|

PSG daily investment update 22 May 2019

Date: 21 May 2019 Category: Stock Market |

Related Topics |

|

In our continued efforts to give our readers a broad number of views, opinions and information, we continue to provide PSG's daily market updates and add our own daily rant at the end.

|

|

Short summary of PSG's market commentary for 22 May 2019

South Africa

The JSE closed lower on Tuesday, despite global sentiment improving a little after the US temporarily lifted its ban on Chinese telecoms giant Huawei. Today investors will watch the release of US Federal Reserve minutes and SARB’s interest rate decision on Thursday. The All Share fell 0.17%.

United States

Technology stocks fueled a rebound on Wall Street on Tuesday after the US temporarily eased curbs on China’s Huawei Technologies, raising expectations that the two countries would work toward a trade deal. After the ALSI closed, the Dow had firmed by 0.72%.

Europe

European shares rose on Tuesday, with tech shares contributing to gains as they recovered some ground lost in the previous session following a temporary easing of US restrictions on China’s Huawei. At the JSE’s close, the FTSE 100 was up by 0.25% and the DAX by 0.87%.

Hong Kong

The Hang Seng dropped on Tuesday as investors worried about the risk of escalating trade tensions between Washington and Beijing despite a temporary easing of restrictions on China’s Huawei. The index closed down by 0.20%.

Japan

The Nikkei slipped on Tuesday as Washington’s blacklisting of Huawei took a heavy toll on suppliers to the Chinese telecoms equipment maker, but the downside was limited after the US temporarily eased trade restrictions. The Nikkei ended 0.14% lower.

Rand

The rand was slightly weaker on Tuesday, as the US-China trade war continued to weigh on emerging market currencies. At 20h10, a dollar traded at R14.39.

Precious metals

Gold eased on Tuesday as increasing bets that the US Fed will not cut interest rates this year boosted the dollar. At 20h15, an ounce of spot gold traded at $1273.89.

Oil

Oil prices rose on Tuesday on escalating US-Iran tensions and amid expectations that oil cartel Opec producers will continue to curb supply this year. A barrel of Brent crude traded at $72.23 at 20h15.

The JSE closed lower on Tuesday, despite global sentiment improving a little after the US temporarily lifted its ban on Chinese telecoms giant Huawei. Today investors will watch the release of US Federal Reserve minutes and SARB’s interest rate decision on Thursday. The All Share fell 0.17%.

United States

Technology stocks fueled a rebound on Wall Street on Tuesday after the US temporarily eased curbs on China’s Huawei Technologies, raising expectations that the two countries would work toward a trade deal. After the ALSI closed, the Dow had firmed by 0.72%.

Europe

European shares rose on Tuesday, with tech shares contributing to gains as they recovered some ground lost in the previous session following a temporary easing of US restrictions on China’s Huawei. At the JSE’s close, the FTSE 100 was up by 0.25% and the DAX by 0.87%.

Hong Kong

The Hang Seng dropped on Tuesday as investors worried about the risk of escalating trade tensions between Washington and Beijing despite a temporary easing of restrictions on China’s Huawei. The index closed down by 0.20%.

Japan

The Nikkei slipped on Tuesday as Washington’s blacklisting of Huawei took a heavy toll on suppliers to the Chinese telecoms equipment maker, but the downside was limited after the US temporarily eased trade restrictions. The Nikkei ended 0.14% lower.

Rand

The rand was slightly weaker on Tuesday, as the US-China trade war continued to weigh on emerging market currencies. At 20h10, a dollar traded at R14.39.

Precious metals

Gold eased on Tuesday as increasing bets that the US Fed will not cut interest rates this year boosted the dollar. At 20h15, an ounce of spot gold traded at $1273.89.

Oil

Oil prices rose on Tuesday on escalating US-Iran tensions and amid expectations that oil cartel Opec producers will continue to curb supply this year. A barrel of Brent crude traded at $72.23 at 20h15.

Our daily update

We have a few updates today:

Firstly lets start with Bidcorp that released a trading update yesterday. Below a short summary of the trading update.

Current trading performance and overall market conditions of continuing operations

• Trading to the end of April F2019 continues to be positive (measured in home currencies). The Easter holidays fell in mid-April versus late March in F2018. Performance achieved by the Group remains on trend. Our large UK, European and Australasian businesses continue to perform well. Angliss China and South Africa remain challenging geographies however monthly performance is starting to improve against last year.

