|

Related Topics |

|

We take a look at the full year financial results for the period ending June 2019 for Shoprite Holdings (SHP). How has Africa's largest retailer found the economic and operating environment they are in? Most other retailers in South Africa has struggled to keep margins and to grow profits. Lets take a look at Shoprite's latest numbers

|

|

About Shoprite Holdings

From the moment the Shoprite Group opened its very first stores in 1979, it had a bold vision for the future. One that would see the Group grow from strength to strength with new acquisitions and innovative expansion strategies building it into the leading food retailer it is today. With more than 2843 outlets in 15 countries across Africa and the Indian Oceans islands, employing over 147 478 people, the Group continues to seize new opportunities for growth and even greater success in years to come. The image below shows the list of Shoprite (SHP) brands

The number of Shoprite (SHP) brands includ but are not limited to

- Shoprite

- Checkers

- Checkers Hyper

- Usave

- OK furniture

- House and Home

- Computicket

- Freshmark

Financial overview

Key information regarding Shoprite's latest financial results according to the group

% change 2019 2018

Now for the numbers we are interested in:

% change 2019 2018

- Sale of merchandise (Rm) 3.6 150 395 145 104

- Trading profit (Rm) -14.3 6 876 8 024

- Operating profit (Rm) -8.2 6 911 7 527

- Profit before income tax (Rm) -13.7 6 339 7 347

- Income tax expense (Rm) -2.6 2 068 2 124

- Profit for the year (Rm) -18.2 4 271 5 223

- Attributable to owners of the parent (Rm) 4 260 5 211

- Attributable to non-controlling interest (Rm) 11 12

- Basic headline earnings per share (cents) -19.6 780.8 971.4

- Basic earnings per share (cents) -17.9 768.2 936.0

- Dividend per share (cents) -34.1 319.0 484.0

Now for the numbers we are interested in:

- Net profit margin: 2.83%

- Diluted Headline Earnings per share: R7.79 (down 19.6% from R9.70 in the prior year)

- PE ratio: 17.7

- Dividend declared for year: R3.19 per share (down -34.1% from R4.84 in the prior year)

- Dividend yield: 2.3%

- Cash generated from operations: R4.98 billion

- Cash generated from operations per share: R8.42 per share

- Net asset value per share: R47.01 (down -4.7% from R49.37 in the prior year)

- So trading at 2.9 times it stated net asset value

- Cash on balance sheet: R7.7 billion (up 3.14% from R7.465 billion in the prior year)

- Cash on balance sheet per share: R13 or 9.4% of the current share price

Management commentary on the results

The segment below contains some of the commentary made on the results by Shoprite's management

Pieter Engelbrecht, chief executive officer:

Our core operations, Supermarkets RSA's sales growth of 4.9%, with like-for- like sales growth of 1.9%, is a performance significantly impacted by our well documented first half challenges. With the strike in the DC behind us, our team worked tirelessly to restore performance in the second half. It is pleasing to report that we ended the year with our final quarter's sales in Supermarkets RSA growing by 9.4%. Our in-stock levels are now higher than prior to our system implementation and without compromising on our low price leadership, we achieved a second half trading margin in Supermarkets RSA of 5.5%. We've continued with our growth strategy to capture a larger share of the premium food segment through the ongoing Checkers repositioning.

The number of Checkers stores in the new look FreshX format now totals 21. We are most pleased with returns from these upgrades and, therefore, our medium to long- term target of 80 stores in this format remains unchanged. Our focus on the core Shoprite and Usave customers, who we strive to serve with excellence daily, has remained strong as we continue to bring affordable food retail into the communities where our customers reside. Notwithstanding the much improved recent performance in our core Supermarkets RSA division, which generates 74.9% of our sales and grew second half sales by 7.4%, it was a testing year.

