|

Related Topics |

|

We take a look at the interim results for the period ending end of August 2018 of listed industrial firm Argent Industrial. Argent owns various well known brands such as Jetmaster braais and fire places, Xpanda security gates, Paint & ladders and Cedar paint as well as vehicle accesories supplier Excalibur to name but a few.

|

|

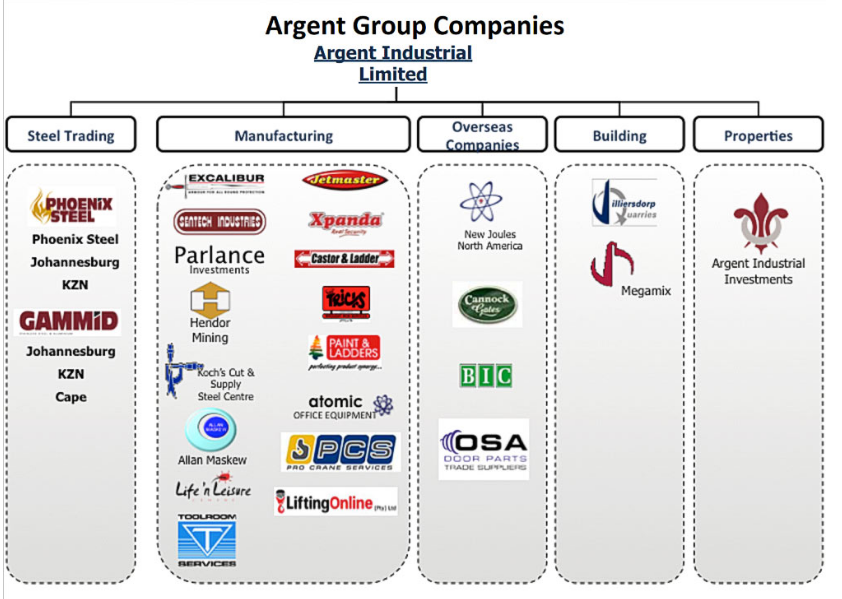

About Argent Industrial

Argent listed on the JSE in September 1999. The group has an annual turnover of close to R2billion. It has 24 companies that falls under the group and it has exposure to the USA and UK markets. Its main business divisions are:

- Steel trading

- Engineering

- Manufacturing

According to Argent's last annual report they define their corporate profile as follows.

"Argent Industrial Limited is largely a steel-based beneficiation group with a very diverse portfolio of businesses that include international brands. The business portfolio consists of Argent Industrial Engineering, Atomic Office Equipment, Allan Maskew, Castor and Ladder, Gammid Trading, Hendor Mining, Jetmaster, Koch’s Cut & Supply Steel Centre, Lifting Online, Megamix, Phoenix Steel, Pro Crane Services, Rifumo Concepts, Toolroom Services, Tricks Wrought Iron Services, Xpanda Security, Cannock Gates & Burbage Iron Craft, OSA Door Parts and New Joules North America. These businesses cover a huge spectrum of products and services from manufacturing and steel-based trading, to concrete building products, with regional outlets that trade in a number of these products. The company has 24 operating units which operate throughout South Africa, the United Kingdom and North America. Manufacturing is the biggest activity of the group and this, together with a strategy of vertical integration and being self-sufficient has led the group to being totally diversified. This protects the group from economic swings in any one segment of the market and is a catalyst for new growth opportunity. The group’s character is innovation, speed, delivery and service. Argent has a bold approach to business and is always seeking new investments and investors. Our customers are the key to our success, and benefit from our dedicated attention. The Argent group’s strategic intent is to grow profitability by streamlining the business and extracting maximum value from vertical integration and good management practice"

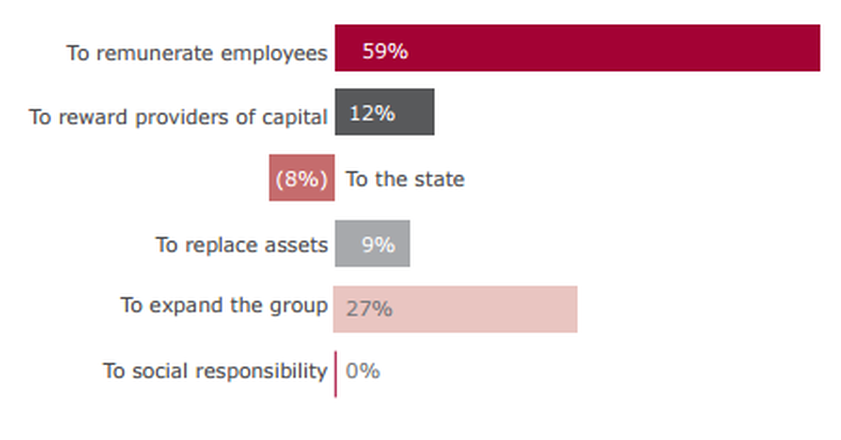

The image below shows how the "value added" by the group is spent.

