|

Related Topics |

|

We take a look at the interim results for the period ending end of August 2018 of Cartrack, the group active in the car, bike and asset tracking industry.

|

|

About Cartrack

So what exactly does Cartrack do and in which markets do they operate in? Well the following section will provide more details regarding the group's operations, services and markets they operate it.

Cartrack commenced operations in 2004 and listed on the Johannesburg Stock Exchange as Cartrack Holdings Limited in 2014 Sharecode (CTK). Cartrack has developed into a leading global provider of Fleet Management, Stolen Vehicle Recovery and Insurance telematics services with a strong focus on technology development to enhance customer experience. An extensive footprint is already well established in Africa, Europe and South East Asia; more recently, operations have been opened in America and New Zealand.

Cartrack is a service-centric organisation supported by a strong focus on in-house design, development and installation of Telematics technology and data analytics. Cartrack provides fleet, mobile asset and workforce management solutions underpinned by real-time actionable business intelligence, delivered as Software-as-a-Service (‘SaaS’), plus the service of tracking and recovery of stolen vehicles.

Our technology is widely accepted by motor manufacturers and insurers, with hardware and installations being of the highest standard. Cartrack’s user-friendly and cost-effective web-based Fleet Management portal provides a comprehensive set of features ensuring the optimisation of both fleet and human resources. To expand its integrated service offering, Cartrack is providing driver risk assessment offerings in the field of Insurance Telematics.

Cartrack also specialises in vehicle tracking and recovery, providing an invaluable service to combat vehicle theft in countries where crime is prevalent. Demonstrating its confidence in its systems, Cartrack was the first company globally to offer a cash back recovery warranty of up to R150 000 to its customers in the unlikely event of non-recovery of their stolen vehicles. An industry leading audited recovery rate of 91% in South Africa is evidence of the superior quality of our technology and services.

Our vision is to achieve global industry leadership in the telematics industry including Fleet Management, Stolen Vehicle Recovery and Insurance Telematics services with our mission being to provide our clients and partners with real-time actionable business intelligence based on advanced technology and reliable data.

Cartrack commenced operations in 2004 and listed on the Johannesburg Stock Exchange as Cartrack Holdings Limited in 2014 Sharecode (CTK). Cartrack has developed into a leading global provider of Fleet Management, Stolen Vehicle Recovery and Insurance telematics services with a strong focus on technology development to enhance customer experience. An extensive footprint is already well established in Africa, Europe and South East Asia; more recently, operations have been opened in America and New Zealand.

Cartrack is a service-centric organisation supported by a strong focus on in-house design, development and installation of Telematics technology and data analytics. Cartrack provides fleet, mobile asset and workforce management solutions underpinned by real-time actionable business intelligence, delivered as Software-as-a-Service (‘SaaS’), plus the service of tracking and recovery of stolen vehicles.

Our technology is widely accepted by motor manufacturers and insurers, with hardware and installations being of the highest standard. Cartrack’s user-friendly and cost-effective web-based Fleet Management portal provides a comprehensive set of features ensuring the optimisation of both fleet and human resources. To expand its integrated service offering, Cartrack is providing driver risk assessment offerings in the field of Insurance Telematics.

Cartrack also specialises in vehicle tracking and recovery, providing an invaluable service to combat vehicle theft in countries where crime is prevalent. Demonstrating its confidence in its systems, Cartrack was the first company globally to offer a cash back recovery warranty of up to R150 000 to its customers in the unlikely event of non-recovery of their stolen vehicles. An industry leading audited recovery rate of 91% in South Africa is evidence of the superior quality of our technology and services.

Our vision is to achieve global industry leadership in the telematics industry including Fleet Management, Stolen Vehicle Recovery and Insurance Telematics services with our mission being to provide our clients and partners with real-time actionable business intelligence based on advanced technology and reliable data.

