|

South African Reserve Bank Monetary Policy Review Presentation

Date: 23 April 2019 Category: Economics |

Related Topics |

|

We take a look at the latest Monetary Policy Review presentation made available by the South African Reserve Bank (SARB), who is responsible for setting monetary policy. For the man on the street, SARB is responsible for setting base line interest rates in South Africa which banks then use to derive the prime lending rate and what they offer clients based on their risk profile

|

|

Monetary Policy Review

The South African Reserve Bank (SARB) is responsible for setting South Africa's monetary policy. This includes the cash reserve requirements (how much of total cash and loans issued that banks need to keep as safety net etc. But SARB monetary policy large revolves around its inflation targeting mandate. SARB is responsible for ensuring South Africa's inflation rate remains between 3% and 6% range. Quiet arbitrary numbers that no on knows how SARB decided on but that is a discussion for another day. The main tool used by the SARB Monetary Policy Committee (MPC) to influence the inflation rate is interest rates. Unfortunately it is a very ineffective and crude tool to use to try and keep inflation within the 35 and 6% range. The theory is that if inflation increases the SARB MPC raises interest rates, which deminishes consumer's available spending funds as more money is spent on paying off debt. This diminished spending funds will imply consumers spend less, and retailers and wholesalers will struggle to move their stock unless they stop increasing prices, or increase it a slower rate, or cut prices all together. And this will then see recorded inflation levels decline.

But what happens when consumers are being punished by having to pay higher interest rates when they are not the cause of the higher inflation rate? In South Africa for example increased taxes on alcohol and tobacco, or the increased fuel levy and road accident fund levy set on fuel prices, or massive tariff increases by ESKOM and municipalities. All of these factors push up inflation and none of them caused by consumers. So by raising interest rates consumers are "punished" for factors outside their control. Not only that raising interest rates reduces economic growth, of which South Africa has very little. So in cases where fiscal policy (government spending) is increasing and trying to boost the economy, if monetary policy raises interest rates it counter acts the attempts by fiscal policy to grow the economy. See more on Monetary Fiscal Policy Mix here.

But what happens when consumers are being punished by having to pay higher interest rates when they are not the cause of the higher inflation rate? In South Africa for example increased taxes on alcohol and tobacco, or the increased fuel levy and road accident fund levy set on fuel prices, or massive tariff increases by ESKOM and municipalities. All of these factors push up inflation and none of them caused by consumers. So by raising interest rates consumers are "punished" for factors outside their control. Not only that raising interest rates reduces economic growth, of which South Africa has very little. So in cases where fiscal policy (government spending) is increasing and trying to boost the economy, if monetary policy raises interest rates it counter acts the attempts by fiscal policy to grow the economy. See more on Monetary Fiscal Policy Mix here.

So having set the scene in terms of the importance of monetary policy and getting it right, by ensuring interest rates are only raised or cut when absolutely necessary, lets take a look at the Monetary Policy Review Presentation released by the SARB.

In their first slide it boldly states: April 2018 review: Towards permanently lower inflation as the heading. They then have the following bullets on this first slide:

• Global growth slowdown, monetary tightening deferred

• SA growth modestly higher over medium term, but trend rate low

• Near‐term inflation slower, largely due to helpful shocks

• Interest rate path keeping longer‐term inflation close to midpoint

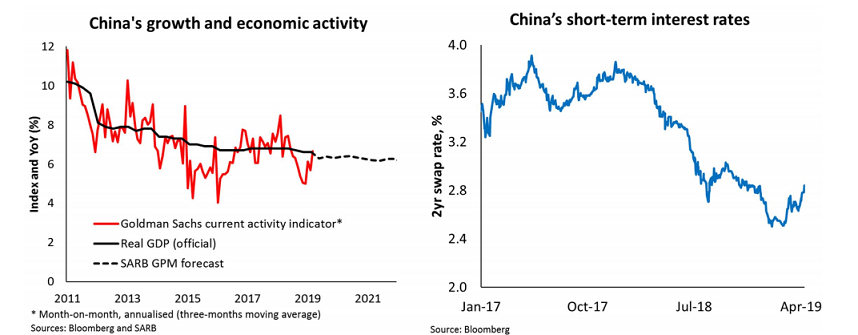

The image below shows SARB's project of China's growth, which is the main contributor to a slowdown in global growth as mentioned in bullet 1 above

