|

|

Related Topics |

About Woolworths

The first Woolworths store opened its doors to the public in Cape Town in October 1931. And it was founder Max Sonnenberg who captured the public’s imagination with dynamic store policies that set Woolworths apart from its competitors. Three years later, a second branch opened in Durban, with another two in Port Elizabeth and Johannesburg a year later. And since then we’ve been building on our reputation for superior quality, exciting innovation and excellent value.

At Woolworths we take our business values seriously. They aren’t just words in an annual report - they are the foundation of our business. They give us direction and guide our behaviour, actions and choices. In fact, our values are so important to us that we’re measured not only on our performance, but also by how well we live up to them.

- FIRST TO OFFER EMPLOYEE BENEFITSKeen to attract and retain the best retail professionals, Woolworths was among the first local retailers to offer employees a pension fund, medical aid and maternity leave.

- FIRST IN ADVANCING TECHNot just a forward thinking employer, Woolworths was also an early adopter of technology. A lease agreement for the first computer was agreed to with National Cash Registers (NCR) in the late 60s and Woolworths was already using a computerised merchandising system by the early 1970s.

- FIRST TO INTRODUCE SELL BY DATESThis dynamic thinking extends to Woolworths product offering. In 1974, Woolworths became the first South African retailer to introduce ‘sell by’ dates on food packaging. Convenience, too, has long been a watchword at Woolworths - we were the first South African retailer to offer pre-washed lettuce and machine-washable wool clothing to consumers.

- OUR GOOD BUSINESS JOURNEYIn April 2007, we launched our Good Business Journey – a bold plan to make a difference in eight key areas on our journey towards sustainability: Energy, Water, Waste, Sustainable Farming, Ethical Sourcing, Transformation, Social Development and Health and Wellness. Read more about our Good Business Journey

At Woolworths we take our business values seriously. They aren’t just words in an annual report - they are the foundation of our business. They give us direction and guide our behaviour, actions and choices. In fact, our values are so important to us that we’re measured not only on our performance, but also by how well we live up to them.

- QUALITY AND STYLE - DELIVER THE BESTIt means giving 100%, 100% of the time. Whether it’s making sure that a supplier is delivering to the standards we set or preparing a report, it all boils down to one thing: there’s no compromising on quality, because ‘good enough’ just isn’t good enough.

- VALUE - A SIMPLE AND FAIR DEALOffering real value goes beyond offering our customers quality at a good price: it also means offering value to each other, from sharing our knowledge with colleagues and suppliers to being able to evaluate how the decisions we make affect the business.

- SERVICE - WE ALWAYS THINK CUSTOMERAt Woolies, we know that we have to go that bit further to really make a difference. Putting the customer first is what service is all about. Whether your customer is a shopper in our stores or the store manager who needs a vital delivery, service is about understanding others’ needs, being willing to do more than is expected, and being a good ambassador for the Woolies brand.

- INNOVATION - DISCOVER THE DIFFERENCEWe do it for our customers. We love discovering new ideas, new products and new processes. We enjoy thinking ‘out of the box’ and finding solutions that benefit the business.

- INTEGRITY - DOING WHAT YOU SAY YOU WILL DOKeeping our promises is important to us, whether it’s maintaining confidentiality, not accepting gifts from suppliers, or simply listening to what others have to say with an open mind. By being true to ourselves, we earn the trust of our colleagues and our customers.

- ENERGY - BE PASSIONATE AND DELIVERWhen you’re passionate about what you do, when you really care, your enthusiasm and belief rub off on others. At Woolies, you’re part of a 23 000-member team. Being part of a team means being an inspiration to others and being inspired by their successes and triumphs.

- SUSTAINABILITY - BUILD FOR A BETTER FUTUREWhile you may be familiar with some of our environmental and conservation projects, for us in a South African, and African, context, sustainability isn’t just about being ‘green’. It’s about sharing expertise, helping local enterprises to grow, and contributing to a prosperous, secure future for our country. Please see more about our Good Business Journey.

