|

Related Topics |

|

We take a look at the latest South African Reserve Bank (SARB) Monetary Policy Review presentation as at 6 April 2020. The latest monetary policy review from the South African Reserve Bank contains estimates of their expected impact from the Coronavirus on South Africa's unemployment, inflation and economic growth.

|

|

What is the South African Reserve Bank Monetary Policy Review?

Twice a year the South African Reserve Bank published a monetary policy review presentation which gives a broad overview of global financial markets as well as a global economic overview. The reason for this is the fact that South Africa's monetary policy is influenced by a whole host of factors which includes what is happening in local and foreign markets. The first slide of their MPR presentation starts with the heading "Having monetary policy space, and using it "

- COVID-19 biggest shock to global economy since Lehman Brothers’ bankruptcy

- SA economy likely to contract this year, by at least 2%

- Monetary policy has space to respond, given lower inflation

- Stronger recovery needs “bridging” and longer-run fixes

Advertisement

The main news story in recent weeks and months has been the Coronavirus and its impact on global economic growth as large parts of the world being under some for of lockdown, or self isolation or quarantine. The big question is just what will the economic impact of the Coronavirus pandemic be. And closer to home the question is what impact Coronavirus will have on South Africa's economy. The South Africa Reserve Bank (SARB) in their latest monetary policy review looked at the potential impact of the Coronavirus on South Africa inflation rate, job losses, economic growth, business closures and more.

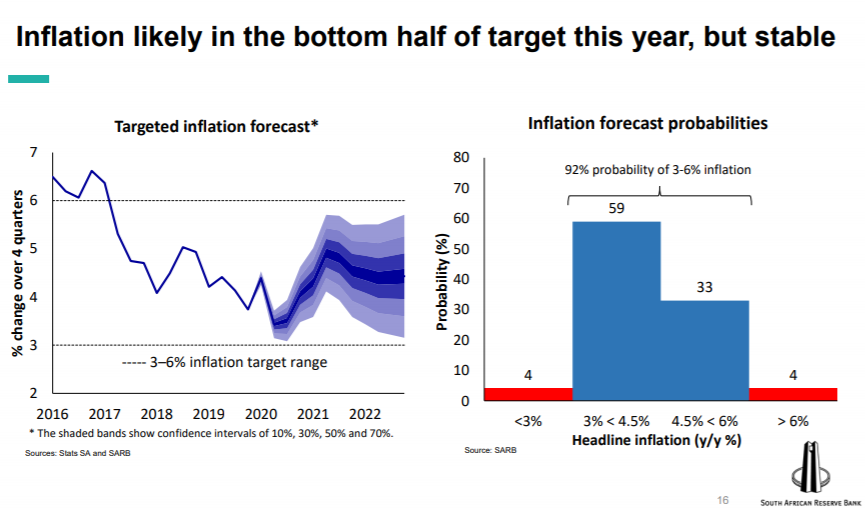

The image below shows SARB's expectations for South Africa's inflation rate up to the end of 2022. According to the bank there is a 59% chance that the inflation rate will average between 3% and 4.5% during this period.

The image below shows SARB's expectations for South Africa's inflation rate up to the end of 2022. According to the bank there is a 59% chance that the inflation rate will average between 3% and 4.5% during this period.

