|

Related Topics |

|

Latest Financial Results for KAP industrial: We take a look at the full year financial results of KAP Industrial Holdings for the year end June 2019.

KAP Industrial Holdings Limited (KAP) is a JSE-listed diversified industrial group consisting of industrial, chemical and logistics business |

|

About KAP

KAP Industrial Holdings Limited (KAP) is a JSE-listed diversified industrial group consisting of industrial, chemical and logistics businesses. The group is focused on delivering on its strategy of being a market leader in the industries it serves in a growing African market.

In July 2003, Daun & Cie gained control of Kolosus, a JSE-listed company, which was used as the basis for new transactions, mainly the acquisition of a diversified group of manufacturing companies. Kolosus then became KAP, with the new name being derived from the German translation of the Cape of Good Hope (Kap der Guten Hoffnung) and was listed on the JSE in 2004.

KAP acquired the industrial assets of Steinhoff Africa in 2012, and restructured into three distinct segments – diversified industrial, diversified chemical and diversified logistics – in January 2017. KAP is now truly a leading industrial business in southern Africa and has moved from a small-cap to a mid-cap listed company on the JSE. “KAP is independently funded, independently managed with strong governance structures, and maintains a clear strategy with a very effective management team.”

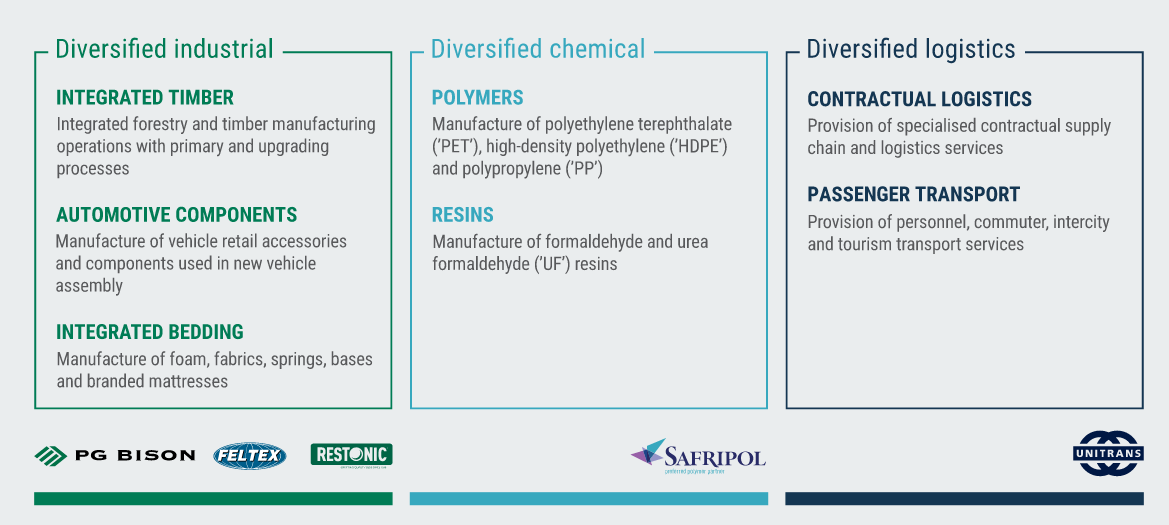

The image below provides a more detailed overview of KAP's divisions and their products and services delivered.

In July 2003, Daun & Cie gained control of Kolosus, a JSE-listed company, which was used as the basis for new transactions, mainly the acquisition of a diversified group of manufacturing companies. Kolosus then became KAP, with the new name being derived from the German translation of the Cape of Good Hope (Kap der Guten Hoffnung) and was listed on the JSE in 2004.

KAP acquired the industrial assets of Steinhoff Africa in 2012, and restructured into three distinct segments – diversified industrial, diversified chemical and diversified logistics – in January 2017. KAP is now truly a leading industrial business in southern Africa and has moved from a small-cap to a mid-cap listed company on the JSE. “KAP is independently funded, independently managed with strong governance structures, and maintains a clear strategy with a very effective management team.”

The image below provides a more detailed overview of KAP's divisions and their products and services delivered.

Advertisement

So to the numbers we go

Highlights of the financial results reported by KAP in their financial results are as follows:

From continuing operations

From continuing and discontinued operations

The numbers we are interested in are discussed below:

From continuing operations

- Revenue increased by 12% to R25 602 million, from R22 813 million in the prior corresponding period.

