|

Related Topics |

|

We take a look at the latest dry cargo shipping trends as published by the United Nations conference on trade and development (UNCTAD). South Africa is mentioned in the report, especially when it comes to the supply of Iron Ore, with South Africa supplying 4% of China's iron ore imports. With Australia supplying a whopping 21% of China's iron ore imports

|

|

Trends of dry cargo being shipped.

Dry bulk shipments: Major and minor dry bulks

Following a limited expansion in 2015–2016, global dry bulk trade grew by about 4 per cent in 2017, bringing total volumes to 5.1 billion tons. A sharp increase in iron ore imports to China, a rebound in global coal trade and improved growth in minor bulk trades supported the expansion. Overall, strong import demand in China remained the main factor behind growth in global dry bulk trade. An overview of global players in the dry bulk commodities trade sector is presented in table 1.8.

Iron ore

Iron ore imports to China increased by 5 per cent in 2017, bringing total volumes to nearly 1.1 billion tons. With a market share of more than 70 per cent, China remains the main source of global iron ore demand. A rise in steel production and the closure of more than 100 million tons per annum of outdated steelmaking capacity in 2016–2017 boosted the country’s demand for imports. Further, the increased use of higher grade imported iron ore displaced domestic supplies. The leading iron ore exporters were Australia, Brazil and South Africa; Australia and Brazil supplied over 85 per cent of the demand for imports in China. Nevertheless, Australia is by far the largest exporter, supplying nearly two thirds of iron ore requirements in China. The country imports 21 per cent of its iron ore requirements from Brazil, which benefits the dry bulk shipping industry through long distances. South Africa generates 4 per cent of all iron ore imports to China. Other suppliers, such as India, the Islamic Republic of Iran and Sierra Leone, have also increased their exports to China.

Coal

Global coal trade resumed growth in 2017, increasing by 5.8 per cent following a limited expansion in 2016 and a significant decline in 2015. Higher import demand in China, the Republic of Korea and a number of South-East Asian countries supported the volume increase. Coal imports to China continued to provide strong support for dry bulk shipping demand. China, India, Japan, Malaysia, and the Republic of Korea are major importers of coal, while Australia and Indonesia are major exporters of the commodity. Growing coal exports from the United States to China are benefiting dry bulk shipping. One factor is the uncertainty over the Indian coal trade. On the one hand, India plans to increase domestic production, which may alter the balance between locally sourced and imported coal. On the other hand, growing demand from the steel sector in India may boost seaborne imports of coking coal

Grain

Global grain trade, including wheat, coarse grains and soybeans, reached 515.1 million tons in 2017, a 7.1 per cent increase over 2016. Exports are dominated by a few countries, notably the United States; importers tend to be regionally diverse. As in other dry bulk trades, Asia was a driving force of growth, albeit not the only one. In 2017, grain trade was underpinned by a 14.7 per cent increase in soybean imports to China and growing exports from Brazil and the United States. China dominates the soybean trade and accounted for nearly two thirds of the global soybean import demand in 2017. Outside Asia and the European Union, some lesser consuming regions, such as Africa and Western Asia, also contributed to such growth. Tariffs by the United States on certain goods imported from China, including steel and aluminium, and retaliation by China, may lead to restricting soybean import from the United States. China is the world’s largest consumer and importer of uncrushed soybeans. However, it may decide to replace imports from the United States and source its soybean requirements from alternative suppliers such as Brazil. While trade restrictions generally portend ominous consequences for shipping, a shift in suppliers and routes in this context may have an unintended positive effect on ton-miles generated.

Minor bulks

Growing manufacturing activity and construction demand supported a 2.2 per cent increase in minor bulks commodity trade. Rising demand for commodities such as bauxite, scrap and nickel ore pushed volumes to 1.9 billion tons. However, the large drop (less 30.8 per cent) in exports of steel products from China due to reforms in the country’s steel sector undermined the expansion to some extent. Bauxite shipments expanded by 19.5 per cent, accounting for 13 per cent of minor dry bulks commodities trade in 2017.