"Argent Industrial Limited is largely a steel-based beneficiation group with a very diverse portfolio of businesses that include international brands. The business portfolio consists of Argent Industrial Engineering, Atomic Office Equipment, Allan Maskew, Castor and Ladder, Gammid Trading, Hendor Mining, Jetmaster, Koch’s Cut & Supply Steel Centre, Lifting Online, Megamix, Phoenix Steel, Pro Crane Services, Rifumo Concepts, Toolroom Services, Tricks Wrought Iron Services, Xpanda Security, Cannock Gates & Burbage Iron Craft, OSA Door Parts and New Joules North America. These businesses cover a huge spectrum of products and services from manufacturing and steel-based trading, to concrete building products, with regional outlets that trade in a number of these products. The company has 24 operating units which operate throughout South Africa, the United Kingdom and North America. Manufacturing is the biggest activity of the group and this, together with a strategy of vertical integration and being self-sufficient has led the group to being totally diversified. This protects the group from economic swings in any one segment of the market and is a catalyst for new growth opportunity. The group’s character is innovation, speed, delivery and service. Argent has a bold approach to business and is always seeking new investments and investors. Our customers are the key to our success, and benefit from our dedicated attention. The Argent group’s strategic intent is to grow profitability by streamlining the business and extracting maximum value from vertical integration and good management practice"

The image below shows how the "value added" by the group is spent.

Argent industrial's value added

The group’s key values are:

• Seeking long-term, sustained, real growth for shareholders;

• Maintaining a balance in the investment of its resources in focused markets;

• Conducting business with professionalism and integrity;

• Developing long-term relationships through co-operation and fair play;

• Practicing financial prudence;

• Meeting all legal and moral obligations;

• Generating eagerness to learn and improve;

• Respecting the dignity and human rights of all employees; and

• Maintaining a high standard in the areas of workplace safety and health.

• Seeking long-term, sustained, real growth for shareholders;

• Maintaining a balance in the investment of its resources in focused markets;

• Conducting business with professionalism and integrity;

• Developing long-term relationships through co-operation and fair play;

• Practicing financial prudence;

• Meeting all legal and moral obligations;

• Generating eagerness to learn and improve;

• Respecting the dignity and human rights of all employees; and

• Maintaining a high standard in the areas of workplace safety and health.

So to the numbers we go

Revenue R858 million (down 8.7% from R940 million a year ago)

Headline earnings per share: 50.4c (up 60% from 31.5c a share a year ago). Places the group on a forward PE of 3.5

Net Asset Value (NAV) per share: R11.97

Cash generated per share: R1.36 (or R113 million)

Gearing is reported at 3%, but the group has no cash and equivalents on the balance sheet. Basically they have to tap into their overdraft or borrow if they want to pay items now. Their trade and other payables increased from R204million a year ago to R223million. Question is whether ART is struggling to pay off its bills due to their tight cash position?

Headline earnings per share: 50.4c (up 60% from 31.5c a share a year ago). Places the group on a forward PE of 3.5

Net Asset Value (NAV) per share: R11.97

Cash generated per share: R1.36 (or R113 million)

Gearing is reported at 3%, but the group has no cash and equivalents on the balance sheet. Basically they have to tap into their overdraft or borrow if they want to pay items now. Their trade and other payables increased from R204million a year ago to R223million. Question is whether ART is struggling to pay off its bills due to their tight cash position?

So any comments from management on the results?

The following extracts were taken from their financial results as published earlier today.

Financial Overview

Argent Industrial Limited has had a successful six months despite a difficult South African economy. The group achieved its objectives in that it stabilised its local operations, grew its off-shore investments and continued with its share buy-back programme.

Operations Review

Manufacturing

The division relative to the South African economy performed well and has been enhanced by the group’s acquisition on 28 June 2018 of Fuel Proof Limited (“Fuel Proof”) and Roll-Tec Safety Limited (“Roll-Tec”), based in the United Kingdom. Fuel Proof is a manufacturer and trade supplier of mobile and static bunded fuel storage and dispensing systems. Roll-Tec is a specialist manufacturer of roll-over protection bars for construction machinery as well as being the rental agent for Fuel Proof, renting out its products into the European market. The purchase consideration was an amount of GBP 4 600 000. This is based on a maintainable before tax income of GBP 960 000 per annum. In terms of the transaction agreement, the purchase consideration will be recalculated twenty-four months after the effective date in that it will either reduce to a minimum of GBP 4 080 000 or increase to a maximum of the GBP 6 000 000. The group has entered into a sale agreement for the sale of Parlance Investments and the property situated at 107 Kotzenberg Street, Rosslyn, Pretoria for an amount of R 2 million for the powder coating business and R 7 million for the property. The transaction has a number of conditions / hurdles, which allows the buyer to either withdraw or close the deal by 31 March 2019.

Financial Overview

Argent Industrial Limited has had a successful six months despite a difficult South African economy. The group achieved its objectives in that it stabilised its local operations, grew its off-shore investments and continued with its share buy-back programme.

