|

Related Topics |

|

In our continued efforts to provide readers with a broad range of views regarding South Africa's economy, we take a look at the latest quarterly bulletin published by the South African Reserve Bank, and review some of the data and graphics contained within their 4th quarter 2019 quarterly bulletin.

|

|

South African Reserve Bank surprises with 100 basis points cut in the REPO rate

With the South African Reserve Bank (SARB) surprising economists and market commentators with a significant 100 basis point cut in the REPO rate at their last monetary policy committee meeting to try and provide relief to consumers and attempting to provide some relief to the economy and markets struggling with the effects of the Coronavirus and lockdowns of countries across the world, lets take a look at the SARB's view of the South African and global economy for the 4th quarter of 2019, which is the last quarter that is untainted by the Coronavirus. Since the start of the 1st quarter of 2020 Coronavirus (Covid-19) has dominated world headlines and financial markets. Below the introduction of the 4th quarter 2019 Quarterly Bulletin

Global economic developments

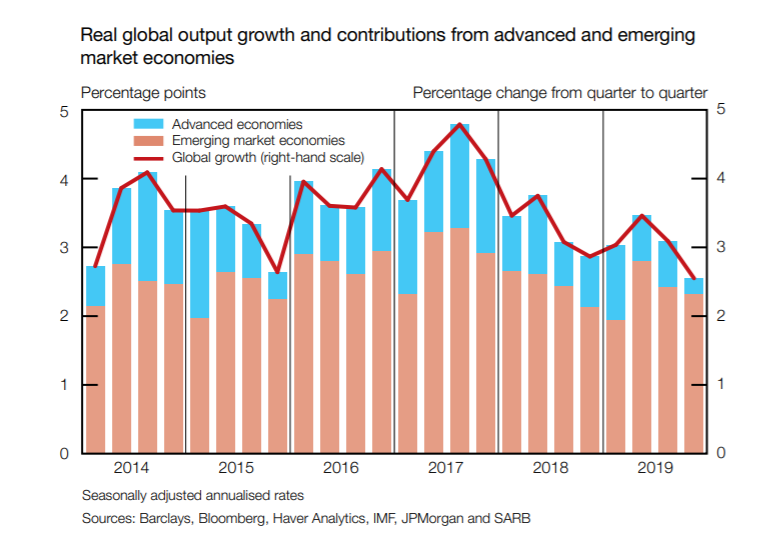

Global economic growth slowed to 2.5% in the fourth quarter of 2019 from an annualised real rate of 3.1% in the third quarter, and to an annual average of 3.0% in 2019 – the weakest pace of economic expansion since the 2007–08 global financial crisis. The slowdown in the fourth quarter reflected a sharp deceleration in the real economic growth momentum of advanced economies and a moderation in emerging markets

Most advanced economies, with the exception of the United States (US), recorded weaker economic growth in the fourth quarter of 2019. Real output growth in the US stabilised at 2.1% in the fourth quarter, supported by personal consumption expenditure and government spending. In addition, the sharp decline in imports by the US, partly due to higher tariffs on Chinese goods, contributed 1.3 percentage points to overall growth.

Global inflation remains muted

Global inflation remained muted in the fourth quarter of 2019. In advanced economies, headline consumer price inflation continued to undershoot most central banks’ inflation targets. Inflationary pressures in emerging markets also remained well contained, with the exception of a few countries such as Argentina and Turkey. World trade volumes (using exports as a proxy) declined for the seventh consecutive month in December 2019, at a year-on-year rate (three-month moving average) of 0.5%, as trade tensions continued to weigh on sentiment.

Declines in trade volumes were especially pronounced in emerging markets where export volumes contracted by 1.2% over this period, mainly due to lower exports from Africa and the Middle East as well as Latin America and emerging Asia (excluding China). Meanwhile, exports from advanced economies stabilised in December as lower exports from the US, Japan and the euro area were offset by higher exports from other advanced economies.