A constrained economy, inventory shortages post industrial action and the implementation of a new enterprise wide IT system across our store base resulted in lost sales. With affordability remaining the top priority for our customers, we unquestionably stood by our lowest price promise. Selling price inflation in our Supermarkets RSA division for the year measured only 1.2%, and similar to last year, we traded throughout the year with many items in key categories in deflation. At year-end, the number of products priced lower than last year measured at 9 679. Ongoing forex shortages, currency devaluations and the aftermath of rampant inflation in Angola and its ongoing impact on affordability took a further toll on our Non-RSA business. Supermarkets Non-RSA reported a trading loss of R265 million for the year. Despite no foreseen respite in short-term trading conditions in the region, we are committed to our customers in the 14 Non-RSA countries in which we operate.

We remain confident in the opportunity our entrenched position as Africa's leading food retailer will bring as the economic fortunes of the countries where we trade improve. Given the challenging global economic backdrop, we are remaining focused on growth opportunities in our home market, inclusive of our established African operations, rather than pursuing businesses in foreign geographies. Social responsibility has and always will be a priority for the Group. Amongst many initiatives focused on improving the lives of our fellow South Africans, it is noteworthy that this year we sold a record of 53 million subsidised deli meals and 58 million loaves of brown bread, both for under R5. We also created a further 3 175 employment opportunities whilst improving our focus on sustainability and governance. I am pleased to be able to say that we have the right people, resources and plans in place to entrench and grow our leading food retail position, both in South Africa and on the rest of the African continent and, therefore, to grow our profitability over the long term."

General comments obtained from the results

Supermarkets RSA

The Group’s core business, Supermarkets RSA, trading through 1 580 stores and representing 74.9% of Group sales achieved 4.9% sales growth for the period to report sales of R112.7 billion. Like-for-like growth measured 1.9% with internal selling price inflation of 1.2% up from only 0.3% last year. This full-year performance should be viewed in the context of a disappointing first half in which sales grew by only 2.6%, impacted by the completion of our multi-year ERP IT system re-platforming, as well as the aftermath of the May and June 2018 industrial action at our largest distribution centre in Gauteng. However, a much improved second half period in which sales increased by 7.4% on the back of better customer and volume growth, as well as an improvement in on-shelf availability and promotional effectiveness, leaves us confident in the restored strength of this division and its formats. Our Checkers supermarket chain, although also hampered by the availability issues that plagued the Group, was the better performing of our major food retail brands in RSA. Turnover growth, inclusive of its 37 larger format Hypers, was 4.6%. Its strategy to grow its share of spend in the mid-to-upper segment of the market by focusing on improving its fresh offer, amongst other improvement areas such as private label and ready-to-eat convenience foods, has continued to gain traction. The chain now operates 21 FreshX concept stores, up from 13 at this time last year. Through a combination of refurbishments and some new stores, we expect to grow the number of these formats by a further 21 next year, with the medium-term target of 80 stores in this new format unchanged. After opening a net 6 new stores, Checkers (excluding Hypers) ended the year with 219 stores in South Africa. Excluding the Hypers, a number of which were undergoing renovation during the year, Checkers grew overall market share, especially in its focus categories of fresh, convenience and prepared meals. The vulnerabilities of both the Shoprite and Usave customers, who rely on many food categories still in deflation, is evidenced in the more subdued sales growth reported by these two chains. After reporting sales growth of 1.2% for the first six months of the year, Shoprite grew sales for the year by 3.5%. It opened a net 17 new locations to end the year with a base of 488 South African stores. As our mainstay low price champion, Shoprite stayed true to its price leadership positioning as evidenced by reported market share gains in the most recent quarter. Given Usave’s significant Gauteng footprint and smaller ranges, it was most exposed to inventory shortages during and post our distribution centre strike. This, together with price deflation and a very constrained customer base, resulted in Usave reporting sales growth for the year of 0.8%. This low cost, limited assortment discount chain has stayed focused on its customer segment, opening a net 32 stores to end the year with 367 locations throughout South Africa. Liquorshop, spanning both the Checkers and Shoprite brands, reported 25.1% sales growth. It opened a net 44 new stores in South Africa this year.

