|

Related Topics |

|

We take a look at the financial results for the year ended June 2019 of Spur Corporation (SUR), one of the leading restaurant and food franchise groups in South Africa.

|

|

About Spur Corporation

Spur Corporation owns some of the most well know food franchise brands in South Africa. Some of their brands names include

- Spur Steak Ranches

- Pizza and Pasta (Panarottis and Casa Bella):

- John Dory’s Fish Grill Sushi:

- The Hussar Grill

- RocoMamas

- Nikos Chargrilled Greek

Review of Spur's latest financial results

- Revenue: R944.779 million (up 5.9% from R891.797 million for the same period of the previous year)

- Profit for the period: R173. 105 million (up 6.6% from R162.459 million for the same period of the previous year)

- Diluted earnings per share: R1.73 (up from R1.61 for the same period of the previous year)

- PE ratio: 12.89

- Dividend declared: R0.73

- Dividend yield: 3.27%

- Cash and equivalents: R283.979 million

- Cash and equivalents per share: R2.61

- Cash and equivalents makes up 11.7% of Spur's market capital

- Cash and equivalents makes up 27.3% of Spur's total assets

- Shareholders equity in Spur: R865.715 million

- Shareholders equity per share: R7.97

- So Spur is trading at 2.79 times its shareholders equity

- Cash generated from operations: R244.9 million

- Cash generated from operations per share: R2.25

Currently Rocomamas revenue is about 14.6% that of thegroup's biggest brand Spur Steak Ranches. So Rocomams is now a bigger contributor to Spur's revenues than John Dory's who only contributes 9.2% of the revenues that Spur Steak Ranches brings in. Rocomamas might soon bring in more revenues than Panarotti's and Casa Bela's combined

Spur's management commentary on the latest results

Spur Corporation posted a resilient performance for the year to 30 June 2019 as total franchised restaurant sales across the local and international operations increased by 7.2% to R7.6 billion. Trading conditions continue to be challenging in the low growth domestic market while the group’s international business was impacted by the weak economy and high operating costs in Australia. Franchised restaurant sales in South Africa grew by 6.2% as the group’s main middle-income customer base came under increasing pressure in the slowing economic climate.

The group’s trading results reported in this commentary exclude the Captain DoRegos chain which was sold with effect from 1 March 2018. In this constrained spending environment, management continues to focus on enhancing franchisee margins across the brands. Measures include expanding the range of “home-made” products manufactured in Spur restaurants, rationalising menu offerings in certain brands to promote efficiencies, renegotiating rentals and reducing the size of restaurants where appropriate. These factors are positively impacting franchisee margins and profitability, resulting in a more sustainable franchise business.

The group has embraced the call-and-collect and delivery models and experienced strong growth from third-party delivery services, such as Mr D Food and Uber Eats, across all brands. After increasing local restaurant sales by 11.3% and 1.3% in the first and second quarters of the financial year respectively, the group reported growth of 7.5% in the third quarter and 6.0% in the fourth quarter. Spur Steak Ranches increased restaurant sales by 5.4% for the year and by 4.2% in existing restaurants. Spur’s loyal customer base of over 1.2 million active adult Spur Family Card members is a key driver of sales growth. Franchisees’ commitment to the iconic Spur brand is evident in their investment of R80.2 million in new restaurants and the relocation or revamping of existing outlets over the past year.

Thirteen new Spur restaurants were opened, including three of the smaller format Spur Grill & Go outlets. Spur was ranked first in the Sunday Times Generation Next survey for the Coolest Eat Out Place for the 15th consecutive year and continues to be the largest retail brand in South Africa on Facebook and Twitter. Restaurant sales in Pizza and Pasta, incorporating Panarottis and Casa Bella, grew by 0.9% as the Panarottis chain continued to be impacted by aggressive discounting by competitors in the takeaway pizza market. In this environment, management has shifted the brand’s strategy away from discounting to focus on product quality and value. As anticipated by management, this had a negative impact on turnover in the short term.

Restaurant sales in RocoMamas grew by 7.5%. RocoMamas has been one of the fastest growing restaurant brands in the country’s casual dining sector and has a national footprint of 72 restaurants, complemented by 13 international outlets. An increased investment in marketing, including the first brand television commercial, saw RocoMamas return to positive existing business growth in the second half of the year, following a decline in the first half. The first two outlets for RocoGo, a smaller on-the-go concept, were opened and an additional outlet is planned for the new year. Further potential sites are being actively pursued.