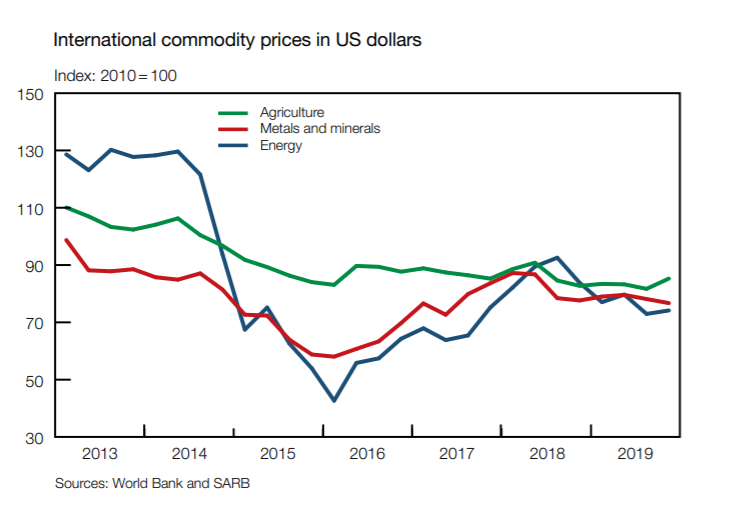

The international prices of agricultural products and energy rose modestly in the fourth quarter of 2019, while the prices of metals and minerals declined further. The price of Brent crude oil rose from around US$58 per barrel in the beginning of October 2019 to a high of US$69 per barrel in early January 2020 amid optimism that a US–China trade deal would boost global economic growth prospects. In mid-February, oil prices decreased sharply to US$53 per barrel due to concerns that the outbreak of the coronavirus disease 2019 (COVID-19) would reduce world growth prospects. Oil prices declined further in early March as the virus spread to several countries across the world. The Organization of the Petroleum Exporting Countries (OPEC) subsequently decided to cut production. Russia, however, refused to join OPEC’s production cut and oil prices initially dropped by 10%. Saudi Arabia then announced that it would boost production and oil prices declined further by almost 30% to US$31 per barrel in mid-March.

Declines in trade volumes were especially pronounced in emerging markets where export volumes contracted by 1.2% over this period, mainly due to lower exports from Africa and the Middle East as well as Latin America and emerging Asia (excluding China). Meanwhile, exports from advanced economies stabilised in December as lower exports from the US, Japan and the euro area were offset by higher exports from other advanced economies.

The international prices of agricultural products and energy rose modestly in the fourth quarter of 2019, while the prices of metals and minerals declined further. The price of Brent crude oil rose from around US$58 per barrel in the beginning of October 2019 to a high of US$69 per barrel in early January 2020 amid optimism that a US–China trade deal would boost global economic growth prospects. In mid-February, oil prices decreased sharply to US$53 per barrel due to concerns that the outbreak of the coronavirus disease 2019 (COVID-19) would reduce world growth prospects. Oil prices declined further in early March as the virus spread to several countries across the world. The Organization of the Petroleum Exporting Countries (OPEC) subsequently decided to cut production. Russia, however, refused to join OPEC’s production cut and oil prices initially dropped by 10%. Saudi Arabia then announced that it would boost production and oil prices declined further by almost 30% to US$31 per barrel in mid-March.

