|

Related Topics |

|

We take a look at the latest trade and development report for 2019 from UNCTAD that covers a wide range of issues facing global economic growth and development

|

|

Financing a global green new deal

From this point onward the content is as obtained from the United Nations Conference on Trade and Development (UNCTAD) unless specified otherwise.

Foreword

The deep and widespread economic and social damage caused by the global financial crisis has been followed, in most advanced economies, by a decade of austerity, sluggish productivity growth and stagnant real wages. Growth has also slowed in most developing countries, albeit with considerable variation across regions. The struggle to create good jobs has intensified, with rapid urbanization, premature deindustrialization and rural stagnation accompanying rising inequality and growing political tensions.

Everywhere, anxiety over the prospect of increasing economic insecurity is compounded by the impending threat of environmental breakdown. The Intergovernmental Panel on Climate Change has recently raised the stakes by starting the clock on a climate meltdown; but a shortening time horizon is just part of a growing recognition of a wider and deeper ecological crisis.

Efforts to address these challenges have aligned around a series of goals and targets, which the international community agreed in 2015, to ensure an inclusive and sustainable future for all people and the planet. But with little more than a decade left to achieve Agenda 2030, meeting these goals has already fallen behind schedule and there is broad agreement that what is now required is a coordinated investment push on an unprecedented scale and across the entire global commons. The financing numbers are daunting, from “billons to trillions”, requiring an additional 2.5 trillion dollars a year, just in developing countries, on UNCTAD estimates.

A decade ago at the G20 gathering in London, the world’s major economies came together to stem the global financial panic triggered by the collapse of the sub-prime mortgage market in the United States and to establish a more stable growth path going forward. Their talk of a fresh start was an acknowledgement that the existing multilateral system had failed to provide both the resources and the coordination needed to underpin stable markets and a healthy investment climate.

A decade on, that effort has stalled, leaving those tasked with meeting the SDGs wondering whether the multilateral system is fit for purpose. Their concern is compounded by the deteriorating state of the global economy. Increased disagreements over trade rules, currency movements and technology flows are fostering uncertainty and instability, draining trust from the multilateral system at the very moment consensus and coordination are key to scaling up the resources needed to meet the massive economic, social and environmental challenges we all face.

This year’s Trade and Development Report suggests that meeting the financing demands of the Agenda 2030 requires rebuilding multilateralism around the idea of a Global Green New Deal, and pursuing a financial future very different from the recent past. The place to begin building such a future is with a serious discussion of public financing options, as part of a wider process of repairing the social contract on which inclusive and sustainable outcomes can emerge and from which private finance can be engaged on more socially productive terms

Foreword

The deep and widespread economic and social damage caused by the global financial crisis has been followed, in most advanced economies, by a decade of austerity, sluggish productivity growth and stagnant real wages. Growth has also slowed in most developing countries, albeit with considerable variation across regions. The struggle to create good jobs has intensified, with rapid urbanization, premature deindustrialization and rural stagnation accompanying rising inequality and growing political tensions.

Everywhere, anxiety over the prospect of increasing economic insecurity is compounded by the impending threat of environmental breakdown. The Intergovernmental Panel on Climate Change has recently raised the stakes by starting the clock on a climate meltdown; but a shortening time horizon is just part of a growing recognition of a wider and deeper ecological crisis.

Efforts to address these challenges have aligned around a series of goals and targets, which the international community agreed in 2015, to ensure an inclusive and sustainable future for all people and the planet. But with little more than a decade left to achieve Agenda 2030, meeting these goals has already fallen behind schedule and there is broad agreement that what is now required is a coordinated investment push on an unprecedented scale and across the entire global commons. The financing numbers are daunting, from “billons to trillions”, requiring an additional 2.5 trillion dollars a year, just in developing countries, on UNCTAD estimates.

A decade ago at the G20 gathering in London, the world’s major economies came together to stem the global financial panic triggered by the collapse of the sub-prime mortgage market in the United States and to establish a more stable growth path going forward. Their talk of a fresh start was an acknowledgement that the existing multilateral system had failed to provide both the resources and the coordination needed to underpin stable markets and a healthy investment climate.

A decade on, that effort has stalled, leaving those tasked with meeting the SDGs wondering whether the multilateral system is fit for purpose. Their concern is compounded by the deteriorating state of the global economy. Increased disagreements over trade rules, currency movements and technology flows are fostering uncertainty and instability, draining trust from the multilateral system at the very moment consensus and coordination are key to scaling up the resources needed to meet the massive economic, social and environmental challenges we all face.

This year’s Trade and Development Report suggests that meeting the financing demands of the Agenda 2030 requires rebuilding multilateralism around the idea of a Global Green New Deal, and pursuing a financial future very different from the recent past. The place to begin building such a future is with a serious discussion of public financing options, as part of a wider process of repairing the social contract on which inclusive and sustainable outcomes can emerge and from which private finance can be engaged on more socially productive terms

Advertisement

Good times, bad times

Prospects for the global economy are currently shrouded in a fog of international trade tensions and geopolitical disputes. But, the bigger story a decade after the G20 stepped in to contain panic in markets and salvage a battered financial system, is that growth has failed to find a firm footing. The United States is in its longest recovery on record but it is also one of the weakest, and the impact on incomes has been subdued. The pick-up since the 2017 tax cut is fading, with little sign of the promised investment boom. Elsewhere in the developed world, the pick-up has been even more short-lived. The eurozone is slipping back towards stagnation, with the German economy showing clear signs of fatigue; and while Brexit is an unwanted distraction for the entire European economy, the United Kingdom looks set for a particularly traumatizing 2019. There is a good deal of speculation that recessionary winds will blow the advanced economies, and with them the global economy, off course in 2020. Monetary normalization has already been put on hold by leading central banks but there are growing concerns that even another round of quantitative easing will fail to provide the needed boost to overall demand. Whether or not pushing down on the monetary accelerator would again help emerging economies is also an open question. The slowdown this year, 2019, is apparent across all developing regions, with Latin America particularly hard hit. Talk of “decoupling” and “convergence” which briefly united the chattering and investor classes after the global financial crisis (GFC), as developing (including so-called emerging) economies bounced back quickly, has gone quiet. The BRICS economies, which as a group saw average annual growth over 10 per cent immediately after the GFC, grew at 6.3 per cent last year.