Cartrack service offerings

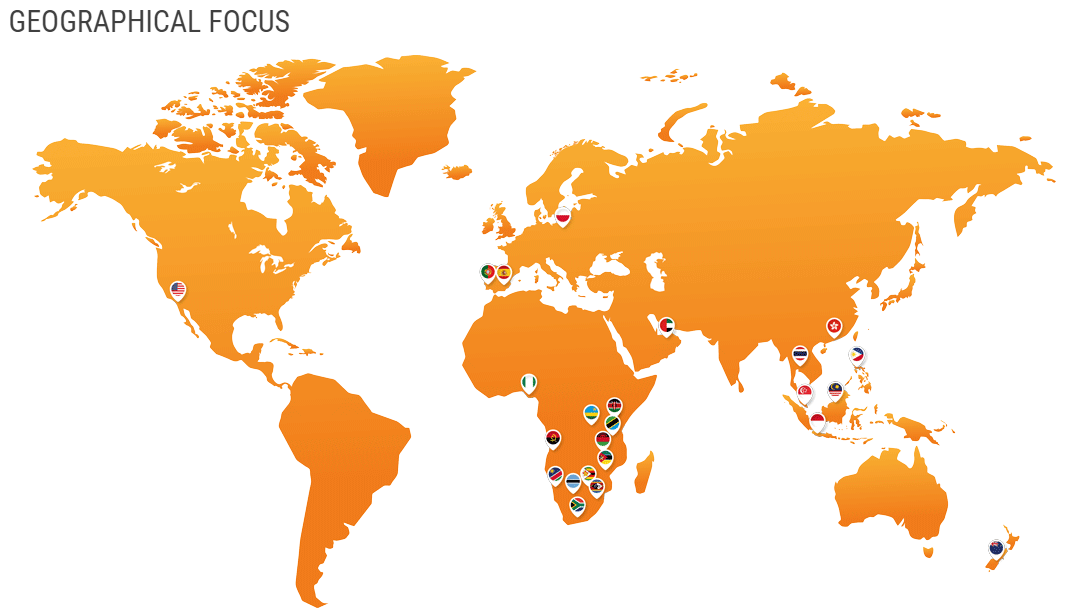

Cartrack spread far and wide.

The image below shows in which markets Cartrack are actively operating in. The fact that they are not just in South Africa means the group does provide potential "Rand hedge" benefits, by which a weakening exchange rate could lead to higher reported earnings in Rands from their offshore operations.

Cartrack Geographical representation of their markets

Overview of the results

A short summary on their current group profile

Cartrack, with an active subscriber base of more than 849,772, ranks amongst of the largest telematics companies globally. The Group's impressive growth since its inception in 2004 has resulted in the development of an extensive footprint in 24 countries across Africa, Europe, North America, Asia Pacific and the Middle East.

Cartrack's success is attributed to its status as a service-centric organisation that focuses on the in-house design, development, production and installation of telematics technology and data analytics products. The Group's technology is widely accepted by motor manufacturers and insurers. Cartrack's customer telematics web interface provides a comprehensive set of features, thereby ensuring the optimisation of its customers' fleet and human resources. As an expansion of its integrated service offering, Cartrack also provides driver risk-assessment offerings in the insurance telematics field.

Cartrack, with an active subscriber base of more than 849,772, ranks amongst of the largest telematics companies globally. The Group's impressive growth since its inception in 2004 has resulted in the development of an extensive footprint in 24 countries across Africa, Europe, North America, Asia Pacific and the Middle East.

Cartrack's success is attributed to its status as a service-centric organisation that focuses on the in-house design, development, production and installation of telematics technology and data analytics products. The Group's technology is widely accepted by motor manufacturers and insurers. Cartrack's customer telematics web interface provides a comprehensive set of features, thereby ensuring the optimisation of its customers' fleet and human resources. As an expansion of its integrated service offering, Cartrack also provides driver risk-assessment offerings in the insurance telematics field.

So get to the numbers already

So lets take a look at the main numbers published in the results update:

- Revenue: R765,7 million (up 21.5%) from R629.8 million 12 months ago

- Gross profit: R611 million (up 25%) from R488.6 million 12 months ago

- Net profit: R178.3million (up 23.8% ) from R143.95 million 12 months ago

- Earnings per share: 5739c a share (up 24.2%) from 46.6c a share 12 months ago

- Cash generated from operations: R339.9 million (up 40% ) from R242.6million 12 months ago

- The cash generated per share is therefore R1.13 a share. Solid cash generating capabilities from the group

- A slight worry is the increase in "Trade and other receivables" which grew by 22% from R164 million to R201.1 million over the last 12 months

So what did Cartrack management have to say about the results and their prospects?

Below follows a few extracts from Cartrack's financial results.

"Cartrack delivered strong interim results with EPS increasing by 24% (FY18: 17% and HY18: 21%). These robust results were achieved due to strong subscriber and annuity revenue growth, while maintaining industry-leading operating profit and EBITDA margins of 34% (FY18: 33% and HY18: 32%) and 50% (FY18: 49% and HY18: 47%), respectively. The Group achieved subscriber growth of 28% (FY18: 25% and HY18: 21%), with the number of subscribers increasing from 666,422 to 849,772. The Group continues to maintain a strong order book while focusing efforts on research and development, customer experience and distribution.

