|

Related Topics |

|

We take a look at the financial stability review, first edition 2019, published by the South African Reserve Bank (SARB), who is ultimately responsible for financial stability in South Africa.

|

|

What is financial stability?

According to the publication by the SARB, the purpose of the financial stability review and the definition of financial stability are discussed below

Purpose of the Financial Stability Review

The primary objective of the South African Reserve Bank (SARB) is to protect the value of the currency in the interest of balanced and sustainable economic growth in South Africa. In addition to this, the SARB’s function and mandate of protecting and enhancing financial stability in the Republic of South Africa is affirmed in the Financial Sector Regulation Act 9 of 2017 (FSR Act).

In pursuit of this objective, and to promote a stable financial system, the SARB publishes a semiannual Financial Stability Review. The publication aims to identify and analyse potential risks to financial system stability, communicate such assessments, and stimulate debate on pertinent issues. The SARB recognises that it is not the sole custodian of financial system stability, but that it contributes significantly towards and coordinates a larger effort involving government, other regulators, self-regulatory agencies, and financial market participants.

Defining ‘financial stability’

Financial stability is not an end in itself but, like price stability, is generally regarded as an important precondition for sustainable economic growth, development, and employment creation. Financial stability refers to a financial system that is resilient to systemic shocks, facilitates efficient financial intermediation, and mitigates the macroeconomic costs of disruptions in such a way that confidence in the system is maintained.

Purpose of the Financial Stability Review

The primary objective of the South African Reserve Bank (SARB) is to protect the value of the currency in the interest of balanced and sustainable economic growth in South Africa. In addition to this, the SARB’s function and mandate of protecting and enhancing financial stability in the Republic of South Africa is affirmed in the Financial Sector Regulation Act 9 of 2017 (FSR Act).

In pursuit of this objective, and to promote a stable financial system, the SARB publishes a semiannual Financial Stability Review. The publication aims to identify and analyse potential risks to financial system stability, communicate such assessments, and stimulate debate on pertinent issues. The SARB recognises that it is not the sole custodian of financial system stability, but that it contributes significantly towards and coordinates a larger effort involving government, other regulators, self-regulatory agencies, and financial market participants.

Defining ‘financial stability’

Financial stability is not an end in itself but, like price stability, is generally regarded as an important precondition for sustainable economic growth, development, and employment creation. Financial stability refers to a financial system that is resilient to systemic shocks, facilitates efficient financial intermediation, and mitigates the macroeconomic costs of disruptions in such a way that confidence in the system is maintained.

Overview

The South African Reserve Bank (SARB) regularly assesses the risks to financial stability with a view of identifying and mitigating any vulnerabilities that may be present in the domestic financial system. The identified risks, which form part of the SARB’s assessment, include:

(i) a deteriorating domestic fiscal position, exacerbated by, among other things, weak domestic growth, a poor revenue outlook, deteriorating debt dynamics and the fragile financial positions of state-owned enterprises (SOEs);

(ii) spillovers from weaker global economic growth, mostly emanating from a slowdown in Europe and China, an escalation of trade tensions and the prospect of a no-deal Brexit;

(iii) the possibility of renewed and unexpected tightening in global financial conditions, which in turn could result in a rapid repricing of risk. A disconnect between market expectations and the implemented policy of major central banks could raise the risk of a sudden market correction, which, if combined with a deterioration in market sentiment, could have a significant negative impact on financial market conditions in South Africa and ultimately on economic growth; and

(iv) rising cyber dependency and security risks attributed to increasing digital interconnection of people, systems and organisations. Cyberattacks could have direct material consequences for institutions through financial losses as well as indirect costs such as diminished reputation.

Given South Africa’s high level of interconnectedness with the global financial system, weaker global economic activity could lead to negative spillovers into the domestic economy and financial system through the trade, financial and investment channels. South Africa’s economy expanded by 1.4% in the fourth quarter of 2018, with GDP averaging 0.8% for the year. The country’s growth outlook remains weak in the near term, but is expected to recover over the medium term. Besides being negatively affected by exogenous factors, domestic growth is expected to face headwinds from a deteriorating fiscal position and persistent weakness in some significant SOEs, electricity supply constraints, high unemployment and low business confidence. The SARB’s latest forecast for domestic growth is 1.0% in 2019 (down from 1.3% previously). The forecast for 2020 is 1.8% (from 2.0%), rising to 2.0% in 2021 (from 2.2%).