With debt levels higher than ever across the developing world, totalling around $67 trillion, keeping interest rates on hold would ease servicing pressures. But financial markets are fickle and under the wrong circumstances can turn feral; against a backdrop of rising uncertainty and investor anxiety, a flight from emerging markets to the relative safety of the United States could still trigger a self-reinforcing deflationary spiral. Not surprisingly, policymakers everywhere are scanning the horizon for possible shocks. Heightened trade tensions are one likely source of increased friction. Trade has stalled with the weakening of global demand; growth in the first quarter of 2019 relative to the corresponding quarter of 2018 is estimated at just 0.4 per cent. Unilateral tariff increases by the United States, which began in early 2018 on specific products and have subsequently been extended on a broader range of imports from China, have not helped. Retaliation has followed in a number of countries. While the impact to date has been contained, a resumption of tit-for-tat tariff increases could prove very costly if combined with a further slowdown in investment. There are other dangerous currents beneath these already troubled economic waters. There is a growing awareness that the dispute between the United States and China is less about tariffs and more about the technological ambitions of a middle-income developing country. Accessing foreign technology helped today’s advanced economies climb the development ladder and efforts to kick that ladder away by further reducing their policy space will face resistance from developing countries. This could add to the already diminished levels of trust in the multilateral system, with further damage to global economic prospects. Currency movements are adding to the sense of economic anxiety. These have become much more volatile in the era of hyperglobalization with the financialization of currency markets. The Morgan Stanley Emerging Market Currency Index rose significantly at the beginning of 2019 but fell sharply between mid-April and late May, only to climb again thereafter. Three factors are behind this volatility: sharp fluctuations in crisishit countries such as Argentina and Turkey; the volatility of capital flows to emerging markets resulting from policy uncertainty in the developed countries and weaker growth prospects in emerging markets; and more generalized pressure from the United States Administration to keep the dollar “competitive”. In an international financial system still heavily dependent on a predictable role for the dollar, turning that role – long recognized as an “exorbitant privilege” – into a source of economic ordnance could bring more destabilizing consequences. An immediate worry for many developing countries is that any sharp loss of confidence in their own currency coming after a rapid increase in external debt could expose them to much deeper deflationary pressures, as has already occurred in Argentina and Turkey. Commodity markets have been on a rollercoaster ride since the financial crisis; these are now in a softer phase, with prices well below post-crisis highs. While depressed demand underlies the absence of price buoyancy in many commodity markets in recent months, medium-term volatility has been influenced by the wide fluctuations in oil prices, by the financialization of commodity markets and by the concentration of market power in a small number of international trading companies. The UNCTAD commodity price index fell from 134 in October 2018 to 112 in December that year, and since then has risen to reach a level in the neighbourhood of 120. Fuel prices drove the fall in the index in the last quarter of 2018, with the index of fuel prices falling from 149 in October to 115 in December. The subsequent recovery has been partially on account of higher oil prices affected by sanctions on Iran and partially because of mild buoyancy in the prices of minerals, ores and metals. A spluttering North, a general slowdown in the South and rising levels of debt everywhere are hanging ominously over the global economy; these, combined with increased market volatility, a fractured multilateral system and mounting uncertainty, are framing the immediate policy challenge. The macroeconomic policy stance adopted to date has been lopsided and insufficiently coordinated to give a sustained boost to aggregate demand, with adjustments left to the vagaries of the market through a mixture of cost-cutting and liberalization measures. Ephemeral growth spurts and financial volatility have been the predictable results. But there are deeper challenges ahead that are truly daunting for people and the planet

Sign o' the times

Financial insecurity, economic polarization and environmental degradation have become hallmarks of the hyperglobalization era. These are, moreover, closely interconnected and mutually reinforcing, in ways that can give rise to vicious cycles of economic, social and environmental breakdown. This threat coincides with a worrying erosion of political trust, as income gaps have widened across all countries and the policy agenda perceived as catering to the interests of the winners from hyperglobalization, with scant attention paid to those who have seen limited gains or have fallen further behind. Even after the GFC, the rules of the game that had generated high levels of inequality, insecurity and indebtedness prior to that crisis have remained largely intact, adding further layers of resentment, often aimed against outsiders, and widening political divisions. This breakdown in trust has occurred at the very moment the collective actions needed to build a better future for all depend on a greater sense of shared responsibility and solidarity. The SDGs, agreed at the United Nations in 2015, were designed as a guide to that future. But with their delivery – planned for 2030 –already behind schedule, frustration is growing across different policy communities and at all levels of development. The perceived problem is a shortage of finance to achieve the scaling-up of investments on which the 2030 Agenda ultimately depends. With government finances burdened by increased debt levels and a fractured politics impeding long-term planning, pushing the financial envelope from billions to trillions of dollars each year will, it is claimed, have to rely on tapping the resources of high-wealth individuals and private financial institutions. At first glance the signs are encouraging. Global corporations are sitting on an estimated $2 trillion cash pile, while high net worth individuals have access to more than $60 trillion in assets. The OECD estimates that institutional investors in member countries hold global assets of US$92.6 trillion and while figures for institutional investors in developing countries are harder to come by, estimates for the assets held by Brazilian pension funds exceed $220 billion and some $350 billion for combined African pension funds. Redirecting a relatively small portion of these resources to meet the SDGs should, the argument goes, be able to solve the financing challenge facing the 2030 Agenda. A string of measures, marshalled under the call to “blend” and “maximize” finance, have been proposed that would channel public money into “de-risking” big investment projects while employing securitization and hedging techniques to bring in the private investors. If only things were that simple; the evidence suggests that blended finance fails to mitigate risk and instead boomerangs back to the public purse and the tax payer. In fact, vast amounts of public resources have already been used to save banks (and other financial institutions) that proved too big to fail after employing these same techniques to indulge a frenzy of speculative activity in the run-up to the financial crisis. Moreover, underpinning the vast trove of private assets is a tangled web of financial funds and debt instruments. Channelling a portion of these assets into long-term productive investment, whether in the public or private sectors, is not a matter of appealing to the better nature of those managing such funds nor establishing a more welcoming environment in which they can do business. In reality, too many governments, at all levels, have for decades been extending incentives and protections to international finance in the hope of boosting capital formation. Instead, they have been sucked in to an unstable financial world geared to short-term trading in existing assets, prone to boom and bust cycles, with baleful distributional outcomes and large debt overhangs that act as a persistent drag on the real economy. Re-engineering financial stocks and flows to support productive investments (whether private or public) will not happen without a fundamental change in the rules of the game. The current global economic environment – where austerity is the macroeconomic default option, liberalization the favoured policy tool for affecting structural change and debt the main engine of growth – is heading in the wrong direction when it comes to delivering on the ambition of the 2030 Agenda. Accordingly, this year’s Report seeks to make an alternative case for delivering the 2030 Agenda through a Global Green New Deal with a leading role for the public sector

Prospects for the global economy are currently shrouded in a fog of international trade tensions and geopolitical disputes. But, the bigger story a decade after the G20 stepped in to contain panic in markets and salvage a battered financial system, is that growth has failed to find a firm footing. The United States is in its longest recovery on record but it is also one of the weakest, and the impact on incomes has been subdued. The pick-up since the 2017 tax cut is fading, with little sign of the promised investment boom. Elsewhere in the developed world, the pick-up has been even more short-lived. The eurozone is slipping back towards stagnation, with the German economy showing clear signs of fatigue; and while Brexit is an unwanted distraction for the entire European economy, the United Kingdom looks set for a particularly traumatizing 2019. There is a good deal of speculation that recessionary winds will blow the advanced economies, and with them the global economy, off course in 2020. Monetary normalization has already been put on hold by leading central banks but there are growing concerns that even another round of quantitative easing will fail to provide the needed boost to overall demand. Whether or not pushing down on the monetary accelerator would again help emerging economies is also an open question. The slowdown this year, 2019, is apparent across all developing regions, with Latin America particularly hard hit. Talk of “decoupling” and “convergence” which briefly united the chattering and investor classes after the global financial crisis (GFC), as developing (including so-called emerging) economies bounced back quickly, has gone quiet. The BRICS economies, which as a group saw average annual growth over 10 per cent immediately after the GFC, grew at 6.3 per cent last year.

