|

Related Topics |

|

We take a look at the interim results for the period ending end of August 2018 of listed construction company Stefanutti Stocks. The construction industry has not been a easy space to operate in, in South Africa so the results might look pretty gloomy. Lets take a look.

|

|

About Stefanutti Stocks

Stefanutti Stocks is a construction company operating throughout South Africa, sub-Saharan Africa and the United Arab Emirates with multi-disciplinary expertise including concrete structures, marine construction, piling and geotechnical services, roads and earthworks, bulk pipelines, open pit contract mining and surface mining related services, all forms of building works, including affordable housing, and mechanical and electrical installation and construction. Stefanutti Stocks is one of South Africa's largest multidisciplinary construction groups with over 12 000 employees.

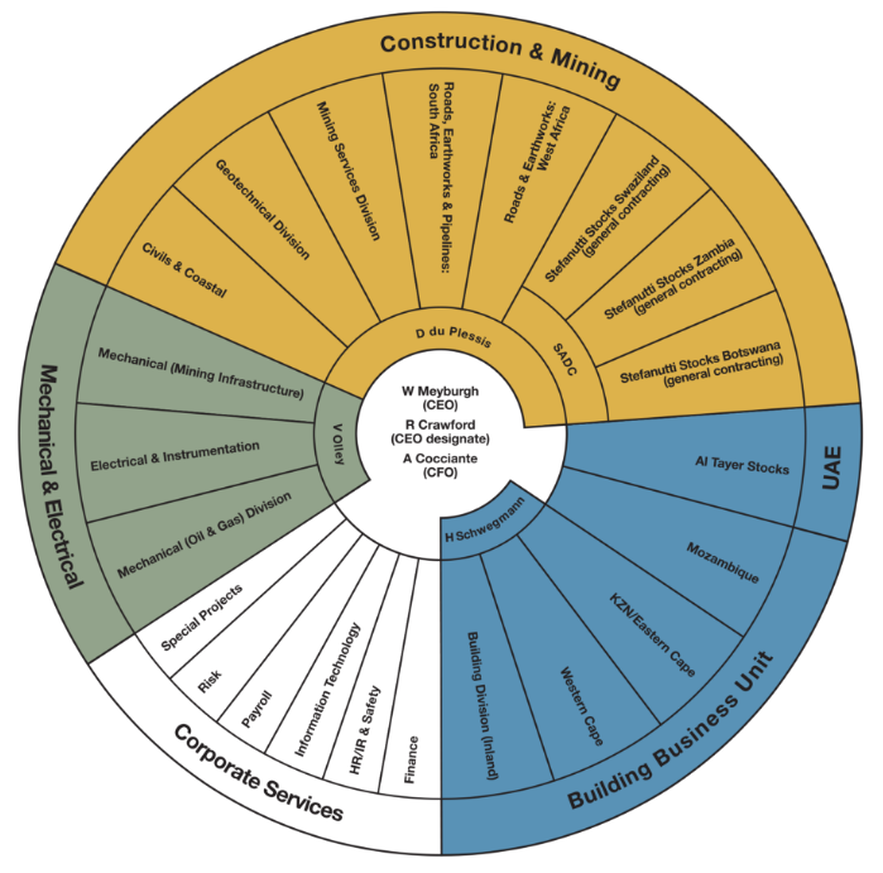

The image below shows Stefanutt's group structure in detail. But basically the main divisions include:

The image below shows Stefanutt's group structure in detail. But basically the main divisions include:

- Construction and Mining

- Building Business Unit

- Corporate Services

- Mechanical and Electrical

Business units operate in South Africa and across sub-Saharan Africa including in Benin, Botswana, Mozambique, Namibia, Nigeria, Sierra Leone, Swaziland, Tanzania and Zambia. The biggest contributor to Stefanutti Stocks revenue, and profits is its Construction and Mining division. So a bit more detail on this particular division follows:

The Construction & Mining business unit offers multidisciplinary construction capabilities across the full spectrum of infrastructure construction.

• Water infrastructure: including environmental rehabilitation, water supply projects, construction and refurbishment of large dams, institutional waste-water treatment facilities, water purification works, bulk pipelines, water storage reservoirs, municipal roads and stormwater.

