|

Bidcorp (BID) Capital Markets update regarding trading environment on 21 May 2019

Date: 21 May 2019 Category: Stock Market Share Price: R295.88 |

Related Topics |

|

We take a look at the SENS released by Bidcorp in which it provides investors, analysts and financial markets with an update regarding their trading environment. What follows (after the brief introduction into who Bidcorp is) below is as released by the group on SENS earlier today regarding their trading environment and current trading performance.

|

|

About Bidcorp (BID)

Bid Corporation Limited known as Bidcorp separated from Bidvest and listed on the JSE on Monday May 30 2016. The unbundling provides Bidvest shareholders with the opportunity to participate directly in Bidcorp’s foodservice operations, as well as enabling each of the businesses to achieve their respective strategic goals. Bidcorp will focus on realising the potential that exists in its current foodservice operations as well as acquisitive growth opportunities. Bidcorp is an international broad-line foodservice group, listed on the JSE, South Africa, and present in developed and developing economies in five continents. Focused on foodservice, the business comprises a mix of well-established leading and rapidly growing market positions, offering significant future upside. The profile of the customer base is strategically targeted to fully service the foodservice industry’s needs.

Bidcorp is a broadline foodservice group with a geographic reach encompassing over 34 countries on five continents. Bidcorp, operating as Bidfood in most geographies, has adopted a decentralised model of management which encourages the entrepreneurial spirit contained in each of its businesses. Each business is directly responsible for its product range, its buying and sales approach. Businesses in the different regions retain their local brand, tone of voice, look and feel specific to local culture.

Just like a truly great dish, a dynamic and successful foodservice partnership requires the right ingredients. As a leading distributor to the foodservice industry, Bidfood has come to understand this particular recipe intimately. It involves maintaining a balance between leading edge innovation and a consistent, reliable delivery of “the classics”. We offer a wide selection of local and internationally sourced products that have been tailored to suit all customer types – large and small. We believe that the key ingredients Bidfood brings together create a robust and forward looking framework for us to deliver the reliability, support and inspiration our customers have come to expect.

Bidcorp is a broadline foodservice group with a geographic reach encompassing over 34 countries on five continents. Bidcorp, operating as Bidfood in most geographies, has adopted a decentralised model of management which encourages the entrepreneurial spirit contained in each of its businesses. Each business is directly responsible for its product range, its buying and sales approach. Businesses in the different regions retain their local brand, tone of voice, look and feel specific to local culture.

Just like a truly great dish, a dynamic and successful foodservice partnership requires the right ingredients. As a leading distributor to the foodservice industry, Bidfood has come to understand this particular recipe intimately. It involves maintaining a balance between leading edge innovation and a consistent, reliable delivery of “the classics”. We offer a wide selection of local and internationally sourced products that have been tailored to suit all customer types – large and small. We believe that the key ingredients Bidfood brings together create a robust and forward looking framework for us to deliver the reliability, support and inspiration our customers have come to expect.

SENS released earlier today regarding the trading environment of the group

Current trading performance and overall market conditions of continuing operations

• Trading to the end of April F2019 continues to be positive (measured in home currencies). The Easter holidays fell in mid-April versus late March in F2018. Performance achieved by the Group remains on trend. Our large UK, European and Australasian businesses continue to perform well. Angliss China and South Africa remain challenging geographies however monthly performance is starting to improve against last year.

• Sales have continued to show real growth, with the gross margin percentage increasing. This has offset higher operating costs impacted by rising wage costs (due to full employment levels in numerous economies) and higher fuel and energy expenses. Overall trading margins are being maintained.

• Economic growth in the UK, Europe and Australasia remains supportive of the foodservice industry. Food inflation remains relatively benign across most markets. • Currency volatility has positively impacted Bidcorp’s rand translated results. The rand translated results are approximately 4,5% higher than the constant currency results to the end of April 2019. • Acquisition opportunities are being limited by unrealistic vendor valuation expectations at this stage of the cycle, a consequence of which is that fewer bolt-on acquisitions have been concluded. Focus remains on extracting the benefits from some of the more recent acquisitions, most notably in Australia, Iberia and Germany.