Supermarkets Non-RSA

Supermarkets Non-RSA reported constant currency turnover growth of 0.9%, inclusive of a 12.2% decline in turnover at constant currencies in our Angolan operation. Rampant inflation in recent years has reduced spending power and, therefore, our ability to maintain gross margins, whilst foreign currency shortages and an increasingly onerous regulatory environment around the importation of products have hampered availability. Despite this, we have maintained operational excellence and opened a net eight new stores for the year. During the financial year, currencies of other large countries in which we trade, namely Zambia and Nigeria, also showed sharp declines against the US dollar of 29.4% and 17.9% respectively. This too had a negative impact on turnover growth. Across the 14 countries outside South Africa in which we operate, we estimate that internal food inflation averaged 3.3% for the current year. Supermarkets Non-RSA’s turnover declined with 7.7% to R21.3 billion, inclusive of a decline in Angola supermarkets of 38.4%. Supermarkets Non-RSA like-for-like sales declined with 11.9%.

Furniture

Despite challenging trading conditions, the Furniture division, inclusive of its Non-RSA business, increased turnover by 4.0% to R6.2 billion. As a result of the continued impact of the introduction of affordability assessments, credit participation reduced further to 12.7% of sales. In South Africa, OK Furniture closed a net 13 stores after accounting for four openings. House & Home closed six stores. On a net basis outside South Africa, the division added no stores.

Other Operating Segments

Other Operating Segments, which include OK Franchise, MediRite Pharmacy and Checkers Food Services, achieved pleasing growth of 10.0% with our franchise division’s growth benefiting from our stated strategy to build on this offer. Our rebranded OK Franchise opened a net 36 stores this year with the base now totalling 398 stores throughout South Africa. Outside South Africa, OK Franchise added a net 6 stores, with a base of 62 at year-end. Our total footprint includes 38 forecourt stores which are performing well. Gross profit Gross profit growth of 1.8% year-on-year to R35.3 billion, resulted in a gross margin of 23.5%. The South African businesses’ gross profit margin increased over the year, a considerable achievement in exceptionally difficult circumstances. Shrinkage once again remained well controlled.

Pieter Engelbrecht, chief executive officer:

Our core operations, Supermarkets RSA's sales growth of 4.9%, with like-for- like sales growth of 1.9%, is a performance significantly impacted by our well documented first half challenges. With the strike in the DC behind us, our team worked tirelessly to restore performance in the second half. It is pleasing to report that we ended the year with our final quarter's sales in Supermarkets RSA growing by 9.4%. Our in-stock levels are now higher than prior to our system implementation and without compromising on our low price leadership, we achieved a second half trading margin in Supermarkets RSA of 5.5%. We've continued with our growth strategy to capture a larger share of the premium food segment through the ongoing Checkers repositioning.

The number of Checkers stores in the new look FreshX format now totals 21. We are most pleased with returns from these upgrades and, therefore, our medium to long- term target of 80 stores in this format remains unchanged. Our focus on the core Shoprite and Usave customers, who we strive to serve with excellence daily, has remained strong as we continue to bring affordable food retail into the communities where our customers reside. Notwithstanding the much improved recent performance in our core Supermarkets RSA division, which generates 74.9% of our sales and grew second half sales by 7.4%, it was a testing year.

A constrained economy, inventory shortages post industrial action and the implementation of a new enterprise wide IT system across our store base resulted in lost sales. With affordability remaining the top priority for our customers, we unquestionably stood by our lowest price promise. Selling price inflation in our Supermarkets RSA division for the year measured only 1.2%, and similar to last year, we traded throughout the year with many items in key categories in deflation. At year-end, the number of products priced lower than last year measured at 9 679. Ongoing forex shortages, currency devaluations and the aftermath of rampant inflation in Angola and its ongoing impact on affordability took a further toll on our Non-RSA business. Supermarkets Non-RSA reported a trading loss of R265 million for the year. Despite no foreseen respite in short-term trading conditions in the region, we are committed to our customers in the 14 Non-RSA countries in which we operate.