With debt levels higher than ever across the developing world, totalling around $67 trillion, keeping interest rates on hold would ease servicing pressures. But financial markets are fickle and under the wrong circumstances can turn feral; against a backdrop of rising uncertainty and investor anxiety, a flight from emerging markets to the relative safety of the United States could still trigger a self-reinforcing deflationary spiral. Not surprisingly, policymakers everywhere are scanning the horizon for possible shocks. Heightened trade tensions are one likely source of increased friction. Trade has stalled with the weakening of global demand; growth in the first quarter of 2019 relative to the corresponding quarter of 2018 is estimated at just 0.4 per cent. Unilateral tariff increases by the United States, which began in early 2018 on specific products and have subsequently been extended on a broader range of imports from China, have not helped. Retaliation has followed in a number of countries. While the impact to date has been contained, a resumption of tit-for-tat tariff increases could prove very costly if combined with a further slowdown in investment. There are other dangerous currents beneath these already troubled economic waters. There is a growing awareness that the dispute between the United States and China is less about tariffs and more about the technological ambitions of a middle-income developing country. Accessing foreign technology helped today’s advanced economies climb the development ladder and efforts to kick that ladder away by further reducing their policy space will face resistance from developing countries. This could add to the already diminished levels of trust in the multilateral system, with further damage to global economic prospects. Currency movements are adding to the sense of economic anxiety. These have become much more volatile in the era of hyperglobalization with the financialization of currency markets. The Morgan Stanley Emerging Market Currency Index rose significantly at the beginning of 2019 but fell sharply between mid-April and late May, only to climb again thereafter. Three factors are behind this volatility: sharp fluctuations in crisishit countries such as Argentina and Turkey; the volatility of capital flows to emerging markets resulting from policy uncertainty in the developed countries and weaker growth prospects in emerging markets; and more generalized pressure from the United States Administration to keep the dollar “competitive”. In an international financial system still heavily dependent on a predictable role for the dollar, turning that role – long recognized as an “exorbitant privilege” – into a source of economic ordnance could bring more destabilizing consequences. An immediate worry for many developing countries is that any sharp loss of confidence in their own currency coming after a rapid increase in external debt could expose them to much deeper deflationary pressures, as has already occurred in Argentina and Turkey. Commodity markets have been on a rollercoaster ride since the financial crisis; these are now in a softer phase, with prices well below post-crisis highs. While depressed demand underlies the absence of price buoyancy in many commodity markets in recent months, medium-term volatility has been influenced by the wide fluctuations in oil prices, by the financialization of commodity markets and by the concentration of market power in a small number of international trading companies. The UNCTAD commodity price index fell from 134 in October 2018 to 112 in December that year, and since then has risen to reach a level in the neighbourhood of 120. Fuel prices drove the fall in the index in the last quarter of 2018, with the index of fuel prices falling from 149 in October to 115 in December. The subsequent recovery has been partially on account of higher oil prices affected by sanctions on Iran and partially because of mild buoyancy in the prices of minerals, ores and metals. A spluttering North, a general slowdown in the South and rising levels of debt everywhere are hanging ominously over the global economy; these, combined with increased market volatility, a fractured multilateral system and mounting uncertainty, are framing the immediate policy challenge. The macroeconomic policy stance adopted to date has been lopsided and insufficiently coordinated to give a sustained boost to aggregate demand, with adjustments left to the vagaries of the market through a mixture of cost-cutting and liberalization measures. Ephemeral growth spurts and financial volatility have been the predictable results. But there are deeper challenges ahead that are truly daunting for people and the planet

Sign o' the times

Financial insecurity, economic polarization and environmental degradation have become hallmarks of the hyperglobalization era. These are, moreover, closely interconnected and mutually reinforcing, in ways that can give rise to vicious cycles of economic, social and environmental breakdown. This threat coincides with a worrying erosion of political trust, as income gaps have widened across all countries and the policy agenda perceived as catering to the interests of the winners from hyperglobalization, with scant attention paid to those who have seen limited gains or have fallen further behind. Even after the GFC, the rules of the game that had generated high levels of inequality, insecurity and indebtedness prior to that crisis have remained largely intact, adding further layers of resentment, often aimed against outsiders, and widening political divisions. This breakdown in trust has occurred at the very moment the collective actions needed to build a better future for all depend on a greater sense of shared responsibility and solidarity. The SDGs, agreed at the United Nations in 2015, were designed as a guide to that future. But with their delivery – planned for 2030 –already behind schedule, frustration is growing across different policy communities and at all levels of development. The perceived problem is a shortage of finance to achieve the scaling-up of investments on which the 2030 Agenda ultimately depends. With government finances burdened by increased debt levels and a fractured politics impeding long-term planning, pushing the financial envelope from billions to trillions of dollars each year will, it is claimed, have to rely on tapping the resources of high-wealth individuals and private financial institutions. At first glance the signs are encouraging. Global corporations are sitting on an estimated $2 trillion cash pile, while high net worth individuals have access to more than $60 trillion in assets. The OECD estimates that institutional investors in member countries hold global assets of US$92.6 trillion and while figures for institutional investors in developing countries are harder to come by, estimates for the assets held by Brazilian pension funds exceed $220 billion and some $350 billion for combined African pension funds. Redirecting a relatively small portion of these resources to meet the SDGs should, the argument goes, be able to solve the financing challenge facing the 2030 Agenda. A string of measures, marshalled under the call to “blend” and “maximize” finance, have been proposed that would channel public money into “de-risking” big investment projects while employing securitization and hedging techniques to bring in the private investors. If only things were that simple; the evidence suggests that blended finance fails to mitigate risk and instead boomerangs back to the public purse and the tax payer. In fact, vast amounts of public resources have already been used to save banks (and other financial institutions) that proved too big to fail after employing these same techniques to indulge a frenzy of speculative activity in the run-up to the financial crisis. Moreover, underpinning the vast trove of private assets is a tangled web of financial funds and debt instruments. Channelling a portion of these assets into long-term productive investment, whether in the public or private sectors, is not a matter of appealing to the better nature of those managing such funds nor establishing a more welcoming environment in which they can do business. In reality, too many governments, at all levels, have for decades been extending incentives and protections to international finance in the hope of boosting capital formation. Instead, they have been sucked in to an unstable financial world geared to short-term trading in existing assets, prone to boom and bust cycles, with baleful distributional outcomes and large debt overhangs that act as a persistent drag on the real economy. Re-engineering financial stocks and flows to support productive investments (whether private or public) will not happen without a fundamental change in the rules of the game. The current global economic environment – where austerity is the macroeconomic default option, liberalization the favoured policy tool for affecting structural change and debt the main engine of growth – is heading in the wrong direction when it comes to delivering on the ambition of the 2030 Agenda. Accordingly, this year’s Report seeks to make an alternative case for delivering the 2030 Agenda through a Global Green New Deal with a leading role for the public sector