Operations Review

Manufacturing

The division relative to the South African economy performed well and has been enhanced by the group’s acquisition on 28 June 2018 of Fuel Proof Limited (“Fuel Proof”) and Roll-Tec Safety Limited (“Roll-Tec”), based in the United Kingdom. Fuel Proof is a manufacturer and trade supplier of mobile and static bunded fuel storage and dispensing systems. Roll-Tec is a specialist manufacturer of roll-over protection bars for construction machinery as well as being the rental agent for Fuel Proof, renting out its products into the European market. The purchase consideration was an amount of GBP 4 600 000. This is based on a maintainable before tax income of GBP 960 000 per annum. In terms of the transaction agreement, the purchase consideration will be recalculated twenty-four months after the effective date in that it will either reduce to a minimum of GBP 4 080 000 or increase to a maximum of the GBP 6 000 000. The group has entered into a sale agreement for the sale of Parlance Investments and the property situated at 107 Kotzenberg Street, Rosslyn, Pretoria for an amount of R 2 million for the powder coating business and R 7 million for the property. The transaction has a number of conditions / hurdles, which allows the buyer to either withdraw or close the deal by 31 March 2019.

Steel Trading

The groups two mild steel operations showed an improved R 7.9 million before tax. The two aluminium and stainless-steel operations were just above break even. Both divisions have showed signs of improvement in October and November 2018. This is definitely an area that the group can improve on.

Share buy-back programme

Argent repurchased and cancelled 424 608 shares in the period under review and will be repurchasing an additional R34 million worth of shares over the next 3 months.

Outlook

The outlook remains positive. The group anticipates that even though consumers are pressured, there is emerging confidence. Argent is also encouraged by recent political changes in South Africa and believes that the country is on the cusp of a much-needed confidence boost. The year has started off in a much more positive vein with consumer and business confidence increasing. There are signs of improvement in certain sectors in which we operate and particularly mining and manufacturing are benefiting from strengthening commodity prices. Our businesses are sized optimally for current market conditions, both locally and internationally and will now focus on balancing its returns on investment, share price and net asset value in order to achieve shareholder value and returns

The groups two mild steel operations showed an improved R 7.9 million before tax. The two aluminium and stainless-steel operations were just above break even. Both divisions have showed signs of improvement in October and November 2018. This is definitely an area that the group can improve on.

Share buy-back programme

Argent repurchased and cancelled 424 608 shares in the period under review and will be repurchasing an additional R34 million worth of shares over the next 3 months.

Outlook

The outlook remains positive. The group anticipates that even though consumers are pressured, there is emerging confidence. Argent is also encouraged by recent political changes in South Africa and believes that the country is on the cusp of a much-needed confidence boost. The year has started off in a much more positive vein with consumer and business confidence increasing. There are signs of improvement in certain sectors in which we operate and particularly mining and manufacturing are benefiting from strengthening commodity prices. Our businesses are sized optimally for current market conditions, both locally and internationally and will now focus on balancing its returns on investment, share price and net asset value in order to achieve shareholder value and returns

So should you buy their shares?

While Argent is trading at a very low PE ratio one has to wonder why you would buy back 400 000 shares during the period under the review, yet according to the balance sheet they have no cash and equivalents on the books. It sends a very confusing message. You dont have cash in the bank, but you buying back shares? What is more important, keeping float in the business bank accounts to pay the bills, or to buy back your own shares? Further to that the group promises to buy back an addition R34 million worth of shares in the next 3 year. Well at R3.60 a share they would be able to buy back a further 9.44 million shares, which will leave them with just 73.6 million shares in issue. Assuming nothing else in the business changes and their earnings remains the same, their earnings per share and net asset value per share would increase purely based on the fact that earnings and assets are now divided between fewer shares. While this is great for unlocking value for current investors we have to question if that money could not be better spent expanding the group via a few small acquisitions?

They have never shot the lights out in terms of share price performance, or earnings that blew investors away or dividends that filled investors pockets. And while their aggressive share buy backs might help improve the fortunes of their shares and its long term performance, we are worried about their cash flow management and the fact that during difficult economic times they are buying back shares instead of looking to acquire businesses who might be offering value due to the struggling economic environment.

We would recommend owning a few Argent shares, as it covers a wide variety of sectors and they have a good product mix and footprint in South Africa, but no more than 1% of a investors portfolio should be invested into Argent.

They have never shot the lights out in terms of share price performance, or earnings that blew investors away or dividends that filled investors pockets. And while their aggressive share buy backs might help improve the fortunes of their shares and its long term performance, we are worried about their cash flow management and the fact that during difficult economic times they are buying back shares instead of looking to acquire businesses who might be offering value due to the struggling economic environment.

We would recommend owning a few Argent shares, as it covers a wide variety of sectors and they have a good product mix and footprint in South Africa, but no more than 1% of a investors portfolio should be invested into Argent.