|

Related Topics |

|

We take a look at the latest quarterly economic review from the South African Reserve Bank as contained in their latest quarterly bulletin covering quarter 1 of 2019. So what does the South African Reseve Bank, the authority responsible for South Africa's monetary policy have to say about South Africa's economy?

Note from this point forward all text and images are as received from the South African Reserve Bank quarterly bulletin |

|

Quarter 1, 2019 economic review

Global economic growth accelerated marginally to 3.3% in the first quarter of 2019 following a subdued second half of 2018. The quickening in output growth was fairly broad-based among the advanced economies, and was led by the United States (US). Real economic activity also increased at a faster pace in some major emerging market economies, such as China and Turkey, in the first quarter of 2019, while contracting in others. However, world trade volumes decreased in the opening quarter of 2019 as the notable decline in the export volumes of emerging markets reflected the impact of ongoing international trade tensions.

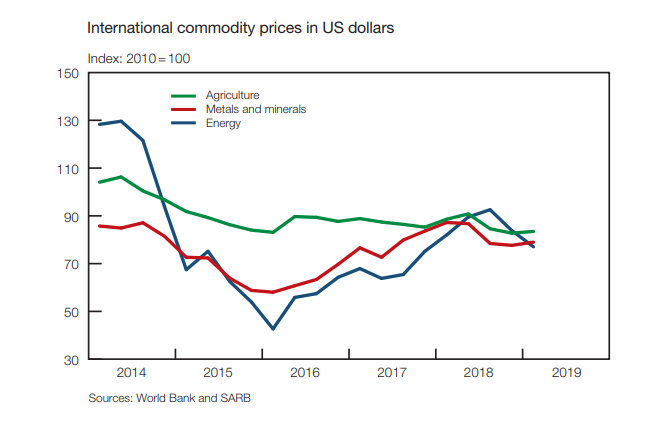

Consumer price inflation in the major advanced economies remained broadly below central bank targets in the first quarter of 2019, despite tightening labour markets, while inflationary pressures generally eased in emerging market economies. The international prices of agricultural commodities as well as metals and minerals increased marginally in the first quarter of 2019, while energy prices decreased further. Although the price of Brent crude oil declined on a quarter-to-quarter average basis in the first quarter of 2019, it increased from below US$50 per barrel at the end of December 2018 to around US$74 per barrel by mid-May 2019. Oil prices subsequently declined significantly to around US$62 per barrel in early June on concerns that US–China trade tensions would weigh on demand.

In South Africa, the first quarter of 2019 was characterised by severe electricity-supply disruptions, continued weak business confidence and caution ahead of the national elections in May. Real gross domestic product (GDP) contracted sharply by an annualised 3.2% in the first quarter of 2019 – the largest decrease since the first quarter of 2009 – but remained unchanged when measured over four quarters. The contraction was broad-based with real output decreasing in the primary, secondary and tertiary sectors, and in seven of the ten subsectors. The real gross value added (GVA) by the primary sector contracted for a fifth successive quarter in the first quarter of 2019, as real output receded sharply in both the agricultural and mining sectors. A further decline in the wine grape harvest and the postponement of the citrus fruit harvest to the second quarter of 2019 largely contributed to the lower agricultural output.

The domestic maize harvest is also expected to be much lower than last year’s record harvest, but should be sufficient to cover domestic consumption. The decrease in the real output of the mining sector was fairly broad-based among the different mineral groups and was exacerbated by Stage 4 electricity load-shedding in February and March, planned maintenance and stocktaking at platinum mines, and the prolonged strike at a large gold mine. The real output of the secondary sector also contracted sharply in the first quarter of 2019, aggravated by the electricity-supply disruptions. The real GVA by the manufacturing as well as the electricity, gas and water supply sectors reverted from expansions to contractions, while construction activity decreased further in the first quarter of 2019.

The real GVA by the tertiary sector switched from an expansion in the fourth quarter of 2018 to a contraction in the first quarter of 2019. The decrease in the real output of the commerce as well as the transport, storage and communication sectors reflected generally weak consumer demand and lower export and import volumes. The real GVA by the finance sector advanced at a slower pace, while that by the general government services sector reverted to an increase following a marginal decrease in the fourth quarter of 2018. In contrast to the contraction in real GDP, real gross domestic expenditure (GDE) increased by 4.5% in the first quarter of 2019 following a sharp contraction in the previous quarter. The reversal in real GDE reflected a notably slower pace of de-accumulation in inventories alongside a slight acceleration in final consumption expenditure by general government.