Local economic developments

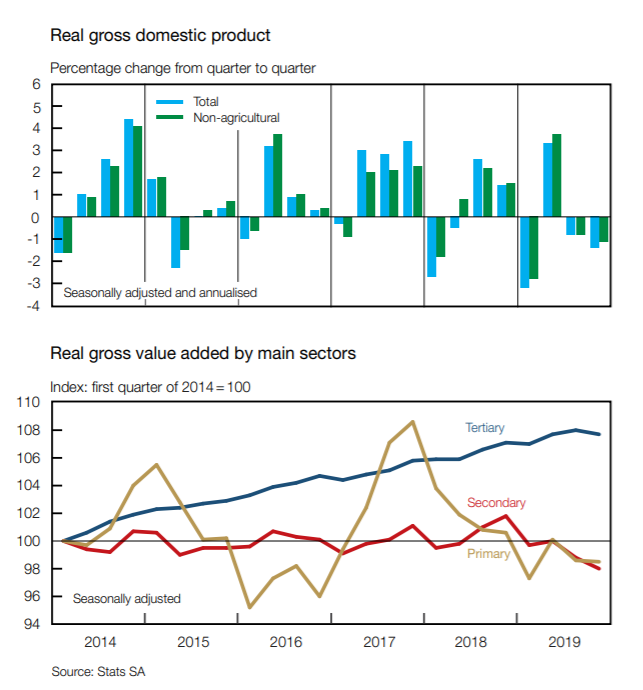

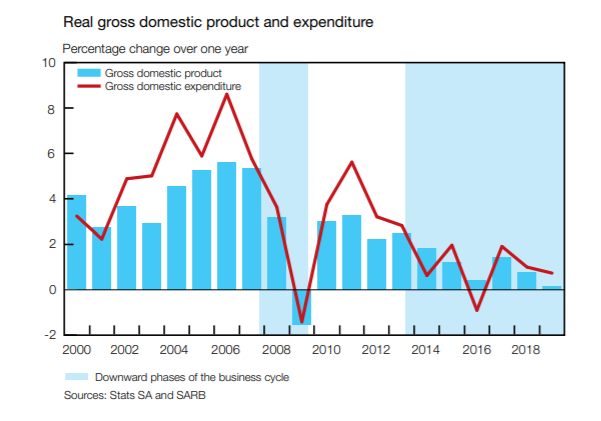

The South African economy entered a technical recession as real gross domestic product (GDP) contracted further at an annualised rate of 1.4% in the fourth quarter of 2019, following a contraction of 0.8% in the third quarter. This is the second time that output has contracted for two successive quarters since the first quarter of 2018. Economic activity decreased in the primary, secondary and tertiary sectors in the fourth quarter of 2019

When excluding the contribution of the generally more weather-reliant agricultural sector, the non-agricultural sector contracted by a lesser 1.1% in the fourth quarter of 2019. Annual output growth slowed significantly from a high of 3.3% in 2011 to only 0.2% in 2019 – the lowest growth rate since the sharp contraction in 2009 following the global financial crisis. Annual growth in real GDP only averaged 1.0% in the current downward phase of the business cycle compared with 2.8% during the previous short upward phase. The further moderation in annual real GDP growth in 2019 reflected a contraction in output in all but the second quarter, and in both the primary and the secondary sectors along with a slowdown in the tertiary sector.

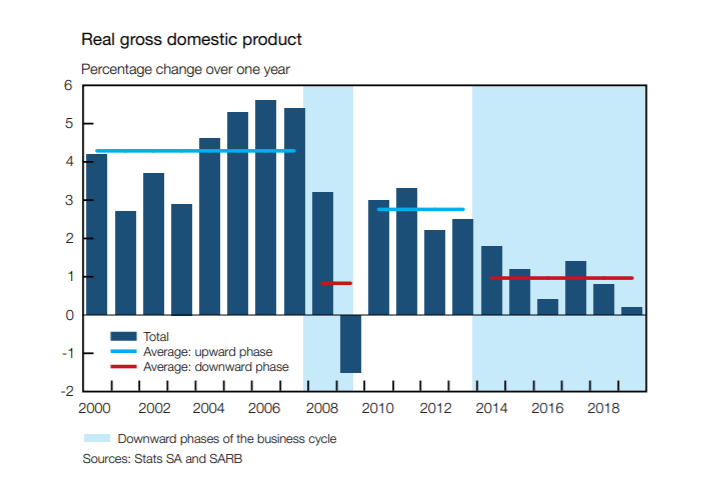

The image above shows just how long and protracted South Africa's economic downward phase has been. Ever since the great recession brought about by the sub prime lending crisis in the United States in 2008/2009 the South African economy has struggled to get any sort of traction and momentum. And this has placed significant pressure on the fiscus of the South African government (read more about South Africa's fiscal policy here), as the population keeps growing, demand for government social grants and services keeps growing but the taxes collected fro the South African economy can't keep up with the growth in demand for services from government. Government's way out of this has been to borrow more and more, but the bill comes due at some point. And the greater the drag on South Africa's fiscal resources the higher the premium (yield) the South African government has to pay to lure investors to borrow them money. And this model is not sustainable in the long run so it crucial that government gets the economy going and growing, for its own fiscal well being.

Real gross domestic expenditure

Real gross domestic expenditure (GDE) decreased by a further 4.6% in the fourth quarter of 2019 following a decrease of 4.5% in the third quarter. Both real gross fixed capital formation and real final consumption expenditure by general government reverted from an increase in the third quarter of 2019 to a contraction in the fourth quarter, alongside a much faster pace of deaccumulation in real inventory holdings. The real final consumption expenditure by households increased somewhat over the period. For 2019 as a whole, the pace of expansion in real GDE moderated slightly to 0.7%, from 1.0% in 2018. Annual growth in real GDE has exceeded that in real GDP on 16 occasions since 2000, as the demand for goods and services exceeded the production thereof.