Global risk sentiment deteriorated during the fourth quarter of 2018, reflecting concerns about slowing global growth, tightening global financial conditions and uncertainty on trade relations between the United States (US) and China, as well as Brexit. However, sentiment towards risky assets improved significantly since late December 2018, mostly owing to a pivot by major central banks to a more dovish monetary policy stance. As a result, most risky assets recorded notable gains since the beginning of 2019 and measures of volatility declined to multi-year lows. Emerging markets with strong fundamentals benefited from the positive sentiment, as reflected in narrower credit default swap spreads. A risk to this positive scenario is that, should US economic growth and inflation surprise to the upside, this could likely result in a renewed tightening of global financial conditions and a subsequent repricing of risk that could negatively impact on emerging markets, as witnessed in 2018. In addition, some emerging markets remain vulnerable to idiosyncratic risks. In South Africa, gains in financial asset prices were limited by the worsening of public sector finances and the risk of further sovereign credit rating downgrades to subinvestment grade.

The banking sector remains well capitalised at levels considerably above the minimum regulatory requirement. Impaired advances have continued to increase since January 2018 due to a combination of the implementation of the new expected credit loss accounting standard, International Financial Reporting Standard (IFRS) 9, and the deterioration in the credit quality of selected corporate and retail loan categories. In the current extended period of low economic growth, credit risk can arise from increasing financial stress in corporates and small- and medium-sized entities (SMEs) as well as households affected by job losses and/or deteriorating disposable income. The construction, manufacturing, wholesale and retail trade, and private household sectors exhibited the highest growth in default ratios since September 2017. Although not always indicative of the trend in the sector, the return on equity and assets of smaller banks has been declining (since May 2018) as a result of the reduction in non-interest income and increases in credit losses and operating expenses. By contrast, the return on equity and assets of the five largest banks increased marginally as their more diversified income streams provide additional resilience to profitability.

The financial position of households remains weak due to a combination of lower disposable income, a decline in net wealth and a significant increase in household debt. Overall, while there are concerns about the ability of households to service their debt, interest rates have remained relatively stable, thereby providing the sector with some relief.

Corporate profitability rose slightly in the 4th quarter of 2018. However, overall, profitability has been on a downward trend since the first quarter of 2018 due to subdued economic conditions and a sharp slowdown in the growth of non-financial corporate deposits. There has also been a slowdown in gross fixed capital formation, which could lead to lower economic growth prospects, further impeding profitability. Fiscal sustainability remains an important factor for South Africa’s sovereign credit rating. As a percentage of gross domestic product (GDP), government debt has doubled over the past 10 years, but remains below the 70% threshold level identified as high risk by the International Monetary Fund (IMF). Key fiscal metrics have continued to deteriorate during the reporting period and fiscal consolidation efforts have been hindered by debt-burdened SOEs that have struggled to meet their debt obligations. This adds to the probability of these contingent liabilities materialising on government’s balance sheet, thereby negatively impacting government debt levels. Eskom was recently granted a cumulative R69 billion over three years in support of its financial position. Despite the financial support, Eskom’s balance sheet remains stressed and continues to pose a systemic risk to the country’s economy. For the period under review, there have been a number of legislative and regulatory initiatives that, once implemented, could enhance the resilience of the South African financial system. These include the release, for public comment, of the Conduct of Financial Institutions Bill and the proposed Financial Matters Amendment Bill.1 The review of the National Payment System Act 78 of 1998 to take into account changes in the payment landscape and to align the regulation of the payment system to international best practice is also underway. The national payment system (NPS) plays a critical role in the settlement of domestic and international payment transactions and is key to a stable financial system

In conclusion, since the previous edition of the Financial Stability Review (FSR), global economic growth has slowed, and medium-term risks remain tilted to the downside. More recently, indications of continued less restrictive monetary policy by central banks in advanced economies, against a backdrop of slowing global growth, have led to easier financial conditions which supported global risk sentiment. Aside from being affected by exogenous factors through trade, investment and financial channels, South Africa’s growth prospects will be affected by domestic policy setting and idiosyncratic risks, reflected in the deterioration of a number of key indicators. Despite these challenges, the South African financial system continues to efficiently facilitate financial intermediation and mitigate negative spillovers and disruptions. Overall, the financial sector remains strong and stable, even with some headwinds from increased uncertainty around global economic policy, a challenging low domestic economic growth environment and persistent fiscal risks. The South African financial sector is also characterised by well-regulated, highly-capitalised, liquid and profitable financial institutions, supported by a robust financial infrastructure and strong regulatory and supervisory frameworks.