Following a limited expansion in 2015–2016, global dry bulk trade grew by about 4 per cent in 2017, bringing total volumes to 5.1 billion tons. A sharp increase in iron ore imports to China, a rebound in global coal trade and improved growth in minor bulk trades supported the expansion. Overall, strong import demand in China remained the main factor behind growth in global dry bulk trade. An overview of global players in the dry bulk commodities trade sector is presented in table 1.8.

Iron ore

Iron ore imports to China increased by 5 per cent in 2017, bringing total volumes to nearly 1.1 billion tons. With a market share of more than 70 per cent, China remains the main source of global iron ore demand. A rise in steel production and the closure of more than 100 million tons per annum of outdated steelmaking capacity in 2016–2017 boosted the country’s demand for imports. Further, the increased use of higher grade imported iron ore displaced domestic supplies. The leading iron ore exporters were Australia, Brazil and South Africa; Australia and Brazil supplied over 85 per cent of the demand for imports in China. Nevertheless, Australia is by far the largest exporter, supplying nearly two thirds of iron ore requirements in China. The country imports 21 per cent of its iron ore requirements from Brazil, which benefits the dry bulk shipping industry through long distances. South Africa generates 4 per cent of all iron ore imports to China. Other suppliers, such as India, the Islamic Republic of Iran and Sierra Leone, have also increased their exports to China.

Coal

Global coal trade resumed growth in 2017, increasing by 5.8 per cent following a limited expansion in 2016 and a significant decline in 2015. Higher import demand in China, the Republic of Korea and a number of South-East Asian countries supported the volume increase. Coal imports to China continued to provide strong support for dry bulk shipping demand. China, India, Japan, Malaysia, and the Republic of Korea are major importers of coal, while Australia and Indonesia are major exporters of the commodity. Growing coal exports from the United States to China are benefiting dry bulk shipping. One factor is the uncertainty over the Indian coal trade. On the one hand, India plans to increase domestic production, which may alter the balance between locally sourced and imported coal. On the other hand, growing demand from the steel sector in India may boost seaborne imports of coking coal

Grain

Global grain trade, including wheat, coarse grains and soybeans, reached 515.1 million tons in 2017, a 7.1 per cent increase over 2016. Exports are dominated by a few countries, notably the United States; importers tend to be regionally diverse. As in other dry bulk trades, Asia was a driving force of growth, albeit not the only one. In 2017, grain trade was underpinned by a 14.7 per cent increase in soybean imports to China and growing exports from Brazil and the United States. China dominates the soybean trade and accounted for nearly two thirds of the global soybean import demand in 2017. Outside Asia and the European Union, some lesser consuming regions, such as Africa and Western Asia, also contributed to such growth. Tariffs by the United States on certain goods imported from China, including steel and aluminium, and retaliation by China, may lead to restricting soybean import from the United States. China is the world’s largest consumer and importer of uncrushed soybeans. However, it may decide to replace imports from the United States and source its soybean requirements from alternative suppliers such as Brazil. While trade restrictions generally portend ominous consequences for shipping, a shift in suppliers and routes in this context may have an unintended positive effect on ton-miles generated.

Minor bulks

Growing manufacturing activity and construction demand supported a 2.2 per cent increase in minor bulks commodity trade. Rising demand for commodities such as bauxite, scrap and nickel ore pushed volumes to 1.9 billion tons. However, the large drop (less 30.8 per cent) in exports of steel products from China due to reforms in the country’s steel sector undermined the expansion to some extent. Bauxite shipments expanded by 19.5 per cent, accounting for 13 per cent of minor dry bulks commodities trade in 2017.

The continued rise in Chinese aluminium production and the availability of bauxite ore, following years of export disruptions, led to an expansion in

bauxite trade. While China dominates the import side with a market share of more than two thirds, key players on the supply side are more varied and include Australia, Brazil, Guinea and India. Nickel ore trade rose by 7.6 per cent, highlighted in particular by increased growth in nickel ore shipments from Indonesia, following its decision to relax its export ban on unprocessed ores.