• Global growth slowdown, monetary tightening deferred

• SA growth modestly higher over medium term, but trend rate low

• Near‐term inflation slower, largely due to helpful shocks

• Interest rate path keeping longer‐term inflation close to midpoint

The image below shows SARB's project of China's growth, which is the main contributor to a slowdown in global growth as mentioned in bullet 1 above

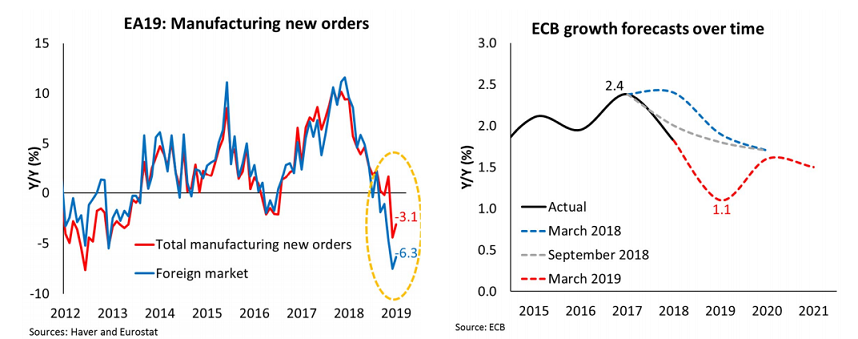

The next image shows some of the slowing growth in China spilling over into Europe has new manufacturing order decline year on year. It also shows the ECB's growth forecast for the EU over various periods and it highlights the share decline in the latest growth forecast compared to prior forecasts.

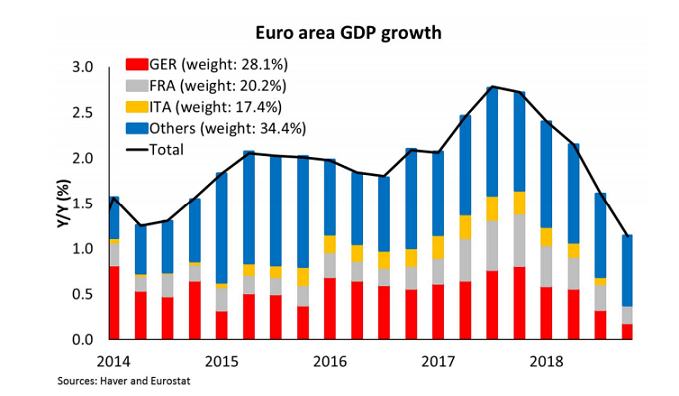

The image below shows Euro area growth with the following weights assigned to various of the larger Euro area countries:

- Germany: 28.1%

- France: 20.2%

- Italy: 17.4%

- Other: 34.4%

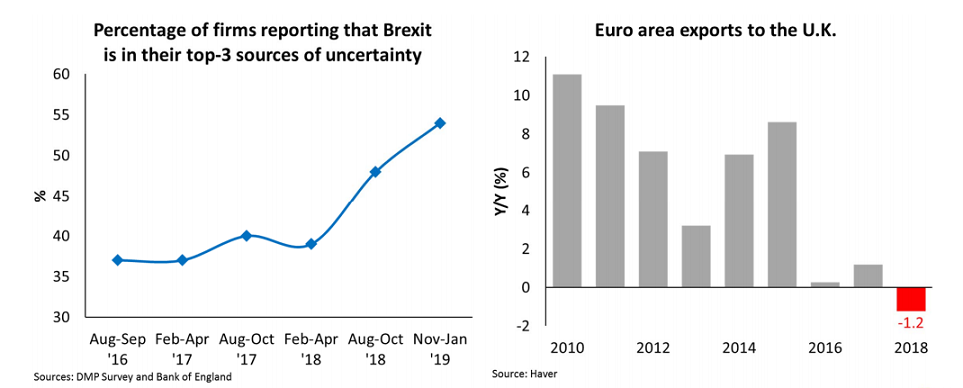

Of course Brexit uncertainty another cause for concern and possibly holding back growth rates not only in the UK and EU but the global economy. The image below shows two graphics. One graphic shows percentage of firms reporting Brexit as one of their Top 3 sources of uncertainty, the other graphic shows EU area exports to the UK.

