|

Related Topics |

|

In our continued efforts to give our readers a broad number of views, opinions and information, we provide readers with Peregrine Treasury Services weekly market wrap below.

|

|

Peregrine Treasury Services Weekly Wrap as at 30 August 2019

In a world where modern ‘political chess games’ are being manipulated and communicated through social media platforms, one should expect future market volatility, and the speed at which it rapidly accelerates to its turning point, to be largely ungovernable and potentially unjustifiably devastating to global investors. On Friday last week, one would’ve seen how quickly a tweet, from the right person, can be taken as ‘absolute gospel’, sending global markets into immediate panic. Are the golden days of investing slowly fading away, when it comes to underlying economic and fundamental research, as Donald Trump’s Twitter Tweets now have the potential to move markets more than ethically intended.

GLOBAL DATA AND POLITICS

Looking east, and 13 weeks into the Hong Kong (HK) protests, Beijing and HK are no-closer to any kind of peaceful resolution. With between 8,000 and 10,000 new Chinese troops moving into HK over the last few days, echoes of Tiananmen Square start to resonate through history books into the present day. Year-on-year (YoY), for July, HK export and import numbers deceased by 5.7% and 8.7% percent, respectively. This relatively large drop-off from previous numbers can be directly linked to a slowing global growth scenario, where consumer and manufacturing demand has drastically fallen, while the social unrest in HK is slowly starting to negatively impact trade numbers in that region.

Industrial production numbers released out of Thailand came in stronger than previous numbers (-3.23% vs previous -5.54%), however a definite slowdown in production still shrouds the Kingdom. Japanese consumer confidence numbers dropped to 37.1, from a previous 37.8, for August – this, the lowest confidence numbers since April 2014. Main attributors to the continual lack of confidence among Japanese citizens tends to be focused on concerns over unemployment, general livelihood and a general slowdown in the purchasing of durable goods.

German unemployment figures remained stable at 5%, for the month of August, while their preliminary inflation rate numbers dropped to 1.4% from a previous 1.7%, YoY, for August. Heading west, Israel kept their benchmark interest rate at 0.25%, as analysts had expected. Now trending toward the strongest levels ever experienced for the country, Israel managed to decrease its unemployment rate, in July, to 3.7%, from the previous month’s 4.1%.

After a few quiet weeks, and as US company earning’s season comes to a close, the trade war between the United States and China was reignited, as Donald Trump got snug with his social media application, Twitter, once again. Jerome Powell’s speech at the Jackson Hole Symposium pointed toward a Federal Reserve that’s looking to keep interest rates around the two percent level, while tweaking monetary policies in order to incubate and foster further growth within the US economy. No defined path of action has been picked up from his speech however, with fragile monetary policies to manage, against a raging Trump, Powell has a hard task on his hands, as 2019 moves toward its end.

The US saw their economy growing by 2% for Q2, 2019, below analyst expectations of 2.1%. Initial jobless claims in the US rose this week to 215,000 vs a previous 211,000.

US EQUITIES

“Our great American companies are hereby ordered to immediately start looking for an alternative to China, including bringing your companies HOME and making your products in the USA.” – The tweet by US President Donald Trump that sent markets plummeting last Friday, amidst the vague tone set by Jerome Powell.

As waves of fear rushed over the equity markets on Friday, the impact of this tweet saw the Dow Jones, NASDAQ and S&P 500 falling 2.45%, 3.20% and 3.09%, respectively, on the day. Stocks such as Apple, Caterpillar, Broadcom and Nvidia were seen dipping between three-and-five percent on Friday’s trading day. Along with the turbulence recently seen, mainly influenced by the trade war and a slowing global economy, it’s also interesting to note that the elusive ‘inverted yield curve’ inverted further, when looking at US Treasuries. In essence the US’ 30-year treasury yields dipped lower than their US three-month notes, pointing toward a general investor who is starting to question the historic belief that a bond associated with a longer time horizon (carrying a stronger yield), should be as expensive as they are and if they actually hold the worth one pays for them, currently. All these confusing questions created a small dragging-effect on the market this week, with investors becoming relatively wary of the economic story that’s playing out.