- Operating profit before capital items decreased by 13% to R2 527 million, from R2 901 million in the prior corresponding period.

- Headline earnings per share (“HEPS”) decreased by 25% to 45.9 cents per share, from 61.6 cents per share in the prior corresponding period.

- Earnings per share (“EPS”) decreased by 31% to 41.4 cents per share, from 59.6 cents per share in the prior corresponding period.

From continuing and discontinued operations

- Revenue increased by 12% to R25 765 million, from R23 038 million in the prior corresponding period.

- Operating profit before capital items decreased by 14% to R2 445 million, from R2 842 million in the prior corresponding period.

- HEPS decreased by 28% to 42.9 cents per share, from 59.8 cents per share in the prior corresponding period.

- EPS decreased by 34% to 38.3 cents per share, from 57.7 cents per share in the prior corresponding period.

- Net asset value per share (“NAVPS”) increased by 4% to 474 cents per share, from 454 cents per share in the prior corresponding period

- Dividend per share (“DPS”) at 23 cents per share, unadjusted from the prior corresponding period.

The numbers we are interested in are discussed below:

- PE ratio: 11.39

- Dividend yield: 4.7%

- Cash generated from operations: R4 billion

- Cash generated per share: R1.47 a share

- Price to book value: 1.03 (basically trading at the same price as the net asset value)

- Cash on balance sheet: R1.785 billion

- Cash per share: 66c a share (or 13.5% of their share price)

So any comments or guidance from management on the results?

Integrated Timber

The Integrated Timber division comprises forestry, sawmilling, pole manufacture, panel manufacture and upgrading operations. In line with international industry peers, the resin manufacturing and paper impregnation operations are now reported as part of this division (previously reported as part of the diversified chemical segment), as they represent strategic raw materials to the panel products operation and reflect the group’s strategy of integration (prior year segmental analysis has been restated for comparative purposes). The division’s panel products operations performed well for the year, showing volume, revenue and operating profit growth. It continued to pursue its strategy of technology investments to reduce its cost of manufacture, increase the proportion of value-added products and grow market share. The division’s performance was positively impacted by the postponement of certain plant maintenance shutdowns. The required maintenance activities will be completed in conjunction with plant expansions planned in F2020, thereby minimising overall production downtime. The division continued to drive exports to ensure process optimisation through its plants. It discontinued the sale and distribution of solid surfacing and high-pressure laminate products during the year in order to focus on its own manufactured products. The resin operation performed well for the year with increased volume and improved sales mix. The division’s forestry, sawmilling and pole operations in the southern Cape were significantly impacted by the operational effects of the extensive fires experienced in the region during 2017 and 2018, which had a R68 million negative impact on the division’s operating results compared to the prior year. The division has initiated new projects to expand particleboard capacity and improve efficiencies at both its Ugie and Piet Retief plants, which will be commissioned in February and March 2020 respectively. An additional MFB (melamine-faced board) upgrading press at Piet Retief will be commissioned in August 2019. The combined cost of these investments will be approximately R200 million, the majority of which will be incurred in F2020

Automotive components

An 11% increase in industry new vehicle assembly volumes over the prior comparative period supported the revenue, volume and profit growth of the division. The model replacements of the VW Polo and the BMW X3 introduced during the previous financial year were ramped up as planned. Efficiency improvement projects and new technologies associated with the new model introductions were successfully implemented during the second half of the year. The aftermarket accessories business was rationalised during the year. In this regard, the Maxe operations, which are aligned with the strategy of the division and remain an area of potential expansion, performed well for the year in spite of subdued industry new vehicle sales volumes. A process for the disposal of the remaining aftermarket accessories operations was initiated during the year and will be completed during F2020. These operations, including closure costs, are reflected as discontinued operations in the company’s income statement (prior year figures have been restated for comparative purposes). The extension of the Automotive Production and Development Programme (APDP) to 2035 provides much-needed clarity and stability to the automotive sector, which management believes will lead to growth opportunities for the division. Production disruptions associated with the introduction of a replacement model are expected during F2020