• Transport infrastructure: including roads, bridges, airport terminals, aprons and runways, quay walls and breakwaters in port facilities.

• Power generation infrastructure: including coal-fired power stations and renewable energy generation — such as wind, solar and hydro power.

• Industrial infrastructure: including facilities, factories and industrial processing plants, smelters, glass factories, mills (steel, sugar, cement), pharmaceutical and car production facilities.

• Petrochemical infrastructure: including new installations for the petrochemical industry (foundation, base and tank construction) as well as extensions or improvements to existing operational plants (including refineries, storage, fire protection and both land and sea offloading facilities).

• Mining infrastructure: including decline shafts, terraces for new developments and civil infrastructure. The business unit’s Mining Services division specialises in mine residue disposal facilities and open-pit contract mining; its technical services division offers the design, development and management of mine infrastructure.

The combined capabilities of the divisions within the business unit, enable it to offer a fully-comprehensive construction service to its clients. Niche capabilities include marine construction, as well as the design & construction of deeplevel foundations and lateral support solutions in the most challenging geological environments.

The Construction & Mining business unit offers multidisciplinary construction capabilities across the full spectrum of infrastructure construction.

• Water infrastructure: including environmental rehabilitation, water supply projects, construction and refurbishment of large dams, institutional waste-water treatment facilities, water purification works, bulk pipelines, water storage reservoirs, municipal roads and stormwater.

• Transport infrastructure: including roads, bridges, airport terminals, aprons and runways, quay walls and breakwaters in port facilities.

• Power generation infrastructure: including coal-fired power stations and renewable energy generation — such as wind, solar and hydro power.

• Industrial infrastructure: including facilities, factories and industrial processing plants, smelters, glass factories, mills (steel, sugar, cement), pharmaceutical and car production facilities.

• Petrochemical infrastructure: including new installations for the petrochemical industry (foundation, base and tank construction) as well as extensions or improvements to existing operational plants (including refineries, storage, fire protection and both land and sea offloading facilities).

• Mining infrastructure: including decline shafts, terraces for new developments and civil infrastructure. The business unit’s Mining Services division specialises in mine residue disposal facilities and open-pit contract mining; its technical services division offers the design, development and management of mine infrastructure.

The combined capabilities of the divisions within the business unit, enable it to offer a fully-comprehensive construction service to its clients. Niche capabilities include marine construction, as well as the design & construction of deeplevel foundations and lateral support solutions in the most challenging geological environments.

So to the numbers we go

- Revenue R5,1 billion (down 1% from R5.2billion)

- Operating profit R125 million (up 26% from restated figures of August 2017)

- Net profit R104 million (up 40% from R74 million a year ago)

- Cash at end of period R964 million (down 23% from R1.26billion)

- Diluted earnings per share: 55.3c (up 39% from 39.8c the previous year) putting SSK on a PE ratio of 2.7 (assuming the 55c per share earnings for the first 6 months of financial year will be repeated for next 6 months).

- Cash generated per share R1.15 per share

-Current order book R12,8 billion

-No dividend declared

- Operating profit R125 million (up 26% from restated figures of August 2017)

- Net profit R104 million (up 40% from R74 million a year ago)

- Cash at end of period R964 million (down 23% from R1.26billion)

- Diluted earnings per share: 55.3c (up 39% from 39.8c the previous year) putting SSK on a PE ratio of 2.7 (assuming the 55c per share earnings for the first 6 months of financial year will be repeated for next 6 months).

- Cash generated per share R1.15 per share

-Current order book R12,8 billion

-No dividend declared

So any comments from management on the results?

The following extracts were taken from their financial results as published earlier today.

"The Board of Directors report that the group's performance continues to reflect the impact of operating within a demanding trading environment. Contract revenue from operations reduced to R5,1 billion compared to the previous period (restated Aug 2017: R5,2 billion). However, operating profit increased from R110 million in the previous period to R125 million in the current period. This excludes the United Arab Emirates operation, which contributed R38 million (restated Aug 2017: R16 million) towards the share of profits of equity accounted investees. As a result of the above, earnings per share and headline earnings per share increased by 41% and 46% from the comparative period to 61,76 cents (restated Aug 2017: 43,65 cents) and 60,30 cents (restated Aug 2017: 41,41 cents) respectively."