Woolworths East London 1948

Trading Statement

The following was published on the JSE Security Exchange News Syteme (SENS) system earlier today

SENS START

TRADING STATEMENT: 53 WEEKS ENDED 30 JUNE 2019

Shareholders are advised that earnings per share ('EPS'), headline earnings per share ('HEPS') and adjusted diluted HEPS for the 53 weeks ended 30 June 2019 are expected to be within the ranges reflected in the table below:

June 2018 June 2019 (expected increase/decrease) in % June 2019

EPS (cents) - 369.5 65.0% to 75.0% -92.4 to -129.3

HEPS (cents) 346.3 -3.5% to 1.5% 334.2 to 351.5

Adjusted diluted HEPS (cents) 364.1 -2.5% to 2.5% 355.0 to 373.2

EPS reflects a further impairment of the David Jones business. An impairment charge of A$437.4 million (net of deferred tax) will be recognised at the period end 30 June 2019, reducing the valuation of David Jones to approximately A$965 million.

A strategic review of the David Jones store portfolio has also identified stores with onerous leases resulting in an additional provision of A$22.4 million at period end. The impairment reflects the economic headwinds and the accelerating structural changes affecting the Australian retail sector as well as the performance of the business, which has fallen short of expectations.

The WHL Board believes that the valuation of David Jones is realistic and reflective of its prospects. EPS, HEPS and adjusted diluted HEPS for the pro forma 52 weeks ended 23 June 2019 are expected to be within the ranges reflected in the table below:

June 2018 June 2019 (expected increase/decrease) in % June 2019

EPS (cents) -369.5 60.0% to 70.0% -110.8 to -147.8

HEPS (cents) 346.3 -7.5% to -2.5% 320.3 to 337.6

Adjusted diluted HEPS (cents) 364.1 -5.0% to 0% 345.9 to 364.1

The Group manages its retail operations on a 52-week basis and, as a result, a 53rd week is required approximately every six years for realignment. The current year has 53 weeks. To facilitate comparison against the 52-week prior year, financial information for the current year has been presented on a 52 week basis, constituting pro forma information in terms of the JSE Limited ('JSE') Listings Requirements.

The pro forma information, which is the responsibility of the Group's directors, has been prepared for illustrative purposes only, and may not fairly present the Group's financial position, changes in equity, cash flows or results of operations. The information contained in this announcement, including the estimated financial information and pro forma financial information, has not been reviewed or reported on by the Group's external auditors. The Group's year-end results for the 53-week period ended 30 June 2019 are scheduled to be announced on the SENS on or about 29 August 2019.

Contact: Reeza Isaacs (Group Finance Director) on 021 407 2464 Ralph Buddle (Director: Strategy and Business Development) on 021 407 3250 [email protected]

Cape Town 1 August 2019

SENS ENDS

SENS START

TRADING STATEMENT: 53 WEEKS ENDED 30 JUNE 2019

Shareholders are advised that earnings per share ('EPS'), headline earnings per share ('HEPS') and adjusted diluted HEPS for the 53 weeks ended 30 June 2019 are expected to be within the ranges reflected in the table below:

June 2018 June 2019 (expected increase/decrease) in % June 2019

EPS (cents) - 369.5 65.0% to 75.0% -92.4 to -129.3

HEPS (cents) 346.3 -3.5% to 1.5% 334.2 to 351.5

Adjusted diluted HEPS (cents) 364.1 -2.5% to 2.5% 355.0 to 373.2

EPS reflects a further impairment of the David Jones business. An impairment charge of A$437.4 million (net of deferred tax) will be recognised at the period end 30 June 2019, reducing the valuation of David Jones to approximately A$965 million.

A strategic review of the David Jones store portfolio has also identified stores with onerous leases resulting in an additional provision of A$22.4 million at period end. The impairment reflects the economic headwinds and the accelerating structural changes affecting the Australian retail sector as well as the performance of the business, which has fallen short of expectations.

The WHL Board believes that the valuation of David Jones is realistic and reflective of its prospects. EPS, HEPS and adjusted diluted HEPS for the pro forma 52 weeks ended 23 June 2019 are expected to be within the ranges reflected in the table below:

June 2018 June 2019 (expected increase/decrease) in % June 2019

EPS (cents) -369.5 60.0% to 70.0% -110.8 to -147.8

HEPS (cents) 346.3 -7.5% to -2.5% 320.3 to 337.6

Adjusted diluted HEPS (cents) 364.1 -5.0% to 0% 345.9 to 364.1

The Group manages its retail operations on a 52-week basis and, as a result, a 53rd week is required approximately every six years for realignment. The current year has 53 weeks. To facilitate comparison against the 52-week prior year, financial information for the current year has been presented on a 52 week basis, constituting pro forma information in terms of the JSE Limited ('JSE') Listings Requirements.