• We continue to invest in organic growth through ongoing capex spend, with the focus on having more but smaller depots closer to the customer base.

• Further evolution (not revolution) of our ecommerce and CRM platforms continue to provide competitive advantage across all businesses in the Group. Our global procurement initiatives are expanding both in Asia and Europe, the benefits of which reflect in each individual business.

• Bidcorp’s strategy remains focused on growth – organically in current markets through real sales growth focussed on the correct customer base; via in-territory bolt-on acquisitions to expand geographic reach and product ranges; and via strategic acquisitions as the group enters new markets. • Management’s expectations for F2019 remain unchanged.

Australasia

• Australia’s trading performance remains at anticipated levels. Revenue growth has been dampened by the exiting of a residual low margin contract in the latter part of calendar 2018. The core foodservice businesses are doing well, and the meat business is slowly improving. Supply Solutions (Imports) continues to perform well off the back of further upstream integration, such as cheese processing. Our focus on liquor continues to prove challenging but will be a key driver of growth in years to come. Further capex is being spent on organic expansion in foodservice. Bolt-on acquisition opportunities remain, however the current focus remains on performance improvement at Festival Liquor.

• New Zealand continues its solid performance. Revenue gains and margin improvements are being offset by higher costs, particularly labour (full employment and no migration) and the costs of recent increased capacity. All segments of the business continue to develop profitably with ongoing innovation and product development, particularly value add and processing. Further capacity expansion is being planned to accommodate organic growth.

United Kingdom (“UK”)

• Bidfood UK continues to perform well. Consumer confidence is being dented due to ‘Brexit’ fatigue. Sales volumes continue to grow in the independent sector as our focus on service levels continues. National account volume growth is being carefully managed in favour of improved margins. Business improvement initiatives continue to deliver margin improvements. Ecommerce implementation continues to gather traction. Further investment into increased distribution capacity remains a key focus to cater for anticipated growth. Growth in ‘own’ brands continues and importing of an exclusive range of brands is gaining traction. The acquisition of Punjab Kitchen (niche ready-meals business) in February will add to Bidfood’s manufacturing / value add products capability. An acquisition of an independent foodservice businesses is likely to conclude in Q1 F2020. • Trading in Bidfresh improved in Q3 however market conditions remain challenging. Our customer base has experienced the decline in the ‘casual dining’ segment as well as several suppliers going bankrupt. Seafood has performed well, Produce is getting better but the Meat division is taking longer than anticipated to reach scale. Management’s focus is on building the customer base in the Meat pillar.

Europe

• Overall results from our European businesses remains solid. Good like-for-like trading profit growth in constant FX has been achieved by the Netherlands, Belgium, Czech & Slovakia, Poland and Italy. Large cost increases, particularly labour and fuel, remain however do appear to be moderating. Our businesses are compensating for these by driving higher revenues and improved gross margins. Performance at Iberia and Germany remains below expectation although business improvement initiatives are starting to deliver improvements in both operations.

• Netherlands has maintained its good momentum despite a tightening labour market. Its business simplification journey with product range rationalisation and IT infrastructure reconfiguration is starting to benefit the overall cost base, improving net margins.

• Belgium’s performance is positive, delivering higher profitability. Volume growth in its freetrade and institutional sectors is ongoing. Depot consolidation between Bestfoods and Langens to achieve operational efficiencies in its infrastructure continue. Private label development in the freetrade segment is being pursued. The roll out of the ‘myBidfood’ ecommerce platform is ongoing.

• Czech & Slovakia continues to deliver a strong performance across all segments of the business. Economic growth is slowing however sales and gross margins have continued to grow. These have mitigated higher labour costs. Timely depot investments in F2018 have positioned the business well in terms of market share gains. Further infrastructure investment in depots is planned. Production facilities are operating at high capacities ahead of anticipated summer demand.

• Solid organic growth in Poland has continued, driven by focus on the freetrade sector. Development of the product range into both Asian cuisine and liquor is driving sales growth. Increased investment into customer focused IT initiatives are expected to grow market share. Further net margin improvement continues to be achieved.