By contrast, final consumption expenditure by households reverted from an increase to a decrease and real gross fixed capital formation contracted further. Real net exports detracted significantly from real GDP growth in the first quarter of 2019 as export volumes declined much more than import volumes.

Consumer price inflation in the major advanced economies remained broadly below central bank targets in the first quarter of 2019, despite tightening labour markets, while inflationary pressures generally eased in emerging market economies. The international prices of agricultural commodities as well as metals and minerals increased marginally in the first quarter of 2019, while energy prices decreased further. Although the price of Brent crude oil declined on a quarter-to-quarter average basis in the first quarter of 2019, it increased from below US$50 per barrel at the end of December 2018 to around US$74 per barrel by mid-May 2019. Oil prices subsequently declined significantly to around US$62 per barrel in early June on concerns that US–China trade tensions would weigh on demand.

In South Africa, the first quarter of 2019 was characterised by severe electricity-supply disruptions, continued weak business confidence and caution ahead of the national elections in May. Real gross domestic product (GDP) contracted sharply by an annualised 3.2% in the first quarter of 2019 – the largest decrease since the first quarter of 2009 – but remained unchanged when measured over four quarters. The contraction was broad-based with real output decreasing in the primary, secondary and tertiary sectors, and in seven of the ten subsectors. The real gross value added (GVA) by the primary sector contracted for a fifth successive quarter in the first quarter of 2019, as real output receded sharply in both the agricultural and mining sectors. A further decline in the wine grape harvest and the postponement of the citrus fruit harvest to the second quarter of 2019 largely contributed to the lower agricultural output.

The domestic maize harvest is also expected to be much lower than last year’s record harvest, but should be sufficient to cover domestic consumption. The decrease in the real output of the mining sector was fairly broad-based among the different mineral groups and was exacerbated by Stage 4 electricity load-shedding in February and March, planned maintenance and stocktaking at platinum mines, and the prolonged strike at a large gold mine. The real output of the secondary sector also contracted sharply in the first quarter of 2019, aggravated by the electricity-supply disruptions. The real GVA by the manufacturing as well as the electricity, gas and water supply sectors reverted from expansions to contractions, while construction activity decreased further in the first quarter of 2019.

The real GVA by the tertiary sector switched from an expansion in the fourth quarter of 2018 to a contraction in the first quarter of 2019. The decrease in the real output of the commerce as well as the transport, storage and communication sectors reflected generally weak consumer demand and lower export and import volumes. The real GVA by the finance sector advanced at a slower pace, while that by the general government services sector reverted to an increase following a marginal decrease in the fourth quarter of 2018. In contrast to the contraction in real GDP, real gross domestic expenditure (GDE) increased by 4.5% in the first quarter of 2019 following a sharp contraction in the previous quarter. The reversal in real GDE reflected a notably slower pace of de-accumulation in inventories alongside a slight acceleration in final consumption expenditure by general government.

By contrast, final consumption expenditure by households reverted from an increase to a decrease and real gross fixed capital formation contracted further. Real net exports detracted significantly from real GDP growth in the first quarter of 2019 as export volumes declined much more than import volumes.

The contraction in real household consumption expenditure in the first quarter of 2019 resulted largely from notable declines in spending on durable and semi-durable goods. In addition, growth in real spending on non-durable goods moderated while that on services accelerated somewhat. The level of real expenditure by households was only 0.4% higher in the first quarter of 2019 than in the corresponding period of 2018, reflecting weak demand as growth in the real disposable income of households was weighed down by lacklustre employment growth, an increased tax burden and slower wage growth. However, households’ net wealth increased in the first quarter of 2019 as the increase in assets outpaced that in liabilities.

The faster growth in the financial assets of households was underpinned by gains in equity portfolios as the FTSE/ JSE All-Share Price Index increased by 7.1% in the first quarter of 2019 – its best first-quarter performance since 2007 – following losses in the preceding two quarters. This was partly offset by slower growth in the non-financial assets of households due to a further slowdown in nominal house price growth. Real gross fixed capital formation decreased for a fifth consecutive quarter in the first quarter of 2019. Real fixed capital outlays by private business enterprises contracted sharply, consistent with the protracted period of low business confidence and subdued economic activity. By contrast, capital spending by public corporations and general government increased in the first quarter of 2019 following several consecutive quarters of contraction.