While gross domestic expenditure's growth has exceeded that of gross domestic product the downward trend in the annual growth rate of both GDP and GDE is obvious and very similar in nature.

Household debt in South Africa

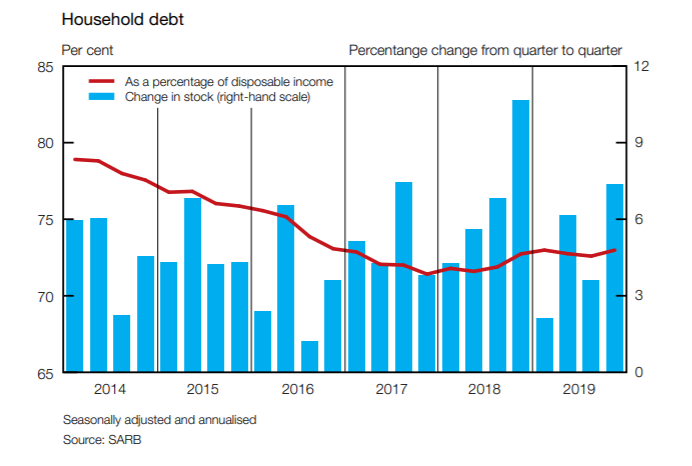

The pace of household debt accumulation accelerated in the fourth quarter of 2019 due to faster growth in the extension of mortgage advances (which includes mortgage securitisation) as well as leasing finance and instalment sale loans. Consequently, growth in household debt exceeded that in disposable income, with the ratio of household debt to nominal disposable income increasing marginally to 73.0% in the fourth quarter of 2019, from 72.6% in the third quarter. Households’ cost of servicing debt as a percentage of nominal disposable income remained unchanged at 9.4% in both the third and fourth quarter of 2019. Growth in household debt accelerated marginally from 5.5% in 2018 to 5.7% in 2019. Household debt as a percentage of nominal disposable income increased from 72.0% to 72.8% over the same period, as the annual increase in household debt exceeded that in household nominal disposable income. Likewise, households’ cost of servicing debt relative to disposable income inched higher from 9.2% to 9.4% over the same period.

Households’ net wealth increased in the fourth quarter of 2019 as the increase in the value of equity portfolios and housing stock exceeded that in household debt. The ratio of net wealth to nominal disposable income rose slightly to 359.5% in the fourth quarter of 2019 from 359.1% in the previous quarter, and declined in 2019 as a whole, as the increase in nominal disposable income exceeded that in wealth.

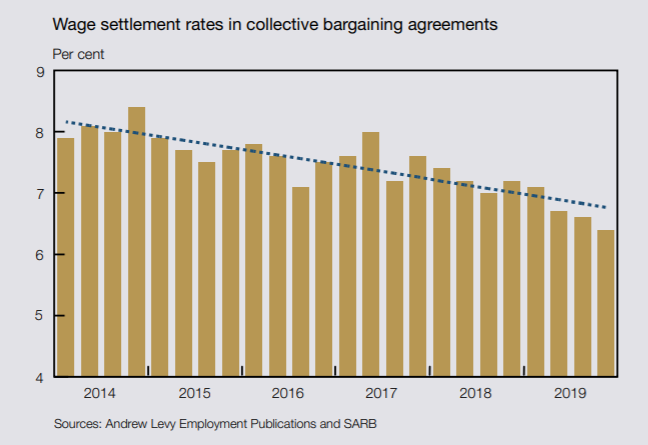

Slow down in wage settlement rates

With real gross domestic expenditure slowing an household debt picking up pace, lets take a look at the wage settlement rates (pay increases) overt time.

The slowdown in nominal wage and income growth observed in the official statistics in recent years is corroborated by the decline in the average wage settlement rate in collective bargaining agreements. These settlements reflect annual wage increases and exclude bonuses and overtime payments. This measure provides an indication of wage increases for employees who are part of the surveyed collective bargaining units but excludes centralised bargaining agreements through sectoral bargaining councils. The average wage settlement rate moderated from a peak of 8.4% in the fourth quarter of 2014 to 6.4% in the fourth quarter of 2019.

Our expectation is that with the Coronavirus playing havoc with world economies, we expect companies to cut back on wage settlements even more, and to make matters worse for consumers in South Africa, we expect the unemployment rate to skyrocket in South Africa in coming weeks and months.