• DAC Italy continues to grow with good penetration of the independent sector. Business and consumer confidence is holding up. D&D’s integration into DAC is ongoing. Procurement benefits in Italian product (sourced/ co-sourced from/ with DAC) continues to grow.

• Iberia comprises our businesses in Spain and Portugal. Overall performance in Spain is well below expectations. Improvements to the business platform through efficiencies in the infrastructure, a new ERP system and skilled people, are starting to show improvements however financial performance remains poor. Our business in Portugal goes from strength to strength. The bolt-on acquisition Igartza (July 2018), a multi-category distributor in northern Spain, is performing in line with expectations. Management remain positive about the growth opportunity in the Iberian market.

• Germany has underperformed however trading losses are narrowing. Work continues in building its business foundation including sales structures, IT platforms, human capital and infrastructure. Additional management, deployed to assist the local operators, is starting to make a difference. Germany still represents a very large foodservice opportunity.

• The Baltics, with a focus on Lithuania, is profitable. The new depot in Kaunas became operational in Q3. • Further expansion, both in terms of in-country bolt-on acquisitions and strategic entry into new geographies in Europe, remains possible, as we are not represented or underrepresented in many countries.

• Trading to the end of April F2019 continues to be positive (measured in home currencies). The Easter holidays fell in mid-April versus late March in F2018. Performance achieved by the Group remains on trend. Our large UK, European and Australasian businesses continue to perform well. Angliss China and South Africa remain challenging geographies however monthly performance is starting to improve against last year.

• Sales have continued to show real growth, with the gross margin percentage increasing. This has offset higher operating costs impacted by rising wage costs (due to full employment levels in numerous economies) and higher fuel and energy expenses. Overall trading margins are being maintained.

• Economic growth in the UK, Europe and Australasia remains supportive of the foodservice industry. Food inflation remains relatively benign across most markets. • Currency volatility has positively impacted Bidcorp’s rand translated results. The rand translated results are approximately 4,5% higher than the constant currency results to the end of April 2019. • Acquisition opportunities are being limited by unrealistic vendor valuation expectations at this stage of the cycle, a consequence of which is that fewer bolt-on acquisitions have been concluded. Focus remains on extracting the benefits from some of the more recent acquisitions, most notably in Australia, Iberia and Germany.

• We continue to invest in organic growth through ongoing capex spend, with the focus on having more but smaller depots closer to the customer base.

• Further evolution (not revolution) of our ecommerce and CRM platforms continue to provide competitive advantage across all businesses in the Group. Our global procurement initiatives are expanding both in Asia and Europe, the benefits of which reflect in each individual business.

• Bidcorp’s strategy remains focused on growth – organically in current markets through real sales growth focussed on the correct customer base; via in-territory bolt-on acquisitions to expand geographic reach and product ranges; and via strategic acquisitions as the group enters new markets. • Management’s expectations for F2019 remain unchanged.

Australasia

• Australia’s trading performance remains at anticipated levels. Revenue growth has been dampened by the exiting of a residual low margin contract in the latter part of calendar 2018. The core foodservice businesses are doing well, and the meat business is slowly improving. Supply Solutions (Imports) continues to perform well off the back of further upstream integration, such as cheese processing. Our focus on liquor continues to prove challenging but will be a key driver of growth in years to come. Further capex is being spent on organic expansion in foodservice. Bolt-on acquisition opportunities remain, however the current focus remains on performance improvement at Festival Liquor.

• New Zealand continues its solid performance. Revenue gains and margin improvements are being offset by higher costs, particularly labour (full employment and no migration) and the costs of recent increased capacity. All segments of the business continue to develop profitably with ongoing innovation and product development, particularly value add and processing. Further capacity expansion is being planned to accommodate organic growth.

United Kingdom (“UK”)

• Bidfood UK continues to perform well. Consumer confidence is being dented due to ‘Brexit’ fatigue. Sales volumes continue to grow in the independent sector as our focus on service levels continues. National account volume growth is being carefully managed in favour of improved margins. Business improvement initiatives continue to deliver margin improvements. Ecommerce implementation continues to gather traction. Further investment into increased distribution capacity remains a key focus to cater for anticipated growth. Growth in ‘own’ brands continues and importing of an exclusive range of brands is gaining traction. The acquisition of Punjab Kitchen (niche ready-meals business) in February will add to Bidfood’s manufacturing / value add products capability. An acquisition of an independent foodservice businesses is likely to conclude in Q1 F2020. • Trading in Bidfresh improved in Q3 however market conditions remain challenging. Our customer base has experienced the decline in the ‘casual dining’ segment as well as several suppliers going bankrupt. Seafood has performed well, Produce is getting better but the Meat division is taking longer than anticipated to reach scale. Management’s focus is on building the customer base in the Meat pillar.