"The Board of Directors report that the group's performance continues to reflect the impact of operating within a demanding trading environment. Contract revenue from operations reduced to R5,1 billion compared to the previous period (restated Aug 2017: R5,2 billion). However, operating profit increased from R110 million in the previous period to R125 million in the current period. This excludes the United Arab Emirates operation, which contributed R38 million (restated Aug 2017: R16 million) towards the share of profits of equity accounted investees. As a result of the above, earnings per share and headline earnings per share increased by 41% and 46% from the comparative period to 61,76 cents (restated Aug 2017: 43,65 cents) and 60,30 cents (restated Aug 2017: 41,41 cents) respectively."

Construction & Mining

The number of tender enquiries and awards received from the mining sector has increased, whilst limited infrastructure work has been secured from the public sector. As a consequence of less public infrastructure spend, combined with a policy of increased fragmentation of civil contracts, the civils operations' order book and operating profit margins remain under pressure and it has not performed to expectations. The long outstanding amounts due from the governments of Zambia and Nigeria continue to be a source of concern. The outstanding amounts are not in dispute and periodic payments are being received. In both Nigeria and Zambia work will only recommence on affected contracts once all outstanding amounts have been received.

Building

The Building business unit's contract revenue has reduced to R1,7 billion (restated Aug 2017: R2,3 billion) with a contraction in operating profit to R6 million (restated Aug 2017: R22 million). The profit of the equity accounted United Arab Emirates operation is excluded from this operating profit. Within this business unit, the Mozambique and Coastal divisions continue to deliver positive results. However, despite scaling down and restructuring the Inland division, it continues to underperform due to the ongoing reduction in available work and not being able to recover holding costs. Furthermore, delayed payments from government in the social housing sector, continue to negatively affect the divisions working capital. This business unit is pursuing a number of contractual claims and compensation events on a large public sector project in South Africa, which also impacts on the conversion of work in progress into cash.

Mechanical & Electrical

Mechanical & Electrical's turnover and operating profit increased to R581 million (restated Aug 2017: R541 million) and R8 million (restated Aug 2017: R1 million) respectively. The Mechanical division's order book has increased due to awards of surface mining related projects. The ongoing shortage of work in the traditional petrochemical market is negatively affecting the Oil & Gas division's financial performance. This has resulted in the Electrical & Instrumentation division being incorporated into the Mechanical division. In addition, the contract which was cancelled by a client in the previous financial year, has been referred to arbitration. The hearing is scheduled for the first quarter of 2019 and at this stage the financial impact thereof cannot be quantified..

Outlook and strategy

As has already been widely reported, the South African construction market remains at an historic low. A continuing slowdown in construction activity coupled with an aggressive contracting environment will result in operating profit margins remaining under pressure in the short to medium term. The group has improved to a level 2 Broad-Based Black Economic Empowerment contributor measured in terms of the new Construction Sector scorecard. Notwithstanding, there is increasing pressure from the local market to improve our level of black ownership. The group is assessing various options in order to address this requirement.

The group's order book has reduced to R12,8 billion from R14,3 billion since the last report. In the short term there are opportunities in the local market which include surface mining related services, selected open pit mining contracts, urban developments, petrochemical tank farms, smaller oil and gas projects, pipelines, water and sanitation treatment plants as well as warehouses and some design and construct opportunities in the building sector. Uncertainty exists with respect to the recently announced Government Stimulus Package. Depending on the detail relating to its implementation, this could create opportunities for various divisions within the group.

Cross-border opportunities exist in road and bridge construction, bulk pipelines, marine and mixed-use building projects and will be prudently considered. Our multi-disciplinary and geographically diversified business structure continues to enable the group to remain a strong competitor in the markets in which it operates. The group also continues to seek opportunities both in Southern Africa and, on a more selective basis, further afield in sub-Saharan Africa. With the challenges being experienced in construction markets, management constantly reviews and aligns each business unit and its respective divisions to ensure their ongoing sustainability.

The number of tender enquiries and awards received from the mining sector has increased, whilst limited infrastructure work has been secured from the public sector. As a consequence of less public infrastructure spend, combined with a policy of increased fragmentation of civil contracts, the civils operations' order book and operating profit margins remain under pressure and it has not performed to expectations. The long outstanding amounts due from the governments of Zambia and Nigeria continue to be a source of concern. The outstanding amounts are not in dispute and periodic payments are being received. In both Nigeria and Zambia work will only recommence on affected contracts once all outstanding amounts have been received.