Total household-surveyed employment decreased in the first quarter of 2019, weighed down by the sharp contraction in real GDP. The decline was most pronounced in the formal non-agricultural sector of the economy. The increase in the number of unemployed South Africans lifted the official unemployment rate to 27.6% in the first quarter of 2019, while the seasonally adjusted unemployment rate decreased to 27.2%. The number of discouraged work seekers increased by a notable 7.5% year on year to a record high of 3.0 million in the first quarter of 2019, as the prolonged period of weak economic growth made employment opportunities scarcer. Growth in nominal remuneration per worker in the formal non-agricultural sector of the economy slowed in the fourth quarter of 2018 as wage growth moderated in both the private and public sectors. On an annual average basis, growth in nominal remuneration per worker moderated from 6.4% in 2017 to a record low (since the inception of the data in 1971) of 4.7% in 2018. The slowdown in nominal wage growth resulted in a moderation in formal non-agricultural nominal unit labour cost growth in the fourth quarter of 2018. For 2018 as a whole, growth in nominal unit labour cost slowed to 4.4% – its slowest pace since 2007 – indicative of the lack of wage pressure in the domestic economy. Domestic inflationary pressures increased gradually in the first five months of 2019 in the wake of higher international crude oil prices and the depreciation in the exchange value of the rand.

Most measures of producer price inflation have accelerated thus far in 2019, largely reflecting higher energy and food prices. Headline consumer price inflation also accelerated, from a recent low of 4.0% in January 2019 to 4.5% in May, but remained within the inflation target range for 26 consecutive months. Despite the gradual acceleration in producer food price inflation, consumer food price inflation remained muted up to April 2019 before accelerating slightly in May. Core inflation remained unchanged at 4.4% in the five months up to March 2019 before slowing to 4.1% in both April and May, reflecting an environment of weak domestic demand where margins are tight and firms are constrained to fully pass on cost increases to consumers. South Africa’s trade surplus with the rest of the world narrowed from the fourth quarter of 2018 to the first quarter of 2019 as the value of net gold and merchandise exports decreased more than that of merchandise imports. The value of mining, manufacturing and agricultural exports all declined notably, driven largely by lower volumes, which were adversely affected by the electricity-supply disruptions and labour strikes in the mining sector. In addition to the smaller trade surplus, the shortfall on the services, income and current transfer account widened slightly in the first quarter of 2019 as the services and current transfer deficits widened marginally, while the income deficit remained broadly unchanged. Accordingly, the deficit on the current account of the balance of payments widened from 2.2% of GDP in the fourth quarter of 2018 to 2.9% in the first quarter of 2019.

The faster growth in the financial assets of households was underpinned by gains in equity portfolios as the FTSE/ JSE All-Share Price Index increased by 7.1% in the first quarter of 2019 – its best first-quarter performance since 2007 – following losses in the preceding two quarters. This was partly offset by slower growth in the non-financial assets of households due to a further slowdown in nominal house price growth. Real gross fixed capital formation decreased for a fifth consecutive quarter in the first quarter of 2019. Real fixed capital outlays by private business enterprises contracted sharply, consistent with the protracted period of low business confidence and subdued economic activity. By contrast, capital spending by public corporations and general government increased in the first quarter of 2019 following several consecutive quarters of contraction.

Total household-surveyed employment decreased in the first quarter of 2019, weighed down by the sharp contraction in real GDP. The decline was most pronounced in the formal non-agricultural sector of the economy. The increase in the number of unemployed South Africans lifted the official unemployment rate to 27.6% in the first quarter of 2019, while the seasonally adjusted unemployment rate decreased to 27.2%. The number of discouraged work seekers increased by a notable 7.5% year on year to a record high of 3.0 million in the first quarter of 2019, as the prolonged period of weak economic growth made employment opportunities scarcer. Growth in nominal remuneration per worker in the formal non-agricultural sector of the economy slowed in the fourth quarter of 2018 as wage growth moderated in both the private and public sectors. On an annual average basis, growth in nominal remuneration per worker moderated from 6.4% in 2017 to a record low (since the inception of the data in 1971) of 4.7% in 2018. The slowdown in nominal wage growth resulted in a moderation in formal non-agricultural nominal unit labour cost growth in the fourth quarter of 2018. For 2018 as a whole, growth in nominal unit labour cost slowed to 4.4% – its slowest pace since 2007 – indicative of the lack of wage pressure in the domestic economy. Domestic inflationary pressures increased gradually in the first five months of 2019 in the wake of higher international crude oil prices and the depreciation in the exchange value of the rand.