Europe

• Overall results from our European businesses remains solid. Good like-for-like trading profit growth in constant FX has been achieved by the Netherlands, Belgium, Czech & Slovakia, Poland and Italy. Large cost increases, particularly labour and fuel, remain however do appear to be moderating. Our businesses are compensating for these by driving higher revenues and improved gross margins. Performance at Iberia and Germany remains below expectation although business improvement initiatives are starting to deliver improvements in both operations.

• Netherlands has maintained its good momentum despite a tightening labour market. Its business simplification journey with product range rationalisation and IT infrastructure reconfiguration is starting to benefit the overall cost base, improving net margins.

• Belgium’s performance is positive, delivering higher profitability. Volume growth in its freetrade and institutional sectors is ongoing. Depot consolidation between Bestfoods and Langens to achieve operational efficiencies in its infrastructure continue. Private label development in the freetrade segment is being pursued. The roll out of the ‘myBidfood’ ecommerce platform is ongoing.

• Czech & Slovakia continues to deliver a strong performance across all segments of the business. Economic growth is slowing however sales and gross margins have continued to grow. These have mitigated higher labour costs. Timely depot investments in F2018 have positioned the business well in terms of market share gains. Further infrastructure investment in depots is planned. Production facilities are operating at high capacities ahead of anticipated summer demand.

• Solid organic growth in Poland has continued, driven by focus on the freetrade sector. Development of the product range into both Asian cuisine and liquor is driving sales growth. Increased investment into customer focused IT initiatives are expected to grow market share. Further net margin improvement continues to be achieved.

• DAC Italy continues to grow with good penetration of the independent sector. Business and consumer confidence is holding up. D&D’s integration into DAC is ongoing. Procurement benefits in Italian product (sourced/ co-sourced from/ with DAC) continues to grow.

• Iberia comprises our businesses in Spain and Portugal. Overall performance in Spain is well below expectations. Improvements to the business platform through efficiencies in the infrastructure, a new ERP system and skilled people, are starting to show improvements however financial performance remains poor. Our business in Portugal goes from strength to strength. The bolt-on acquisition Igartza (July 2018), a multi-category distributor in northern Spain, is performing in line with expectations. Management remain positive about the growth opportunity in the Iberian market.

• Germany has underperformed however trading losses are narrowing. Work continues in building its business foundation including sales structures, IT platforms, human capital and infrastructure. Additional management, deployed to assist the local operators, is starting to make a difference. Germany still represents a very large foodservice opportunity.

• The Baltics, with a focus on Lithuania, is profitable. The new depot in Kaunas became operational in Q3. • Further expansion, both in terms of in-country bolt-on acquisitions and strategic entry into new geographies in Europe, remains possible, as we are not represented or underrepresented in many countries.

Emerging markets

• South Africa overall is showing improvement despite weak economic conditions. Bidfood and the Chipkins Puratos (CP) JV have achieved pleasing growth through good cost containment and improved margins. The aftermath of the listeriosis crisis in processed meats continues to impact the Crown Food Group (CFG) business however, from April, is largely in the comparative base. The food inflation trajectory is up which will start to assist Bidfood. The CP JV is investing in new product offerings with the benefit of the Puratos influence. The small ingredients distributor acquired by CFG in H1 F2019 is meeting expectations. Overall results in the month of April were much improved on the comparative month in F2018.

