words in an annual report - they are the foundation of our business. They give us direction and guide our behaviour, actions and choices. In fact, our values are so important to us that we’re measured not only on our performance, but also by how well we live up to them.

- FIRST TO OFFER EMPLOYEE BENEFITSKeen to attract and retain the best retail professionals, Woolworths was among the first local retailers to offer employees a pension fund, medical aid and maternity leave.

- FIRST IN ADVANCING TECHNot just a forward thinking employer, Woolworths was also an early adopter of technology. A lease agreement for the first computer was agreed to with National Cash Registers (NCR) in the late 60s and Woolworths was already using a computerised merchandising system by the early 1970s.

- FIRST TO INTRODUCE SELL BY DATESThis dynamic thinking extends to Woolworths product offering. In 1974, Woolworths became the first South African retailer to introduce ‘sell by’ dates on food packaging. Convenience, too, has long been a watchword at Woolworths - we were the first South African retailer to offer pre-washed lettuce and machine-washable wool clothing to consumers.

- OUR GOOD BUSINESS JOURNEYIn April 2007, we launched our Good Business Journey – a bold plan to make a difference in eight key areas on our journey towards sustainability: Energy, Water, Waste, Sustainable Farming, Ethical Sourcing, Transformation, Social Development and Health and Wellness. Read more about our Good Business Journey

At Woolworths we take our business values seriously. They aren’t just words in an annual report - they are the foundation of our business. They give us direction and guide our behaviour, actions and choices. In fact, our values are so important to us that we’re measured not only on our performance, but also by how well we live up to them.

- QUALITY AND STYLE - DELIVER THE BESTIt means giving 100%, 100% of the time. Whether it’s making sure that a supplier is delivering to the standards we set or preparing a report, it all boils down to one thing: there’s no compromising on quality, because ‘good enough’ just isn’t good enough.

- VALUE - A SIMPLE AND FAIR DEALOffering real value goes beyond offering our customers quality at a good price: it also means offering value to each other, from sharing our knowledge with colleagues and suppliers to being able to evaluate how the decisions we make affect the business.

- SERVICE - WE ALWAYS THINK CUSTOMERAt Woolies, we know that we have to go that bit further to really make a difference. Putting the customer first is what service is all about. Whether your customer is a shopper in our stores or the store manager who needs a vital delivery, service is about understanding others’ needs, being willing to do more than is expected, and being a good ambassador for the Woolies brand.

- INNOVATION - DISCOVER THE DIFFERENCEWe do it for our customers. We love discovering new ideas, new products and new processes. We enjoy thinking ‘out of the box’ and finding solutions that benefit the business.

- INTEGRITY - DOING WHAT YOU SAY YOU WILL DOKeeping our promises is important to us, whether it’s maintaining confidentiality, not accepting gifts from suppliers, or simply listening to what others have to say with an open mind. By being true to ourselves, we earn the trust of our colleagues and our customers.

- ENERGY - BE PASSIONATE AND DELIVERWhen you’re passionate about what you do, when you really care, your enthusiasm and belief rub off on others. At Woolies, you’re part of a 23 000-member team. Being part of a team means being an inspiration to others and being inspired by their successes and triumphs.

- SUSTAINABILITY - BUILD FOR A BETTER FUTUREWhile you may be familiar with some of our environmental and conservation projects, for us in a South African, and African, context, sustainability isn’t just about being ‘green’. It’s about sharing expertise, helping local enterprises to grow, and contributing to a prosperous, secure future for our country. Please see more about our Good Business Journey.