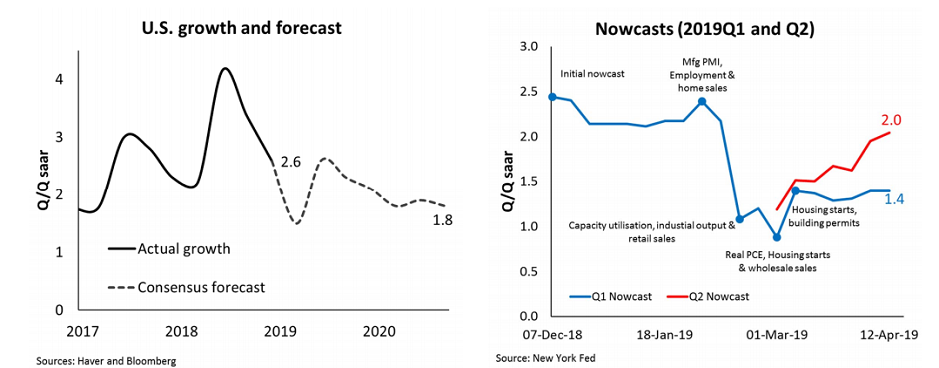

Now shifting focus to the world's biggest economy. The United States. Their rampant growth has started to slow down, and some of the growth was fueled by tax cuts which most believed mostly benefited the rich and well off. Based on Haver and Bloomberg consensus forecasts it looks like US economic growth is set to moderate quiet a bit in the next few years.

So what has all this got to do with South Africa's monetary policy you ask? Well South Africa is a small open economy (open in this case meaning we import and export a lot of goods and services). So demand for goods in the rest of the world has a significant impact on our exports and the price we pay for imports. If demand for goods we import is very strong in other countries it will push prices up which means our levels of inflation will be higher. So when looking at monetary policy a large host of external factors has to be considered.

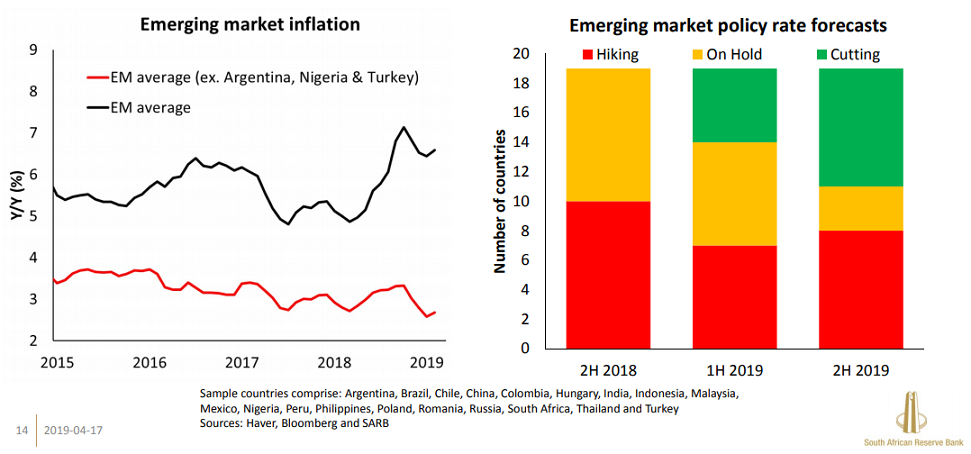

So focusing on emerging market (EM) inflation levels and the current monetary policy stance of a large number of EM countries we see the following

So focusing on emerging market (EM) inflation levels and the current monetary policy stance of a large number of EM countries we see the following

Looking at the red line, which the average inflation rate for EM countries excluding Argentina, Nigeria and Turkey as these countries have temporary hyper and higher than usual inflation levels due to political unrest etc, we see that the average inflation rate of EM countries have tended lower. And the bar chart to the right shows that in 2nd half of 2018 EM central banks where basically split between hiking interest rates or holding steady. In the first half of 2019 we see that about 20% of EM central banks are considering cutting rates, and by the 2nd half of 2019 it looks like almost half the EM central banks are considering cutting interest rates due to it tending lower. So what is the inflation expectations of South Africa and some of South Africa's BRICS partners such as Brazil, India over the next year?