• Greater China’s year to date financial performance remains significantly below F2018 however month on month is starting to recover as expected. In mainland China, our geographic distribution network is reasonably complete. Dairy remains an important category however diversification of the product range continues. Operations are expected to commence at the new meat (value add processing) factory in Q4. Mainland China has reacted well in recovering from the effects of dairy market supply dislocation, accordant margin pressures and rising operating and logistics costs. Hong Kong’s cost inefficiencies remain due to duplicate warehousing, but these will rectify themselves from the beginning of Q4. Some further supplier dislocation in dairy is anticipated in Hong Kong in Q4 however management are well prepared to deal with the challenge. The working capital cycle remains under scrutiny. The focus on bolstering the overall management structures continues.

• Singapore continues to deliver steady growth as we develop our foodservice model. Good traction is being achieved in the core foodservice market with other areas such as exports, marine and commodities being scaled back significantly. Our investment into Malaysia is rolling out nationwide. Our small joint venture in Vietnam is progressing, albeit a little later than planned.

• Further expansion in Asia depends on finding the correct opportunities.

• In South America, our focus remains on building a strong platform in a region with significant growth potential. Brazil has delivered an improved organic performance. Recent political change has not yet manifested itself in higher economic growth, yet business confidence is up. Refinement of the business model continues to enable sales growth and expansion of their broadline product range. Further capex is being spent to cater for growth. Bolt-on opportunities are being pursued however vendor expectations remain unrealistic. Chile is performing well and has a true national presence off the back of the significant customer base and two additional depots which were acquired in October. Integration continues.

• In the Middle East, our businesses have rebounded strongly benefitting from improved geopolitical stability and the flow through effects of higher oil prices. The UAE is starting to show some improvement as tourism and hotel occupancies improve. A significant agency was won in Q3 which should assist going forward. Our Saudi operation has performed very well, buoyed by structural reforms which are translating in higher economic activity. All businesses are profitable other than the small Jordan operation.

• Turkey continues to improve as the local operations grow. Further bolt-on opportunities are being sought.

Acquisitive activity

• Bidcorp remains alert to all acquisition opportunities that present themselves both in current markets and in new territories.

• In the 3 months to March 2019, we made the following bolt-on acquisition costing (inclusive of acquisition costs) R291 million: o Bidfood UK acquired Punjab Kitchen, a niche ready meals business.

Discontinued operations

– UK Logistics activities:

• CD business o We are in advanced negotiations for the disposal of the CD business (Bestfood Logistics), to a reputable international buyer. At this stage we cannot provide any further details and will update the market in due course. We are reasonably confident at this stage of the sale progressing, but it is still subject to clearing several hurdles which are considered normal and usual for a transaction of this nature. We anticipate closure in Q1 F2020. o Trading performance in Bestfood Logistics continues to improve off the back of better service levels and a more sustainable revenue platform. The rest of the re-awarded KFC contract is being onboarded and will be complete by June.

• PCL o The exit of the highly unprofitable transport contracts were completed at the end of April. The residual fleet is in the process of being disposed of, which should be complete by June. The remaining warehousing activities are small and management are working on an exit plan for these. All costs of closure will be expensed by year-end.

• South Africa overall is showing improvement despite weak economic conditions. Bidfood and the Chipkins Puratos (CP) JV have achieved pleasing growth through good cost containment and improved margins. The aftermath of the listeriosis crisis in processed meats continues to impact the Crown Food Group (CFG) business however, from April, is largely in the comparative base. The food inflation trajectory is up which will start to assist Bidfood. The CP JV is investing in new product offerings with the benefit of the Puratos influence. The small ingredients distributor acquired by CFG in H1 F2019 is meeting expectations. Overall results in the month of April were much improved on the comparative month in F2018.

• Greater China’s year to date financial performance remains significantly below F2018 however month on month is starting to recover as expected. In mainland China, our geographic distribution network is reasonably complete. Dairy remains an important category however diversification of the product range continues. Operations are expected to commence at the new meat (value add processing) factory in Q4. Mainland China has reacted well in recovering from the effects of dairy market supply dislocation, accordant margin pressures and rising operating and logistics costs. Hong Kong’s cost inefficiencies remain due to duplicate warehousing, but these will rectify themselves from the beginning of Q4. Some further supplier dislocation in dairy is anticipated in Hong Kong in Q4 however management are well prepared to deal with the challenge. The working capital cycle remains under scrutiny. The focus on bolstering the overall management structures continues.