Integrated bedding

The Integrated Bedding division produced pleasing results for the year in the context of a depressed retail environment. The division continued to implement its strategy of technology investments to reduce its cost of manufacture, further integrate into the manufacture of its primary raw materials, develop its brands and grow market share. Following the acquisition of Support-a-Paedic during the previous financial year, the division continued to grow its market share and brand equity. It was able to grow volumes during the year in line with its strategy. This facilitated a 23% increase in intra-divisional revenue, which supported margins. The unexpected high volumes achieved during retail ‘Black Friday’ promotions impacted negatively on the division during the first half of the year. Excess volumes in this regard proved beneficial during the second half, which is traditionally a low demand period. The mattress manufacturing and process automation investments associated with the R250 million Integrated Bedding plant in Johannesburg will be completed before the 2019 peak trading period, which will facilitate production efficiencies at higher production volumes. The division has made strong progress in adjusting its business model to support increased retail promotional activities

Diversified chemicals

The recently expanded PET operation in Durban ran at an average of 93% of rated capacity for the year, excluding a post-commissioning shutdown during July 2018, which affected 14 days’ production. Production yields improved from 92% to 96% during the year. The plant was also successfully tested to 108% of nameplate capacity and separately tested to 98% yield. Demand for the product was strong during the first half of the year, however demand weakened during the second half of the year, a traditionally slower period, which necessitated increased exports at lower margins. HDPE operations ran above normal capacity for the year due to increased availability of ethylene raw material, which was consistent with the prior year. While global and South African demand for HDPE remained stable, volumes were impacted by an industry strike in 1H19. Margins were particularly volatile during the year; the delayed commissioning of new ethylene capacity in the United States resulted in elevated margins during the first half, with significant margin weakness during the second half as this capacity was commissioned. PP operations ran marginally below capacity as a result of two unscheduled shutdowns that affected five days’ production during the first half of the year. Demand for the product remained buoyant and in excess of production capacity. Margins weakened during the second half as a result of increased global polypropylene capacity and aggressive competitor activity. The division is expected to continue its strong operational performance in terms of production volumes and efficiency levels. The final debottlenecking project in the PET operations, which will cost R50 million, will improve the operational metrics of the plant and is scheduled to be completed over seven days during 2H20. Margins are expected to remain volatile, with some weakness, as the global monomer and polymer production capacity expansion activities take time to be absorbed by markets. The International Trade Administration Commission of South Africa (ITAC) instituted a provisional anti-dumping duty of 22.9% on imports of PET originating from China with effect from 2 August 2019. The division will continue to export polymers to supplement local demand in order to maximise operational efficiencies

Contractual logistics- South Africa

This division is now reported separately from the group’s non-South African Contractual Logistics operations. A new executive management structure was implemented during the year to focus only on South African operations. The division’s operations and support functions were significantly restructured during the second half of the year, with steady month-onmonth improvements evident from January 2019. The division’s operations in the Petroleum, Mining and General Freight sectors remained stable, while its activities in the Chemicals and Cement sectors were negatively impacted by lower customer volumes. The performance in the division’s Food-related activities was poor, primarily as a result of margin pressure in the poultry sector and a significant contractual dispute, for which the division has initiated arbitration proceedings. Operating profit was further negatively impacted by a R50 million non-operating provision for an onerous contract. During the year, the division renewed contracts with annualised revenue of R913 million; secured new contracts with annualised revenue of R426 million; and was unsuccessful in contract renewals with annualised revenue of R86 million

Contractual logistics:- Africa

Contractual Logistics’ operations in non-South African territories comprise mainly of activities in the Petrochemical and Agricultural sectors, with smaller operations in Mining and Cement, in southern and east African countries. Following the sale of 45% of USCS, the non-South African operations are managed and reported separately as Unitrans Africa Proprietary Limited. A new executive management structure was implemented on 1 December 2018 to focus only on non-South African operations. The division performed well for the year, supported by stable volumes at its major operations and good operational execution. The impact of Cyclone Idai on the division’s Beira operations was effectively mitigated by management and insurance. With a significant number of contracts at or nearing renewal stage, the division is focused on contract retention, volume growth, technology investments and efficiency improvements in an increasingly competitive environment. Management also continues to focus on growth opportunities in its existing territories, existing and new industry sectors and areas of operation.