Woolworths store in East London 1948

Financial results overview

The numbers we are interested in:

- Revenue: R75.179 billion (up 6.5% from R70.572 billion in the prior year)

- Cost of sales: R45.139 billion (up 8.2% from R41.700 billion in the prior year)

- Operating profit for the year: R5 121 (down 2.6% from R5.259 billion in the prior year)

- Loss for the year: -R1.086 billion (due to a R6.1 billion impairment on David Jones)

- Diluted earnings per share: -R1.13 (an improvement from -R3.69 in the prior year)

- Dividend for the final period: R0.985 a share (down -24.5% compared to the prior year)

- Dividend yield: 3.53%

- Cash generated from operations: R6.3 billion

- Cash generated from operations per share: R6.57 a share

- Cash on balance sheet: R1.9 billion

- Cash on balance sheet per share: R1.98 a share (or 3.6% of the company's current share price)

- Net asset value per share: R9.81(so trading at close to 3 times its net asset value)

- Inventories sitting at: R8.23 billion (up R1.152 billion from the prior year)

- Inventories makes up 23% of the group's total assets

- Inventories makes up 23% of the group's total assets

- Trade and other receivables (money owed to the group: R1.4 billion

- Trade and other receivables makes up 3.9% of the group's total assets

- Trade and other receivables makes up 3.9% of the group's total assets

Management comment on the results

Challenging economic and trading conditions in both South Africa and Australia continued to weigh on Group results. In South Africa, a steady improvement in the Woolworths Fashion business was experienced throughout the second half of the year. In Australia, David Jones experienced peak disruption from the refurbishment of the company’s flagship Sydney store, impacting their sales by approximately 3.0% in the second half of the year. An impairment charge of A$437.4 million (net of deferred tax) was recognised at 30 June 2019, reducing the valuation of David Jones to approximately A$965.0 million. A strategic review of the David Jones store portfolio also identified stores with onerous leases, resulting in an additional provision of A$22.4 million. The impairment reflects the economic headwinds and the accelerating structural changes affecting the Australian retail sector as well as the performance of the business, which has fallen short of expectations.

The WHL Board believes that the valuation of David Jones is realistic and reflective of its prospects. The Board is focused on the turnaround of David Jones and is ensuring that the business effects the necessary actions. Our statutory financial results are prepared on a 53-week basis. However, to facilitate comparison against the prior year, this commentary refers to a pro forma 52-week period, and excludes the impact of IFRS 15.

Woolworths SA (’WSA’)

Sales for the year increased by 5.8%, buoyed by an acceleration in the second half of 8.0%, with stronger performances in the second half from both the Fashion and Food businesses. Our online business grew by 28.7%, contributing 1.0% to total sales.

Woolworths Fashion, Beauty and Home (’FBH’)

Sales increased by 1.5% for the year (comparable store sales up 1.0%), with second half sales up 5.5%, as a result of the focus on core ranges and basics, backed by improved availability. Price movement for the year for Fashion was 2.5%. Net retail space declined by 0.1%, with the focus on productivity and operating efficiencies in existing space. Gross profit margin increased by 0.9% to 47.6%, as a result of lower markdowns. Expenses grew by 5.1%, while store costs increased by 3.5%. Operating profit declined by 1.1% to R1 688 million, with an operating margin of 12.1%, with operating profit increasing in the second half by 15.7%.

Woolworths Food

Sales increased by 7.7% for the year (comparable store sales 5.4% up), with second half growth of 9.0%, driven by further investment in price, innovation and convenience, resulting in strong volume growth. Price movement was 1.8% and net space grew by 2.0%. Gross profit margin was 0.1% lower than the prior period as a result of the price investment. Expenses grew by 7.5% and operating profit increased by 5.4% to R2 283 million, with an operating margin of 7.2%.

Woolworths Financial Services

The Woolworths Financial Services book reflected positive year-on-year growth of 7.4%. The impairment rate for the 12 months ended 30 June 2019 was 3.7% under IFRS 9 (4.6% adjusted under IAS 39). The Group implemented IFRS 9 with effect from the beginning of the 2019 financial year.

David Jones

Turnover and concession sales declined by 0.8% for the year, with comparable store sales 0.1% lower. The Elizabeth Street store refurbishment is on track to be completed by the end of the third quarter of the 2020 financial year. Net retail space grew by 0.4% with the opening of two new stores. Space reduction to improve the productivity of the existing store portfolio is a priority. Following the recent re-platforming of our online business, we have seen significant growth in online sales of 46.8%, now contributing 7.7% to total sales. Gross profit margin was 1.1% lower than the prior period as a result of higher markdowns and an increased focus on clearance. Store costs increased by 1.9%, while other operating costs were 6.6% lower as a result of various cost savings initiatives. Operating profit declined to A$37.0 million with an operating margin of 1.7%. The Elizabeth Street store’s fashion and beauty floors will be completed ahead of the Christmas trading period, with the below-ground food and home floors opening in March 2020.