Most measures of producer price inflation have accelerated thus far in 2019, largely reflecting higher energy and food prices. Headline consumer price inflation also accelerated, from a recent low of 4.0% in January 2019 to 4.5% in May, but remained within the inflation target range for 26 consecutive months. Despite the gradual acceleration in producer food price inflation, consumer food price inflation remained muted up to April 2019 before accelerating slightly in May. Core inflation remained unchanged at 4.4% in the five months up to March 2019 before slowing to 4.1% in both April and May, reflecting an environment of weak domestic demand where margins are tight and firms are constrained to fully pass on cost increases to consumers. South Africa’s trade surplus with the rest of the world narrowed from the fourth quarter of 2018 to the first quarter of 2019 as the value of net gold and merchandise exports decreased more than that of merchandise imports. The value of mining, manufacturing and agricultural exports all declined notably, driven largely by lower volumes, which were adversely affected by the electricity-supply disruptions and labour strikes in the mining sector. In addition to the smaller trade surplus, the shortfall on the services, income and current transfer account widened slightly in the first quarter of 2019 as the services and current transfer deficits widened marginally, while the income deficit remained broadly unchanged. Accordingly, the deficit on the current account of the balance of payments widened from 2.2% of GDP in the fourth quarter of 2018 to 2.9% in the first quarter of 2019.

The net inflow of capital on the financial account of the balance of payments increased in the first quarter of 2019. On a net basis, portfolio investment and reserve assets recorded inflows, while direct investment, financial derivatives and other investment registered outflows. South Africa’s positive net international investment position decreased from the end of September 2018 to the end of December as the value of foreign assets decreased and that of foreign liabilities increased marginally. The decrease in the value of foreign assets mainly reflected the effect of the sharp decline in global equity prices on portfolio investment assets. South Africa’s external debt increased from the end of September 2018 to the end of December as the value of foreign currency-denominated external debt increased, mainly due to short-term foreign loans to the domestic banking sector.

The nominal effective exchange rate (NEER) of the rand decreased further in the first quarter of 2019 amid ongoing month-to-month volatility and despite a notable increase in January 2019. The strong increase in January followed the release of the trade balance for November 2018 that reverted to a surplus, as well as further monetary policy easing by the People’s Bank of China and another interest rate pause by the US Federal Reserve, all of which provided support to emerging market assets. The exchange value of the rand then depreciated in February and March following the release of the 2019 Budget Review, concerns about the potential impact of the electricity outages on economic growth, the risk of successive fuel price increases to inflation, and uncertainty ahead of the national elections in May. The NEER increased again in April 2019 following South Africa’s retention of a sovereign investment-grade rating, but decreased in the aftermath of the national elections due to policy uncertainty and the larger than-expected contraction in domestic real GDP in the first quarter of 2019. In early 2019 South African bond yields broadly tracked the movements in the exchange rate of the rand before continuing lower up to the end of May, in step with lower international bond yields. Year-on-year growth in the broadly defined money supply (M3) rebounded in the first quarter of 2019, contrary to the slower growth in nominal GDP.

Growth in the deposit holdings of the corporate sector accelerated markedly, in particular that of financial companies, amid risk aversion in the run-up to the national elections. By contrast, growth in the deposit holdings of households bottomed out at fairly subdued rates. Growth in bank credit extended to the domestic private sector accelerated in the first four months of 2019 as the gradual acceleration in loans and advances to households continued and credit extension to the corporate sector quickened. Although growth in most of the credit categories to both households and companies accelerated over the period, growth in mortgage advances remained subdued. National government’s cash book deficit increased by R21.0 billion from fiscal 2017/18 to fiscal 2018/19, and was R42.0 billion more than the original budget estimate. The deterioration in national government finances in fiscal 2018/19 resulted from further revenue shortfalls, while expenditure was slightly below the original estimate. The revenue shortfall could largely be ascribed to weaker-than-expected domestic economic activity and higher tax refunds, in particular of value-added tax. Despite the larger cash book deficit of national government, the non-financial public sector borrowing requirement was marginally lower in fiscal 2018/19 than in the previous fiscal year, as the larger cash deficits of national government and of non-financial public enterprises and corporations were more than offset by cash surpluses of all other tiers of general government.