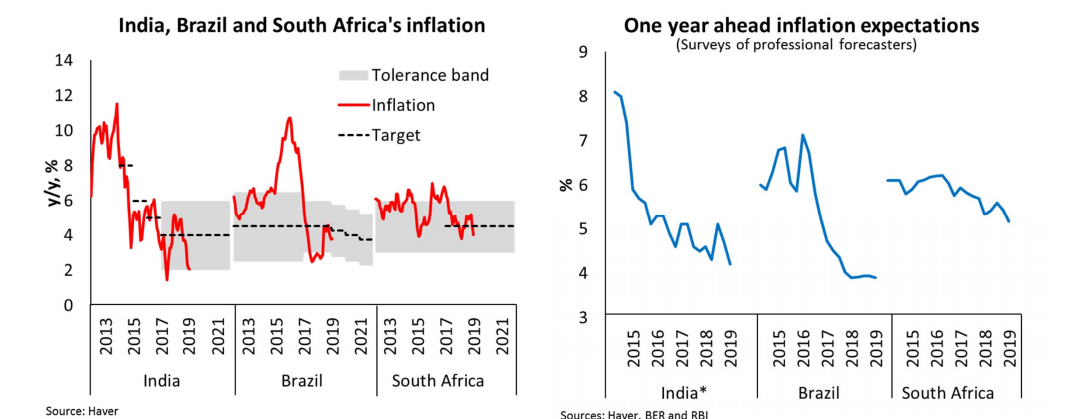

As the image above shows that India, Brazil and South Africa's inflation rates are all tending lower and currently all three are within their "tolerance" or inflation target bands. Lets hope for ailing South African consumers and the South African economy, South Africa gets to see a interest rate cut to relieve some of the financial pressures most households find themselves under. A short while ago we published an article regarding South Africa's household debt and the debt servicing costs that are busy drowning South African consumers.

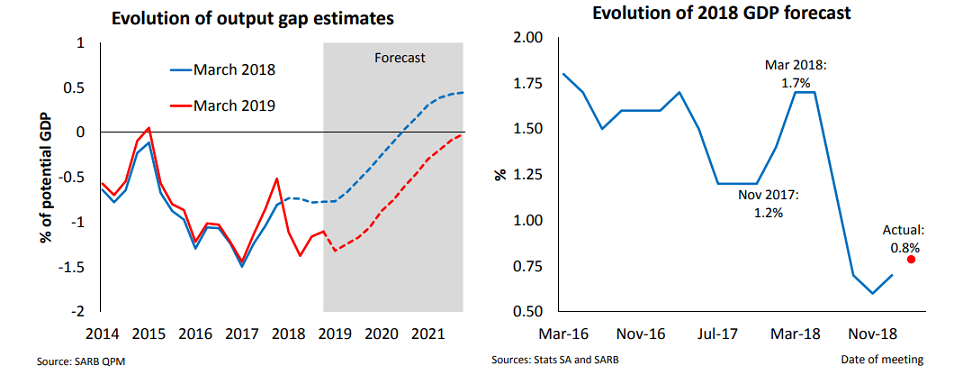

Talking about ailing economy, the image below shows South Africa's output gap over time as well as the evolution of South Africa's 2018 growth forecast over time

Talking about ailing economy, the image below shows South Africa's output gap over time as well as the evolution of South Africa's 2018 growth forecast over time

The image to right shows that in March 2016, the South African Reserve Bank forecasted South Africa's economy to grow at 1.8% , in November 2017 it forecasted it to grow at 1.2%, and eventually growth ended up being 0.8% for 2018. A constant decline in the forecast and actual growth achieved by the South African economy, and this while the population grows at a rate of closer to 2% a year. Basically South Africa's economic pie is growing slower than the population, which means per citizen we are actually worse off every year that the population grows at a rate faster than the economy. You wont hear that in the ANC election campaign and electioneering currently going on.