• Sales have continued to show real growth, with the gross margin percentage increasing. This has offset higher operating costs impacted by rising wage costs (due to full employment levels in numerous economies) and higher fuel and energy expenses. Overall trading margins are being maintained.

• Economic growth in the UK, Europe and Australasia remains supportive of the foodservice industry. Food inflation remains relatively benign across most markets. • Currency volatility has positively impacted Bidcorp’s rand translated results. The rand translated results are approximately 4,5% higher than the constant currency results to the end of April 2019. • Acquisition opportunities are being limited by unrealistic vendor valuation expectations at this stage of the cycle, a consequence of which is that fewer bolt-on acquisitions have been concluded. Focus remains on extracting the benefits from some of the more recent acquisitions, most notably in Australia, Iberia and Germany.

• We continue to invest in organic growth through ongoing capex spend, with the focus on having more but smaller depots closer to the customer base.

• Further evolution (not revolution) of our ecommerce and CRM platforms continue to provide competitive advantage across all businesses in the Group. Our global procurement initiatives are expanding both in Asia and Europe, the benefits of which reflect in each individual business.

• Bidcorp’s strategy remains focused on growth – organically in current markets through real sales growth focussed on the correct customer base; via in-territory bolt-on acquisitions to expand geographic reach and product ranges; and via strategic acquisitions as the group enters new markets. • Management’s expectations for F2019 remain unchanged.

Read the full article here

The next update covers an update on Reinet (RNI) share repurchase program released yesterday:

Reinet Investments S.C.A. has repurchased 201 599 ordinary shares in the period 13 to 17 May 2019. The shares were repurchased on the Johannesburg Stock Exchange at an average price of ZAR 230.27 per share (highest price: ZAR 236.05; lowest price: ZAR 225.13) for a total consideration of some ZAR 46.42 million (EUR 2.9 million), plus transaction costs.

These repurchases were made as part of the share buyback programme announced on 6 February 2019. The total number of shares repurchased under this programme to date is 3 056 416 ordinary shares for a total consideration of some ZAR 710.05 million (EUR 44.2 million), plus transaction costs.

So on average RNI has spent R232.29 a share to buy back their own shares since the share repurchase program was announced in February. We asked then if the group feels that there is no value in the markets , if it is using its cahs to buy back it's own shares instead of investing in new assets. We still believe that RNI doesn't see value in other assets, so they are using their cash to buy back their own shares.

Read the full financial results review and share repurchase program update here.

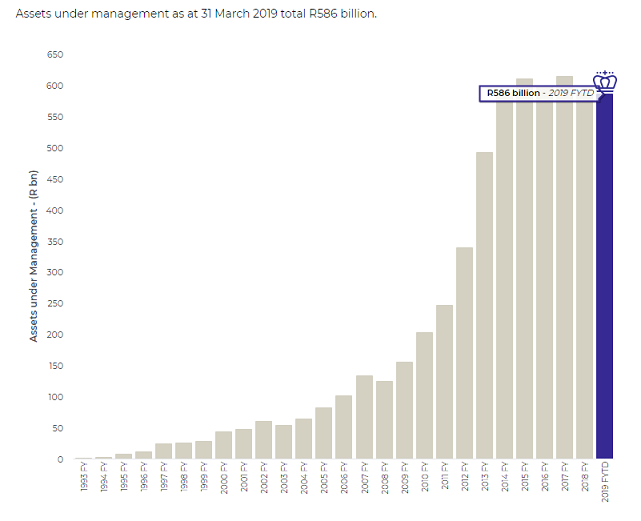

Lastly we take a look at Coronation's latest financial results, and to be honest they dont look to good. Group has been hit by poor market performances which means they earn less and less performance fees. Pressure from cheaper ETF/ETN products also starting to put a squeeze on their margins. The image below shows their assets under management per quarter.

Firstly lets start with Bidcorp that released a trading update yesterday. Below a short summary of the trading update.

Current trading performance and overall market conditions of continuing operations

• Trading to the end of April F2019 continues to be positive (measured in home currencies). The Easter holidays fell in mid-April versus late March in F2018. Performance achieved by the Group remains on trend. Our large UK, European and Australasian businesses continue to perform well. Angliss China and South Africa remain challenging geographies however monthly performance is starting to improve against last year.