• Singapore continues to deliver steady growth as we develop our foodservice model. Good traction is being achieved in the core foodservice market with other areas such as exports, marine and commodities being scaled back significantly. Our investment into Malaysia is rolling out nationwide. Our small joint venture in Vietnam is progressing, albeit a little later than planned.

• Further expansion in Asia depends on finding the correct opportunities.

• In South America, our focus remains on building a strong platform in a region with significant growth potential. Brazil has delivered an improved organic performance. Recent political change has not yet manifested itself in higher economic growth, yet business confidence is up. Refinement of the business model continues to enable sales growth and expansion of their broadline product range. Further capex is being spent to cater for growth. Bolt-on opportunities are being pursued however vendor expectations remain unrealistic. Chile is performing well and has a true national presence off the back of the significant customer base and two additional depots which were acquired in October. Integration continues.

• In the Middle East, our businesses have rebounded strongly benefitting from improved geopolitical stability and the flow through effects of higher oil prices. The UAE is starting to show some improvement as tourism and hotel occupancies improve. A significant agency was won in Q3 which should assist going forward. Our Saudi operation has performed very well, buoyed by structural reforms which are translating in higher economic activity. All businesses are profitable other than the small Jordan operation.

• Turkey continues to improve as the local operations grow. Further bolt-on opportunities are being sought.

Acquisitive activity

• Bidcorp remains alert to all acquisition opportunities that present themselves both in current markets and in new territories.

• In the 3 months to March 2019, we made the following bolt-on acquisition costing (inclusive of acquisition costs) R291 million: o Bidfood UK acquired Punjab Kitchen, a niche ready meals business.

Discontinued operations

– UK Logistics activities:

• CD business o We are in advanced negotiations for the disposal of the CD business (Bestfood Logistics), to a reputable international buyer. At this stage we cannot provide any further details and will update the market in due course. We are reasonably confident at this stage of the sale progressing, but it is still subject to clearing several hurdles which are considered normal and usual for a transaction of this nature. We anticipate closure in Q1 F2020. o Trading performance in Bestfood Logistics continues to improve off the back of better service levels and a more sustainable revenue platform. The rest of the re-awarded KFC contract is being onboarded and will be complete by June.

• PCL o The exit of the highly unprofitable transport contracts were completed at the end of April. The residual fleet is in the process of being disposed of, which should be complete by June. The remaining warehousing activities are small and management are working on an exit plan for these. All costs of closure will be expensed by year-end.

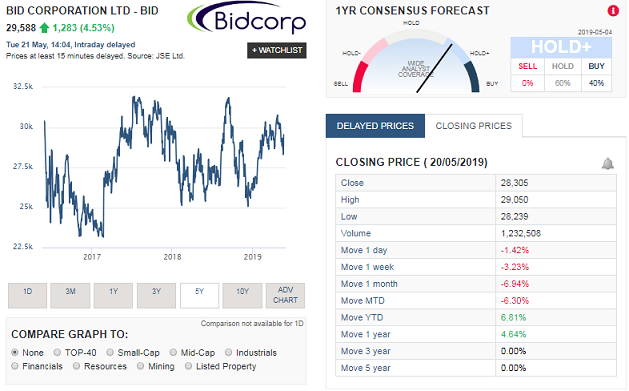

Bidcorp (BID) share price performance

The screenshot of Bidcorp share price performance taken from Sharenet below shows that BID has been moving gradually higher but has not exactly shot the lights out for their shareholders.

- Last Week: -3.23%

- Month to Date (MTD) : -6.3%

- Year to Date (YTD): 6.81%

- 1 year move: 4.64%

Bidcorp (BID) share valuation (as we valued the group on 20 February 2019)

So what are Bidcorp shares worth, based on their revenues, net profits, dividend yield and their cash generation capabilities and the markets and geographies they operate in? Based on Bidcorp's financial results, and their future prospects we value the company's shares at R303.81 (at the top end of our valuation model). So trading at R289 it is relatively close to our top en valuation is believe long term investors currently holding it should continue to do so, and those looking to get in should look to get in at a about 15% below our top end valuation of R303, so look to get in at around R270 levels if possible