A climate for change: The case for a global green expansion

Beyond the immediate risks that could stall the global economy are a series of macrostructural challenges that predate the GFC and have gone largely unattended since then. Four stand out because of their high degree of interdependence: the falling income share of labour; the erosion of public spending; the weakening of productive investment; and the unsustainable increases in carbon dioxide in the atmosphere. International economic-policy gatherings, where fidelity to the virtues of open borders, capital mobility and market competition is often a condition of participation, have largely neglected these challenges.

But if trends continue along current lines, the global economy in 2030 will have gone through another decade of substandard and unstable growth, income gaps within and across countries will have widened further and the natural environment will be stretched to breaking point. As labour shares across the world continue to fall, household spending will weaken, further reducing the incentive to invest in productive activities. At a minimum, this will mean lacklustre job creation and stagnant wages in developed countries as well as slow expansion (or outright contraction) of domestic markets in developing countries. Both outcomes will worsen if governments keep promoting cuts to labour costs as their adjustment strategy of choice.

Aggregate demand will be weakened further, as governments continue to reduce social protection and abstain from infrastructure investment, which will also make supply constraints tighter. Unchecked private credit creation and predatory financial practices will continue to fuel destabilizing financial transactions, while failing to stimulate private productive investment. In the meantime, absent sufficient investment and international agreement on technology transfer, carbon emissions will push the climate closer towards a point of no return. Against these trends, it is critical for governments across the world to reclaim policy space and act to boost aggregate demand. To do so, they must tackle high levels of income inequality head on, adopting more progressive fiscal arrangements, and directly targeting social outcomes through employment creation, decent work programmes and expanded social insurance. But they must also spearhead a coordinated investment push, especially towards decarbonization of the economy, both by investing directly (through public sector entities) and by boosting private investment in more productive and sustainable economic activities.

The threat of global warming requires immediate action to reduce greenhouse gas emissions and stabilize the Earth’s climate. Recent studies by the Intergovernmental Panel on Climate Change (IPCC) and the United States Global Change Research Program, among others, have made it clear that if we fail to change course, we are only a few decades away from disastrous climate-driven losses. A successful response to the climate crisis will have multiple benefits, including environmental “co-benefits” such as cleaner air and oceans and forest reclamation. Less obvious, but also important, is the economic impact of climate policy. Climate protection requires a massive new wave of investment, reinventing energy and other carbon-emitting sectors. New low-carbon technologies must be created, installed and maintained on a global scale. That wave of green investment would be a major source of income and employment growth, contributing to global macroeconomic recovery. Many, though not all, of the jobs created by green investment are inherently local to the area where investment occurs and involve training in new skills. Recent discussions call this strategy (in combination with high wages and standards, social services, and employment opportunities for all) the “Green New Deal” recalling the 1930s New Deal, which tackled unemployment and low wages, the predatory nature of finance, infrastructure gaps and regional inequalities, in the context of recovering from the Great Depression.

There are certainly numerous opportunities for investment in energy efficiency and renewable energy supply, many of them already cost-effective at today’s prices and in new patterns of high-density, transitcentred urbanism. This implies new configurations of housing, work and public services, connected by more extensive mass transit. A full-scale transition to electric vehicles will also require a more extensive infrastructure of charging stations, and continued progress in reducing vehicle costs. New technologies, not yet commercialized, will be needed to complete the decarbonization of the global economy, along with new agricultural practices, tailored to minimize emissions. A just transition will also require big investments in communities that have become dependent on resource-intensive livelihoods. Developing countries may face lower conversion costs as they are still building their energy systems.

As a result, the available resource savings from clean energy may be greater in developing countries. Clean energy is of great potential value to developing countries for another reason. Delivering energy to remote communities via an urban-centred national grid, as is usually done in developed countries, entails the substantial expense of long-distance transmission lines. Developing countries may be able to move directly to more efficient microgrid systems without the sunk cost of running wires far into remote areas. Still, they will need technology transfers and significant financial support from the international community to make the transition. Such an investment push requires governments to use all policy instruments at their disposal, including fiscal policies, industrial policies, credit provision, financial regulation and welfare policies, as well as international trade and investment policies. International coordination is critical to counteract the disruptive influence of capital mobility, contain current-account imbalances and support the transition to a low-carbon economy, especially in developing countries. Strategies for sustainable development and economic growth can take a variety of paths but they must all correct current patterns of aggregate demand. Leveraging the multiplicative effects of government spending and higher labour incomes is a straightforward approach.

First, raising the shares of labour income towards the levels of a not-so-distant past can by itself lead to significantly faster growth (0.5 per cent annually on average) thereby also increasing capital incomes. This effect will be strongest if all or most countries act in a coordinated manner. Second, a fiscal reflation financed by progressive tax increases and credit creation would boost growth even more, owing to fiscal multipliers in the range of 1.3 to 1.8 (or even higher if fiscal expansion takes place in many countries in a coordinated way). In particular, with many economies currently experiencing weak or insufficient demand, fiscal stimulus is likely to elicit a strong response of private investment. Third, public investment in clean transport and energy systems is necessary to establish low-carbon growth paths and transform food production for the growing global population, as well as to address problems of pollution and environmental degradation more generally. This requires the design of appropriate industrial policies, using subsidies, tax incentives, loans and guarantees, as well as investments in R&D and a new generation of intellectual property and licensing laws.

