South African Reserve Bank, Monetary Policy Review, April 2022

|

Category: Economics, Inflation, Monetary Policy

Date: 14 September 2022 On a bi-annual basis the South African Reserve Bank, or SARB in short publishes a monetary policy review. According to SARB, "The Monetary Policy Review (MPR) is published twice a year and is aimed at broadening the public’s understanding of the objectives and conduct of monetary policy. The MPR covers domestic and international developments that affect the monetary policy stance. "

Instead of publishing the full monetary policy review we take out the best parts and make it available on this site. |

SARB Monetary Policy Review

|

Monetary Policy Review April 2022, highlights

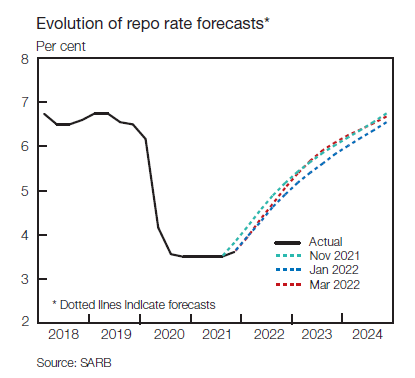

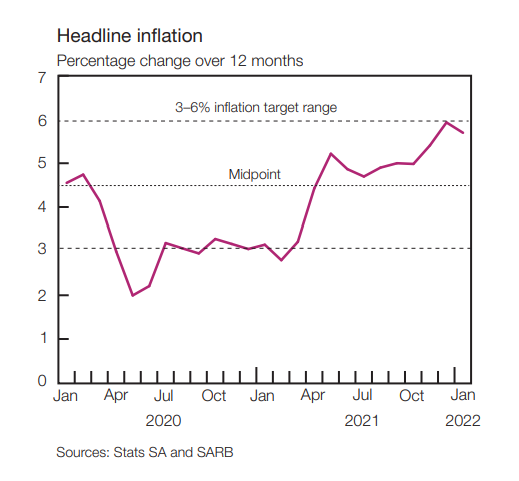

In response to rising inflation and a closing output gap, the Monetary Policy Committee (MPC) has raised the repurchase (repo) rate by a cumulative 75 basis points since the previous edition of the Monetary Policy Review (MPR), bringing it to 4.25%. The policy stance remained strongly supportive of the economic recovery over the six-month period under review. By the fourth quarter of 2021, the economy had recovered to above 98% of the 2019 gross domestic product (GDP) level. Economic growth this year is expected to be somewhat stronger than previously forecast on stronger commodity export prices. Headline inflation, however, rose sharply from 5% in September 2021 to 5.9% in December, before moderating somewhat. Inflation was pushed higher by large increases in fuel and food prices amid a more modest pickup in core inflation. Headline inflation is expected to average 5.8% in 2022, well above the 4.9% forecasted in January this year, and with risks tilted to the upside. Global economic activity rebounded sharply over the past year, led by advanced economies and underpinned by ample policy support and progress made with COVID-19 vaccinations. Emerging market economies recovered at a slower pace than advanced economies, and for many of them activity remains somewhat below 2019 levels.

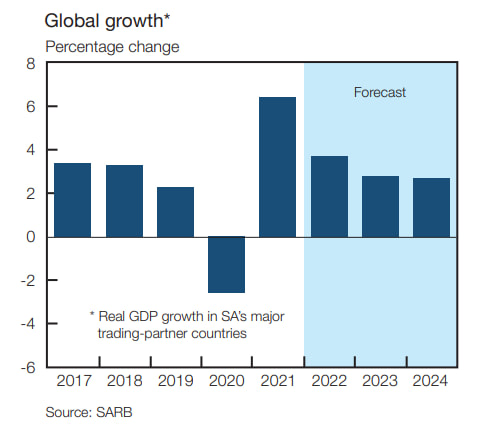

Persistent supply constraints and robust demand growth at a global level, however, continue to give strong impetus to inflation, which accelerated rapidly in a wide range of countries, both advanced and emerging. As a result, policy tightening has been expected for some time. In this complex environment, economic uncertainty spiked in February 2022 with the Russian invasion of Ukraine. Oil prices rose sharply to above US$130 per barrel in early March before retreating somewhat, followed by wheat and other grains prices. Higher input prices and disruptions to global trade have increased downside risks to global growth and raised forecasts for global inflation. The South African Reserve Bank (SARB) expects global growth to decelerate sharply to 3.7% in 2022, down from an estimated 6.4% in 2021, and to remain modest over the medium term. Up until February, the foremost risk to global growth in 2022 was an acute rise and then progressively non-transitory inflation.1 Inflation was given impetus by the massive fiscal support provided by advanced economies, an accumulation of household savings, and expansive monetary conditions which led to a surge in demand for consumer goods as restrictions eased.