Our expectation is that with the Coronavirus playing havoc with world economies, we expect companies to cut back on wage settlements even more, and to make matters worse for consumers in South Africa, we expect the unemployment rate to skyrocket in South Africa in coming weeks and months.

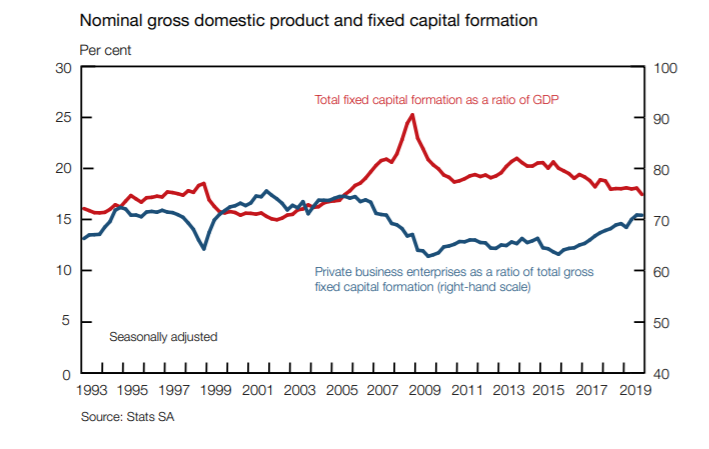

Gross fixed capital formation in South Africa

Real gross fixed capital outlays by private business enterprises decreased by 10.3% in the fourth quarter of 2019 following robust growth in the previous two quarters. Capital expenditure on transport equipment, construction works as well as machinery and other equipment receded. In 2019, growth in real gross fixed capital formation by private business enterprises slowed to 1.1%, from 2.1% in 2018. The private sector’s share of total nominal gross fixed capital formation nevertheless increased slightly from 68.5% in 2018 to 70.0% in 2019, as budget constraints negatively impacted capital spending by public corporations and general government.

Real gross fixed capital expenditure by the public sector decreased for a third consecutive quarter in the fourth quarter of 2019, especially due to the lower capital expenditure by general government. Gross fixed capital formation by public corporations contracted anew by 0.3% in the fourth quarter of 2019 after increasing marginally by a revised 0.7% in the third quarter. The slight increase in capital outlays on transport equipment was outweighed by lower capital spending on all the other asset types, most notably on construction works and on machinery and equipment. Real capital spending by general government receded notably further by 17.6% in the fourth quarter of 2019 following a marked decline of 15.6% in the third quarter, as all three spheres of government reduced capital outlays in the fourth quarter.

Gross fixed capital formation by general government – constituting 15.1% of total fixed investment in 2019 – has contracted consistently over the past two years, declining by 4.4% in 2018 and a further 8.9% in 2019.

Gross fixed capital formation by general government – constituting 15.1% of total fixed investment in 2019 – has contracted consistently over the past two years, declining by 4.4% in 2018 and a further 8.9% in 2019.

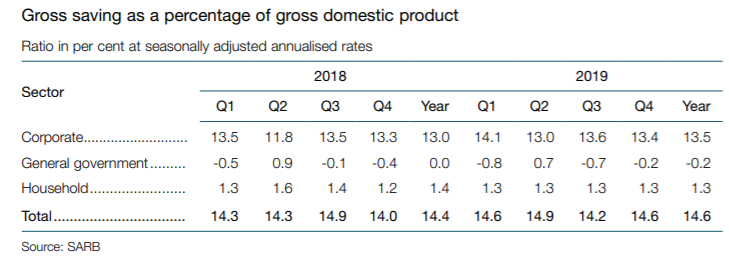

Gross nominal savings in South Africa

The national saving rate (gross saving as a percentage of nominal GDP) increased from 14.2% in the third quarter of 2019 to 14.6% in the fourth quarter, mainly due to a smaller dissaving by general government

Gross saving by the corporate sector as a percentage of GDP decreased from 13.6% in the third quarter of 2019 to 13.4% in the fourth quarter, while that of general government improved to a dissaving of 0.2% in the fourth quarter of 2019 from a dissaving of 0.7% in the third quarter. The increase in seasonally adjusted government revenue from income tax, fuel levy and excise duties exceeded that in government’s nominal expenditure in the fourth quarter. Gross saving by the household sector as a percentage of GDP remained unchanged at 1.3% in the fourth quarter of 2019, as the increase in nominal consumption expenditure more or less equalled that in nominal disposable income