|

Related Topics |

|

We take a look at the operational and trading update released by Shoprite (SHP) for the period ending June 2019. In a struggling consumer environment, how has the largest retailer in Africa gone in the last 6 months? Based on the fact that earnings per share declined significantly it looked like the struggled.

|

|

OPERATIONAL UPDATE AND TRADING UPDATE

Pieter Engelbrecht, Chief Executive: “Emerging from a transformational year in 2018, which resulted in only marginal sales growth in the first half to December, we are pleased to report improved growth in the second half with Group sales up 6.5% (excluding hyperinflation impact). This performance was driven mainly by our Supermarkets RSA operation growing sales by 7.4% in the six months to June 2019 and 9.4% in the final quarter. The market share gain in the most recent quarter is testament to our core South African business being back to full operational strength. Trading conditions in the rest of Africa remain relentless as the results attest but given our optimism for the long-term food retail opportunity on the continent, we remain resolute in our purpose to be Africa’s most affordable and accessible retailer. The combination of on-going low food inflation in South Africa and currency devaluations in the rest of Africa have resulted in this being a most challenging year, however the continued improvement throughout the second half is pleasing and product availability now surpasses pre- system implementation levels. We honoured our promise of lower prices, serving more than 1.1 billion customers in the year.

Better customer service levels and recent market share gains are indicative that the challenges following last year’s industrial action and the successful deployment of our new enterprise-wide system are now behind us. We look forward to the returns from the new capabilities this large scale system implementation has enabled. Shoprite has emerged a stronger, fitter retailer with many exciting innovations underway. The Group’s expansion remains on track with 80 new supermarkets opened in the period and 88 planned for the next year.

The Shoprite team is making headway in all of our strategic areas of focus; including advancing our digital transformation agenda, growing Checkers’ share of premium food retail, building a better franchise offer and increasing our private label penetration. Ultimately these have all laid a stronger foundation for growth in the medium term.”

Operational update (52 weeks ended 30 June 2019) Excluding hyperinflation, the Group increased total turnover by 3.2% (0.1% like for like) to approximately R150.6 billion in the period to June 2019. The Group’s supermarkets increased the number of customers served by 2.3% and product volumes sold by 1.2%. Including the impact of the Angolan hyperinflation accounting adjustment, Group turnover increased by 3.6% for the full year.

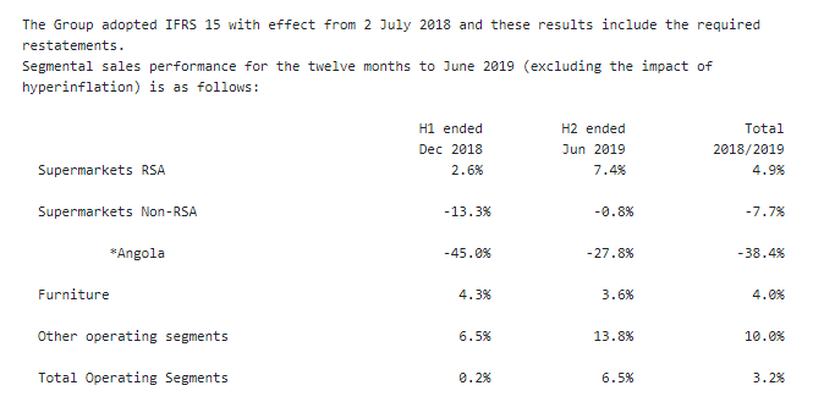

The image below shows the segmental revenue for the Shoprite group for the 52 weeks ending June 2019

Better customer service levels and recent market share gains are indicative that the challenges following last year’s industrial action and the successful deployment of our new enterprise-wide system are now behind us. We look forward to the returns from the new capabilities this large scale system implementation has enabled. Shoprite has emerged a stronger, fitter retailer with many exciting innovations underway. The Group’s expansion remains on track with 80 new supermarkets opened in the period and 88 planned for the next year.

The Shoprite team is making headway in all of our strategic areas of focus; including advancing our digital transformation agenda, growing Checkers’ share of premium food retail, building a better franchise offer and increasing our private label penetration. Ultimately these have all laid a stronger foundation for growth in the medium term.”