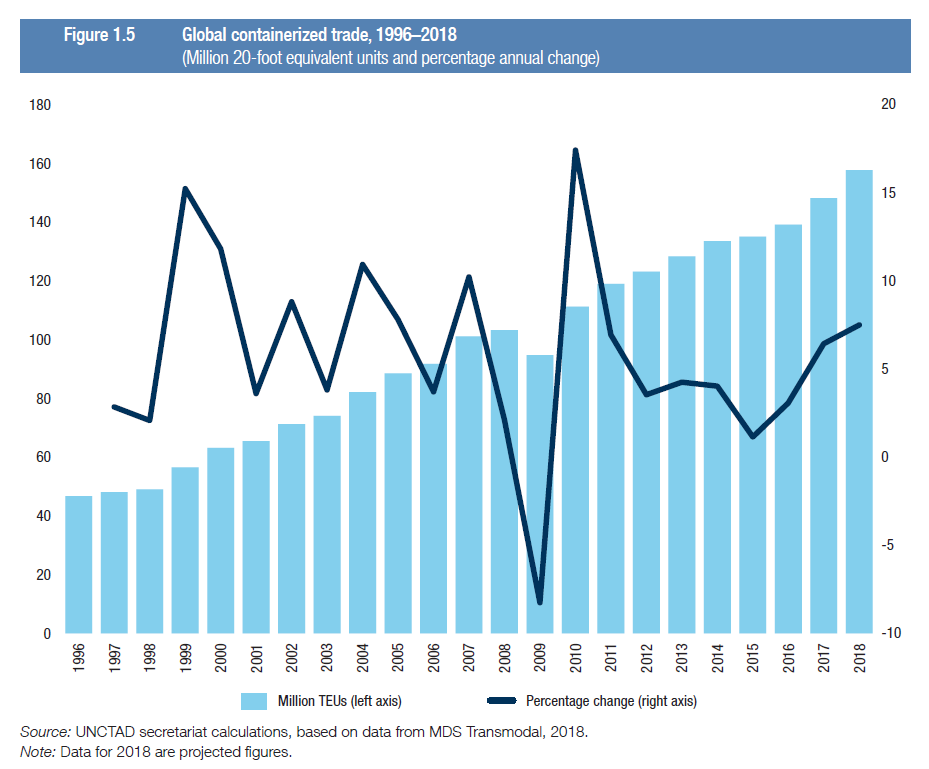

Other dry cargo: Containerized trade

Following the difficult years of 2015 and 2016 when containerized trade grew modestly at 1.1 per cent and 3.1 per cent, respectively, container market conditions improved in 2017, and strong growth in volumes was recorded across all routes. World containerized trade volumes expanded by a strong 6.4 per cent in 2017,the fastest rate since 2011. Global volumes reached 148 million TEUs, supported by various positive trends. The modest global recovery was central to the rise in containerized volumes. In addition, factors such as a recession in Brazil and the Russian Federation,

increased consumption requirements in the United States, improved commodity prices, strong import demand from China and the rapid growth of intra-Asian trade reflecting the effect of regional integration and participation in global value chains, contributed to the recovery. Trade growth strengthened on the major East–West trade lanes, namely Asia–Europe, the Trans-Pacific and transatlantic routes

Volumes on the Trans-Pacific route (eastbound and westbound) increased by 4.7 per cent, while volumes on the East Asia–North America route (eastbound and westbound) increased by 7.1 per cent. Overall, the Trans-Pacific trade lane remained the busiest, with total volumes reaching 27.6 million TEUs, followed by 24.8 million TEUs on the Asia–Europe route and 8.1 million TEUs on the transatlantic route. Growth accelerated across non-mainlane routes. Robust growth (6.5 per cent) on the North–South trade route reflected improvements in the commodity price environment and the higher import demand of oil- and commodity-exporting countries. Supported by positive economic trends in China, economic growth in emerging Asian economies, as well as regional integration and global value chains, volumes on the intra-Asian routes picked up, expanding by 6.7 per cent. Containerized trade on the non-mainlane East–West routes grew by an estimated 4.0 per cent, with varied performances across individual routes; key factors were faster growth on routes within and outside the Indian subcontinent and slower growth on routes within and outside Western Asia.

bauxite trade. While China dominates the import side with a market share of more than two thirds, key players on the supply side are more varied and include Australia, Brazil, Guinea and India. Nickel ore trade rose by 7.6 per cent, highlighted in particular by increased growth in nickel ore shipments from Indonesia, following its decision to relax its export ban on unprocessed ores.