John Dory’s increased restaurant sales by 4.6%, benefiting from the reopening of two major outlets which were temporarily closed due to shopping mall redevelopments. The Hussar Grill’s higher-income customers continue to be resilient in the economic downturn and the brand’s restaurant sales grew by 13.4%. The Hussar Grill has strengthened its positioning as the premium steakhouse brand in the Western Cape and has successfully expanded its presence into Gauteng.

The group acquired a 51% shareholding in the Nikos Coalgrill Greek chain, which comprised six restaurants at the effective date of 1 August 2018. Three outlets have been opened post-acquisition in Gauteng, including a smaller format restaurant in Rosebank (Johannesburg). The chain contributed franchised restaurant sales of R65.9 million for the 11 months since acquisition.

New restaurant openings contributed to international restaurant sales increasing by 12.3% on a constant exchange rate basis and by 16.2% in Rand terms. Trading in Africa, Mauritius and the Middle East remains strong, although trading in certain African countries including Namibia, Kenya and Lesotho has been slower. At a constant exchange rate, restaurant sales in Africa grew by 18.3% (49 outlets (2018: 38 outlets)), Mauritius by 21.2% (13 outlets (2018: 11 outlets)) and the Middle East by 80.6% (four outlets (2018: two outlets)). Restaurant trading conditions in Australia and New Zealand continue to be impacted by high operating costs, escalating rentals and declining disposable income, with sales in the region declining by 15.9% following the closure of three restaurants.

John Dory’s increased restaurant sales by 4.6%, benefiting from the reopening of two major outlets which were temporarily closed due to shopping mall redevelopments. The Hussar Grill’s higher-income customers continue to be resilient in the economic downturn and the brand’s restaurant sales grew by 13.4%. The Hussar Grill has strengthened its positioning as the premium steakhouse brand in the Western Cape and has successfully expanded its presence into Gauteng. The group acquired a 51% shareholding in the Nikos Coalgrill Greek chain, which comprised six restaurants at the effective date of 1 August 2018. Three outlets have been opened post-acquisition in Gauteng, including a smaller format restaurant in Rosebank (Johannesburg). The chain contributed franchised restaurant sales of R65.9 million for the 11 months since acquisition.

New restaurant openings contributed to international restaurant sales increasing by 12.3% on a constant exchange rate basis and by 16.2% in Rand terms. Trading in Africa, Mauritius and the Middle East remains strong, although trading in certain African countries including Namibia, Kenya and Lesotho has been slower. At a constant exchange rate, restaurant sales in Africa grew by 18.3% (49 outlets (2018: 38 outlets)), Mauritius by 21.2% (13 outlets (2018: 11 outlets)) and the Middle East by 80.6% (four outlets (2018: two outlets)).

Restaurant trading conditions in Australia and New Zealand continue to be impacted by high operating costs, escalating rentals and declining disposable income, with sales in the region declining by 15.9% following the closure of three restaurants.

Prospects

The group expects trading conditions to remain constrained in the short to medium term against the background of low economic growth, the weak labour market, fragile consumer confidence and continued pressure on household budgets from rising food, fuel and utility costs. In this environment, management will maintain its focus on tight cost management, excellent product quality and the profitability of franchisees.

Technology continues to disrupt our industry and we are pursuing several opportunities within our digital transformation strategy. In response to the significant demand by customers for cost-effective convenience, the group is planning to launch its own click-and-collect service in the year ahead to complement the services currently offered by third-party service providers. The group’s model will be more cost-effective than outsourced channels as well as being more customer-centric, ensuring a better service to customers while maintaining a direct relationship between the group’s brands and their customers. The group plans to open at least 11 restaurants in South Africa in the year ahead across all brands

.Ten new international restaurants are planned for the new year. These include three RocoMamas outlets in Saudi Arabia, two additional restaurants in each of Kenya and Nigeria, and one outlet in each of Mauritius, Zambia and Zimbabwe. While international expansion will continue to focus on countries where the group currently operates, new territories will be considered if the group is able to secure a local partner with the expertise, infrastructure and financial resources to open a set minimum number of franchised restaurants, and the local economic and political environment can support our presence.

Management continues to evaluate the operations in Australasia given the challenging trading conditions, high franchisee operating costs and financial losses being incurred in these countries.