Passenger transport

The Passenger Transport division found trading conditions challenging during the year, particularly during the second half. The Intercity and Tourism operations experienced lower industry passenger numbers and aggressive competition on all routes. In the divisions’ legacy commuter contracts, it was unable to recover the impact of inflated fuel costs. The impact of a 19% higher average diesel price compared to the prior year, which the division was unable to contractually recover, amounted to R54 million for the year. The remainder of the commuter and personnel travel operations performed satisfactorily for the year in spite of a particularly challenging environment with increasing unemployment levels. The division’s Mozambique operations performed well, showing revenue and profit growth. The primary focus of this division is the renegotiation of onerous conditions in its commuter contracts and the rationalisation or sale of its Intercity operations. The division continues to pursue growth opportunities where it can earn acceptable returns, including further expansion in Mozambique

Outlook

The macroeconomic and political environment in South Africa is expected to remain challenging and uncertain for the foreseeable future, with limited real economic growth and subdued consumer spending. The company remains focused on the execution of its strategy, the optimisation of its operations, market share growth and generation of cash to further strengthen its balance sheet and to provide a platform for growth. Various new capacity expansion projects and technology investments have been initiated that will be commissioned during F2020. Management continue to seek out further capacity expansion opportunities, in line with the group’s strategy in order to grow earnings and enhance shareholder returns. Acquisition opportunities that meet the group’s strategic requirements and create shareholder value remain a key element of the growth objectives of management. It is anticipated that the current distressed economic environment will yield increased opportunities in this regard.

The Integrated Timber division comprises forestry, sawmilling, pole manufacture, panel manufacture and upgrading operations. In line with international industry peers, the resin manufacturing and paper impregnation operations are now reported as part of this division (previously reported as part of the diversified chemical segment), as they represent strategic raw materials to the panel products operation and reflect the group’s strategy of integration (prior year segmental analysis has been restated for comparative purposes). The division’s panel products operations performed well for the year, showing volume, revenue and operating profit growth. It continued to pursue its strategy of technology investments to reduce its cost of manufacture, increase the proportion of value-added products and grow market share. The division’s performance was positively impacted by the postponement of certain plant maintenance shutdowns. The required maintenance activities will be completed in conjunction with plant expansions planned in F2020, thereby minimising overall production downtime. The division continued to drive exports to ensure process optimisation through its plants. It discontinued the sale and distribution of solid surfacing and high-pressure laminate products during the year in order to focus on its own manufactured products. The resin operation performed well for the year with increased volume and improved sales mix. The division’s forestry, sawmilling and pole operations in the southern Cape were significantly impacted by the operational effects of the extensive fires experienced in the region during 2017 and 2018, which had a R68 million negative impact on the division’s operating results compared to the prior year. The division has initiated new projects to expand particleboard capacity and improve efficiencies at both its Ugie and Piet Retief plants, which will be commissioned in February and March 2020 respectively. An additional MFB (melamine-faced board) upgrading press at Piet Retief will be commissioned in August 2019. The combined cost of these investments will be approximately R200 million, the majority of which will be incurred in F2020

Automotive components

An 11% increase in industry new vehicle assembly volumes over the prior comparative period supported the revenue, volume and profit growth of the division. The model replacements of the VW Polo and the BMW X3 introduced during the previous financial year were ramped up as planned. Efficiency improvement projects and new technologies associated with the new model introductions were successfully implemented during the second half of the year. The aftermarket accessories business was rationalised during the year. In this regard, the Maxe operations, which are aligned with the strategy of the division and remain an area of potential expansion, performed well for the year in spite of subdued industry new vehicle sales volumes. A process for the disposal of the remaining aftermarket accessories operations was initiated during the year and will be completed during F2020. These operations, including closure costs, are reflected as discontinued operations in the company’s income statement (prior year figures have been restated for comparative purposes). The extension of the Automotive Production and Development Programme (APDP) to 2035 provides much-needed clarity and stability to the automotive sector, which management believes will lead to growth opportunities for the division. Production disruptions associated with the introduction of a replacement model are expected during F2020