Other dry cargo: Containerized trade

Following the difficult years of 2015 and 2016 when containerized trade grew modestly at 1.1 per cent and 3.1 per cent, respectively, container market conditions improved in 2017, and strong growth in volumes was recorded across all routes. World containerized trade volumes expanded by a strong 6.4 per cent in 2017,the fastest rate since 2011. Global volumes reached 148 million TEUs, supported by various positive trends. The modest global recovery was central to the rise in containerized volumes. In addition, factors such as a recession in Brazil and the Russian Federation,

increased consumption requirements in the United States, improved commodity prices, strong import demand from China and the rapid growth of intra-Asian trade reflecting the effect of regional integration and participation in global value chains, contributed to the recovery. Trade growth strengthened on the major East–West trade lanes, namely Asia–Europe, the Trans-Pacific and transatlantic routes

Volumes on the Trans-Pacific route (eastbound and westbound) increased by 4.7 per cent, while volumes on the East Asia–North America route (eastbound and westbound) increased by 7.1 per cent. Overall, the Trans-Pacific trade lane remained the busiest, with total volumes reaching 27.6 million TEUs, followed by 24.8 million TEUs on the Asia–Europe route and 8.1 million TEUs on the transatlantic route. Growth accelerated across non-mainlane routes. Robust growth (6.5 per cent) on the North–South trade route reflected improvements in the commodity price environment and the higher import demand of oil- and commodity-exporting countries. Supported by positive economic trends in China, economic growth in emerging Asian economies, as well as regional integration and global value chains, volumes on the intra-Asian routes picked up, expanding by 6.7 per cent. Containerized trade on the non-mainlane East–West routes grew by an estimated 4.0 per cent, with varied performances across individual routes; key factors were faster growth on routes within and outside the Indian subcontinent and slower growth on routes within and outside Western Asia.

Positive trends in the containerized trade market unfolded against the backdrop of continued market consolidation; alliance reshuffling; ordering of larger ships, with capacities likely to stabilize at close to 20,000–22,000 TEUs; as well as a growing momentum surrounding e-commerce and digitalization. Together these factors are reshaping the containerized trade and liner shipping landscape and raising new challenges and opportunities for the sector. The rise of mega alliances is likely to reinforce the commoditization of container transportation services, as they tend to limit liner shipping service or product differentiation (McKinsey and Company, 2017a). This means that lines would be unable to differentiate themselves and to compete based on service. As a member of an alliance, a shipping line may not be able to offer faster and more reliable services than its alliance partners. For shippers, the commoditization of services would also be an unfavourable development, as it limits their ability to obtain greater transparency and reliability, as well as the right services. This is because shippers do not know which ship or operator is handling their cargo in an alliance arrangement. Overall, it seems that alliances help to expand the service range available but tend to heighten operational complexities and detract from transparency along the logistics chain.

Electronic commerce

The rapid expansion of e-commerce is of direct relevance to the container shipping market, given the related implications for consumption patterns, retail models, distribution networks, and transport and logistics. UNCTAD estimates global e-commerce at almost $26 trillion in 2016 (UNCTAD, 2018d). Cross-border e-commerce is particularly relevant to shipping and accounts for a relatively smaller share of total e-commerce in general and business-to consumer sales, in particular. According to UNCTAD, such cross-border transactions were worth about $189 billion in 2015. Dwarfed by the size of domestic business-to-consumer e-commerce, cross-border sales in that year accounted for 6.5 per cent of total business-to-consumer e-commerce (UNCTAD, 2017a). Nevertheless, business-to-consumer e-commerce, including cross-border transactions, is growing rapidly, and Asia is becoming a major growth area. While data on e-commerce trends in developing countries are difficult to obtain, cross-border e-commerce in China was said to account for up to 20 per cent of total import and export trading volumes (JOC.com, 2017).

