South Africa's financial cycles

Category: Financial markets and economics

Date: 25 April 2023

Date: 25 April 2023

|

We take a look at South Africa's financial cycles as defined by the South African Reserve Bank (SARB) and take a look at the SARB's view on South Africa's financial stability.

|

|

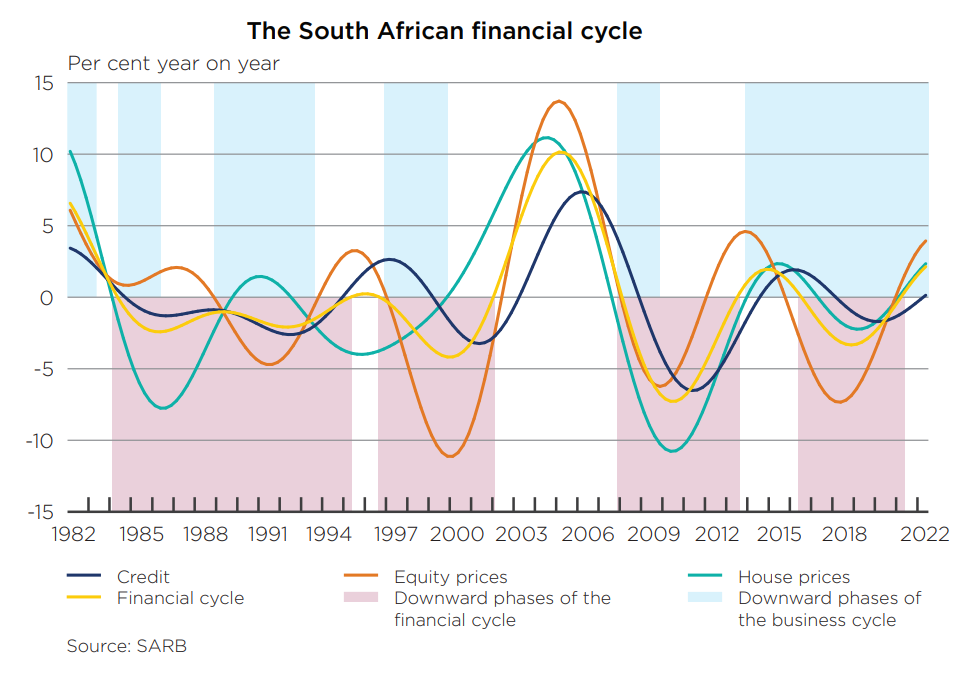

The South African financial cycle remained in an upward phase

What follows below comes from the South African Reserve Bank's 2nd Financial Stability Review for 2022 unless stated otherwise.

The South African financial cycle remained in an upward phase amid rising equity and house prices, and a normalisation in credit extension. As a result, the credit component of the financial cycle moved into an upward phase during the period under review for the first time since the first quarter of 2018 (Figure 7). House price growth was supported by the low interest rate environment, although this impact is expected to taper off as interest rates increase. The SARB has increased the policy rate by a cumulative 350 basis points since November 2021.

The South African financial cycle remained in an upward phase amid rising equity and house prices, and a normalisation in credit extension. As a result, the credit component of the financial cycle moved into an upward phase during the period under review for the first time since the first quarter of 2018 (Figure 7). House price growth was supported by the low interest rate environment, although this impact is expected to taper off as interest rates increase. The SARB has increased the policy rate by a cumulative 350 basis points since November 2021.

South Africa’s financial markets traded largely in tandem with the prevailing global sentiment

South Africa’s financial markets traded largely in tandem with the prevailing global sentiment, with the exchange value of the rand depreciating against the US dollar from R15.20 on 9 June 2022 to R18.45 on 25 October 2022 before recovering somewhat to R16.96 on 24 November 2022. The rand also depreciated by 5% and 2.5% against the euro and British pound respectively. The main drivers of the broader-based depreciation in the exchange value of the rand were negative investor sentiment and capital outflows, in line with global trends but exacerbated by domestic factors such as increased loadshedding and a deterioration in the current account.

During the review period, the South African government bond (SAGB) yield curve remained steep and shifted higher across all maturities. In line with those of other emerging markets, rand- and dollar-denominated South African government debt spreads widened, broadly reflecting the prevailing negative global risk sentiment. Liquidity conditions in the domestic government bond market also deteriorated during the review period, with widening bidoffer spreads across all maturities mainly reflecting global risk aversion and reduced appetite by non-resident investors. Liquidity in the SAGB market is discussed in detail in the May 2022 FSR, 6 which noted that although the SARB had taken various steps to restore and maintain smooth market functioning since the onset of the COVID-19-induced shock, the decline in SAGB market liquidity had prevailed beyond the initial shock.

When considered alongside the bank-sovereign nexus, as discussed in detail in the first edition of the 2021 FSR, liquidity in the SAGB market will continue to be monitored from a financial stability perspective. Non-resident investors were net sellers of R8 billion worth of SAGBs, resulting in a continued decline in non-resident holdings of SAGBs during the review period from 28.1% to 26.8% of total SAGBs outstanding – a level last seen in June 2011 (Figure 9). Banks, which accumulated large volumes of bonds during the onset of COVID-19, topped the list of buyers during the review period, acquiring R47.7 billion, or 54%, of the net primary market issuance of SAGBs. The increased take-up by banks of SAGBs contributed to lower liquidity in the secondary market for SAGBs, as several banks follow a buy-and-hold strategy for SAGBs as part of their investment portfolios.

During the review period, the South African government bond (SAGB) yield curve remained steep and shifted higher across all maturities. In line with those of other emerging markets, rand- and dollar-denominated South African government debt spreads widened, broadly reflecting the prevailing negative global risk sentiment. Liquidity conditions in the domestic government bond market also deteriorated during the review period, with widening bidoffer spreads across all maturities mainly reflecting global risk aversion and reduced appetite by non-resident investors. Liquidity in the SAGB market is discussed in detail in the May 2022 FSR, 6 which noted that although the SARB had taken various steps to restore and maintain smooth market functioning since the onset of the COVID-19-induced shock, the decline in SAGB market liquidity had prevailed beyond the initial shock.

When considered alongside the bank-sovereign nexus, as discussed in detail in the first edition of the 2021 FSR, liquidity in the SAGB market will continue to be monitored from a financial stability perspective. Non-resident investors were net sellers of R8 billion worth of SAGBs, resulting in a continued decline in non-resident holdings of SAGBs during the review period from 28.1% to 26.8% of total SAGBs outstanding – a level last seen in June 2011 (Figure 9). Banks, which accumulated large volumes of bonds during the onset of COVID-19, topped the list of buyers during the review period, acquiring R47.7 billion, or 54%, of the net primary market issuance of SAGBs. The increased take-up by banks of SAGBs contributed to lower liquidity in the secondary market for SAGBs, as several banks follow a buy-and-hold strategy for SAGBs as part of their investment portfolios.