The South Africa segment delivered particularly strong results, with annuity revenue increasing by 26% from R410,4 million to R518,8 million (HY18: 19%) and subscribers grew by 30% (HY18: 19%) over the same period. The primary contributors to this organic growth were the realisation of a strong sales pipeline, investment in operating capacity and an effective distribution strategy. In line with expectations, the sales mix in HY19 as in FY18 shifted to include significantly more rental sales than cash sales. The South African market remains underpenetrated in both the corporate and consumer segments, despite South Africa having one of the highest telematic penetration rates in the world. As the subscriber base continues to grow, Cartrack will continue to identify and exploit opportunities to realise economies of scale and operating efficiencies. The South Africa segment is expected to deliver stronger bottom-line results in the next 18 months as it is currently deploying an upgraded proprietary customer-centric platform which allows for improved efficiencies to deal with the current accelerated growth.

Europe

The Europe segment delivered strong subscriber growth of 23% (HY18: 24%), largely as a result of an investment in distribution and operating capacity over the past two years. The annuity revenue increased by 28% from R52,8 million to R67,3 million. The continued investment in distribution and operating capacity for future growth led to a consistent year-on-year operating profit of R9,2 million. Europe presents lucrative growth opportunities to provide telematics offerings and related value-added services and Cartrack is now well positioned to capitalise on these opportunities. Asia Pacific Asia Pacific is now the second largest segment in the Group based on revenue contribution, with the annuity revenue up 54% from R46,7 million to R71,7 million (HY18: 112%). These results are due to an increase in subscribers of 43% (HY18: 122%). The market in this segment remains considerably underpenetrated due to fragmented market participants delivering entry-level telematics offerings, thereby enabling Cartrack to exploit its more sophisticated, reliable products and customer-centric services. Cartrack remains poised to exploit new opportunities while expanding cross-border relationships as it drives its robust and proven offerings in this segment.

USA

The investment to date has largely been in research and development, which has been expensed in terms of the Group Policy. Cartrack is experiencing delays in fully rolling out its services in the region primarily due to unforeseen delays in the development of the machine-to-machine devices that operate on the USA 4G frequency spectrum. The good news is that Cartrack has now completed the development of both the machine-to-machine devices and a sophisticated electronic logging device ("ELD"). Cartrack is now positioned to roll out in the USA and to capitalise on the 3G sunset which is expected to occur in 2020. The vast majority of the existing competitors' subscribers are currently using 3G machine-to- machine devices which will soon be obsolete."

So what is the group's outlook and prospects like? Well the management of the group sounds very positive. Below their outlook

"Cartrack delivered strong interim results with EPS increasing by 24% (FY18: 17% and HY18: 21%). These robust results were achieved due to strong subscriber and annuity revenue growth, while maintaining industry-leading operating profit and EBITDA margins of 34% (FY18: 33% and HY18: 32%) and 50% (FY18: 49% and HY18: 47%), respectively. The Group achieved subscriber growth of 28% (FY18: 25% and HY18: 21%), with the number of subscribers increasing from 666,422 to 849,772. The Group continues to maintain a strong order book while focusing efforts on research and development, customer experience and distribution.

The South Africa segment delivered particularly strong results, with annuity revenue increasing by 26% from R410,4 million to R518,8 million (HY18: 19%) and subscribers grew by 30% (HY18: 19%) over the same period. The primary contributors to this organic growth were the realisation of a strong sales pipeline, investment in operating capacity and an effective distribution strategy. In line with expectations, the sales mix in HY19 as in FY18 shifted to include significantly more rental sales than cash sales. The South African market remains underpenetrated in both the corporate and consumer segments, despite South Africa having one of the highest telematic penetration rates in the world. As the subscriber base continues to grow, Cartrack will continue to identify and exploit opportunities to realise economies of scale and operating efficiencies. The South Africa segment is expected to deliver stronger bottom-line results in the next 18 months as it is currently deploying an upgraded proprietary customer-centric platform which allows for improved efficiencies to deal with the current accelerated growth.

Europe

The Europe segment delivered strong subscriber growth of 23% (HY18: 24%), largely as a result of an investment in distribution and operating capacity over the past two years. The annuity revenue increased by 28% from R52,8 million to R67,3 million. The continued investment in distribution and operating capacity for future growth led to a consistent year-on-year operating profit of R9,2 million. Europe presents lucrative growth opportunities to provide telematics offerings and related value-added services and Cartrack is now well positioned to capitalise on these opportunities. Asia Pacific Asia Pacific is now the second largest segment in the Group based on revenue contribution, with the annuity revenue up 54% from R46,7 million to R71,7 million (HY18: 112%). These results are due to an increase in subscribers of 43% (HY18: 122%). The market in this segment remains considerably underpenetrated due to fragmented market participants delivering entry-level telematics offerings, thereby enabling Cartrack to exploit its more sophisticated, reliable products and customer-centric services. Cartrack remains poised to exploit new opportunities while expanding cross-border relationships as it drives its robust and proven offerings in this segment.