Based on the existing estimates, an internationally coordinated policy package of redistribution, fiscal expansion and state-led investment can realistically yield growth rates of GDP in developed economies of at least 1 per cent above what could be expected without it. In developing economies other than China, growth rates will increase by about 1.5–2 per cent annually. China will have a more moderate acceleration as its growth axis bends towards the household, with lower growth rates than the earlier East Asian tiger economies experienced when they had the current per capita income of China. By 2030, employment would increase above projections from current trends by approximately 20 million to 25 million jobs in developed countries and by more than 100 million jobs in developing countries (20 million to 30 million of which would be in China). These are conservative estimates that probably underestimate the employment gains, because existing econometric estimates based on decades of job-shedding strategies cannot incorporate the potential of a globally coordinated strategy centred on state-led investment and social spending, the expansion of service employment and a new energy matrix.

Data on growth and employment as well as on environmental factors, suggest that bold efforts are necessary to achieve global growth and development that are sustainable economically, socially and environmentally. Estimates of multipliers for the world’s 20 largest economies and the remaining regional blocs indicate that this is a matter of pragmatic policy choice, not of immutable financial constraints. A Global Green New Deal would require additional financial resources – for less than a decade – generated through a mixture of domestic resource mobilization and international cooperation agreements. Estimates also indicate that the growth impact of social spending is high in all countries, while progressive taxation has little or no cost in terms of growth, pointing to a future of higher labour incomes, lower inequality, stronger growth and a healthier environment that is available for policymakers to choose. International coordination is key both to mobilizing the required resources and to expanding policy space to manage the changes involved. Today’s economic and geopolitical tensions do not bode well in this respect. But it bears remembering that Franklin Delano Roosevelt called the founding of the International Labour Organization at the end of the First World War “a wild dream”; and wild dreamers are exactly what may be needed to deliver on the bold promises of the 2030 Agenda.

All dried up and drowning in debt

Finance is a matter of faith; and at the heart of that faith is credit – whose etymological origins lie in the Latin verb “to believe”. History has demonstrated the effectiveness of credit in fostering economic development by financing investment supported by present and future income flows, rather than by pre-existing saving, leading to higher productivity and, in turn, increasing revenues from which the debt could be repaid. But there is a darker side to debt that carries a more cautionary tale and this poses a persistent challenge to policymakers. Once banks got involved in the process of credit creation, its economic possibilities began to expand.

Using deposits (and other short-term loans) to create longer-term loans has been a standard practice of banks for centuries. But even when existing assets, such as land or houses, can be mobilized as collateral to back borrowing to finance investment, maturity transformation is inherently risky. That has typically meant commercial banks restricting their credit activities to smaller-scale and more short-term lending. Largescale and longer-term lending, particularly to governments and corporations, was traditionally left to more specialized institutions. This entire system is founded on trust: that borrowers will honour their commitment to make good on future payments; that banks will honour their liabilities; and that the state will provide secure assets for banks to hold, monitor bank behaviour and discipline them if there is a breach of trust, and provide liquidity through the lender-of-last-resort facility in the event of unforeseen difficulties. Managing debt thus involves a focus on banks as creators of credit, but also on a set of robust institutional practices that can help build trust between lenders and borrowers and can employ regulatory firewalls and disciplines that keep the system in check. In their absence, credit creation can drag the economy through damaging episodes of boom and bust and can embolden irresponsible or predatory behaviour of one kind or another.

Critically, policies to generate sustainable and equitable growth by managing debt require a state with the fiscal capacity to issue and service its own debt, which can borrow directly from the central bank at varying maturities and can manage, to some degree, the inflow and outflow of capital. This further requires that the state’s tax base expands with the productive opportunities being financed by credit and direct government expenditure. But the more open the economy and the more limited the domestic wealth base, the greater the constraint on government finances. Financial deregulation has a long history of undermining the trust on which a healthy system of credit depends and it has done so on every occasion by allowing an unchecked process of private credit creation. This time is no different. Since the 1980s, when deregulated finance grabbed the reins of hyperglobalization, global debt has risen more than 13-fold from $16 trillion in 1980 to a staggering $213 trillion in 2017, dominated by private debt, which rose from $12 trillion to $145 trillion. Rather than promoting productive and inclusive growth, private credit creation has been heavily concentrated in speculative activities, channelled through shadow-banking practices and leading to deeper income inequalities. While this rise of shadow banking is lionized in some quarters as an indication of the value of financial innovation, in practice these products have proved to be a source of instability. But, particularly when the purpose of credit is to purchase financial assets that in turn are used as collateral for further borrowing to purchase more financial assets, the greater concern is about financial instability, fuelled by speculative excess and the pursuit of assets of diminishing quality, followed by the inevitable defaults by borrowers and falling asset prices.

While these trends have raised alarm bells across international organizations, including UNCTAD, many proponents of the 2030 Agenda have nevertheless turned to private finance to fund the public goods and investment needed to deliver the SDGs. Simply put, without deep-seated reforms to the financial system, this will not do the job; the real question is how to make debt work better for development and its possible role in a Global Green New Deal. Credit creation works when it is accompanied by long run relationships between the lender and the borrower, giving the former inside knowledge of what the latter is doing with the money and encouraging a degree of patience with the management of their debts but also allowing them to exert strategic pressure through their repayment. This is particularly the case when credit creation is used to support the kind of robust domestic profit–investment nexus that has been part of a successful structural transformation over time. By providing advance means of payment, thus purchasing power, the provision of credit backed by claims on future incomes frees current capital accumulation from the shackles of past saving and becomes a central vehicle to unlock future growth potential. But for credit to play this developmental role requires governance and regulatory structures of domestic and international credit creation that put the long-term requirements of structural transformation at the centre of their operations.

This, in turn, necessitates that policymakers have the space to build appropriate public institutions to direct domestic credit creation towards productive investment, as well as sustained efforts by the international community to recover public control of the management of international credit and to redirect public finance towards development-friendly goals. The current international agenda for the financing of development, instead, subordinates developmental policy to timely debt servicing and the minimization of future repayment risk. This agenda seeks to enhance the ability of developing countries to attract private wealth through “financial innovation” that safeguards investor (and creditor) risk by diversifying and insuring such risk. While measures to improve the quality of developing country debt data and debt transparency are generally welcome and long overdue, the focus of the development finance agenda on complex – and mostly non-transparent – new financial instruments and on securitized finance, does not bode well for its ability to deliver reliable financing at the required scale to where it is most needed.

This is a greater concern as the 2030 Agenda entails unprecedented investment requirements, particularly in developing countries. UNCTAD estimates, for a sample of 31 developing countries, that meeting the basic SDG-related investment requirements to address poverty, nutrition, health and education goals, would result in an increase of public debt-to-GDP ratios from around 47 per cent at present to no less than 185 per cent, on average, if current expenditure and financing patterns prevail. Alternatively, to achieve these SDGs without an increase in existing debt-to-GDP ratios by 2030, developing countries would have to grow at an average annual rate of 11.9 per cent per year. Clearly, neither scenario is remotely realistic. The Report estimates that improved domestic resource mobilization could raise between one fifth and one half of this SDG financing gap while stabilizing debt-to-GDP ratios at current levels (depending on country-specific circumstances). “Leveraged” international private finance is not anywhere near on track to provide the trillions needed to close the remaining gap. Substantially scaling up public international development finance, including through development assistance and debt relief, should therefore be an urgent priority, if a massive new developing country debt crisis is to be avoided and the 2030 Agenda achieved on time. Such steep demands on the mobilization of international public finance will require the international monetary and financial system to open up more policy space for developing countries to develop and manage their own banking and financial sectors in the interest of structural transformation.