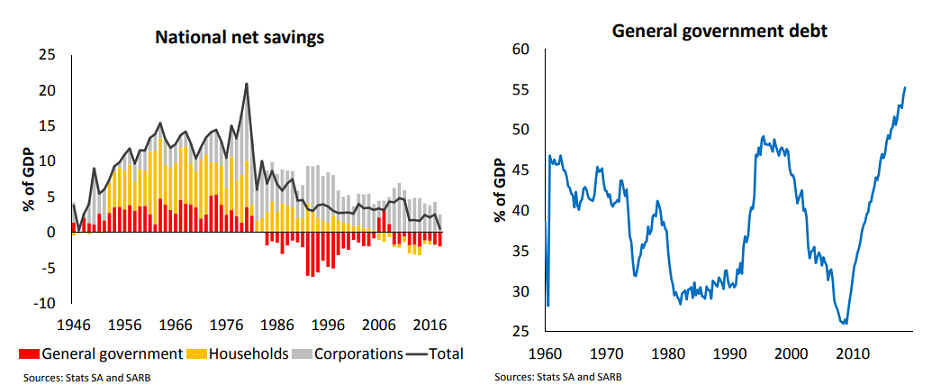

Another big problem for the South African economy is the fact that net saving by citizens are declining, debt increasing, and added to that government debt is also ballooning.

Another big problem for the South African economy is the fact that net saving by citizens are declining, debt increasing, and added to that government debt is also ballooning.

The South African government will find it hard to stimulate the economy or fund its spending programs in future as more and more of tax money collected by the State goes towards paying off its ballooning debt. And consumers as mentioned earlier are taking on more and more debt and saving less and less. All of which affects available funds to spend in the economy right now, and this is part of the reason for lackluster economic growth in SA. Debt is the anchor that is holding down the boat. It is tying household funds into paying off debt instead of investing, spending or saving.

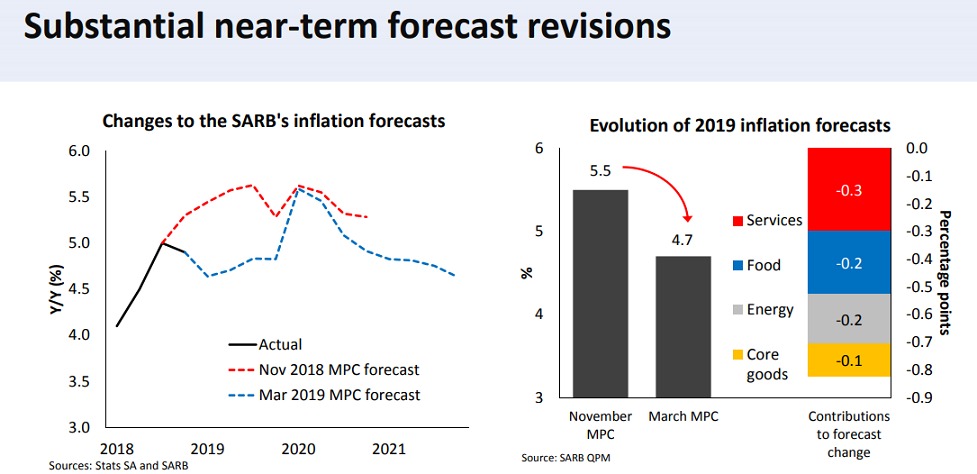

And lastly lets take a look at what the SARB themselves call substantial near-term forecast revisions. (As we have complained a thousand times before, SARB's forecasting is not very good. The image below shows the slide discussing the substantial near-term revisions of their forecast of inflation

And lastly lets take a look at what the SARB themselves call substantial near-term forecast revisions. (As we have complained a thousand times before, SARB's forecasting is not very good. The image below shows the slide discussing the substantial near-term revisions of their forecast of inflation

So in November 2018 the forecasted inflation for 2019 was at 5.5%. Come March 2019 SARB is currently forecasting 2019 inflation to be at 4.7% and states that the largest contributor to the strong downward revision of their 2019 inflation forecast is the cost of services. So are services prices which tend to come down more slowly than the prices of goods (a phenomenon known as sticky prices) finally starting to tend lower? It certainly looks like it based on the graphic above from SARB. But as we said we dont think they very good forecasters so we wouldn't hold our breath just yet. Lets wait and see. And it seems this is the SARB MPC approach to interest rates too now. Lets keep rates stead and wait and see what happens.