The nominal effective exchange rate (NEER) of the rand decreased further in the first quarter of 2019 amid ongoing month-to-month volatility and despite a notable increase in January 2019. The strong increase in January followed the release of the trade balance for November 2018 that reverted to a surplus, as well as further monetary policy easing by the People’s Bank of China and another interest rate pause by the US Federal Reserve, all of which provided support to emerging market assets. The exchange value of the rand then depreciated in February and March following the release of the 2019 Budget Review, concerns about the potential impact of the electricity outages on economic growth, the risk of successive fuel price increases to inflation, and uncertainty ahead of the national elections in May. The NEER increased again in April 2019 following South Africa’s retention of a sovereign investment-grade rating, but decreased in the aftermath of the national elections due to policy uncertainty and the larger than-expected contraction in domestic real GDP in the first quarter of 2019. In early 2019 South African bond yields broadly tracked the movements in the exchange rate of the rand before continuing lower up to the end of May, in step with lower international bond yields. Year-on-year growth in the broadly defined money supply (M3) rebounded in the first quarter of 2019, contrary to the slower growth in nominal GDP.

Growth in the deposit holdings of the corporate sector accelerated markedly, in particular that of financial companies, amid risk aversion in the run-up to the national elections. By contrast, growth in the deposit holdings of households bottomed out at fairly subdued rates. Growth in bank credit extended to the domestic private sector accelerated in the first four months of 2019 as the gradual acceleration in loans and advances to households continued and credit extension to the corporate sector quickened. Although growth in most of the credit categories to both households and companies accelerated over the period, growth in mortgage advances remained subdued. National government’s cash book deficit increased by R21.0 billion from fiscal 2017/18 to fiscal 2018/19, and was R42.0 billion more than the original budget estimate. The deterioration in national government finances in fiscal 2018/19 resulted from further revenue shortfalls, while expenditure was slightly below the original estimate. The revenue shortfall could largely be ascribed to weaker-than-expected domestic economic activity and higher tax refunds, in particular of value-added tax. Despite the larger cash book deficit of national government, the non-financial public sector borrowing requirement was marginally lower in fiscal 2018/19 than in the previous fiscal year, as the larger cash deficits of national government and of non-financial public enterprises and corporations were more than offset by cash surpluses of all other tiers of general government.

International economic developments

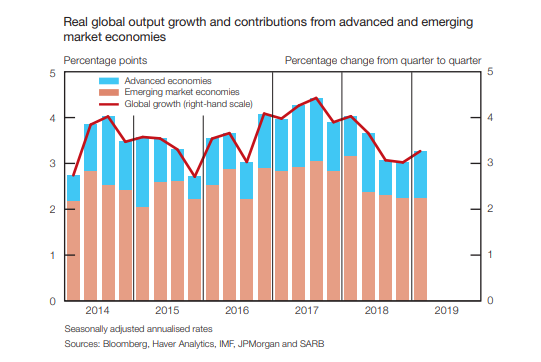

Global economic growth gained some momentum in the first quarter of 2019 following a subdued second half of 2018. Real global output growth accelerated from an annualised rate of 3.0% in the fourth quarter of 2018 to 3.3% in the first quarter of 2019. The acceleration in output growth was fairly broad-based among the advanced economies, while real economic activity also improved in some major emerging markets such as China and Turkey.

The United States (US) led the economic recovery in the advanced economies, with growth in real gross domestic product (GDP) accelerating from 2.2% in the fourth quarter of 2018 to 3.1% in the first quarter of 2019. The acceleration was largely driven by net exports and personal consumption expenditure, which together contributed 1.9 percentage points to real GDP growth, while inventory accumulation added 0.7 percentage points.