Since last Friday morning, equity markets have attempted to scrape back some losses with performance for the week currently around:

Company earnings, this week, continued to point toward a thriving US economy, with Best Buy Co Inc., Dollar General Corp, Guess and Burlington Stores Inc. all releasing stronger-than-expected results for Q2. Abercrombie & Fitch unfortunately saw their stock falling more than 10% on Thursday’s open after a revenue-miss and weaker-than-expected sales growth.

FAANGs performance for the week, so far:

In South African rand-terms, add 6.87% against each of these return-figures to see what the South African investor could be up in 2019, with the currency-effect added.

COMMODITIES

US West Texas Intermediate (WTI) oil managed to outperform OPEC’s Brent Crude oil, this week, with lower US inventories numbers (a week-on-week drop of 10 million barrels) assisting an almost 6.00% recovery, following the snap-correction that most global sectors seem to have experienced on Friday last week. As global growth-worries and the fear of a falling oil demand hang in the undertow, the greater-investor should remain wary, when it comes to dealing in oil-related instruments over the coming months.

Brent Crude opened Friday’s trading day at $61.08 per barrel, while US West Texas Intermediate (WTI) opened at $56.53.

While most global ‘risk-on’ investments got pummeled by last Friday’s tweet, by Trump, gold seemed to morph into its own kind of beast, as it attracted even more attention from investors who are rather happier to dock their ships in the safer waters for now. Gold saw its price jump and maintain levels of around 3% stronger than a week ago. Heading toward the illusive $1,550.00 per-ounce-mark, gold will be a hot commodity to watch in the coming months, should trade tensions continue.

Platinum stole the show this week, however, with prices jumping more than 8% during the course of the week – its highest level since May 2018. Platinum’s move to around the $927.96 level was more of a technical move than a fundamental one. Palladium has definitely lost some steam over the last few weeks, remaining flat for the last five trading days. On Friday morning, gold, platinum and palladium were trading at levels of around $1,526.51, $918.45 and $1,483.67 per fine ounce respectively.

SOUTH AFRICAN FUNDAMENTALS

Closer to home, local producer price index (PPI) numbers, month-on-month and YoY, for July, came in lower than previous and expected numbers. PPI numbers, indicating the price that the manufacturer charges for the final manufactured goods/end product, came in lower mainly due to the drop in oil prices, even though both final food and clothing prices rose 6% and 3.5%, in July. Another standout number was gold PPI that came in 41% higher than previous year’s pricing, thanks to the robust upward move in gold prices, as investors assumedly start seeking safe havens in times of uncertainty.

On the political front, more questions have been raised over the death of Gavin Watson, Bosasa CEO, who died in a high speed car crash just outside of O.R Tambo International Airport in Johannesburg, early on Monday morning. Bosasa’s ties to the African National Congress (ANC), coupled with questionable payments made to both current president, (Cyril Ramaphosa) and ex-president (Jacob Zuma) of South Africa, has turned the whole saga into more of a murder mystery than anything else.

Watson was due to face the South African Revenue Services at the Inquiry, on Tuesday, with regard to his accountability within a firm that potentially dodged millions in taxes and partook in money laundering practices, while adding fuel to South Africa’s corruption-fire. But, not all is negative - Quietly in the undertow, the Hawks have been doing their rounds at various state-owned enterprises (SOE), engaging in many lifestyle audits on employees of influential rank, within these firms. This cleanup of politically-connected firms has sent shock waves through many industries, leading many accountable employees to actually resign, due to the fear of potentially having been unknowingly-involved in fraudulent activities in the past. Needless to say, productivity levels within many SOE departments has definitely been negatively impacted by these lifestyle audits carried out by the Hawks.