Integrated bedding

The Integrated Bedding division produced pleasing results for the year in the context of a depressed retail environment. The division continued to implement its strategy of technology investments to reduce its cost of manufacture, further integrate into the manufacture of its primary raw materials, develop its brands and grow market share. Following the acquisition of Support-a-Paedic during the previous financial year, the division continued to grow its market share and brand equity. It was able to grow volumes during the year in line with its strategy. This facilitated a 23% increase in intra-divisional revenue, which supported margins. The unexpected high volumes achieved during retail ‘Black Friday’ promotions impacted negatively on the division during the first half of the year. Excess volumes in this regard proved beneficial during the second half, which is traditionally a low demand period. The mattress manufacturing and process automation investments associated with the R250 million Integrated Bedding plant in Johannesburg will be completed before the 2019 peak trading period, which will facilitate production efficiencies at higher production volumes. The division has made strong progress in adjusting its business model to support increased retail promotional activities

Diversified chemicals

The recently expanded PET operation in Durban ran at an average of 93% of rated capacity for the year, excluding a post-commissioning shutdown during July 2018, which affected 14 days’ production. Production yields improved from 92% to 96% during the year. The plant was also successfully tested to 108% of nameplate capacity and separately tested to 98% yield. Demand for the product was strong during the first half of the year, however demand weakened during the second half of the year, a traditionally slower period, which necessitated increased exports at lower margins. HDPE operations ran above normal capacity for the year due to increased availability of ethylene raw material, which was consistent with the prior year. While global and South African demand for HDPE remained stable, volumes were impacted by an industry strike in 1H19. Margins were particularly volatile during the year; the delayed commissioning of new ethylene capacity in the United States resulted in elevated margins during the first half, with significant margin weakness during the second half as this capacity was commissioned. PP operations ran marginally below capacity as a result of two unscheduled shutdowns that affected five days’ production during the first half of the year. Demand for the product remained buoyant and in excess of production capacity. Margins weakened during the second half as a result of increased global polypropylene capacity and aggressive competitor activity. The division is expected to continue its strong operational performance in terms of production volumes and efficiency levels. The final debottlenecking project in the PET operations, which will cost R50 million, will improve the operational metrics of the plant and is scheduled to be completed over seven days during 2H20. Margins are expected to remain volatile, with some weakness, as the global monomer and polymer production capacity expansion activities take time to be absorbed by markets. The International Trade Administration Commission of South Africa (ITAC) instituted a provisional anti-dumping duty of 22.9% on imports of PET originating from China with effect from 2 August 2019. The division will continue to export polymers to supplement local demand in order to maximise operational efficiencies

Contractual logistics- South Africa

This division is now reported separately from the group’s non-South African Contractual Logistics operations. A new executive management structure was implemented during the year to focus only on South African operations. The division’s operations and support functions were significantly restructured during the second half of the year, with steady month-onmonth improvements evident from January 2019. The division’s operations in the Petroleum, Mining and General Freight sectors remained stable, while its activities in the Chemicals and Cement sectors were negatively impacted by lower customer volumes. The performance in the division’s Food-related activities was poor, primarily as a result of margin pressure in the poultry sector and a significant contractual dispute, for which the division has initiated arbitration proceedings. Operating profit was further negatively impacted by a R50 million non-operating provision for an onerous contract. During the year, the division renewed contracts with annualised revenue of R913 million; secured new contracts with annualised revenue of R426 million; and was unsuccessful in contract renewals with annualised revenue of R86 million

Contractual logistics:- Africa

Contractual Logistics’ operations in non-South African territories comprise mainly of activities in the Petrochemical and Agricultural sectors, with smaller operations in Mining and Cement, in southern and east African countries. Following the sale of 45% of USCS, the non-South African operations are managed and reported separately as Unitrans Africa Proprietary Limited. A new executive management structure was implemented on 1 December 2018 to focus only on non-South African operations. The division performed well for the year, supported by stable volumes at its major operations and good operational execution. The impact of Cyclone Idai on the division’s Beira operations was effectively mitigated by management and insurance. With a significant number of contracts at or nearing renewal stage, the division is focused on contract retention, volume growth, technology investments and efficiency improvements in an increasingly competitive environment. Management also continues to focus on growth opportunities in its existing territories, existing and new industry sectors and areas of operation.