At the international level, progress can be made by leveraging old instruments to facilitate increased liquidity provision and international funding for climate change mitigation and combating the wider environmental crisis, in developing countries. Region-specific “debt-for-nature” swaps are already gaining traction, and a step further could be to extend these regional initiatives to the creation of Special Environmental Drawing Rights at the international level. While there seems little political appetite at present to use or expand these facilities for short-term crisis management, there is a growing consensus on the need to manage international credit creation in the interest of combating an unfolding environmental crisis that affects us all. Furthermore, and in the absence of a political consensus to rein in global financial rentierism in the interest of development, developing countries can and should leverage the power of credit creation (and debt financing) at the regional (including South–South) levels. This, too, is not a new proposal, as Southern regional payment systems and clearing unions have a fairly long history of facilitating public credit creation and liquidity provision for late development. Regional payment systems that use some form of internal clearing mechanism can make a difference in a number of ways: they can simply lower the costs of intraregional trade by allowing for settlement of corresponding financial transactions in domestic currency. More ambitiously, such arrangements can prop up national self-insurance against exogenous financial shocks through pooled reserve-swaps and by providing temporary liquidity relief within clearance periods and extending credit lines beyond these, for final settlement in domestic currency rather than the United States dollar.

Finally, full-blown regional clearing unions can leverage the power of home-grown credit creation to systematically coordinate regional adjustments between deficit and surplus regional economies, thereby shielding entire developing regions from the nefarious influence of short-term rentierist international capital flows. How and when regional credit creation can provide an effective buffer for developing countries against their exposure to private credit creation in speculative international financial markets largely depends on current regional trading patterns and the political will to shape these in future. Last, though not least, debt restructuring and relief need a revived hearing in light of the demands of the 2030 Agenda. Remarkably, given that the current state of highly complex and fragmented debtor–creditor relations has already generated rising debt and financial distress across developing countries, discussions of their management have been confined to debt reprofiling and renegotiation. Practicable ways forward are now needed to facilitate equitable and efficient sovereign debt restructurings that could, in future, also pave the way to an international regulatory framework to govern sovereign debt restructurings.

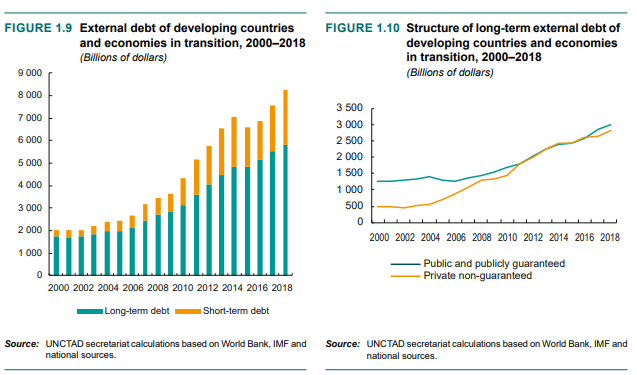

Lets take a break from the report's text and start looking at a few images. So from this point onwards the commentary is that of SouthAfricanMi staff. The image below obtained from the report shows the external debt of developing countries and economies in transition over time as well as the structure of this debt over time

Beyond the immediate risks that could stall the global economy are a series of macrostructural challenges that predate the GFC and have gone largely unattended since then. Four stand out because of their high degree of interdependence: the falling income share of labour; the erosion of public spending; the weakening of productive investment; and the unsustainable increases in carbon dioxide in the atmosphere. International economic-policy gatherings, where fidelity to the virtues of open borders, capital mobility and market competition is often a condition of participation, have largely neglected these challenges.

But if trends continue along current lines, the global economy in 2030 will have gone through another decade of substandard and unstable growth, income gaps within and across countries will have widened further and the natural environment will be stretched to breaking point. As labour shares across the world continue to fall, household spending will weaken, further reducing the incentive to invest in productive activities. At a minimum, this will mean lacklustre job creation and stagnant wages in developed countries as well as slow expansion (or outright contraction) of domestic markets in developing countries. Both outcomes will worsen if governments keep promoting cuts to labour costs as their adjustment strategy of choice.

Aggregate demand will be weakened further, as governments continue to reduce social protection and abstain from infrastructure investment, which will also make supply constraints tighter. Unchecked private credit creation and predatory financial practices will continue to fuel destabilizing financial transactions, while failing to stimulate private productive investment. In the meantime, absent sufficient investment and international agreement on technology transfer, carbon emissions will push the climate closer towards a point of no return. Against these trends, it is critical for governments across the world to reclaim policy space and act to boost aggregate demand. To do so, they must tackle high levels of income inequality head on, adopting more progressive fiscal arrangements, and directly targeting social outcomes through employment creation, decent work programmes and expanded social insurance. But they must also spearhead a coordinated investment push, especially towards decarbonization of the economy, both by investing directly (through public sector entities) and by boosting private investment in more productive and sustainable economic activities.

The threat of global warming requires immediate action to reduce greenhouse gas emissions and stabilize the Earth’s climate. Recent studies by the Intergovernmental Panel on Climate Change (IPCC) and the United States Global Change Research Program, among others, have made it clear that if we fail to change course, we are only a few decades away from disastrous climate-driven losses. A successful response to the climate crisis will have multiple benefits, including environmental “co-benefits” such as cleaner air and oceans and forest reclamation. Less obvious, but also important, is the economic impact of climate policy. Climate protection requires a massive new wave of investment, reinventing energy and other carbon-emitting sectors. New low-carbon technologies must be created, installed and maintained on a global scale. That wave of green investment would be a major source of income and employment growth, contributing to global macroeconomic recovery. Many, though not all, of the jobs created by green investment are inherently local to the area where investment occurs and involve training in new skills. Recent discussions call this strategy (in combination with high wages and standards, social services, and employment opportunities for all) the “Green New Deal” recalling the 1930s New Deal, which tackled unemployment and low wages, the predatory nature of finance, infrastructure gaps and regional inequalities, in the context of recovering from the Great Depression.