Another concerning topic painting news headlines is the growing amount of ANC in-fighting haunting the party. Eventually something has to give, which will likely see a small exodus quietly happening from the party. For now, the global political noise seems to be drowning out South Africa’s parliamentary woes.

SOUTH AFRICAN EQUITY

Considering the rough-ride markets have had this week, South Africa had one or two gems that managed to illumine the dreary economic landscape.

Adjusting to the choppy climate, Bid Corporation (BID), managed to raise earning by 12.5% per share for the six-months-ending 30 June 2019. Revenue was also seen rising by 9.8% to R129.3 billion. A large factor which did play into BID’s hands was the fact that north-of-95% of their revenue is generated offshore in generally-stronger currencies and geographies than that of South Africa and its rand. BID’s final dividend increased by 7.9% to R3.30 per share. Forward-looking guidance has been hinted at high single-figure numbers, albeit heavily influenced by a volatile rand. Over 5% stronger for the week, BID opened Friday’s trading day R319.20 per share

Dis-Chem (DCP) also managed to weather the storm, generating revenues of just under R10 billion, for the five-months-ending 31 July. Both retail and group revenue jumped between 12% and 13.5% for the period. So far, DCP has opened nine new stores this year, with another 13 planned before next year. Rising almost 10% on the back of the strong financial numbers, DCP settled ‘back at square-one’, opening Friday’s trading day flat for the week at R20.45 per share.

PPC Cement, Massmart and Steinhoff teased at some positive numbers this week, with only Steinhoff’s share price reacting positively, to the tune of around 28%. Both PPC and Massmart remained stagnant.

For August, so far:

Year-to-date, the JSE All Share index is up 3.18% and the Top 40 up 3.95%. Sector-wise, industrials have now returned 9.66%, resources 6.64% and financials -10.24% for the 2019 year so far.

THE WEEK AHEAD

As always, the investor should remain cognizant of the greater global tussle overshadowing general market sentiment. Even with China’s spokesman for China’s Ministry of Commerce, Gao Feng, announcing that China would prefer to address the trade war in a more calm and respectable manner, not one soul on this planet could possibly comprehend the impact one little tweet out of Trump’s Twitter account could have on the markets. In 2019, one seemingly finds oneself in an era where a social media platform may actually be the foundation to the way future policies are written and built upon – quite a scary thought. The rand is likely to remain range-bound over the next trading week with its key upper and lower levels, against the US dollar, being R15.25 and R15.40. The rand started the day trading at R15.33/$, R16.94/€ and R18.69/£

GLOBAL DATA AND POLITICS

Looking east, and 13 weeks into the Hong Kong (HK) protests, Beijing and HK are no-closer to any kind of peaceful resolution. With between 8,000 and 10,000 new Chinese troops moving into HK over the last few days, echoes of Tiananmen Square start to resonate through history books into the present day. Year-on-year (YoY), for July, HK export and import numbers deceased by 5.7% and 8.7% percent, respectively. This relatively large drop-off from previous numbers can be directly linked to a slowing global growth scenario, where consumer and manufacturing demand has drastically fallen, while the social unrest in HK is slowly starting to negatively impact trade numbers in that region.

Industrial production numbers released out of Thailand came in stronger than previous numbers (-3.23% vs previous -5.54%), however a definite slowdown in production still shrouds the Kingdom. Japanese consumer confidence numbers dropped to 37.1, from a previous 37.8, for August – this, the lowest confidence numbers since April 2014. Main attributors to the continual lack of confidence among Japanese citizens tends to be focused on concerns over unemployment, general livelihood and a general slowdown in the purchasing of durable goods.

German unemployment figures remained stable at 5%, for the month of August, while their preliminary inflation rate numbers dropped to 1.4% from a previous 1.7%, YoY, for August. Heading west, Israel kept their benchmark interest rate at 0.25%, as analysts had expected. Now trending toward the strongest levels ever experienced for the country, Israel managed to decrease its unemployment rate, in July, to 3.7%, from the previous month’s 4.1%.