We remain confident in the opportunity our entrenched position as Africa's leading food retailer will bring as the economic fortunes of the countries where we trade improve. Given the challenging global economic backdrop, we are remaining focused on growth opportunities in our home market, inclusive of our established African operations, rather than pursuing businesses in foreign geographies. Social responsibility has and always will be a priority for the Group. Amongst many initiatives focused on improving the lives of our fellow South Africans, it is noteworthy that this year we sold a record of 53 million subsidised deli meals and 58 million loaves of brown bread, both for under R5. We also created a further 3 175 employment opportunities whilst improving our focus on sustainability and governance. I am pleased to be able to say that we have the right people, resources and plans in place to entrench and grow our leading food retail position, both in South Africa and on the rest of the African continent and, therefore, to grow our profitability over the long term."

General comments obtained from the results

Supermarkets RSA

The Group’s core business, Supermarkets RSA, trading through 1 580 stores and representing 74.9% of Group sales achieved 4.9% sales growth for the period to report sales of R112.7 billion. Like-for-like growth measured 1.9% with internal selling price inflation of 1.2% up from only 0.3% last year. This full-year performance should be viewed in the context of a disappointing first half in which sales grew by only 2.6%, impacted by the completion of our multi-year ERP IT system re-platforming, as well as the aftermath of the May and June 2018 industrial action at our largest distribution centre in Gauteng. However, a much improved second half period in which sales increased by 7.4% on the back of better customer and volume growth, as well as an improvement in on-shelf availability and promotional effectiveness, leaves us confident in the restored strength of this division and its formats. Our Checkers supermarket chain, although also hampered by the availability issues that plagued the Group, was the better performing of our major food retail brands in RSA. Turnover growth, inclusive of its 37 larger format Hypers, was 4.6%. Its strategy to grow its share of spend in the mid-to-upper segment of the market by focusing on improving its fresh offer, amongst other improvement areas such as private label and ready-to-eat convenience foods, has continued to gain traction. The chain now operates 21 FreshX concept stores, up from 13 at this time last year. Through a combination of refurbishments and some new stores, we expect to grow the number of these formats by a further 21 next year, with the medium-term target of 80 stores in this new format unchanged. After opening a net 6 new stores, Checkers (excluding Hypers) ended the year with 219 stores in South Africa. Excluding the Hypers, a number of which were undergoing renovation during the year, Checkers grew overall market share, especially in its focus categories of fresh, convenience and prepared meals. The vulnerabilities of both the Shoprite and Usave customers, who rely on many food categories still in deflation, is evidenced in the more subdued sales growth reported by these two chains. After reporting sales growth of 1.2% for the first six months of the year, Shoprite grew sales for the year by 3.5%. It opened a net 17 new locations to end the year with a base of 488 South African stores. As our mainstay low price champion, Shoprite stayed true to its price leadership positioning as evidenced by reported market share gains in the most recent quarter. Given Usave’s significant Gauteng footprint and smaller ranges, it was most exposed to inventory shortages during and post our distribution centre strike. This, together with price deflation and a very constrained customer base, resulted in Usave reporting sales growth for the year of 0.8%. This low cost, limited assortment discount chain has stayed focused on its customer segment, opening a net 32 stores to end the year with 367 locations throughout South Africa. Liquorshop, spanning both the Checkers and Shoprite brands, reported 25.1% sales growth. It opened a net 44 new stores in South Africa this year.