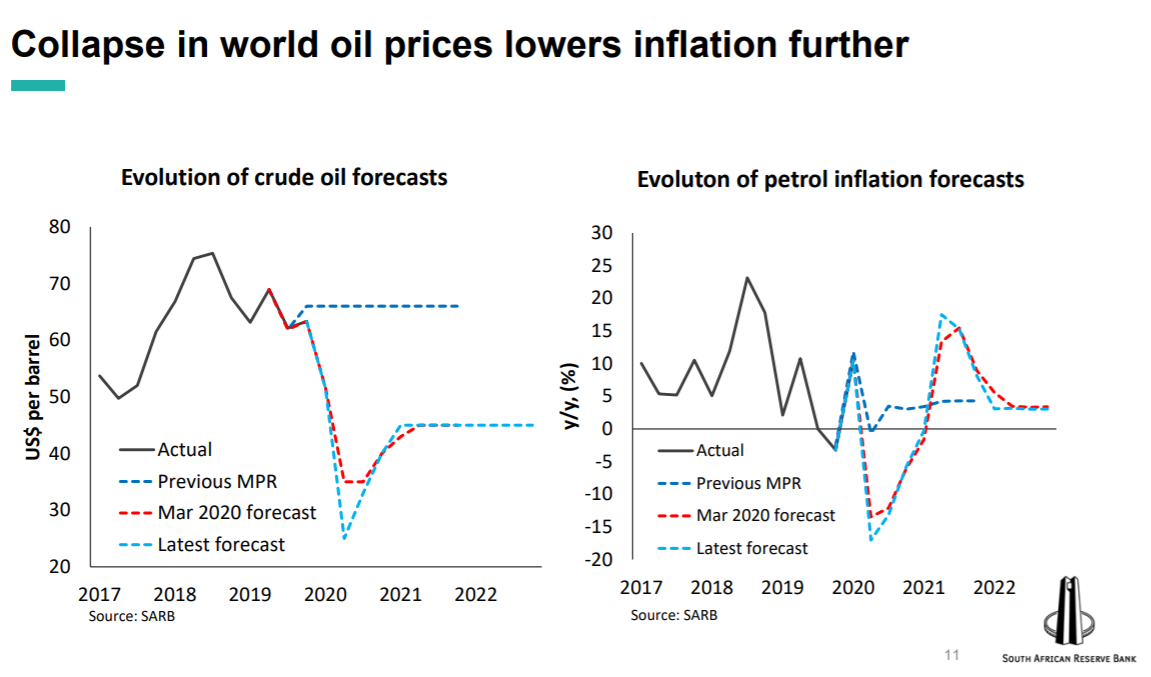

One of the reasons the inflation expectations of SARB is towards the lower end of the inflation target is the fact that world oil prices collapsed due to a price war being waged by Russia and Saudi Arabia. Even with South Africa's extremely weak currency right now (due to a capital flight away from riskier assets and Moody's rating South Africa's bonds as sub investment grade or "junk status") the price per barrel in Rand terms is far cheaper than it has been in recent years. And fuel prices is one of the major drivers of inflation as fuel carries a relative large weight in the CPI and almost all goods that are transported to wholesalers and retailers is done via delivery vehicles, which use fuel. The higher the fuel prices the higher the cost to transport goods to wholesalers and retailers, and those wholesalers and retailers will look to offset the higher fuel costs by charging more for products in order to cover increased costs of fuel, and by raising prices to cover additional costs the inflation rate increases.

The image below shows SARB's crude oil and petrol inflation forecasts. Forecasts include their last monetary policy review, their March 2020 MPC meeting and their latest forecast as per the April 2020 monetary policy review.

The image below shows SARB's crude oil and petrol inflation forecasts. Forecasts include their last monetary policy review, their March 2020 MPC meeting and their latest forecast as per the April 2020 monetary policy review.

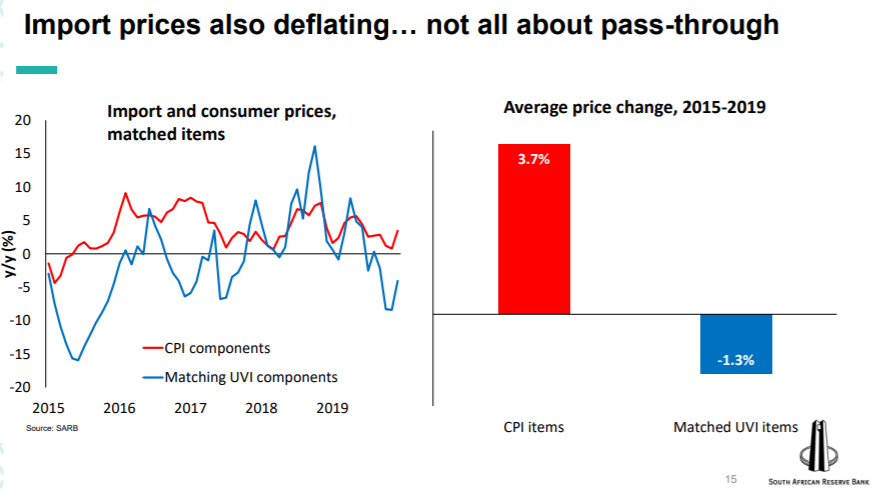

Mentioning the weak exchange rate, the worry with the weakening exchange rate is the fact that import inflation might increase due to the weaker exchange rate. But as the image below shows the unit value indices (derived prices from SARS customs data) shows that import price are actually deflating and that items imported that matched items in the CPI basket actually declined by -1.3% per year since 2015, while the local items in the CPI basket increased by 3.7% per year over the last 5 years. So import inflation is not really something to worry about right now

