|

Related Topics |

|

We take a look at the first quarter of the 2019 fiscal year results of the worlds leading internet entertainment service group, Netflix. Has their revenues been growing at the same pace in the 2019 fiscal year as it did in 2018? Or is it starting moderate and stabilize?

|

|

About Netflix

Netflix is the world's leading internet entertainment service with over 148 million paid memberships in over 190 countries enjoying TV series, documentaries and feature films across a wide variety of genres and languages. Members can watch as much as they want, anytime, anywhere, on any internet-connected screen. Members can play, pause and resume watching, all without commercials or commitments.

Netflix's View: internet entertainment is replacing linear TV

People love TV content, but they don't love the linear TV experience, where channels present programs only at particular times on non-portable screens with complicated remote controls. Now internet entertainment - which is on-demand, personalized, and available on any screen - is replacing linear TV.

Changes of this magnitude are rare. Radio was the dominant home entertainment media for nearly 50 years until linear TV took over in the 1950’s and 1960’s. Linear video in the home was a huge advance over radio, and very large firms emerged to meet consumer desires over the last 60 years. The new era of internet entertainment, which began about a decade ago, is likely to be very big and enduring also, given the flexibility and ubiquity of the internet around the world. We hope to continue being one of the leading firms of the internet entertainment era.

We think we can grow to 60-90 million members in the US, based upon our trajectory to date and the continued growth of internet entertainment. Our operating margin structure is set mostly top down. For any given future period, we estimate revenue, and decide what we want to spend, and how much margin we want in that period. Competitive pressures in bidding for content would lead us to have slightly less content than we would otherwise, rather than overspending. The same is true for our marketing budget. The output variable is membership growth that those spending choices influence.

Our global margin strategy is to expand internationally as fast as possible while staying profitable. The group of international markets we entered first (Canada, Latin America, the UK, Ireland, the Nordic countries and the Netherlands) are growing quickly and have already become contribution-positive. These markets continue to grow and generate meaningful profits that power the expansion in the remaining world markets we launched in 2016. We are targeting a 13% operating margin in 2019 and plan to steadily increase operating profit and margin from there as we balance growth with profitability.

With our rapid increase in content spending, and our growing emphasis on owned original productions, cash outlays are initially greater than content amortization, constraining free cash flow relative to profitability. We have generally funded these cash pre-pay needs with debt. We amortize content as quickly as justified, given industry norms and viewing history.

Netflix's View: internet entertainment is replacing linear TV

People love TV content, but they don't love the linear TV experience, where channels present programs only at particular times on non-portable screens with complicated remote controls. Now internet entertainment - which is on-demand, personalized, and available on any screen - is replacing linear TV.

Changes of this magnitude are rare. Radio was the dominant home entertainment media for nearly 50 years until linear TV took over in the 1950’s and 1960’s. Linear video in the home was a huge advance over radio, and very large firms emerged to meet consumer desires over the last 60 years. The new era of internet entertainment, which began about a decade ago, is likely to be very big and enduring also, given the flexibility and ubiquity of the internet around the world. We hope to continue being one of the leading firms of the internet entertainment era.

We think we can grow to 60-90 million members in the US, based upon our trajectory to date and the continued growth of internet entertainment. Our operating margin structure is set mostly top down. For any given future period, we estimate revenue, and decide what we want to spend, and how much margin we want in that period. Competitive pressures in bidding for content would lead us to have slightly less content than we would otherwise, rather than overspending. The same is true for our marketing budget. The output variable is membership growth that those spending choices influence.

Our global margin strategy is to expand internationally as fast as possible while staying profitable. The group of international markets we entered first (Canada, Latin America, the UK, Ireland, the Nordic countries and the Netherlands) are growing quickly and have already become contribution-positive. These markets continue to grow and generate meaningful profits that power the expansion in the remaining world markets we launched in 2016. We are targeting a 13% operating margin in 2019 and plan to steadily increase operating profit and margin from there as we balance growth with profitability.

With our rapid increase in content spending, and our growing emphasis on owned original productions, cash outlays are initially greater than content amortization, constraining free cash flow relative to profitability. We have generally funded these cash pre-pay needs with debt. We amortize content as quickly as justified, given industry norms and viewing history.

So to the numbers we go

The following highlights were reported by Netflix in their 1 quarter 2019 earnings report.