Supermarkets Non-RSA

Supermarkets Non-RSA reported constant currency turnover growth of 0.9%, inclusive of a 12.2% decline in turnover at constant currencies in our Angolan operation. Rampant inflation in recent years has reduced spending power and, therefore, our ability to maintain gross margins, whilst foreign currency shortages and an increasingly onerous regulatory environment around the importation of products have hampered availability. Despite this, we have maintained operational excellence and opened a net eight new stores for the year. During the financial year, currencies of other large countries in which we trade, namely Zambia and Nigeria, also showed sharp declines against the US dollar of 29.4% and 17.9% respectively. This too had a negative impact on turnover growth. Across the 14 countries outside South Africa in which we operate, we estimate that internal food inflation averaged 3.3% for the current year. Supermarkets Non-RSA’s turnover declined with 7.7% to R21.3 billion, inclusive of a decline in Angola supermarkets of 38.4%. Supermarkets Non-RSA like-for-like sales declined with 11.9%.

Furniture

Despite challenging trading conditions, the Furniture division, inclusive of its Non-RSA business, increased turnover by 4.0% to R6.2 billion. As a result of the continued impact of the introduction of affordability assessments, credit participation reduced further to 12.7% of sales. In South Africa, OK Furniture closed a net 13 stores after accounting for four openings. House & Home closed six stores. On a net basis outside South Africa, the division added no stores.

Other Operating Segments

Other Operating Segments, which include OK Franchise, MediRite Pharmacy and Checkers Food Services, achieved pleasing growth of 10.0% with our franchise division’s growth benefiting from our stated strategy to build on this offer. Our rebranded OK Franchise opened a net 36 stores this year with the base now totalling 398 stores throughout South Africa. Outside South Africa, OK Franchise added a net 6 stores, with a base of 62 at year-end. Our total footprint includes 38 forecourt stores which are performing well. Gross profit Gross profit growth of 1.8% year-on-year to R35.3 billion, resulted in a gross margin of 23.5%. The South African businesses’ gross profit margin increased over the year, a considerable achievement in exceptionally difficult circumstances. Shrinkage once again remained well controlled.

Advertisement

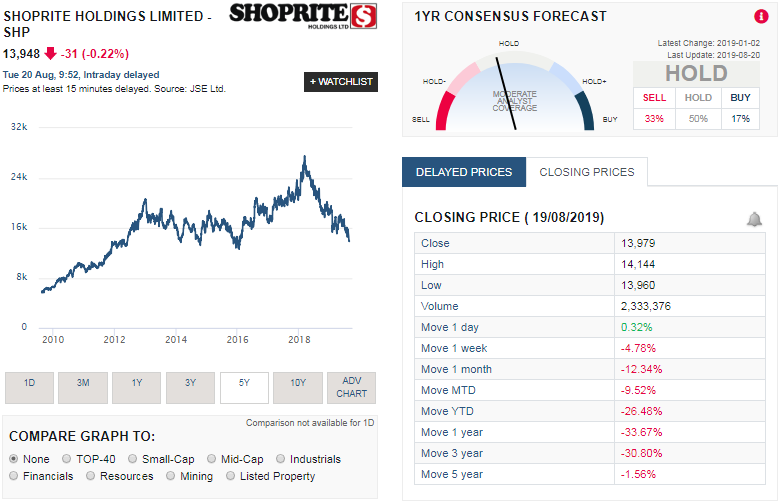

Share price performance

The screenshot below taken from Sharenet shows the share price performance of Shoprite (SHP) over the last 5 years. Below a summary of the performance of Shoprite (SHP) shares over various time periods:

- 1 week: -4.78%

- 1 month: -12.34%

- Year to date (YTD): -26.48%

- 1 Year: -33.67%

- 3 Years: -30.80%

- 5 Years: -1.56%

Shoprite (SHP) share price history

Valuation of Shoprite Holdings (SHP)

So what exactly are Shoprite (SHP) shares worth? Based on the groups latest financial results, their strong balance sheet and cash generation capacity, the decent margins they held on to during the tough economic climate, their cost containment measures and strong footprint across South Africa and the rest of Africa we value Shoprite shares at R143.98 a share