There are certainly numerous opportunities for investment in energy efficiency and renewable energy supply, many of them already cost-effective at today’s prices and in new patterns of high-density, transitcentred urbanism. This implies new configurations of housing, work and public services, connected by more extensive mass transit. A full-scale transition to electric vehicles will also require a more extensive infrastructure of charging stations, and continued progress in reducing vehicle costs. New technologies, not yet commercialized, will be needed to complete the decarbonization of the global economy, along with new agricultural practices, tailored to minimize emissions. A just transition will also require big investments in communities that have become dependent on resource-intensive livelihoods. Developing countries may face lower conversion costs as they are still building their energy systems.

As a result, the available resource savings from clean energy may be greater in developing countries. Clean energy is of great potential value to developing countries for another reason. Delivering energy to remote communities via an urban-centred national grid, as is usually done in developed countries, entails the substantial expense of long-distance transmission lines. Developing countries may be able to move directly to more efficient microgrid systems without the sunk cost of running wires far into remote areas. Still, they will need technology transfers and significant financial support from the international community to make the transition. Such an investment push requires governments to use all policy instruments at their disposal, including fiscal policies, industrial policies, credit provision, financial regulation and welfare policies, as well as international trade and investment policies. International coordination is critical to counteract the disruptive influence of capital mobility, contain current-account imbalances and support the transition to a low-carbon economy, especially in developing countries. Strategies for sustainable development and economic growth can take a variety of paths but they must all correct current patterns of aggregate demand. Leveraging the multiplicative effects of government spending and higher labour incomes is a straightforward approach.

First, raising the shares of labour income towards the levels of a not-so-distant past can by itself lead to significantly faster growth (0.5 per cent annually on average) thereby also increasing capital incomes. This effect will be strongest if all or most countries act in a coordinated manner. Second, a fiscal reflation financed by progressive tax increases and credit creation would boost growth even more, owing to fiscal multipliers in the range of 1.3 to 1.8 (or even higher if fiscal expansion takes place in many countries in a coordinated way). In particular, with many economies currently experiencing weak or insufficient demand, fiscal stimulus is likely to elicit a strong response of private investment. Third, public investment in clean transport and energy systems is necessary to establish low-carbon growth paths and transform food production for the growing global population, as well as to address problems of pollution and environmental degradation more generally. This requires the design of appropriate industrial policies, using subsidies, tax incentives, loans and guarantees, as well as investments in R&D and a new generation of intellectual property and licensing laws.

Based on the existing estimates, an internationally coordinated policy package of redistribution, fiscal expansion and state-led investment can realistically yield growth rates of GDP in developed economies of at least 1 per cent above what could be expected without it. In developing economies other than China, growth rates will increase by about 1.5–2 per cent annually. China will have a more moderate acceleration as its growth axis bends towards the household, with lower growth rates than the earlier East Asian tiger economies experienced when they had the current per capita income of China. By 2030, employment would increase above projections from current trends by approximately 20 million to 25 million jobs in developed countries and by more than 100 million jobs in developing countries (20 million to 30 million of which would be in China). These are conservative estimates that probably underestimate the employment gains, because existing econometric estimates based on decades of job-shedding strategies cannot incorporate the potential of a globally coordinated strategy centred on state-led investment and social spending, the expansion of service employment and a new energy matrix.

Data on growth and employment as well as on environmental factors, suggest that bold efforts are necessary to achieve global growth and development that are sustainable economically, socially and environmentally. Estimates of multipliers for the world’s 20 largest economies and the remaining regional blocs indicate that this is a matter of pragmatic policy choice, not of immutable financial constraints. A Global Green New Deal would require additional financial resources – for less than a decade – generated through a mixture of domestic resource mobilization and international cooperation agreements. Estimates also indicate that the growth impact of social spending is high in all countries, while progressive taxation has little or no cost in terms of growth, pointing to a future of higher labour incomes, lower inequality, stronger growth and a healthier environment that is available for policymakers to choose. International coordination is key both to mobilizing the required resources and to expanding policy space to manage the changes involved. Today’s economic and geopolitical tensions do not bode well in this respect. But it bears remembering that Franklin Delano Roosevelt called the founding of the International Labour Organization at the end of the First World War “a wild dream”; and wild dreamers are exactly what may be needed to deliver on the bold promises of the 2030 Agenda.

All dried up and drowning in debt

Finance is a matter of faith; and at the heart of that faith is credit – whose etymological origins lie in the Latin verb “to believe”. History has demonstrated the effectiveness of credit in fostering economic development by financing investment supported by present and future income flows, rather than by pre-existing saving, leading to higher productivity and, in turn, increasing revenues from which the debt could be repaid. But there is a darker side to debt that carries a more cautionary tale and this poses a persistent challenge to policymakers. Once banks got involved in the process of credit creation, its economic possibilities began to expand.

Using deposits (and other short-term loans) to create longer-term loans has been a standard practice of banks for centuries. But even when existing assets, such as land or houses, can be mobilized as collateral to back borrowing to finance investment, maturity transformation is inherently risky. That has typically meant commercial banks restricting their credit activities to smaller-scale and more short-term lending. Largescale and longer-term lending, particularly to governments and corporations, was traditionally left to more specialized institutions. This entire system is founded on trust: that borrowers will honour their commitment to make good on future payments; that banks will honour their liabilities; and that the state will provide secure assets for banks to hold, monitor bank behaviour and discipline them if there is a breach of trust, and provide liquidity through the lender-of-last-resort facility in the event of unforeseen difficulties. Managing debt thus involves a focus on banks as creators of credit, but also on a set of robust institutional practices that can help build trust between lenders and borrowers and can employ regulatory firewalls and disciplines that keep the system in check. In their absence, credit creation can drag the economy through damaging episodes of boom and bust and can embolden irresponsible or predatory behaviour of one kind or another.

Critically, policies to generate sustainable and equitable growth by managing debt require a state with the fiscal capacity to issue and service its own debt, which can borrow directly from the central bank at varying maturities and can manage, to some degree, the inflow and outflow of capital. This further requires that the state’s tax base expands with the productive opportunities being financed by credit and direct government expenditure. But the more open the economy and the more limited the domestic wealth base, the greater the constraint on government finances. Financial deregulation has a long history of undermining the trust on which a healthy system of credit depends and it has done so on every occasion by allowing an unchecked process of private credit creation. This time is no different. Since the 1980s, when deregulated finance grabbed the reins of hyperglobalization, global debt has risen more than 13-fold from $16 trillion in 1980 to a staggering $213 trillion in 2017, dominated by private debt, which rose from $12 trillion to $145 trillion. Rather than promoting productive and inclusive growth, private credit creation has been heavily concentrated in speculative activities, channelled through shadow-banking practices and leading to deeper income inequalities. While this rise of shadow banking is lionized in some quarters as an indication of the value of financial innovation, in practice these products have proved to be a source of instability. But, particularly when the purpose of credit is to purchase financial assets that in turn are used as collateral for further borrowing to purchase more financial assets, the greater concern is about financial instability, fuelled by speculative excess and the pursuit of assets of diminishing quality, followed by the inevitable defaults by borrowers and falling asset prices.