Passenger transport

The Passenger Transport division found trading conditions challenging during the year, particularly during the second half. The Intercity and Tourism operations experienced lower industry passenger numbers and aggressive competition on all routes. In the divisions’ legacy commuter contracts, it was unable to recover the impact of inflated fuel costs. The impact of a 19% higher average diesel price compared to the prior year, which the division was unable to contractually recover, amounted to R54 million for the year. The remainder of the commuter and personnel travel operations performed satisfactorily for the year in spite of a particularly challenging environment with increasing unemployment levels. The division’s Mozambique operations performed well, showing revenue and profit growth. The primary focus of this division is the renegotiation of onerous conditions in its commuter contracts and the rationalisation or sale of its Intercity operations. The division continues to pursue growth opportunities where it can earn acceptable returns, including further expansion in Mozambique

Outlook

The macroeconomic and political environment in South Africa is expected to remain challenging and uncertain for the foreseeable future, with limited real economic growth and subdued consumer spending. The company remains focused on the execution of its strategy, the optimisation of its operations, market share growth and generation of cash to further strengthen its balance sheet and to provide a platform for growth. Various new capacity expansion projects and technology investments have been initiated that will be commissioned during F2020. Management continue to seek out further capacity expansion opportunities, in line with the group’s strategy in order to grow earnings and enhance shareholder returns. Acquisition opportunities that meet the group’s strategic requirements and create shareholder value remain a key element of the growth objectives of management. It is anticipated that the current distressed economic environment will yield increased opportunities in this regard.

So should you buy their shares?

To be honest we do find their product mix of goods being held rather strange. But the group and their investors will argue it is a well diversified portfolio. They do hold quality assets even though it is spread across vastly different sectors. We like the management team and the strong cash position and the extremely strong cash generating capacity of the group. What we would like to see at some stage is the group announcing a share buy back plan as the amount of shares currently in issue being excessive with them having 2.7 billion shares in issue.

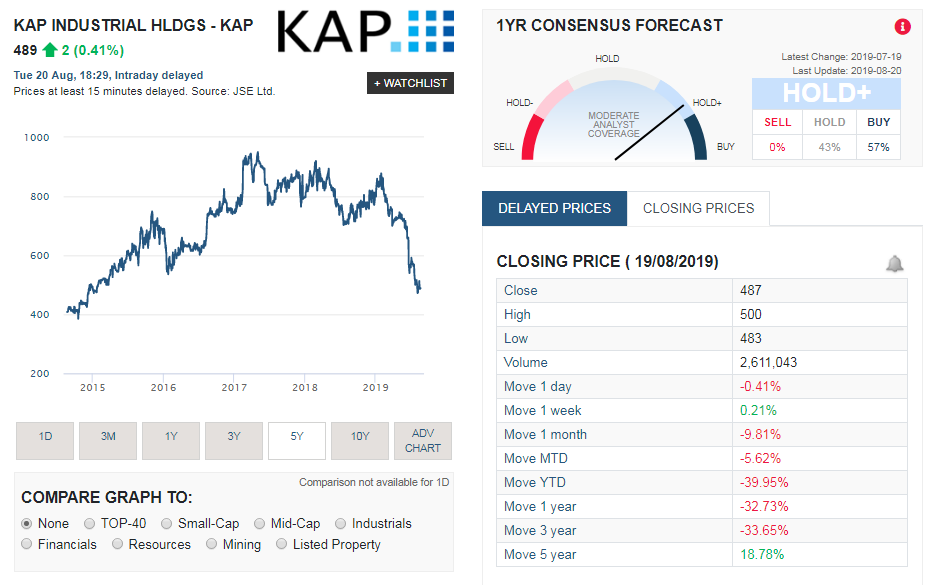

KAP share price history

The screenshot below taken from Sharenet shows KAP's share price history over the last 5 years. And as the image shows its been a pretty wild ride for KAP investors with the group having seen strong gains and declines over the last 5 years.

The summary below shows the share price returns of KAP over various time periods.

- 1 week: 0.21%

- 1 month: -9.81%

- Year to date (YTD): -39.95%

- 1 year: -32.73%

- 3 years: -33.65%

- 5 years: 18.78%

KAP industrial holdings valuation

In our previous KAP valuation (at the release of their interim results) we valued the group's shares at R10.31. So based on their latest financial results what do we value the group at right now? Based on the slight decline in profits, the fact that dividends remained the same, their solid cash position and cash generating capacity we value the group's shares at R8.39 a share based on their latest financial results. We therefore believe they offer good value to patient long term investors as the value of their quality assets will shine through in the long run.