Persistent supply constraints and robust demand growth at a global level, however, continue to give strong impetus to inflation, which accelerated rapidly in a wide range of countries, both advanced and emerging. As a result, policy tightening has been expected for some time. In this complex environment, economic uncertainty spiked in February 2022 with the Russian invasion of Ukraine. Oil prices rose sharply to above US$130 per barrel in early March before retreating somewhat, followed by wheat and other grains prices. Higher input prices and disruptions to global trade have increased downside risks to global growth and raised forecasts for global inflation. The South African Reserve Bank (SARB) expects global growth to decelerate sharply to 3.7% in 2022, down from an estimated 6.4% in 2021, and to remain modest over the medium term. Up until February, the foremost risk to global growth in 2022 was an acute rise and then progressively non-transitory inflation.1 Inflation was given impetus by the massive fiscal support provided by advanced economies, an accumulation of household savings, and expansive monetary conditions which led to a surge in demand for consumer goods as restrictions eased.

SA Headline inflation

10 major industries in SA economy

|

Global growth forecast

|

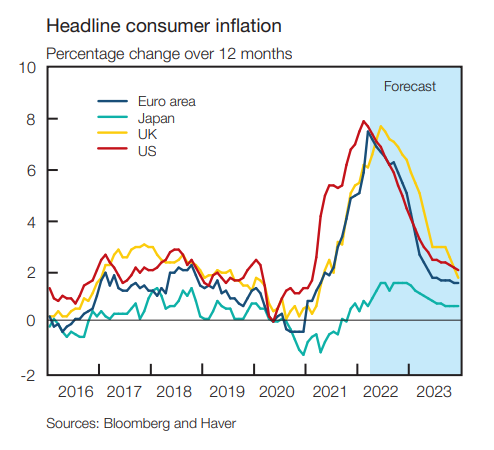

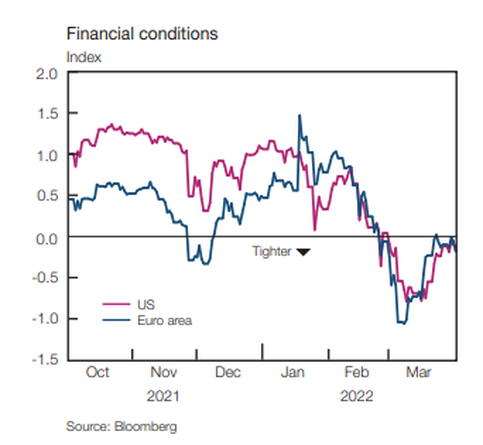

The supply response, however, remained constrained due to supply chain bottlenecks and COVID-19 restrictions that affected production activity. Price pressures further emanated from the tightening in labour markets in some advanced economies (e.g. the United States (US) and the United Kindom (UK)), and sharply higher oil and global food prices. Major emerging markets, particularly Brazil, Mexico and Turkey, also experienced markedly higher inflation from fuel and food, though demand pressures were also evident. For other emerging markets, such as South Africa, the inflation build-up was less pronounced early in the recovery period but has ramped up quickly over the past year. In response to climbing inflation and its increasingly less transitory features, the major global central banks moved faster to normalise rates. The US Federal Reserve (Fed) raised the federal funds rate by 25 basis points in March after two years of rates remaining at the effective zero lower bound. Meanwhile, the Bank of England has raised its policy rate three times since December 2021, bringing it to 0.75% in March 2022.2 For emerging markets, pressure on policy rates has also increased with inflation and heightened risk to capital flows and exchange rates.