Building

The Building business unit's contract revenue has reduced to R1,7 billion (restated Aug 2017: R2,3 billion) with a contraction in operating profit to R6 million (restated Aug 2017: R22 million). The profit of the equity accounted United Arab Emirates operation is excluded from this operating profit. Within this business unit, the Mozambique and Coastal divisions continue to deliver positive results. However, despite scaling down and restructuring the Inland division, it continues to underperform due to the ongoing reduction in available work and not being able to recover holding costs. Furthermore, delayed payments from government in the social housing sector, continue to negatively affect the divisions working capital. This business unit is pursuing a number of contractual claims and compensation events on a large public sector project in South Africa, which also impacts on the conversion of work in progress into cash.

Mechanical & Electrical

Mechanical & Electrical's turnover and operating profit increased to R581 million (restated Aug 2017: R541 million) and R8 million (restated Aug 2017: R1 million) respectively. The Mechanical division's order book has increased due to awards of surface mining related projects. The ongoing shortage of work in the traditional petrochemical market is negatively affecting the Oil & Gas division's financial performance. This has resulted in the Electrical & Instrumentation division being incorporated into the Mechanical division. In addition, the contract which was cancelled by a client in the previous financial year, has been referred to arbitration. The hearing is scheduled for the first quarter of 2019 and at this stage the financial impact thereof cannot be quantified..

Outlook and strategy

As has already been widely reported, the South African construction market remains at an historic low. A continuing slowdown in construction activity coupled with an aggressive contracting environment will result in operating profit margins remaining under pressure in the short to medium term. The group has improved to a level 2 Broad-Based Black Economic Empowerment contributor measured in terms of the new Construction Sector scorecard. Notwithstanding, there is increasing pressure from the local market to improve our level of black ownership. The group is assessing various options in order to address this requirement.

The group's order book has reduced to R12,8 billion from R14,3 billion since the last report. In the short term there are opportunities in the local market which include surface mining related services, selected open pit mining contracts, urban developments, petrochemical tank farms, smaller oil and gas projects, pipelines, water and sanitation treatment plants as well as warehouses and some design and construct opportunities in the building sector. Uncertainty exists with respect to the recently announced Government Stimulus Package. Depending on the detail relating to its implementation, this could create opportunities for various divisions within the group.

Cross-border opportunities exist in road and bridge construction, bulk pipelines, marine and mixed-use building projects and will be prudently considered. Our multi-disciplinary and geographically diversified business structure continues to enable the group to remain a strong competitor in the markets in which it operates. The group also continues to seek opportunities both in Southern Africa and, on a more selective basis, further afield in sub-Saharan Africa. With the challenges being experienced in construction markets, management constantly reviews and aligns each business unit and its respective divisions to ensure their ongoing sustainability.

So should you buy their shares?

Well the share price is pricing the company as if they have no work to do and will receive no new work for years to come, with it trading at a forward PE of under 3. Our concern is the fact that the construction industry remains subdued and will continue to be weak for years to come as lack luster economic growth does little to boost demand for new infrastructure in South Africa. Payment delays from the South Africa, Zambian and Nigerian governments with regards to work completed is another concern. The company might decide to write off outstanding amounts completely, which will affect earnings. Decline in the order book of work from R14.3 billion to just under R13 billion is a concern that work is starting to dry up faster than they expected. A few claims have been made against the company to which could cost them financially.

We would not recommend buying any construction company listed on the JSE, even if they are priced for near dooms days scenarios. While the share price teeters along and doesn't pay a dividend, investors could have invested in a company operating in a sector in which there will always be a demand, think food, beverages, health etc, and at the same probably receive a steady stream of dividends. The opportunity cost of holding SSK shares outweighs the potential price gains it might provide in future.

We would not recommend buying any construction company listed on the JSE, even if they are priced for near dooms days scenarios. While the share price teeters along and doesn't pay a dividend, investors could have invested in a company operating in a sector in which there will always be a demand, think food, beverages, health etc, and at the same probably receive a steady stream of dividends. The opportunity cost of holding SSK shares outweighs the potential price gains it might provide in future.