After a few quiet weeks, and as US company earning’s season comes to a close, the trade war between the United States and China was reignited, as Donald Trump got snug with his social media application, Twitter, once again. Jerome Powell’s speech at the Jackson Hole Symposium pointed toward a Federal Reserve that’s looking to keep interest rates around the two percent level, while tweaking monetary policies in order to incubate and foster further growth within the US economy. No defined path of action has been picked up from his speech however, with fragile monetary policies to manage, against a raging Trump, Powell has a hard task on his hands, as 2019 moves toward its end.

The US saw their economy growing by 2% for Q2, 2019, below analyst expectations of 2.1%. Initial jobless claims in the US rose this week to 215,000 vs a previous 211,000.

US EQUITIES

“Our great American companies are hereby ordered to immediately start looking for an alternative to China, including bringing your companies HOME and making your products in the USA.” – The tweet by US President Donald Trump that sent markets plummeting last Friday, amidst the vague tone set by Jerome Powell.

As waves of fear rushed over the equity markets on Friday, the impact of this tweet saw the Dow Jones, NASDAQ and S&P 500 falling 2.45%, 3.20% and 3.09%, respectively, on the day. Stocks such as Apple, Caterpillar, Broadcom and Nvidia were seen dipping between three-and-five percent on Friday’s trading day. Along with the turbulence recently seen, mainly influenced by the trade war and a slowing global economy, it’s also interesting to note that the elusive ‘inverted yield curve’ inverted further, when looking at US Treasuries. In essence the US’ 30-year treasury yields dipped lower than their US three-month notes, pointing toward a general investor who is starting to question the historic belief that a bond associated with a longer time horizon (carrying a stronger yield), should be as expensive as they are and if they actually hold the worth one pays for them, currently. All these confusing questions created a small dragging-effect on the market this week, with investors becoming relatively wary of the economic story that’s playing out.

Since last Friday morning, equity markets have attempted to scrape back some losses with performance for the week currently around:

- S&P 500: down 0.10%

- NASDAQ: down 0.42%

- Dow Jones: up 0.52%

Company earnings, this week, continued to point toward a thriving US economy, with Best Buy Co Inc., Dollar General Corp, Guess and Burlington Stores Inc. all releasing stronger-than-expected results for Q2. Abercrombie & Fitch unfortunately saw their stock falling more than 10% on Thursday’s open after a revenue-miss and weaker-than-expected sales growth.

FAANGs performance for the week, so far:

- Facebook: up around 1.80%

- Amazon: down around 1.15%

- Apple: down around 1.72%

- Netflix: down around 0.18%

- Alphabet: up around 0.11%

In South African rand-terms, add 6.87% against each of these return-figures to see what the South African investor could be up in 2019, with the currency-effect added.

COMMODITIES

US West Texas Intermediate (WTI) oil managed to outperform OPEC’s Brent Crude oil, this week, with lower US inventories numbers (a week-on-week drop of 10 million barrels) assisting an almost 6.00% recovery, following the snap-correction that most global sectors seem to have experienced on Friday last week. As global growth-worries and the fear of a falling oil demand hang in the undertow, the greater-investor should remain wary, when it comes to dealing in oil-related instruments over the coming months.

Brent Crude opened Friday’s trading day at $61.08 per barrel, while US West Texas Intermediate (WTI) opened at $56.53.

While most global ‘risk-on’ investments got pummeled by last Friday’s tweet, by Trump, gold seemed to morph into its own kind of beast, as it attracted even more attention from investors who are rather happier to dock their ships in the safer waters for now. Gold saw its price jump and maintain levels of around 3% stronger than a week ago. Heading toward the illusive $1,550.00 per-ounce-mark, gold will be a hot commodity to watch in the coming months, should trade tensions continue.