Country Road Group

Sales for the year grew by 0.5% (comparable store sales 0.6% lower), with sales growth slowing in the second half in line with the market. Online sales in Australasia grew by 12.9%, representing 20.3% of sales. Net retail space reduced by 2.9% with further space reduction a priority as the contribution from online sales increases. Gross profit margin improved by 0.6% to 63.4% due to higher full-priced sales and improved sourcing. Expenses grew by 2.3% and operating profit decreased by 2.9% to A$100.0 million, resulting in an operating margin of 9.3%

Group earnings

Headline earnings per share (’HEPS’) and adjusted diluted HEPS, both of which exclude the impairment of David Jones assets, decreased by 4.6% and 2.1% respectively, on a comparable 52-week basis. Earnings per share, which includes the impairment, was -126.0 cents for the 52-week comparable period.

Outlook

In South Africa, consumer spending is expected to remain constrained. However, we expect Food to continue to trade ahead of the market and for FBH to continue its turnaround. In Australia, we believe the retail market will continue to be tough with heavy discounting and promotional activity. We remain committed to delivering our strategies and invest in initiatives that drive growth and efficiencies, while focusing on reducing costs, improving cash flows and strengthening the balance sheet.

The WHL Board believes that the valuation of David Jones is realistic and reflective of its prospects. The Board is focused on the turnaround of David Jones and is ensuring that the business effects the necessary actions. Our statutory financial results are prepared on a 53-week basis. However, to facilitate comparison against the prior year, this commentary refers to a pro forma 52-week period, and excludes the impact of IFRS 15.

Woolworths SA (’WSA’)

Sales for the year increased by 5.8%, buoyed by an acceleration in the second half of 8.0%, with stronger performances in the second half from both the Fashion and Food businesses. Our online business grew by 28.7%, contributing 1.0% to total sales.

Woolworths Fashion, Beauty and Home (’FBH’)

Sales increased by 1.5% for the year (comparable store sales up 1.0%), with second half sales up 5.5%, as a result of the focus on core ranges and basics, backed by improved availability. Price movement for the year for Fashion was 2.5%. Net retail space declined by 0.1%, with the focus on productivity and operating efficiencies in existing space. Gross profit margin increased by 0.9% to 47.6%, as a result of lower markdowns. Expenses grew by 5.1%, while store costs increased by 3.5%. Operating profit declined by 1.1% to R1 688 million, with an operating margin of 12.1%, with operating profit increasing in the second half by 15.7%.

Woolworths Food

Sales increased by 7.7% for the year (comparable store sales 5.4% up), with second half growth of 9.0%, driven by further investment in price, innovation and convenience, resulting in strong volume growth. Price movement was 1.8% and net space grew by 2.0%. Gross profit margin was 0.1% lower than the prior period as a result of the price investment. Expenses grew by 7.5% and operating profit increased by 5.4% to R2 283 million, with an operating margin of 7.2%.

Woolworths Financial Services

The Woolworths Financial Services book reflected positive year-on-year growth of 7.4%. The impairment rate for the 12 months ended 30 June 2019 was 3.7% under IFRS 9 (4.6% adjusted under IAS 39). The Group implemented IFRS 9 with effect from the beginning of the 2019 financial year.

David Jones

Turnover and concession sales declined by 0.8% for the year, with comparable store sales 0.1% lower. The Elizabeth Street store refurbishment is on track to be completed by the end of the third quarter of the 2020 financial year. Net retail space grew by 0.4% with the opening of two new stores. Space reduction to improve the productivity of the existing store portfolio is a priority. Following the recent re-platforming of our online business, we have seen significant growth in online sales of 46.8%, now contributing 7.7% to total sales. Gross profit margin was 1.1% lower than the prior period as a result of higher markdowns and an increased focus on clearance. Store costs increased by 1.9%, while other operating costs were 6.6% lower as a result of various cost savings initiatives. Operating profit declined to A$37.0 million with an operating margin of 1.7%. The Elizabeth Street store’s fashion and beauty floors will be completed ahead of the Christmas trading period, with the below-ground food and home floors opening in March 2020.