Real GDP growth in the euro area rebounded from a weak 1.0% in the fourth quarter of 2018 to 1.6% in the first quarter of 2019 as economic conditions in Italy and Germany improved. The Italian economy expanded by 0.5% following a technical recession in the second half of 2018. Germany also posted a solid gain as real GDP expanded by 1.7% in the first quarter of 2019, from a near standstill of 0.1% at the end of 2018. In general, the euro area benefited from robust consumer spending and increased construction activity amid mild weather conditions. In the United Kingdom, real economic growth more than doubled from 0.9% in the fourth quarter of 2018 to 2.0% in the first quarter of 2019, mainly due to resilient household consumption expenditure and a build-up of inventories in preparation for a possible disorderly Brexit.

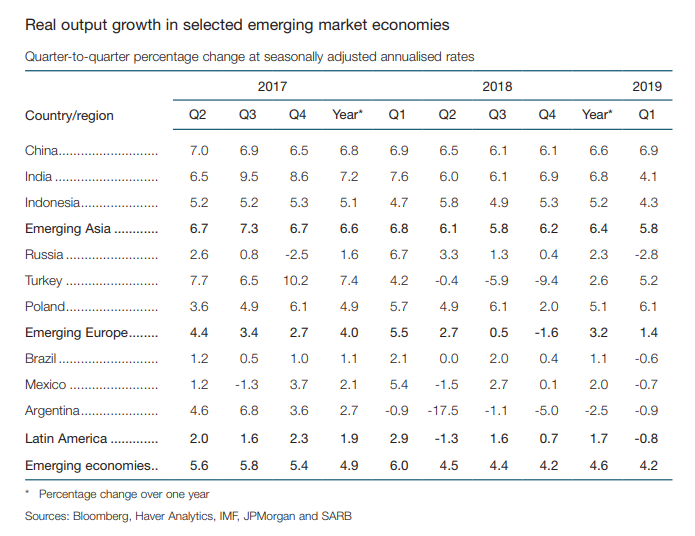

Japanese output growth unexpectedly accelerated from 1.8% in the fourth quarter 2018 to 2.2% in the first quarter of 2019, as imports declined and inventories increased. Real economic growth in emerging markets remained unchanged at 4.2% in the first quarter of 2019, with growth decelerating in emerging Asia and output contracting in Latin America. This was offset by improved economic conditions in emerging Europe, where real output reverted from a contraction in the fourth quarter of 2018 to an expansion in the first quarter of 2019. In emerging Asia, China’s real output growth surprised on the upside at 6.9% in the first quarter of 2019 due to a recovery in the finance and construction sectors. By contrast, real GDP growth in India slowed to 4.1% in the first quarter of 2019 due to weaker consumer demand and fixed investment.

Real GDP growth in the euro area rebounded from a weak 1.0% in the fourth quarter of 2018 to 1.6% in the first quarter of 2019 as economic conditions in Italy and Germany improved. The Italian economy expanded by 0.5% following a technical recession in the second half of 2018. Germany also posted a solid gain as real GDP expanded by 1.7% in the first quarter of 2019, from a near standstill of 0.1% at the end of 2018. In general, the euro area benefited from robust consumer spending and increased construction activity amid mild weather conditions. In the United Kingdom, real economic growth more than doubled from 0.9% in the fourth quarter of 2018 to 2.0% in the first quarter of 2019, mainly due to resilient household consumption expenditure and a build-up of inventories in preparation for a possible disorderly Brexit.

Japanese output growth unexpectedly accelerated from 1.8% in the fourth quarter 2018 to 2.2% in the first quarter of 2019, as imports declined and inventories increased. Real economic growth in emerging markets remained unchanged at 4.2% in the first quarter of 2019, with growth decelerating in emerging Asia and output contracting in Latin America. This was offset by improved economic conditions in emerging Europe, where real output reverted from a contraction in the fourth quarter of 2018 to an expansion in the first quarter of 2019. In emerging Asia, China’s real output growth surprised on the upside at 6.9% in the first quarter of 2019 due to a recovery in the finance and construction sectors. By contrast, real GDP growth in India slowed to 4.1% in the first quarter of 2019 due to weaker consumer demand and fixed investment.

In Latin America, an expansion of 0.7% in real output in the fourth quarter of 2018 switched to a contraction of 0.8% in the first quarter of 2019. Regional growth was constrained by weak economic activity in Argentina, Brazil, Mexico and Venezuela. Argentina’s economy remains in recession as output declined by 0.9% in the first quarter of 2019. Real GDP in Brazil contracted by 0.6% as investor confidence waned, while the contraction of 0.7% in Mexico resulted largely from a decline in services activity and continued weak oil output.