Platinum stole the show this week, however, with prices jumping more than 8% during the course of the week – its highest level since May 2018. Platinum’s move to around the $927.96 level was more of a technical move than a fundamental one. Palladium has definitely lost some steam over the last few weeks, remaining flat for the last five trading days. On Friday morning, gold, platinum and palladium were trading at levels of around $1,526.51, $918.45 and $1,483.67 per fine ounce respectively.

SOUTH AFRICAN FUNDAMENTALS

Closer to home, local producer price index (PPI) numbers, month-on-month and YoY, for July, came in lower than previous and expected numbers. PPI numbers, indicating the price that the manufacturer charges for the final manufactured goods/end product, came in lower mainly due to the drop in oil prices, even though both final food and clothing prices rose 6% and 3.5%, in July. Another standout number was gold PPI that came in 41% higher than previous year’s pricing, thanks to the robust upward move in gold prices, as investors assumedly start seeking safe havens in times of uncertainty.

On the political front, more questions have been raised over the death of Gavin Watson, Bosasa CEO, who died in a high speed car crash just outside of O.R Tambo International Airport in Johannesburg, early on Monday morning. Bosasa’s ties to the African National Congress (ANC), coupled with questionable payments made to both current president, (Cyril Ramaphosa) and ex-president (Jacob Zuma) of South Africa, has turned the whole saga into more of a murder mystery than anything else.

Watson was due to face the South African Revenue Services at the Inquiry, on Tuesday, with regard to his accountability within a firm that potentially dodged millions in taxes and partook in money laundering practices, while adding fuel to South Africa’s corruption-fire. But, not all is negative - Quietly in the undertow, the Hawks have been doing their rounds at various state-owned enterprises (SOE), engaging in many lifestyle audits on employees of influential rank, within these firms. This cleanup of politically-connected firms has sent shock waves through many industries, leading many accountable employees to actually resign, due to the fear of potentially having been unknowingly-involved in fraudulent activities in the past. Needless to say, productivity levels within many SOE departments has definitely been negatively impacted by these lifestyle audits carried out by the Hawks.

Another concerning topic painting news headlines is the growing amount of ANC in-fighting haunting the party. Eventually something has to give, which will likely see a small exodus quietly happening from the party. For now, the global political noise seems to be drowning out South Africa’s parliamentary woes.

SOUTH AFRICAN EQUITY

Considering the rough-ride markets have had this week, South Africa had one or two gems that managed to illumine the dreary economic landscape.

Adjusting to the choppy climate, Bid Corporation (BID), managed to raise earning by 12.5% per share for the six-months-ending 30 June 2019. Revenue was also seen rising by 9.8% to R129.3 billion. A large factor which did play into BID’s hands was the fact that north-of-95% of their revenue is generated offshore in generally-stronger currencies and geographies than that of South Africa and its rand. BID’s final dividend increased by 7.9% to R3.30 per share. Forward-looking guidance has been hinted at high single-figure numbers, albeit heavily influenced by a volatile rand. Over 5% stronger for the week, BID opened Friday’s trading day R319.20 per share

Dis-Chem (DCP) also managed to weather the storm, generating revenues of just under R10 billion, for the five-months-ending 31 July. Both retail and group revenue jumped between 12% and 13.5% for the period. So far, DCP has opened nine new stores this year, with another 13 planned before next year. Rising almost 10% on the back of the strong financial numbers, DCP settled ‘back at square-one’, opening Friday’s trading day flat for the week at R20.45 per share.

PPC Cement, Massmart and Steinhoff teased at some positive numbers this week, with only Steinhoff’s share price reacting positively, to the tune of around 28%. Both PPC and Massmart remained stagnant.

For August, so far:

- All Share and Top 40 indices: down around 4.25%

- Resources: down around 2.95%

- Industrials: down around 3.86% (Naspers: down 2.28%)

- Financials: down around 6.83%

Year-to-date, the JSE All Share index is up 3.18% and the Top 40 up 3.95%. Sector-wise, industrials have now returned 9.66%, resources 6.64% and financials -10.24% for the 2019 year so far.