The pro forma information, which is the responsibility of the Group's directors, has been prepared for illustrative purposes only, and may not fairly present the Group's financial position, changes in equity, cash flows or results of operations. The information contained in this announcement, including the estimated financial information and pro forma financial information, has not been reviewed or reported on by the Group's external auditors. The Group's year-end results for the 53-week period ended 30 June 2019 are scheduled to be announced on the SENS on or about 29 August 2019.

Contact: Reeza Isaacs (Group Finance Director) on 021 407 2464 Ralph Buddle (Director: Strategy and Business Development) on 021 407 3250 [email protected]

Cape Town 1 August 2019

SENS ENDS

So the number we are interested in is the bolded and blue coloured line above. Basically the group's profit for the year is expected to be down by between -5% and 0%. With WHL continuing to struggle in Australia, and continuing to write off more and more of their very expensive investment in Australia. Basically they will make a profit of R3.45 a share (which places the group on a PE ratio of 15.6 which is pretty much middle of the road. Not the cheapest stock around but certainly not the most expensive stock listed on the JSE right now.

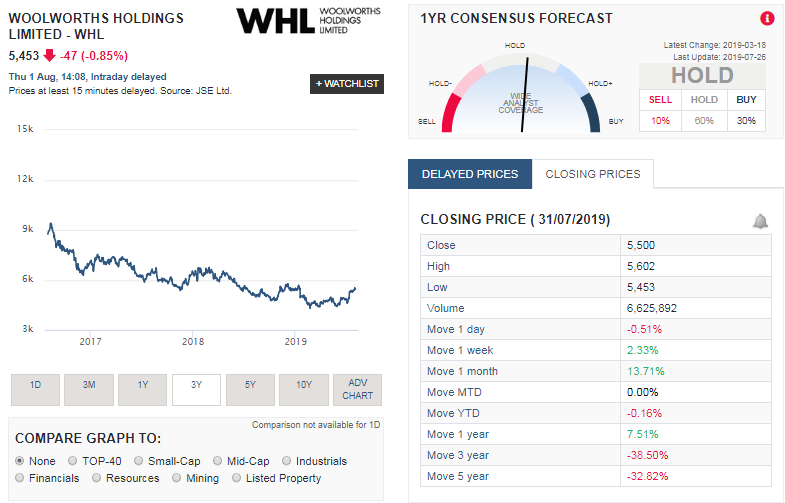

Woolworths (WHL) share price performance over last 3 years

The image below, taken from Sharenet shows Woolworths share price performance over the last 3 years. And it is clear its been a tough old time for Woolworths shareholders with the shares long term trend being a significant downward slope. (But it should be noted the share price is up roughly 9% since their first trading statement for this financial period which was brought out on 11 July 2019)

The summary below shows the share price returns of Woolworths over various time periods:

- 1 week: 2.33%

- 1 month: 13.71%

- Year to date (YTD): -0.16%

- 1 year: 7.51%

- 3 years: -38.5%

- 5 years: -32.8%

Woolworths (WHL) share valuation (as at February 2019)

So what are Woolies shares worth, based on their revenues, net profits, dividend yield and their cash generation capabilities and the markets and geographies they operate in? The image and financial results above just shows that Woolworths has offered investors very little to cheer about in recent years, and to be perfectly honest the results as released today hardly gives investors anything to cheer about either. Declared interim dividend has declined, operating profit has declined, headline earnings per share has declined, their cash on balance sheet is not as much as we would like to see it.

But it is not all bad news. Woolies Foods still charging along nicely. And the changes made at David Jones is bound to pay off for the group going forward. But we wont be surprised if the markets remain a little weary of Woolworths right now, as the retail industry in South Africa is definitely out of favour with the markets right now.

Based on all the above we value WHL shares at R52.78 a share. So it is offering investors a bit of value based on its current share price but investors should not expect it to shoot the lights out anytime soon as the retail industry in SA is struggling at this point in time and WHL's financials and its share price reflects this.

But it is not all bad news. Woolies Foods still charging along nicely. And the changes made at David Jones is bound to pay off for the group going forward. But we wont be surprised if the markets remain a little weary of Woolworths right now, as the retail industry in South Africa is definitely out of favour with the markets right now.

Based on all the above we value WHL shares at R52.78 a share. So it is offering investors a bit of value based on its current share price but investors should not expect it to shoot the lights out anytime soon as the retail industry in SA is struggling at this point in time and WHL's financials and its share price reflects this.