A few numbers we would like to highlight

- Revenue $4.52 billion (up 22.2% from $3.7 billion in the prior year)

- Operating income: $459 million (up 2.8% from $446 million in the prior year)

- Net income: $344 million (up 18.6% from $290 million in the prior year)

- Diluted earnings per share: $0.76 (up 19.1% from $0.64 in the prior year)

- Paid members at end of period (in USA): 60.229 million

- Profit margin in USA: 34.4%

- Paid members at end of period (international): 88.6 million

- Profit margin in international markets:11.6%

A few numbers we would like to highlight

- Cash generated from operations (Net earnings from operating activities): $344 million (or $0.76 share)

- PE ratio: 122. Yes thats right. Their PE ratio is well over 100. In essence investors are expecting Netflix revenues and earnings to grow at a rapid pace which will slowly reduce the PE ratio down to more reasonable levels. But has the stock run to far? Can Netflix increase their margins and revenues and warrant this lofty valuation it is currently trading at?

- Dividend yield: Well they not paying dividend as they using money coming in to grow the business and the brand.

So any comments or guidance from management on the results?

The group released the following guidance with their 1st quarter 2019 earnings report.

In Q1’19, average streaming paid memberships increased 26% year over year, while average rate per user (ARPU) decreased 2% year over year due to currency headwinds. Excluding F/X, global streaming ARPU improved 3% year over year and 2% sequentially. Year over year total revenue growth of 22% compares against 40% in Q1’18, which benefited from several price changes that took place in Q4’17 as well as F/X. On a F/X-neutral basis, Q1’19 revenue grew 28% year over year.

Operating margin of 10.2% exceeded our beginning-of-quarter expectation as some spending was shifted from Q1 to later in the year. EPS of $0.76, vs. $0.64 in the prior year period, included a $58 million non-cash unrealized gain from F/X remeasurement on our Euro denominated debt. Streaming content obligations dipped sequentially in Q1 due in part to the timing of run-of-series commitments. In addition, as we shift to more original content, there will be greater variability in content obligations quarter-to-quarter due to the timing of when productions start. We early-adopted the new content accounting standard (ASU 2019-2) in Q1’19. There is no material impact as our content accounting policies are already consistent with the new rules. Paid net adds in Q1 were 9.6 million (with 1.74m in the US and 7.86m internationally), up 16% year over year, representing a new quarterly record.

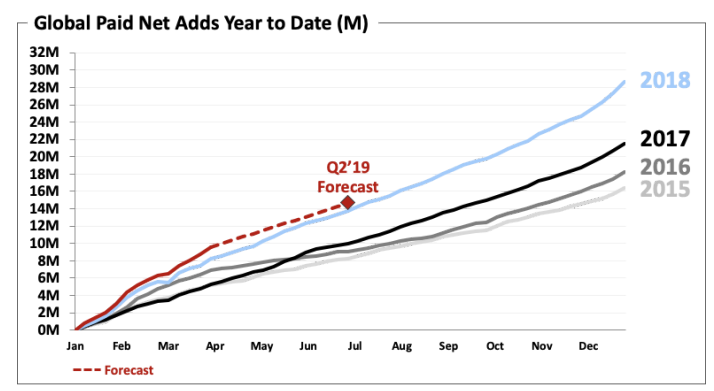

As always, our quarterly guidance is our internal forecast at the time we report. For Q2’19, we project total paid net adds of 5.0m (-8% year over year), with 0.3m in the US and 4.7m for the international segment. This would put us at 14.6m paid net adds for the first half of 2019, up 7% year over year.

In Q1’19, average streaming paid memberships increased 26% year over year, while average rate per user (ARPU) decreased 2% year over year due to currency headwinds. Excluding F/X, global streaming ARPU improved 3% year over year and 2% sequentially. Year over year total revenue growth of 22% compares against 40% in Q1’18, which benefited from several price changes that took place in Q4’17 as well as F/X. On a F/X-neutral basis, Q1’19 revenue grew 28% year over year.