Operational update (52 weeks ended 30 June 2019) Excluding hyperinflation, the Group increased total turnover by 3.2% (0.1% like for like) to approximately R150.6 billion in the period to June 2019. The Group’s supermarkets increased the number of customers served by 2.3% and product volumes sold by 1.2%. Including the impact of the Angolan hyperinflation accounting adjustment, Group turnover increased by 3.6% for the full year.

The image below shows the segmental revenue for the Shoprite group for the 52 weeks ending June 2019

The following provides context to the overall turnover growth for the twelve months:

- The Group’s core business, Supermarkets RSA, achieved 4.9% sales growth for the period (like for like growth: 1.9%) with an improved second half in which sales increased by 7.4% on the back of better customer and volume growth, as well as an improvement in on-shelf availability and promotional effectiveness. The full year performance should be viewed in the context of a first half that was impacted by the completion of our multi-year ERP IT system re-platforming as well as the aftermath of the May and June 2018 industrial action at our largest DC in Gauteng. Supermarkets RSA had a strong Easter sales period and the momentum culminated in final quarter sales growth of 9.4% and the Group reclaiming market share.

- Internal inflation for the year averaged just 1.2% for Supermarkets RSA. Despite an uptick towards year end, it remained lower for longer than was anticipated with 9,679 items still in deflation in June, many of which are in categories in which the Group commands a higher than average market share. - The Checkers chain led the supermarkets’ growth, making strides in improving our fresh offer and gaining market share in fresh produce and convenience meals. The accelerated rollout of our new FreshX concept stores is showing exceptional performance.

- Shoprite’s growth for the year was subdued given the reliance on many food categories in deflation as well as the vulnerability of it’s core target consumers to prevailing economic headwinds. Whilst the primary Shoprite consumer base remains under significant pressure in a strained economy, the Shoprite brand has retained its price leadership, evidenced in the market share gains in the most recent quarter.

- Sales growth in the Usave format was hardest hit in the first half by the combination of deflation and the supply chain issues causing out of stocks in Gauteng, its largest regional market.

- The improvement in our private label offer has seen its participation to RSA sales grow by a further 30 basis points, offering better value to consumers from budget to super premium categories.

- LiquorShop remained a standout performer recording strong double digit growth for the period. This week marks a significant milestone as we are set to open our 500th store.

- Online sales which encompass Click & Collect orders and our on-demand liquor home delivery partnership has increased 386% with rapid customer acceptance.

- Supermarkets Non-RSA recorded a decline in turnover of 7.7% which impacted the overall Group sales performance (on a constant currency basis, turnover for the year increased by 0.9%). The second half saw the decline in sales slowing to 0.8% from the -13.3% in the first half. The underperformance was primarily a result of currency devaluations in the major countries where the Group trades in the rest of Africa, which negatively impacted sales in rand terms. The rebasing of the sales performance in the Angolan operation, the largest contributor in our Non-RSA portfolio, remained a drag on the overall Group performance. Angola’s supermarkets sales declined 38.4% in rand terms after the dramatic 105.4% devaluation of the Angola kwanza to the US dollar since January 2018, combined with an economic recession.

- Excluding Angola, Supermarkets Non-RSA achieved positive sales growth of 5.8% in constant currency amidst difficult macroeconomic conditions persisting in all territories.

- During the financial year, the currencies of the other large countries in which we trade, namely Zambia and Nigeria, also showed a sharp decline against the US dollar of 29.4% and 17.9% respectively.

- The Group’s Furniture division increased sales by 4.0% for the period, affected particularly by the Non-RSA operating environment.

- Other operating segments (OK Franchise, Medirite Pharmacy and Checkers Food Services) achieved pleasing growth of 10.0%.

- The Group’s core business, Supermarkets RSA, achieved 4.9% sales growth for the period (like for like growth: 1.9%) with an improved second half in which sales increased by 7.4% on the back of better customer and volume growth, as well as an improvement in on-shelf availability and promotional effectiveness. The full year performance should be viewed in the context of a first half that was impacted by the completion of our multi-year ERP IT system re-platforming as well as the aftermath of the May and June 2018 industrial action at our largest DC in Gauteng. Supermarkets RSA had a strong Easter sales period and the momentum culminated in final quarter sales growth of 9.4% and the Group reclaiming market share.