THE WEEK AHEAD

As always, the investor should remain cognizant of the greater global tussle overshadowing general market sentiment. Even with China’s spokesman for China’s Ministry of Commerce, Gao Feng, announcing that China would prefer to address the trade war in a more calm and respectable manner, not one soul on this planet could possibly comprehend the impact one little tweet out of Trump’s Twitter account could have on the markets. In 2019, one seemingly finds oneself in an era where a social media platform may actually be the foundation to the way future policies are written and built upon – quite a scary thought. The rand is likely to remain range-bound over the next trading week with its key upper and lower levels, against the US dollar, being R15.25 and R15.40. The rand started the day trading at R15.33/$, R16.94/€ and R18.69/£

Advertisement (and yes South Africans can buy from Amazon as they deliver to SA)

Our highlight for the week:

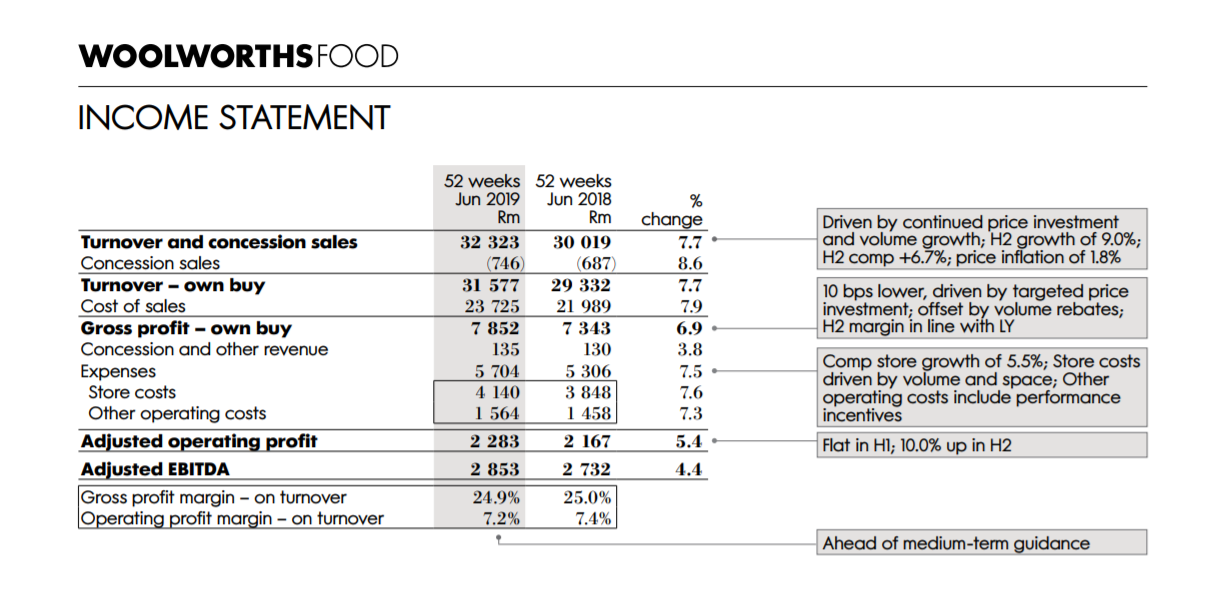

Woolworths published their latest results yesterday. And they wrote off/impaired of R6 billion on David Jones (the Australian clothing retailer they bought at great expense. Looking at the numbers it seems that Woolworths Foods is the crown jewel for the group. The image below shows the income statement of Woolworths Foods.

Read the full article here

Read the full article here

- Woolworths Foods turnover: R32.3 billion (up 7.7%)

- Woolworths Foods gross profit margin: 24.9%

- Woolworths Foods operating profit margin: 7.2%