Operating margin of 10.2% exceeded our beginning-of-quarter expectation as some spending was shifted from Q1 to later in the year. EPS of $0.76, vs. $0.64 in the prior year period, included a $58 million non-cash unrealized gain from F/X remeasurement on our Euro denominated debt. Streaming content obligations dipped sequentially in Q1 due in part to the timing of run-of-series commitments. In addition, as we shift to more original content, there will be greater variability in content obligations quarter-to-quarter due to the timing of when productions start. We early-adopted the new content accounting standard (ASU 2019-2) in Q1’19. There is no material impact as our content accounting policies are already consistent with the new rules. Paid net adds in Q1 were 9.6 million (with 1.74m in the US and 7.86m internationally), up 16% year over year, representing a new quarterly record.

As always, our quarterly guidance is our internal forecast at the time we report. For Q2’19, we project total paid net adds of 5.0m (-8% year over year), with 0.3m in the US and 4.7m for the international segment. This would put us at 14.6m paid net adds for the first half of 2019, up 7% year over year.

The image above shows Netflix's forecast of paid net ads for Q2:2019, and what is immediately noticable is how close the 2019 forecast line is to the 2018 paid net adds. Compare this with the large gap between the 2017 and 2018 net adds in numbers for Netflix. So the growth in their subscriber numbers are slowing down. In fact they predict an 8% decline in net ads for Q2:2019 compared to the previous year. With new subscriber numbers growing at a slower rate, they will have to pass on higher prices to consumers if they want to earn bigger profits and see that lofty stock price valuation justified

Below is what the Netflix had to say regarding price increases they are busy implementing.

We’re working our way through a series of price increases in the US, Brazil, Mexico and parts of Europe. The response in the US so far is as we expected and is tracking similarly to what we saw in Canada following our Q4’18 increase, where our gross additions are unaffected, and we see some modest short-term churn effect as members consent to the price change. We’re looking forward to a strong slate of global content in the second half of the year, including new seasons of some of our biggest series, Stranger Things (July 4th), 13 Reasons Why, Orange is the New Black, The Crown and La Casa de Papel (aka Money Heist) as well as big films like Michael Bay’s Six Underground and Martin Scorsese’s The Irishman, and expect another year of record annual paid net adds in 2019. We forecast an acceleration in both streaming ARPU (+2% vs. -2%) and total revenue growth (26% vs. 22%) in Q2 vs. Q1. Excluding currency, we forecast streaming ARPU and total revenue would rise 7% and 32%, respectively in Q2.

While there will be some quarter-to-quarter lumpiness in operating margins due to the timing of spending, our full year 2019 operating margin target of 13% is unchanged, which means that we expect operating margin in the second half of the year will be higher than the first half

We’re working our way through a series of price increases in the US, Brazil, Mexico and parts of Europe. The response in the US so far is as we expected and is tracking similarly to what we saw in Canada following our Q4’18 increase, where our gross additions are unaffected, and we see some modest short-term churn effect as members consent to the price change. We’re looking forward to a strong slate of global content in the second half of the year, including new seasons of some of our biggest series, Stranger Things (July 4th), 13 Reasons Why, Orange is the New Black, The Crown and La Casa de Papel (aka Money Heist) as well as big films like Michael Bay’s Six Underground and Martin Scorsese’s The Irishman, and expect another year of record annual paid net adds in 2019. We forecast an acceleration in both streaming ARPU (+2% vs. -2%) and total revenue growth (26% vs. 22%) in Q2 vs. Q1. Excluding currency, we forecast streaming ARPU and total revenue would rise 7% and 32%, respectively in Q2.

While there will be some quarter-to-quarter lumpiness in operating margins due to the timing of spending, our full year 2019 operating margin target of 13% is unchanged, which means that we expect operating margin in the second half of the year will be higher than the first half