• Sales have continued to show real growth, with the gross margin percentage increasing. This has offset higher operating costs impacted by rising wage costs (due to full employment levels in numerous economies) and higher fuel and energy expenses. Overall trading margins are being maintained.

• Economic growth in the UK, Europe and Australasia remains supportive of the foodservice industry. Food inflation remains relatively benign across most markets. • Currency volatility has positively impacted Bidcorp’s rand translated results. The rand translated results are approximately 4,5% higher than the constant currency results to the end of April 2019. • Acquisition opportunities are being limited by unrealistic vendor valuation expectations at this stage of the cycle, a consequence of which is that fewer bolt-on acquisitions have been concluded. Focus remains on extracting the benefits from some of the more recent acquisitions, most notably in Australia, Iberia and Germany.

• We continue to invest in organic growth through ongoing capex spend, with the focus on having more but smaller depots closer to the customer base.

• Further evolution (not revolution) of our ecommerce and CRM platforms continue to provide competitive advantage across all businesses in the Group. Our global procurement initiatives are expanding both in Asia and Europe, the benefits of which reflect in each individual business.

• Bidcorp’s strategy remains focused on growth – organically in current markets through real sales growth focussed on the correct customer base; via in-territory bolt-on acquisitions to expand geographic reach and product ranges; and via strategic acquisitions as the group enters new markets. • Management’s expectations for F2019 remain unchanged.

Read the full article here

The next update covers an update on Reinet (RNI) share repurchase program released yesterday:

Reinet Investments S.C.A. has repurchased 201 599 ordinary shares in the period 13 to 17 May 2019. The shares were repurchased on the Johannesburg Stock Exchange at an average price of ZAR 230.27 per share (highest price: ZAR 236.05; lowest price: ZAR 225.13) for a total consideration of some ZAR 46.42 million (EUR 2.9 million), plus transaction costs.

These repurchases were made as part of the share buyback programme announced on 6 February 2019. The total number of shares repurchased under this programme to date is 3 056 416 ordinary shares for a total consideration of some ZAR 710.05 million (EUR 44.2 million), plus transaction costs.

So on average RNI has spent R232.29 a share to buy back their own shares since the share repurchase program was announced in February. We asked then if the group feels that there is no value in the markets , if it is using its cahs to buy back it's own shares instead of investing in new assets. We still believe that RNI doesn't see value in other assets, so they are using their cash to buy back their own shares.

Read the full financial results review and share repurchase program update here.

Lastly we take a look at Coronation's latest financial results, and to be honest they dont look to good. Group has been hit by poor market performances which means they earn less and less performance fees. Pressure from cheaper ETF/ETN products also starting to put a squeeze on their margins. The image below shows their assets under management per quarter.

Our JSE All Share index daily performance calendar

Visit our JSE Calendar tracker page for a expanded version of the calendar below

The graphic below provides the daily returns of the JSE All Share Index (J203) on a calendar chart. Provides a great overview of the All share index over the course of the month. It will be updated daily with our daily investment update as received from PSG.

So after 4 consecutive months of positive returns on the JSE All Share Index, the month of May kicked of trading on a positive note. And then Donald Trump striked by ordering tariffs be raised on billions worth of goods imported from China. China then announced a set of retaliatory tariffs on US goods. So it looks like the trade war is back into full swing. And added to that it seems like tensions between Iran and the US are escalating too, after alleged sabotage of oil container ships by Iran (in which it is alleged that drones laden with explosives flew into these container ships). All of this is leading to the old adage, sell in May and go away. As the month of May is starting to wipe out the gains made from January 2019 to April 2019.

For more on daily market movements see our 2019 Calendar tracker.

But we as South African investors are losing out in Dollar terms. Largely due to continued Rand weakness not only over the short term but over the last couple of years. We continue to advise investors to take money out of South Africa and invest it offshore. Looking for ideas for investments to make? Go read this article

For more on daily market movements see our 2019 Calendar tracker.

But we as South African investors are losing out in Dollar terms. Largely due to continued Rand weakness not only over the short term but over the last couple of years. We continue to advise investors to take money out of South Africa and invest it offshore. Looking for ideas for investments to make? Go read this article