Elsewhere in the region, the size of e-commerce-related business is much smaller, but is characterized by rapid growth. In India, e-commerce sales were estimated at around $40 billion in 2016, up from $4 billion in 2009, while in Indonesia, the market was worth about $6 billion in 2016. By 2020, 45 per cent of online shoppers are expected to buy goods from other countries. This would represent a fourfold increase in the value of cross-border sales since 2014 (Colliers International, 2017). Shipping, like other modes of transport, is also part of the e-commerce supply chain. However, the extent to which container shipping is able to benefit from e-commerce trade flows and capture some of the associated gains remains unclear in view of the relatively small share of cross-border business-to-consumer e-commerce flows and the participation of alternative modes of transport. The speed of air transport favourably positions aviation as a better fit for e-commerce trade, notably for high value and time-sensitive cargo.

Rail transport could also gain market share as illustrated by developments in the China–Europe rail connections and the example offered by the China–Germany service advertised on the Alibaba portal (Colliers International, 2017). Nevertheless, ocean shipping is expected to contribute to e-commerce trade and benefit from the transport of other goods and products that rests on the building of inventories near consumption markets. For shipping to tap the trade potential arising from e-commerce, operators need to adapt, leverage technology for greater efficiencies and design integrated supply chain solutions that are e-commerce-friendly. Adaptation and planning for change is critical for shipping to remain a relevant market player. In this respect, concerns have recently been raised over the potential for e-retailers to displace traditional players such as liner shipping operators. While these concerns have generally been downplayed, shipping lines recognize the potential risks and seem to be adapting their business models to account for these emerging trends, including by leveraging technology and digitalization to ensure efficiency gains and capture market share. An example is the new global integrator strategy pursued by Maersk to drive down costs, improve reliability, enhance responsiveness and forge a better link with customers (Maersk, 2018).

Digitalization

Today, the shipping industry is cautiously embracing relevant technologies arising from digitalization. More and more, carriers and freight forwarders alike are taking measures to digitalize internal processes, develop integrated information technology infrastructures and offer real-time transparency on shipments. Digital start-ups such as Xeneta, Flexport and Kontainers are being launched (McKinsey and Company, 2017b).

These solutions aim to provide user-friendly online interfaces for shippers, while facilitating processes and enhancing transparency. Recent developments relating to blockchain technology aimed at facilitating seaborne trade are also important. Some argue that the technology could save $300 in customs clearance costs for each consignment and that it could potentially generate $5.4 million in savings on each shipment associated with a ship that has a capacity of 18,000 TEUs (Marine and Offshore Technology, 2017). Other technologies of relevance to seaborne trade include robotics, artificial intelligence and additive manufacturing or three-dimensional printing. Robotics have some implications for production localization by enabling zero-labour factories (Danish Ship Finance, 2017). According to UNCTAD research however, robot use in low-wage labour-intensive manufacturing has remained low (UNCTAD, 2017b).

Three-dimensional printing and robotics may facilitate regionalized manufacturing and lead to some reshoring by displacing low-cost labour. While three-dimensional printing, in particular, is not expected to cause a massive relocalization pattern, it may have an incremental impact and affect specific niche markets. In time, this technology may lead to less raw materials being used in manufacturing. Until it becomes widespread and cost-effective, for now the impact of three-dimensional printing is expected to be marginal – existing estimates suggest that TEU volumes will drop by less than 1 per cent by 2035 (JOC.com, 2017).