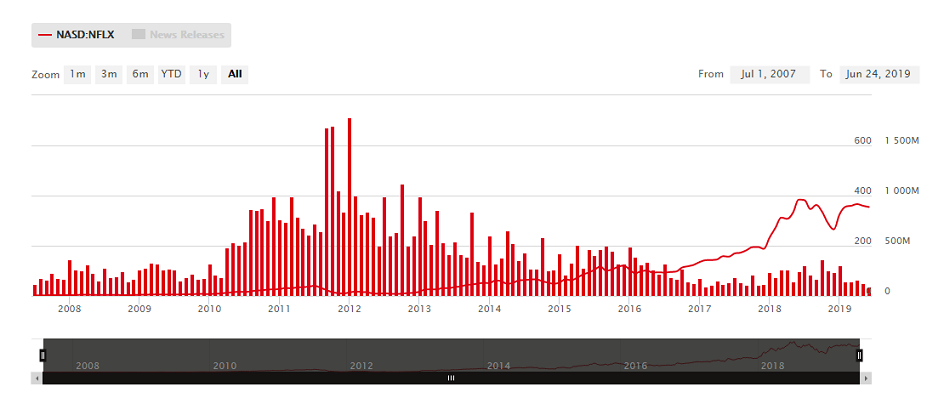

Netflix (NASDAQ: NFLX) share price history

Netflix (NASDAQ:NFLX) share price history since 2007. As the graphic shows its been a pretty steep upwards trajectory for the group's share price over the last couple of years especially in 2018 in which the group's share price surged from around $200 a share to at one point being close to $400 a share.

Netflix share price history since 2007

So should you Netflix shares?

Well they are the single biggest largest internet entertainment company in the world, and one of the biggest companies in the world (based on their market capital). They have a tremendous following and have a head start in the arena which Disney has now decided to join in on. Netflix had the following to say regarding increased competition.

Recently, Apple and Disney each unveiled their direct-to-consumer subscription video services. Both companies are world class consumer brands and we’re excited to compete; the clear beneficiaries will be content creators and consumers who will reap the rewards of many companies vying to provide a great video experience for audiences.

We don’t anticipate that these new entrants will materially affect our growth because the transition from linear to on demand entertainment is so massive and because of the differing nature of our content offerings. We believe we’ll all continue to grow as we each invest more in content and improve our service and as consumers continue to migrate away from linear viewing (similar to how US cable networks collectively grew for years as viewing shifted from broadcast networks during the 1980s and 1990s). We believe there is vast demand for watching great TV and movies and Netflix only satisfies a small portion of that demand. Last quarter, we talked about how our streaming hours in the US (our most mature market) on TV still only represents roughly 10% of total TV usage. We are much smaller and have even more room to grow in other countries and on other devices like mobile. For instance, Sandvine estimates our share of global downstream mobile internet traffic is about 2%.

Based on the above it is clear that Netflix doesn't think that the competition entering the market will have a material effect on them and their business. But we have our reservations.

Recently, Apple and Disney each unveiled their direct-to-consumer subscription video services. Both companies are world class consumer brands and we’re excited to compete; the clear beneficiaries will be content creators and consumers who will reap the rewards of many companies vying to provide a great video experience for audiences.

We don’t anticipate that these new entrants will materially affect our growth because the transition from linear to on demand entertainment is so massive and because of the differing nature of our content offerings. We believe we’ll all continue to grow as we each invest more in content and improve our service and as consumers continue to migrate away from linear viewing (similar to how US cable networks collectively grew for years as viewing shifted from broadcast networks during the 1980s and 1990s). We believe there is vast demand for watching great TV and movies and Netflix only satisfies a small portion of that demand. Last quarter, we talked about how our streaming hours in the US (our most mature market) on TV still only represents roughly 10% of total TV usage. We are much smaller and have even more room to grow in other countries and on other devices like mobile. For instance, Sandvine estimates our share of global downstream mobile internet traffic is about 2%.

Based on the above it is clear that Netflix doesn't think that the competition entering the market will have a material effect on them and their business. But we have our reservations.

Netflix (NASDAQ: NFLX) stock valuation

With all things considered regarding their footprint, their size of the market, the competition coming and their latest financial results and the slower growth in Netflix new subscriber numbers we have to wonder about the very high price tag the market has assigned to them. Their earnings reports for the next couple of years will have to be absolutely amazing for Netflix to justify trading at their current price. We believe the market has pushed the company's stock up way to far way to fast and predict Netflix will drop like a stone of their earnings even hint at disappointing market expectations. We would therefore caution investors against buying Netflix shares at it's current price levels.

While we acknowledge the potential of the group and their future earnings once price increases can be passed on to a ever increasing subsriber base, we believe in value buying and we do not see any value in Netflix at it's current price. Our most favourable valuation model, based on their own earnings guidance and latest financial results value Netflix shares at $274.30 a share. And even that is being very favourable and optimistic regarding Netflix's future earnings potential.