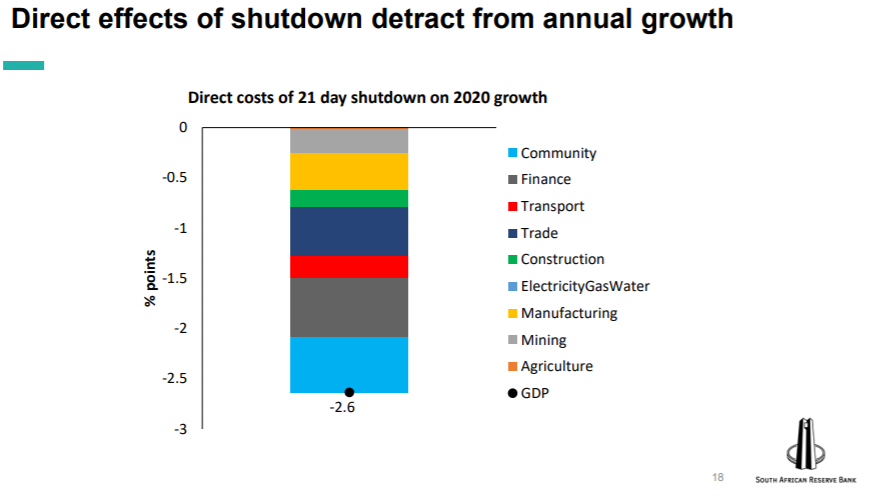

So what is the direct impact of the 21 day lockdown on South Africa's economy and its economic growth. According to the South African Reserve Bank the direct impact of the 21 day lockdown in South Africa is -2.6% off of South Africa's annual economic growth. Basically assuming the economy would have grown at 0% this year, the effect of the 21 day lockdown is that it will make South Africa's economy shrink by 2.6%. Big losses in community (government sector), trade (wholesale,retail and motor trade) and the finance industry. Less transactions taking place, less ATM withdrawals so less fees earning by the finance sector

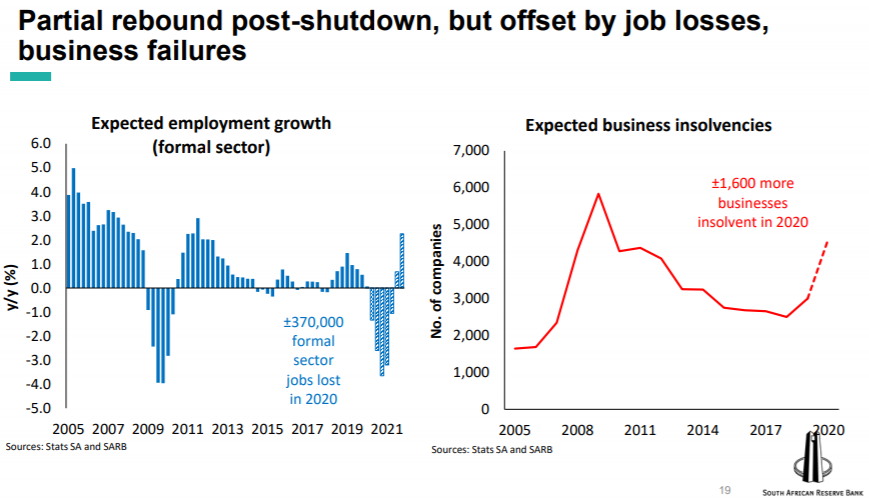

So the impact of the decline in economic activity on businesses and employment? The image below shows SARB's expectations in terms of formal sector job losses during 2020 as well as the expected business insolvencies during 2020.

So the South African Reserve Bank is expecting around 370 000 job losses in the formal sector while it expects around 1 600 businesses to become insolvent in 2020. Both of these numbers should be big concern for all South Africa's, be it government, business or citizens. This will hit the South Africa economy and its citizens hard.

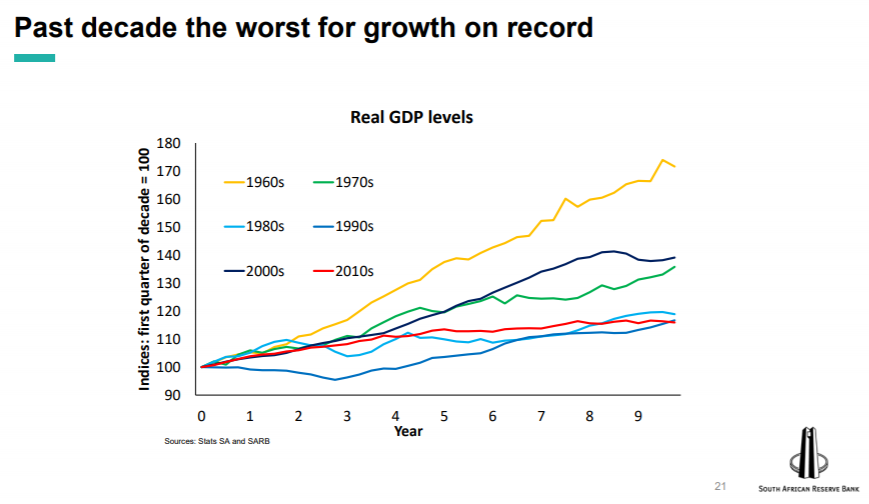

While the expected impact of Coronavirus on South Africa's economy, businesses and employment levels the fact is the South Africa economy has been in a bad place for a while now. The image below shows that the real growth (growth after removing the effects of inflation) over the last decade is the worst on record for South Africa.