While these trends have raised alarm bells across international organizations, including UNCTAD, many proponents of the 2030 Agenda have nevertheless turned to private finance to fund the public goods and investment needed to deliver the SDGs. Simply put, without deep-seated reforms to the financial system, this will not do the job; the real question is how to make debt work better for development and its possible role in a Global Green New Deal. Credit creation works when it is accompanied by long run relationships between the lender and the borrower, giving the former inside knowledge of what the latter is doing with the money and encouraging a degree of patience with the management of their debts but also allowing them to exert strategic pressure through their repayment. This is particularly the case when credit creation is used to support the kind of robust domestic profit–investment nexus that has been part of a successful structural transformation over time. By providing advance means of payment, thus purchasing power, the provision of credit backed by claims on future incomes frees current capital accumulation from the shackles of past saving and becomes a central vehicle to unlock future growth potential. But for credit to play this developmental role requires governance and regulatory structures of domestic and international credit creation that put the long-term requirements of structural transformation at the centre of their operations.

This, in turn, necessitates that policymakers have the space to build appropriate public institutions to direct domestic credit creation towards productive investment, as well as sustained efforts by the international community to recover public control of the management of international credit and to redirect public finance towards development-friendly goals. The current international agenda for the financing of development, instead, subordinates developmental policy to timely debt servicing and the minimization of future repayment risk. This agenda seeks to enhance the ability of developing countries to attract private wealth through “financial innovation” that safeguards investor (and creditor) risk by diversifying and insuring such risk. While measures to improve the quality of developing country debt data and debt transparency are generally welcome and long overdue, the focus of the development finance agenda on complex – and mostly non-transparent – new financial instruments and on securitized finance, does not bode well for its ability to deliver reliable financing at the required scale to where it is most needed.

This is a greater concern as the 2030 Agenda entails unprecedented investment requirements, particularly in developing countries. UNCTAD estimates, for a sample of 31 developing countries, that meeting the basic SDG-related investment requirements to address poverty, nutrition, health and education goals, would result in an increase of public debt-to-GDP ratios from around 47 per cent at present to no less than 185 per cent, on average, if current expenditure and financing patterns prevail. Alternatively, to achieve these SDGs without an increase in existing debt-to-GDP ratios by 2030, developing countries would have to grow at an average annual rate of 11.9 per cent per year. Clearly, neither scenario is remotely realistic. The Report estimates that improved domestic resource mobilization could raise between one fifth and one half of this SDG financing gap while stabilizing debt-to-GDP ratios at current levels (depending on country-specific circumstances). “Leveraged” international private finance is not anywhere near on track to provide the trillions needed to close the remaining gap. Substantially scaling up public international development finance, including through development assistance and debt relief, should therefore be an urgent priority, if a massive new developing country debt crisis is to be avoided and the 2030 Agenda achieved on time. Such steep demands on the mobilization of international public finance will require the international monetary and financial system to open up more policy space for developing countries to develop and manage their own banking and financial sectors in the interest of structural transformation.

At the international level, progress can be made by leveraging old instruments to facilitate increased liquidity provision and international funding for climate change mitigation and combating the wider environmental crisis, in developing countries. Region-specific “debt-for-nature” swaps are already gaining traction, and a step further could be to extend these regional initiatives to the creation of Special Environmental Drawing Rights at the international level. While there seems little political appetite at present to use or expand these facilities for short-term crisis management, there is a growing consensus on the need to manage international credit creation in the interest of combating an unfolding environmental crisis that affects us all. Furthermore, and in the absence of a political consensus to rein in global financial rentierism in the interest of development, developing countries can and should leverage the power of credit creation (and debt financing) at the regional (including South–South) levels. This, too, is not a new proposal, as Southern regional payment systems and clearing unions have a fairly long history of facilitating public credit creation and liquidity provision for late development. Regional payment systems that use some form of internal clearing mechanism can make a difference in a number of ways: they can simply lower the costs of intraregional trade by allowing for settlement of corresponding financial transactions in domestic currency. More ambitiously, such arrangements can prop up national self-insurance against exogenous financial shocks through pooled reserve-swaps and by providing temporary liquidity relief within clearance periods and extending credit lines beyond these, for final settlement in domestic currency rather than the United States dollar.

Finally, full-blown regional clearing unions can leverage the power of home-grown credit creation to systematically coordinate regional adjustments between deficit and surplus regional economies, thereby shielding entire developing regions from the nefarious influence of short-term rentierist international capital flows. How and when regional credit creation can provide an effective buffer for developing countries against their exposure to private credit creation in speculative international financial markets largely depends on current regional trading patterns and the political will to shape these in future. Last, though not least, debt restructuring and relief need a revived hearing in light of the demands of the 2030 Agenda. Remarkably, given that the current state of highly complex and fragmented debtor–creditor relations has already generated rising debt and financial distress across developing countries, discussions of their management have been confined to debt reprofiling and renegotiation. Practicable ways forward are now needed to facilitate equitable and efficient sovereign debt restructurings that could, in future, also pave the way to an international regulatory framework to govern sovereign debt restructurings.

Lets take a break from the report's text and start looking at a few images. So from this point onwards the commentary is that of SouthAfricanMi staff. The image below obtained from the report shows the external debt of developing countries and economies in transition over time as well as the structure of this debt over time

The worry we have with all this debt is the fact that it needs to be repaid at some point, and in the majority of cases the developing and transition economies have to pay higher rates of interest on debt issued as the perceived risk of buying debt issued by developing and transition economies is far greater than buying debt issued by the developed world for example. So if the US issues $1 billion in debt maturing in 5 years they might only have to pay say 3% for example, but of a country like South Africa has to issue the same amount of debt for same maturity date it will have to pay rates of say 5% or even higher to compensate investors for the greater "risk" they are taking by buying developing country debt instead of developed country debt.

Essentially what this means is that if the developed and developing economies issue the same amount of debt over time, the developing countries will pay a far greater amount of money towards servicing and paying off debt than what the developed countries would, and this will mean that developing countries will always lag behind the developed countries based on the fact that money developing countries spend on higher debt and debt servicing costs compared to the developed world, and that difference in debt servicing costs the developed countries can use in actually developing their countries even more, leading to continued disparity between developed and developing economies.

Essentially what this means is that if the developed and developing economies issue the same amount of debt over time, the developing countries will pay a far greater amount of money towards servicing and paying off debt than what the developed countries would, and this will mean that developing countries will always lag behind the developed countries based on the fact that money developing countries spend on higher debt and debt servicing costs compared to the developed world, and that difference in debt servicing costs the developed countries can use in actually developing their countries even more, leading to continued disparity between developed and developing economies.