USA

The investment to date has largely been in research and development, which has been expensed in terms of the Group Policy. Cartrack is experiencing delays in fully rolling out its services in the region primarily due to unforeseen delays in the development of the machine-to-machine devices that operate on the USA 4G frequency spectrum. The good news is that Cartrack has now completed the development of both the machine-to-machine devices and a sophisticated electronic logging device ("ELD"). Cartrack is now positioned to roll out in the USA and to capitalise on the 3G sunset which is expected to occur in 2020. The vast majority of the existing competitors' subscribers are currently using 3G machine-to- machine devices which will soon be obsolete."

So what is the group's outlook and prospects like? Well the management of the group sounds very positive. Below their outlook

"Notwithstanding the significant and continuing investment in customer acquisition costs, Cartrack remains highly cash generative with a strong cash flow forecast for the foreseeable future. OUTLOOK2 SaaS, within the context of the Internet of Things ("IoT"), continues to rapidly expand as the digital age comes to the fore. Cartrack remains at the forefront of the related telematics expansion and continues to drive innovation and application through its interaction with customers and strategic research and development activities. Cartrack's commitment to an eco-system platform for connected-cars that is vehicle brand agnostic has been reconfirmed by its experimentation in smart-mobility in partnership with two of the world's leading companies offering pay-as-a-service transportation.

Cartrack views this development as a strengthening of telematics companies' value proposition, particularly those companies with stable, proven and dynamic platforms that will be able to provide decision-useful information to customers in the future by leveraging both Original Equipment Manufacturer and third-party telematics devices. Increasingly, customers are relying on the telematics market to optimise business intelligence relating to assets and people on a global scale. Cartrack will continue to evolve as a more integral part of its current and future customers' lives. Achieving this aim will require a continued and deliberate investment in technology, information management, human resources and in the distribution and operating capacity of current and new markets.

Cartrack has in the past looked at possible market consolidation opportunities. In the past 18 months Cartrack decided to focus on growing the business organically, unless an attractive opportunity comes along. It should be noted that the South African market remains underpenetrated, with many opportunities available to provide customer-centric solutions to individuals, customers and fleets alike. Furthermore, the order book in Europe remains strong while new sales are being actively pursued. While subscriber growth and customer service remain the primary focus, cost rationalisation strategies will be implemented to leverage subscriber growth in order to increase operating profit and margin."

Cartrack views this development as a strengthening of telematics companies' value proposition, particularly those companies with stable, proven and dynamic platforms that will be able to provide decision-useful information to customers in the future by leveraging both Original Equipment Manufacturer and third-party telematics devices. Increasingly, customers are relying on the telematics market to optimise business intelligence relating to assets and people on a global scale. Cartrack will continue to evolve as a more integral part of its current and future customers' lives. Achieving this aim will require a continued and deliberate investment in technology, information management, human resources and in the distribution and operating capacity of current and new markets.

Cartrack has in the past looked at possible market consolidation opportunities. In the past 18 months Cartrack decided to focus on growing the business organically, unless an attractive opportunity comes along. It should be noted that the South African market remains underpenetrated, with many opportunities available to provide customer-centric solutions to individuals, customers and fleets alike. Furthermore, the order book in Europe remains strong while new sales are being actively pursued. While subscriber growth and customer service remain the primary focus, cost rationalisation strategies will be implemented to leverage subscriber growth in order to increase operating profit and margin."

So should you buy their shares?

Well crime and hijackings in South Africa will not go away anytime soon. So we suspect the demand for their services will continue to be strong on one of their main markets which is South Africa. Their growth has been pretty rapid, but we are worried that they are financing their growth with debt. And increased debt means increased debt repayments, which for investors will imply less or no dividends being paid, as they would need to pay back debt before being able to splash out on shareholders. And if they pay dividends while having mountains of debt to service, one has to be worried about that to. So investors or potential investors needs to take this into account,.

They are currently trading on a dividend yield of 2.5% after the gross dividend of 18c a share was declared, and PE ratio of close to 25, which is pretty steep. But it shows the market is expecting significant earnings growth due to their rapid expansion and growth. We would advise investors to sit on the side line at the current price, unless an investor feels the market they operate in is to good to miss out on and believes subscriber numbers will continue to increase at a rapid rate. If not, we believe there are better quality shares out there that investors can invest in

They are currently trading on a dividend yield of 2.5% after the gross dividend of 18c a share was declared, and PE ratio of close to 25, which is pretty steep. But it shows the market is expecting significant earnings growth due to their rapid expansion and growth. We would advise investors to sit on the side line at the current price, unless an investor feels the market they operate in is to good to miss out on and believes subscriber numbers will continue to increase at a rapid rate. If not, we believe there are better quality shares out there that investors can invest in