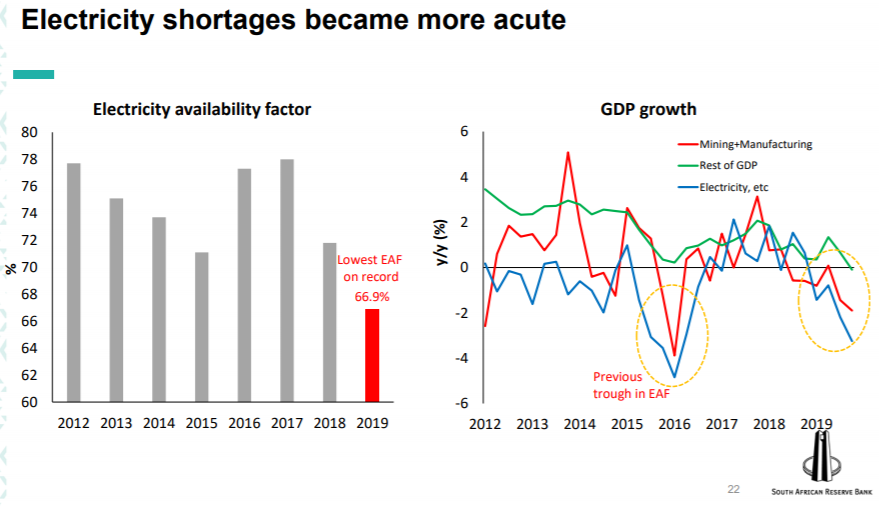

A big part of the growth problems in South Africa is ESKOM, and its inability to supply reliable consistent power to all users including big mines and manufacturers. And the image below shows the drag a lack of consistent available, reliable power has on mining and manufacturing.

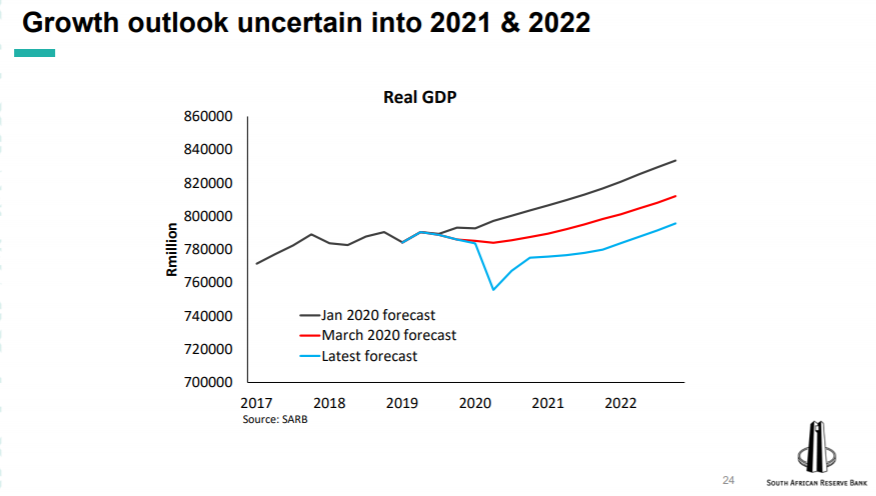

With the 10 year government bond yield offering almost 4% real return a year, the government is paying a hefty premium to borrow money. And as their fiscal position deteriorates further the premium demanded will increase. The South African government is caught in a debt trap that they have no idea how to get out of. One of the main reasons for the state's poor fiscal position is ESKOM, and they have a significant impact on the potential and achieved growth of the South African economy. The image below shows the potential and actual growth for South Africa over the lat 10 years

And with the South African economy struggling and being down in the doldrums, the South African government cannot really help, as its fiscal position is very weak (with it having to borrow to fund its expenditure programs as it cannot afford it with collected taxes alone) and the Coronavirus has led to greater risk aversion, which means the spread emerging markets such as South Africa has to pay to lure investors to lend money to countries such as South Africa increased sharply. The image below shows the yield spread between a 2 year government bond and 30 year bond. With the spread spiking significantly over the last couple of months. So it will cost the South African government a lot more to borrow money as the yield spread is so high now. And with increased cost of borrowing less will be going to expenditure programs and more will be going towards servicing debt, which means government can't really assist to pull the South African economy out of its lul. And if government cannot stimulate demand then it should implement business friendly to let the private sector fuel growth. But in recent years the policies implemented has not been pro business so businesses not the driver of economic growth either and that's why South Africa's economy is just spinning its wheels.

The below is the summary provided by the Monetary Policy Review for their April 2020 review:

- COVID-19 a major shock to already weak economy

- Monetary policy space opened, despite currency weakness

- Ease the cost of adjustment, “bridging” to recovery

- Broader reforms crucial for improving growth