Inflation across the globe |

Financial conditions in US and Euro zone |

|

|

Domestic Outlook

The domestic economy grew by 4.9% in 2021 – its fastest pace of growth since 2007 – after the sharp contraction of 6.4% in 2020. This brought South Africa’s GDP to within 2 percentage points of the 2019 level. This was achieved despite the recovery being temporarily derailed by the steep decline in GDP (1.7% quarter on quarter, seasonally adjusted) during the third quarter of 2021, prompted by the July riots in KwaZulu-Natal and Gauteng, among other factors. The economy would have surpassed pre-COVID-19 economic output in the first quarter of 2022 had the third quarter’s events not transpired.3 The economy’s recovery from the pandemic has featured a gradual resumption of consumption spending, a return to positive private investment growth, and sustained, robust terms of trade gains from high global commodity export prices. Fiscal and monetary policy have been strongly accommodative, adding directly to demand and reducing debt-service costs to ease borrowers’ cash flow and encourage more credit demand. Spending by households also benefitted from the rebound in wages, a recovery in asset prices as well as increased social transfers.

While the recovery of the economy has progressed well, the pandemic has scarred some sectors severely. The most impacted are the construction, transport and trade sectors which remain well below 2019 output levels. As these are more labour-intensive sectors, reduced output levels help explain why overall employment levels have yet to recover. Some firms appear to have delayed re-hiring as sales have been slow, while others may have achieved efficiency gains. At the aggregate sector level, the primary sector has expanded beyond its 2019 size, benefitting from favourable weather conditions (agriculture) and elevated global commodity prices (mining). The secondary sector, at 90% of its 2019 output level, remains furthest behind.

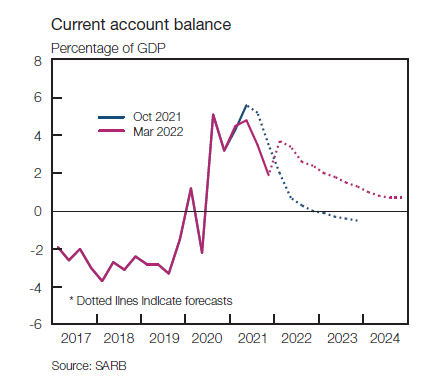

The tertiary sector has surpassed its 2019 output level, despite persistent weakness in transport and trade activity. These two subsectors are expected to rebound as the pandemic fades and help to boost employment. However, inadequate electricity supply remains a serious drag on growth and impedes the contribution of demand to the economy. South Africa’s trajectory through the pandemic and into the recovery phase has demonstrated the overall macroeconomic resilience of the economy – benefiting from the terms of trade despite globally weak output, and able to partially finance higher public spending through greater saving and drawing on external assets. This resilience is perhaps best displayed in the external balances, particularly the current account, which shows the net borrowing needs of the economy given a specific level of spending by households, firms and the public sector. As demand slowed into the pandemic, savings by corporates and households surged, helping drive the current account into surplus, and together with revenue windfalls, provided relatively heap financing to public spending. The current account, which reached 3.7% of GDP in 2021, supported the rand, and contributed to less inflationary pressure than had been expected when the crisis first unfolded. The recent resurgence in commodity export prices could prolong the surplus until 2024, even as imports continue to recover. Despite borrowing requirements remaining high, South Africa’s fiscal ratios improved markedly, underpinned by the revenue recovery and commodity windfalls. Public debt is now projected to stabilise at 75.1% of GDP in 2024/25, 3 percentage points lower than the projection in the 2021 Medium Term Budget Policy Statement (MTBPS).

A permanent reduction in fiscal risk should, all other things being equal, lower long-term borrowing costs, in turn supporting investment. The achievement of fiscal targets remains sensitive to additional support to state-owned enterprises, growth of the public sector wage bill, and the introduction of new and permanent spending streams funded by temporary revenues.

Unlike in the recovery phase, the growth outlook now is more subdued, as deep-seated structural constraints are expected to limit realised and potential growth. The economy is expected to grow at an annual average rate of 1.9%, while potential is much weaker at 0.9% over the outlook period. Despite medium-term growth remaining disappointingly low, the economy is expanding faster than potential, resulting in the output gap closing a little faster and disinflationary pressures moderating further, as seen in the trajectory of core inflation.

While the recovery of the economy has progressed well, the pandemic has scarred some sectors severely. The most impacted are the construction, transport and trade sectors which remain well below 2019 output levels. As these are more labour-intensive sectors, reduced output levels help explain why overall employment levels have yet to recover. Some firms appear to have delayed re-hiring as sales have been slow, while others may have achieved efficiency gains. At the aggregate sector level, the primary sector has expanded beyond its 2019 size, benefitting from favourable weather conditions (agriculture) and elevated global commodity prices (mining). The secondary sector, at 90% of its 2019 output level, remains furthest behind.

