|

South Africa Reserve Bank holds REPO rate steady at March 2019 meeting

Date: 29 March 2019 Category: Economics |

Related Topics |

|

We take a quick look at the announcement by the South Africa Reserve Bank (SARB) monetary policy committee (MPC) announcement that the REPO rate has been kept unchanged which in turn means the prime lending rate used by banks remains unchanged. But what is the bank's expectations of longer term interest rates?

|

|

REPO rate on hold (for now)

So the MPC kept the repurchase rate (REPO) rate unchanged. For those who dont know what the REPO rate is, that is the interest rate at which the South Africa Reserve Bank (SARB) borrows money to regular banks at. Banks who borrow money to consumers at 350 basis points to the REPO rate to get the "prime lending rate". The prime lending rate is the interest rate at which banks offer debt to consumers with good clean credit records. the worse the credit record, the higher the rate of interest charged by the bank.

The REPO rate is used as a tool (a very crude indirect tool) to keep inflation within the bank's 3% to 6% range. As inflation goes up, the REPO rate is pushed up to curb consumer spending, less spending means less demand, and therefore stock moves more slowly, which will force retailers to cut prices to get rid of stock. This cutting of prices then slows down inflation.

Now this is all fair and good if inflation is caused by increased demand from consumers (this is called demand pull inflation). But if inflation is caused by factors outside the control of consumers (say strong electricity tariff increases from ESKOM, increased taxes on alcoholic beverages and tobacco, increased fuel and road accident fund levies or higher fuel prices which is caused by higher international oil prices or weaker exchange rate) then punishing consumers by raising interest rates to curb spending is the wrong way to go about slowing down inflation. As this type of inflation called cost push inflation will hardly be subdued by raising interest rates as consumers had little to nothing to do with causing this type of inflation.

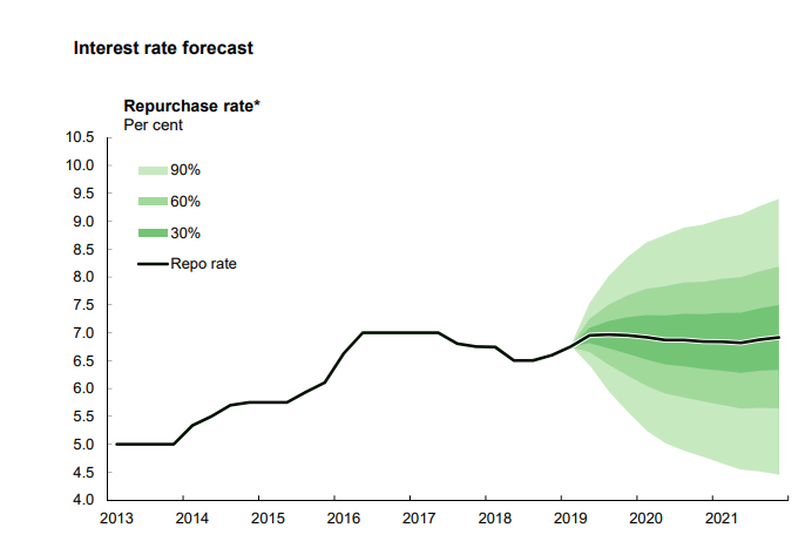

The bank provides a regularly updated forecast on where they expect inflation to be int he coming quarters and years, and recently started publishing a REPO fan chart showing where they expect the REPO rate to be over the next couple of quarters and years. Below an image of the latest REPO fan chart.

The REPO rate is used as a tool (a very crude indirect tool) to keep inflation within the bank's 3% to 6% range. As inflation goes up, the REPO rate is pushed up to curb consumer spending, less spending means less demand, and therefore stock moves more slowly, which will force retailers to cut prices to get rid of stock. This cutting of prices then slows down inflation.

Now this is all fair and good if inflation is caused by increased demand from consumers (this is called demand pull inflation). But if inflation is caused by factors outside the control of consumers (say strong electricity tariff increases from ESKOM, increased taxes on alcoholic beverages and tobacco, increased fuel and road accident fund levies or higher fuel prices which is caused by higher international oil prices or weaker exchange rate) then punishing consumers by raising interest rates to curb spending is the wrong way to go about slowing down inflation. As this type of inflation called cost push inflation will hardly be subdued by raising interest rates as consumers had little to nothing to do with causing this type of inflation.

The bank provides a regularly updated forecast on where they expect inflation to be int he coming quarters and years, and recently started publishing a REPO fan chart showing where they expect the REPO rate to be over the next couple of quarters and years. Below an image of the latest REPO fan chart.

The fan chart is a form of probability chart. The black line shows the REPO rate. The dark green band fanning out from the black line shows that the bank can say with 30% confidence that the REPO rate will be between the bottom and the top of the dark green band up towards the end of 2021. What the REPO line shows though is that the bank is expecting the REPO rate to come down slightly towards the end of 2019 and into early 2020. And only to make a slight uptick back to current levels towards the end of 2021. And according to the bank's projections the lightest green band shows that they are 90% confident that the REPO rate will be between 4.5% and 9% from now up to the end of 2021.

We do expect the bank to cut rates at least once leading up to the end of 2020, basically to fix the interest rate hike of November 2018 meeting. A meeting where they should never have raised interest rates in the first place. It had little to no effect in curbing inflation (as inflation dropped significantly after November 2018 due to massive declines in the Petrol price, remember cost push inflation mentioned earlier). All that interest rate increase did was place a lot of consumers under a lot more financial strain and stress with millions of consumers having to pay more on interest on vehicle loans, personal loans, credit cards, mortgage loans, student loans etc.

The bank should think about the drivers of inflation, and take note of the fact that due to slow economic growth, inflation is largely driven by cost factors and not consumer demand, and if this is the case, they should think twice about raising rates to curb consumer spending to lower inflation, especially when it is not consumer spending and demand that is leading to increased inflation.

We do expect the bank to cut rates at least once leading up to the end of 2020, basically to fix the interest rate hike of November 2018 meeting. A meeting where they should never have raised interest rates in the first place. It had little to no effect in curbing inflation (as inflation dropped significantly after November 2018 due to massive declines in the Petrol price, remember cost push inflation mentioned earlier). All that interest rate increase did was place a lot of consumers under a lot more financial strain and stress with millions of consumers having to pay more on interest on vehicle loans, personal loans, credit cards, mortgage loans, student loans etc.

The bank should think about the drivers of inflation, and take note of the fact that due to slow economic growth, inflation is largely driven by cost factors and not consumer demand, and if this is the case, they should think twice about raising rates to curb consumer spending to lower inflation, especially when it is not consumer spending and demand that is leading to increased inflation.