Electronic commerce

The rapid expansion of e-commerce is of direct relevance to the container shipping market, given the related implications for consumption patterns, retail models, distribution networks, and transport and logistics. UNCTAD estimates global e-commerce at almost $26 trillion in 2016 (UNCTAD, 2018d). Cross-border e-commerce is particularly relevant to shipping and accounts for a relatively smaller share of total e-commerce in general and business-to consumer sales, in particular. According to UNCTAD, such cross-border transactions were worth about $189 billion in 2015. Dwarfed by the size of domestic business-to-consumer e-commerce, cross-border sales in that year accounted for 6.5 per cent of total business-to-consumer e-commerce (UNCTAD, 2017a). Nevertheless, business-to-consumer e-commerce, including cross-border transactions, is growing rapidly, and Asia is becoming a major growth area. While data on e-commerce trends in developing countries are difficult to obtain, cross-border e-commerce in China was said to account for up to 20 per cent of total import and export trading volumes (JOC.com, 2017).

Elsewhere in the region, the size of e-commerce-related business is much smaller, but is characterized by rapid growth. In India, e-commerce sales were estimated at around $40 billion in 2016, up from $4 billion in 2009, while in Indonesia, the market was worth about $6 billion in 2016. By 2020, 45 per cent of online shoppers are expected to buy goods from other countries. This would represent a fourfold increase in the value of cross-border sales since 2014 (Colliers International, 2017). Shipping, like other modes of transport, is also part of the e-commerce supply chain. However, the extent to which container shipping is able to benefit from e-commerce trade flows and capture some of the associated gains remains unclear in view of the relatively small share of cross-border business-to-consumer e-commerce flows and the participation of alternative modes of transport. The speed of air transport favourably positions aviation as a better fit for e-commerce trade, notably for high value and time-sensitive cargo.

Rail transport could also gain market share as illustrated by developments in the China–Europe rail connections and the example offered by the China–Germany service advertised on the Alibaba portal (Colliers International, 2017). Nevertheless, ocean shipping is expected to contribute to e-commerce trade and benefit from the transport of other goods and products that rests on the building of inventories near consumption markets. For shipping to tap the trade potential arising from e-commerce, operators need to adapt, leverage technology for greater efficiencies and design integrated supply chain solutions that are e-commerce-friendly. Adaptation and planning for change is critical for shipping to remain a relevant market player. In this respect, concerns have recently been raised over the potential for e-retailers to displace traditional players such as liner shipping operators. While these concerns have generally been downplayed, shipping lines recognize the potential risks and seem to be adapting their business models to account for these emerging trends, including by leveraging technology and digitalization to ensure efficiency gains and capture market share. An example is the new global integrator strategy pursued by Maersk to drive down costs, improve reliability, enhance responsiveness and forge a better link with customers (Maersk, 2018).

Digitalization

Today, the shipping industry is cautiously embracing relevant technologies arising from digitalization. More and more, carriers and freight forwarders alike are taking measures to digitalize internal processes, develop integrated information technology infrastructures and offer real-time transparency on shipments. Digital start-ups such as Xeneta, Flexport and Kontainers are being launched (McKinsey and Company, 2017b).

These solutions aim to provide user-friendly online interfaces for shippers, while facilitating processes and enhancing transparency. Recent developments relating to blockchain technology aimed at facilitating seaborne trade are also important. Some argue that the technology could save $300 in customs clearance costs for each consignment and that it could potentially generate $5.4 million in savings on each shipment associated with a ship that has a capacity of 18,000 TEUs (Marine and Offshore Technology, 2017). Other technologies of relevance to seaborne trade include robotics, artificial intelligence and additive manufacturing or three-dimensional printing. Robotics have some implications for production localization by enabling zero-labour factories (Danish Ship Finance, 2017). According to UNCTAD research however, robot use in low-wage labour-intensive manufacturing has remained low (UNCTAD, 2017b).

Three-dimensional printing and robotics may facilitate regionalized manufacturing and lead to some reshoring by displacing low-cost labour. While three-dimensional printing, in particular, is not expected to cause a massive relocalization pattern, it may have an incremental impact and affect specific niche markets. In time, this technology may lead to less raw materials being used in manufacturing. Until it becomes widespread and cost-effective, for now the impact of three-dimensional printing is expected to be marginal – existing estimates suggest that TEU volumes will drop by less than 1 per cent by 2035 (JOC.com, 2017).