Country Road Group

Sales for the year grew by 0.5% (comparable store sales 0.6% lower), with sales growth slowing in the second half in line with the market. Online sales in Australasia grew by 12.9%, representing 20.3% of sales. Net retail space reduced by 2.9% with further space reduction a priority as the contribution from online sales increases. Gross profit margin improved by 0.6% to 63.4% due to higher full-priced sales and improved sourcing. Expenses grew by 2.3% and operating profit decreased by 2.9% to A$100.0 million, resulting in an operating margin of 9.3%

Group earnings

Headline earnings per share (’HEPS’) and adjusted diluted HEPS, both of which exclude the impairment of David Jones assets, decreased by 4.6% and 2.1% respectively, on a comparable 52-week basis. Earnings per share, which includes the impairment, was -126.0 cents for the 52-week comparable period.

Outlook

In South Africa, consumer spending is expected to remain constrained. However, we expect Food to continue to trade ahead of the market and for FBH to continue its turnaround. In Australia, we believe the retail market will continue to be tough with heavy discounting and promotional activity. We remain committed to delivering our strategies and invest in initiatives that drive growth and efficiencies, while focusing on reducing costs, improving cash flows and strengthening the balance sheet.

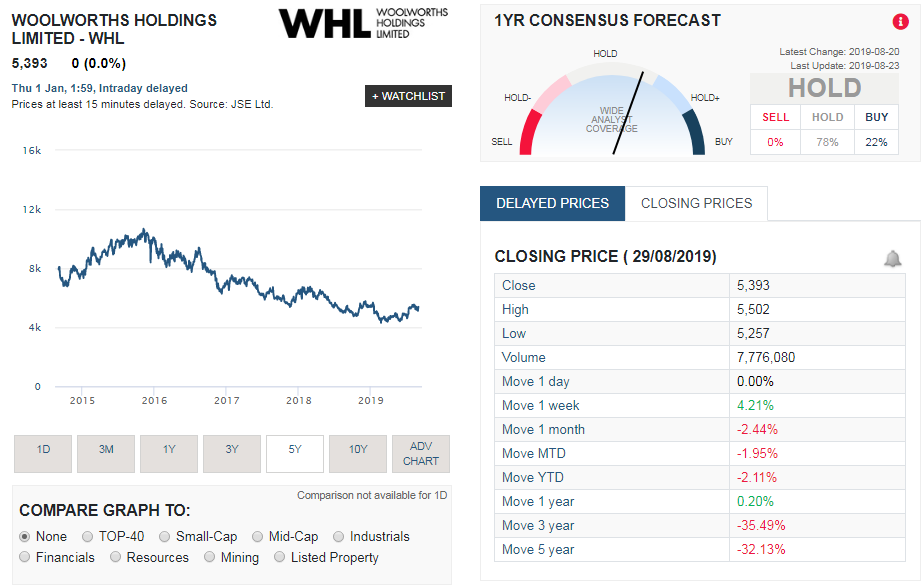

Woolworths (WHL) share price performance

The screenshot of Woolworths share price performance taken from Sharenet below shows that WHL has been struggling for years and investors in the stock probably wonder if there is ever any end in sight for the decline in the company's share price

- Last Week: 4.21%

- Month to Date (MTD) : -2.44%

- Year to Date (YTD): -2.11%

- 1 year move: 0.2%

- 3 year move: -35.49%

- 5 year move: - 32.13%

Wooloworths (WHL) share price history

Woolworths (WHL) share valuation

In our February 2019 valuation of Woolworths we valued WHL shares at R52.78 a share. So the question is based on their latest financial results what do we value the group's shares at now ? Based on the current results, the dim outlook and the continued costs being incurred at David Jones we value the group's shares at R58.60 a share