The group’s trading results reported in this commentary exclude the Captain DoRegos chain which was sold with effect from 1 March 2018. In this constrained spending environment, management continues to focus on enhancing franchisee margins across the brands. Measures include expanding the range of “home-made” products manufactured in Spur restaurants, rationalising menu offerings in certain brands to promote efficiencies, renegotiating rentals and reducing the size of restaurants where appropriate. These factors are positively impacting franchisee margins and profitability, resulting in a more sustainable franchise business.

The group has embraced the call-and-collect and delivery models and experienced strong growth from third-party delivery services, such as Mr D Food and Uber Eats, across all brands. After increasing local restaurant sales by 11.3% and 1.3% in the first and second quarters of the financial year respectively, the group reported growth of 7.5% in the third quarter and 6.0% in the fourth quarter. Spur Steak Ranches increased restaurant sales by 5.4% for the year and by 4.2% in existing restaurants. Spur’s loyal customer base of over 1.2 million active adult Spur Family Card members is a key driver of sales growth. Franchisees’ commitment to the iconic Spur brand is evident in their investment of R80.2 million in new restaurants and the relocation or revamping of existing outlets over the past year.

Thirteen new Spur restaurants were opened, including three of the smaller format Spur Grill & Go outlets. Spur was ranked first in the Sunday Times Generation Next survey for the Coolest Eat Out Place for the 15th consecutive year and continues to be the largest retail brand in South Africa on Facebook and Twitter. Restaurant sales in Pizza and Pasta, incorporating Panarottis and Casa Bella, grew by 0.9% as the Panarottis chain continued to be impacted by aggressive discounting by competitors in the takeaway pizza market. In this environment, management has shifted the brand’s strategy away from discounting to focus on product quality and value. As anticipated by management, this had a negative impact on turnover in the short term.

Restaurant sales in RocoMamas grew by 7.5%. RocoMamas has been one of the fastest growing restaurant brands in the country’s casual dining sector and has a national footprint of 72 restaurants, complemented by 13 international outlets. An increased investment in marketing, including the first brand television commercial, saw RocoMamas return to positive existing business growth in the second half of the year, following a decline in the first half. The first two outlets for RocoGo, a smaller on-the-go concept, were opened and an additional outlet is planned for the new year. Further potential sites are being actively pursued.

John Dory’s increased restaurant sales by 4.6%, benefiting from the reopening of two major outlets which were temporarily closed due to shopping mall redevelopments. The Hussar Grill’s higher-income customers continue to be resilient in the economic downturn and the brand’s restaurant sales grew by 13.4%. The Hussar Grill has strengthened its positioning as the premium steakhouse brand in the Western Cape and has successfully expanded its presence into Gauteng.

The group acquired a 51% shareholding in the Nikos Coalgrill Greek chain, which comprised six restaurants at the effective date of 1 August 2018. Three outlets have been opened post-acquisition in Gauteng, including a smaller format restaurant in Rosebank (Johannesburg). The chain contributed franchised restaurant sales of R65.9 million for the 11 months since acquisition.

New restaurant openings contributed to international restaurant sales increasing by 12.3% on a constant exchange rate basis and by 16.2% in Rand terms. Trading in Africa, Mauritius and the Middle East remains strong, although trading in certain African countries including Namibia, Kenya and Lesotho has been slower. At a constant exchange rate, restaurant sales in Africa grew by 18.3% (49 outlets (2018: 38 outlets)), Mauritius by 21.2% (13 outlets (2018: 11 outlets)) and the Middle East by 80.6% (four outlets (2018: two outlets)). Restaurant trading conditions in Australia and New Zealand continue to be impacted by high operating costs, escalating rentals and declining disposable income, with sales in the region declining by 15.9% following the closure of three restaurants.

John Dory’s increased restaurant sales by 4.6%, benefiting from the reopening of two major outlets which were temporarily closed due to shopping mall redevelopments. The Hussar Grill’s higher-income customers continue to be resilient in the economic downturn and the brand’s restaurant sales grew by 13.4%. The Hussar Grill has strengthened its positioning as the premium steakhouse brand in the Western Cape and has successfully expanded its presence into Gauteng. The group acquired a 51% shareholding in the Nikos Coalgrill Greek chain, which comprised six restaurants at the effective date of 1 August 2018. Three outlets have been opened post-acquisition in Gauteng, including a smaller format restaurant in Rosebank (Johannesburg). The chain contributed franchised restaurant sales of R65.9 million for the 11 months since acquisition.