The tertiary sector has surpassed its 2019 output level, despite persistent weakness in transport and trade activity. These two subsectors are expected to rebound as the pandemic fades and help to boost employment. However, inadequate electricity supply remains a serious drag on growth and impedes the contribution of demand to the economy. South Africa’s trajectory through the pandemic and into the recovery phase has demonstrated the overall macroeconomic resilience of the economy – benefiting from the terms of trade despite globally weak output, and able to partially finance higher public spending through greater saving and drawing on external assets. This resilience is perhaps best displayed in the external balances, particularly the current account, which shows the net borrowing needs of the economy given a specific level of spending by households, firms and the public sector. As demand slowed into the pandemic, savings by corporates and households surged, helping drive the current account into surplus, and together with revenue windfalls, provided relatively heap financing to public spending. The current account, which reached 3.7% of GDP in 2021, supported the rand, and contributed to less inflationary pressure than had been expected when the crisis first unfolded. The recent resurgence in commodity export prices could prolong the surplus until 2024, even as imports continue to recover. Despite borrowing requirements remaining high, South Africa’s fiscal ratios improved markedly, underpinned by the revenue recovery and commodity windfalls. Public debt is now projected to stabilise at 75.1% of GDP in 2024/25, 3 percentage points lower than the projection in the 2021 Medium Term Budget Policy Statement (MTBPS).

A permanent reduction in fiscal risk should, all other things being equal, lower long-term borrowing costs, in turn supporting investment. The achievement of fiscal targets remains sensitive to additional support to state-owned enterprises, growth of the public sector wage bill, and the introduction of new and permanent spending streams funded by temporary revenues.

Unlike in the recovery phase, the growth outlook now is more subdued, as deep-seated structural constraints are expected to limit realised and potential growth. The economy is expected to grow at an annual average rate of 1.9%, while potential is much weaker at 0.9% over the outlook period. Despite medium-term growth remaining disappointingly low, the economy is expanding faster than potential, resulting in the output gap closing a little faster and disinflationary pressures moderating further, as seen in the trajectory of core inflation.

Current Account Balance

|

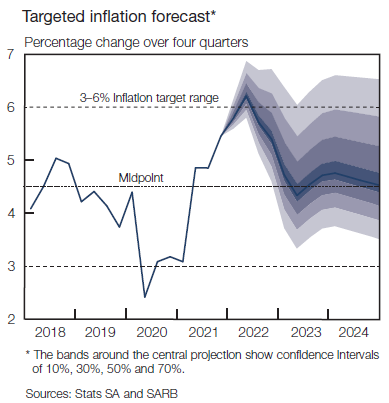

Targeted inflation forecast

|

South Africa’s inflation rate shifted markedly higher during the period under review, underpinned by soaring fuel prices and elevated food inflation, with rising core inflation adding to pressures, though from a low base. After averaging 4.5% in 2021, up from 3.3% in 2020, headline consumer price index (CPI) inflation is projected at 5.8% in 2022 (4.2% in the previous MPR). Administered price inflation (12.2% in 2022) will again exert upward pressure on headline inflation, having risen persistently above the upper limit of the inflation target range. In contrast with headline inflation, core inflation has remained subdued since the release of the previous MPR, kept down by unusually low insurance price inflation and despite a broad rise in services prices from low levels. Core inflation averaged 3.1% in 2021, down from 3.3% in 2020, before increasing to a projected 3.7% in the first quarter of this year. Sharply higher imported inflation and the closing output gap are forecast to lift core inflation to 4.2% in 2022 and 5.0% in 2023, before receding somewhat to 4.7% in 2024.

Looking ahead, domestic inflation could surprise higher if the hostilities in Ukraine continue to intensify or if oil and gas supplies are additionally constrained. The upward drift in inflation expectations and sharply higher producer prices further tilt the inflation risk to the upside.10 Higher expected wage growth, a somewhat weaker rand and further advances in global goods prices could exert additional upward pressure on headline inflation.

Looking ahead, domestic inflation could surprise higher if the hostilities in Ukraine continue to intensify or if oil and gas supplies are additionally constrained. The upward drift in inflation expectations and sharply higher producer prices further tilt the inflation risk to the upside.10 Higher expected wage growth, a somewhat weaker rand and further advances in global goods prices could exert additional upward pressure on headline inflation.

South Africa's REPO rate forecast evolution