- Internal inflation for the year averaged just 1.2% for Supermarkets RSA. Despite an uptick towards year end, it remained lower for longer than was anticipated with 9,679 items still in deflation in June, many of which are in categories in which the Group commands a higher than average market share. - The Checkers chain led the supermarkets’ growth, making strides in improving our fresh offer and gaining market share in fresh produce and convenience meals. The accelerated rollout of our new FreshX concept stores is showing exceptional performance.

- Shoprite’s growth for the year was subdued given the reliance on many food categories in deflation as well as the vulnerability of it’s core target consumers to prevailing economic headwinds. Whilst the primary Shoprite consumer base remains under significant pressure in a strained economy, the Shoprite brand has retained its price leadership, evidenced in the market share gains in the most recent quarter.

- Sales growth in the Usave format was hardest hit in the first half by the combination of deflation and the supply chain issues causing out of stocks in Gauteng, its largest regional market.

- The improvement in our private label offer has seen its participation to RSA sales grow by a further 30 basis points, offering better value to consumers from budget to super premium categories.

- LiquorShop remained a standout performer recording strong double digit growth for the period. This week marks a significant milestone as we are set to open our 500th store.

- Online sales which encompass Click & Collect orders and our on-demand liquor home delivery partnership has increased 386% with rapid customer acceptance.

- Supermarkets Non-RSA recorded a decline in turnover of 7.7% which impacted the overall Group sales performance (on a constant currency basis, turnover for the year increased by 0.9%). The second half saw the decline in sales slowing to 0.8% from the -13.3% in the first half. The underperformance was primarily a result of currency devaluations in the major countries where the Group trades in the rest of Africa, which negatively impacted sales in rand terms. The rebasing of the sales performance in the Angolan operation, the largest contributor in our Non-RSA portfolio, remained a drag on the overall Group performance. Angola’s supermarkets sales declined 38.4% in rand terms after the dramatic 105.4% devaluation of the Angola kwanza to the US dollar since January 2018, combined with an economic recession.

- Excluding Angola, Supermarkets Non-RSA achieved positive sales growth of 5.8% in constant currency amidst difficult macroeconomic conditions persisting in all territories.

- During the financial year, the currencies of the other large countries in which we trade, namely Zambia and Nigeria, also showed a sharp decline against the US dollar of 29.4% and 17.9% respectively.

- The Group’s Furniture division increased sales by 4.0% for the period, affected particularly by the Non-RSA operating environment.

- Other operating segments (OK Franchise, Medirite Pharmacy and Checkers Food Services) achieved pleasing growth of 10.0%.

Shoprite earnings guidance

Notwithstanding the acceleration in Supermarkets RSA’s second half sales, increases in the cost of employment from new legislation, rent and electricity exceeded the year’s overall top line growth given the impact of first half factors. Predominantly, the lost sales following industrial action at our largest distribution centre as well as the gross margin adjustment relating to the change to the moving average method of accounting for inventory, have resulted in lower profitability than the prior year. Pleasingly though, trading profit increased in the second half at a pace ahead of turnover growth. As a result of forex shortages and local currency weakness, the profitability of Supermarkets Non-RSA deteriorated meaningfully in the second half resulting in a trading loss for the period. The Group therefore anticipates lower earnings per share (“EPS”) and headline earnings per share (“HEPS”) (after taking hyperinflation into account) for the full year ended 30 June 2019, falling within the ranges below:

- Basic HEPS (cents) 774.2 - 832.5 (down between 14.3% and 20.3%)

- Basic EPS (cents) 762.8 - 819.0 (down between 12.5% and 18.5%)

Share price performance

The screenshot taken from Moneyweb below shows the performance of SHP's share price over the last year, as well as the performance of the stock over various time frames.

The summary below shows the share price performance of Shoprite over various periods:

The above shows it has been a pretty tough time for investors in Shoprite

- 1 week: -8.7%

- 1 month: -7.65%

- 1 year: -31.65%

- 3 years: -28.63%

- 5 years: -10.86%

The above shows it has been a pretty tough time for investors in Shoprite