New restaurant openings contributed to international restaurant sales increasing by 12.3% on a constant exchange rate basis and by 16.2% in Rand terms. Trading in Africa, Mauritius and the Middle East remains strong, although trading in certain African countries including Namibia, Kenya and Lesotho has been slower. At a constant exchange rate, restaurant sales in Africa grew by 18.3% (49 outlets (2018: 38 outlets)), Mauritius by 21.2% (13 outlets (2018: 11 outlets)) and the Middle East by 80.6% (four outlets (2018: two outlets)).

Restaurant trading conditions in Australia and New Zealand continue to be impacted by high operating costs, escalating rentals and declining disposable income, with sales in the region declining by 15.9% following the closure of three restaurants.

Prospects

The group expects trading conditions to remain constrained in the short to medium term against the background of low economic growth, the weak labour market, fragile consumer confidence and continued pressure on household budgets from rising food, fuel and utility costs. In this environment, management will maintain its focus on tight cost management, excellent product quality and the profitability of franchisees.

Technology continues to disrupt our industry and we are pursuing several opportunities within our digital transformation strategy. In response to the significant demand by customers for cost-effective convenience, the group is planning to launch its own click-and-collect service in the year ahead to complement the services currently offered by third-party service providers. The group’s model will be more cost-effective than outsourced channels as well as being more customer-centric, ensuring a better service to customers while maintaining a direct relationship between the group’s brands and their customers. The group plans to open at least 11 restaurants in South Africa in the year ahead across all brands

.Ten new international restaurants are planned for the new year. These include three RocoMamas outlets in Saudi Arabia, two additional restaurants in each of Kenya and Nigeria, and one outlet in each of Mauritius, Zambia and Zimbabwe. While international expansion will continue to focus on countries where the group currently operates, new territories will be considered if the group is able to secure a local partner with the expertise, infrastructure and financial resources to open a set minimum number of franchised restaurants, and the local economic and political environment can support our presence.

Management continues to evaluate the operations in Australasia given the challenging trading conditions, high franchisee operating costs and financial losses being incurred in these countries.

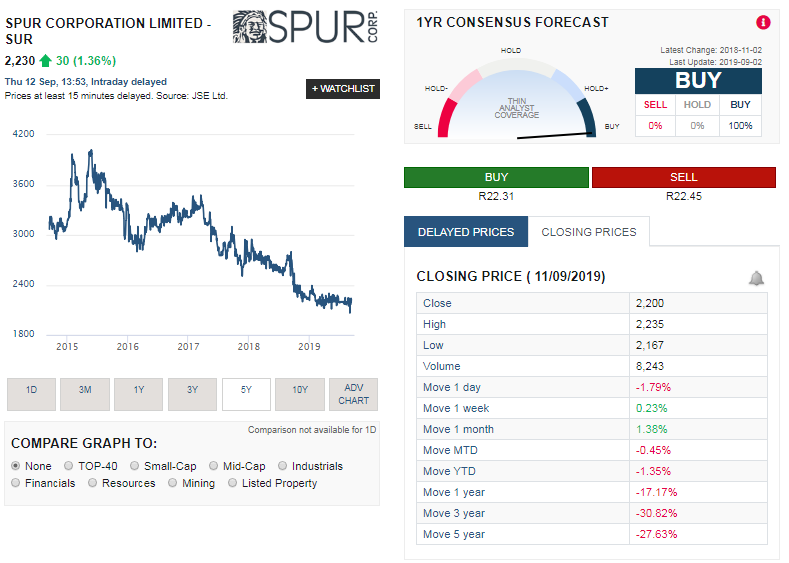

Share price performance

The image below, taken from Sharenet, shows the share price history of Spur Corporation over the last 5 years. And its been a slow and steady decline in the group's share price, a reflection of the difficult environment it is operating in. The summary below shows the share price performance of Spur over various time periods

Valuation of Spur (SUR) shares

Based on Spur's latest financial results, their strong revenue growth, their strong brands, their solid cash on balance sheet and cash generating ability our valuation models (largely based on dividend discount and discounted cash flow models) sets a full value price of R27.20 for Spur. We therefore believe the group is undervalued at its current price.