The economic recovery in emerging Europe was largely driven by a sharp improvement in Turkey’s real GDP, which expanded by 5.2% in the first quarter of 2019 after a severe technical recession in the second half of 2018 (-5.9% in the third quarter and -9.4% in the fourth quarter). The rebound in Turkey’s output growth resulted from an increase in government final consumption expenditure and a decline in imports, which was partly offset by lower exports and reduced gross fixed capital formation. Real GDP growth in Poland also accelerated from 2.0% in the fourth quarter of 2018 to 6.1% in the first quarter of 2019.

This was in sharp contrast to the contraction in economic activity in Russia of 2.8% as consumer demand weakened following an increase in the value-added tax rate. Headline consumer price inflation in the major advanced economies generally remained below central banks’ 2.0% inflation targets, despite tightening labour markets. In the US, growth in the personal consumption expenditure deflator (the US Federal Reserve’s preferred inflation measure) slowed to 1.4% in the first quarter of 2019, partly due to temporary factors. Inflationary pressures in emerging market economies generally eased in the first quarter of 2019. World trade volumes (using world exports as a proxy) declined further by 1.0% in March 2019 (in three-months-to-three-months terms), in part due to ongoing trade tensions. Export volumes in emerging markets fell by 4.6% over this period, mainly due to lower exports from Latin America.

Exports from advanced economies increased by 1.8% in March 2019. The international prices of agricultural commodities as well as metals and minerals rose modestly in the first quarter of 2019, while energy prices declined further. The price of Brent crude oil increased from below US$50 per barrel at the end of December 2018 to around US$74 per barrel by mid-May 2019. The increase in oil prices was mainly driven by production cuts in oil exporting countries and US sanctions on Iranian and Venezuelan oil exports. However, oil prices declined significantly to around US$62 per barrel in early June on concerns that US–China trade tensions would weigh on demand. Rising US oil inventories also contributed to renewed downward pressure on oil prices.

The economic recovery in emerging Europe was largely driven by a sharp improvement in Turkey’s real GDP, which expanded by 5.2% in the first quarter of 2019 after a severe technical recession in the second half of 2018 (-5.9% in the third quarter and -9.4% in the fourth quarter). The rebound in Turkey’s output growth resulted from an increase in government final consumption expenditure and a decline in imports, which was partly offset by lower exports and reduced gross fixed capital formation. Real GDP growth in Poland also accelerated from 2.0% in the fourth quarter of 2018 to 6.1% in the first quarter of 2019.

This was in sharp contrast to the contraction in economic activity in Russia of 2.8% as consumer demand weakened following an increase in the value-added tax rate. Headline consumer price inflation in the major advanced economies generally remained below central banks’ 2.0% inflation targets, despite tightening labour markets. In the US, growth in the personal consumption expenditure deflator (the US Federal Reserve’s preferred inflation measure) slowed to 1.4% in the first quarter of 2019, partly due to temporary factors. Inflationary pressures in emerging market economies generally eased in the first quarter of 2019. World trade volumes (using world exports as a proxy) declined further by 1.0% in March 2019 (in three-months-to-three-months terms), in part due to ongoing trade tensions. Export volumes in emerging markets fell by 4.6% over this period, mainly due to lower exports from Latin America.

Exports from advanced economies increased by 1.8% in March 2019. The international prices of agricultural commodities as well as metals and minerals rose modestly in the first quarter of 2019, while energy prices declined further. The price of Brent crude oil increased from below US$50 per barrel at the end of December 2018 to around US$74 per barrel by mid-May 2019. The increase in oil prices was mainly driven by production cuts in oil exporting countries and US sanctions on Iranian and Venezuelan oil exports. However, oil prices declined significantly to around US$62 per barrel in early June on concerns that US–China trade tensions would weigh on demand. Rising US oil inventories also contributed to renewed downward pressure on oil prices.

The international prices of agricultural products, in US dollar terms, increased slightly by 0.9% in the first quarter of 2019 due to increases in maize, soya bean and sorghum prices. Metals and minerals prices rose by 1.7% over the same period, owing to higher iron ore, nickel and tin prices.