(i) a deteriorating domestic fiscal position, exacerbated by, among other things, weak domestic growth, a poor revenue outlook, deteriorating debt dynamics and the fragile financial positions of state-owned enterprises (SOEs);

(ii) spillovers from weaker global economic growth, mostly emanating from a slowdown in Europe and China, an escalation of trade tensions and the prospect of a no-deal Brexit;

(iii) the possibility of renewed and unexpected tightening in global financial conditions, which in turn could result in a rapid repricing of risk. A disconnect between market expectations and the implemented policy of major central banks could raise the risk of a sudden market correction, which, if combined with a deterioration in market sentiment, could have a significant negative impact on financial market conditions in South Africa and ultimately on economic growth; and

(iv) rising cyber dependency and security risks attributed to increasing digital interconnection of people, systems and organisations. Cyberattacks could have direct material consequences for institutions through financial losses as well as indirect costs such as diminished reputation.

Given South Africa’s high level of interconnectedness with the global financial system, weaker global economic activity could lead to negative spillovers into the domestic economy and financial system through the trade, financial and investment channels. South Africa’s economy expanded by 1.4% in the fourth quarter of 2018, with GDP averaging 0.8% for the year. The country’s growth outlook remains weak in the near term, but is expected to recover over the medium term. Besides being negatively affected by exogenous factors, domestic growth is expected to face headwinds from a deteriorating fiscal position and persistent weakness in some significant SOEs, electricity supply constraints, high unemployment and low business confidence. The SARB’s latest forecast for domestic growth is 1.0% in 2019 (down from 1.3% previously). The forecast for 2020 is 1.8% (from 2.0%), rising to 2.0% in 2021 (from 2.2%).

Global risk sentiment deteriorated during the fourth quarter of 2018, reflecting concerns about slowing global growth, tightening global financial conditions and uncertainty on trade relations between the United States (US) and China, as well as Brexit. However, sentiment towards risky assets improved significantly since late December 2018, mostly owing to a pivot by major central banks to a more dovish monetary policy stance. As a result, most risky assets recorded notable gains since the beginning of 2019 and measures of volatility declined to multi-year lows. Emerging markets with strong fundamentals benefited from the positive sentiment, as reflected in narrower credit default swap spreads. A risk to this positive scenario is that, should US economic growth and inflation surprise to the upside, this could likely result in a renewed tightening of global financial conditions and a subsequent repricing of risk that could negatively impact on emerging markets, as witnessed in 2018. In addition, some emerging markets remain vulnerable to idiosyncratic risks. In South Africa, gains in financial asset prices were limited by the worsening of public sector finances and the risk of further sovereign credit rating downgrades to subinvestment grade.

The banking sector remains well capitalised at levels considerably above the minimum regulatory requirement. Impaired advances have continued to increase since January 2018 due to a combination of the implementation of the new expected credit loss accounting standard, International Financial Reporting Standard (IFRS) 9, and the deterioration in the credit quality of selected corporate and retail loan categories. In the current extended period of low economic growth, credit risk can arise from increasing financial stress in corporates and small- and medium-sized entities (SMEs) as well as households affected by job losses and/or deteriorating disposable income. The construction, manufacturing, wholesale and retail trade, and private household sectors exhibited the highest growth in default ratios since September 2017. Although not always indicative of the trend in the sector, the return on equity and assets of smaller banks has been declining (since May 2018) as a result of the reduction in non-interest income and increases in credit losses and operating expenses. By contrast, the return on equity and assets of the five largest banks increased marginally as their more diversified income streams provide additional resilience to profitability.

The financial position of households remains weak due to a combination of lower disposable income, a decline in net wealth and a significant increase in household debt. Overall, while there are concerns about the ability of households to service their debt, interest rates have remained relatively stable, thereby providing the sector with some relief.

Corporate profitability rose slightly in the 4th quarter of 2018. However, overall, profitability has been on a downward trend since the first quarter of 2018 due to subdued economic conditions and a sharp slowdown in the growth of non-financial corporate deposits. There has also been a slowdown in gross fixed capital formation, which could lead to lower economic growth prospects, further impeding profitability. Fiscal sustainability remains an important factor for South Africa’s sovereign credit rating. As a percentage of gross domestic product (GDP), government debt has doubled over the past 10 years, but remains below the 70% threshold level identified as high risk by the International Monetary Fund (IMF). Key fiscal metrics have continued to deteriorate during the reporting period and fiscal consolidation efforts have been hindered by debt-burdened SOEs that have struggled to meet their debt obligations. This adds to the probability of these contingent liabilities materialising on government’s balance sheet, thereby negatively impacting government debt levels. Eskom was recently granted a cumulative R69 billion over three years in support of its financial position. Despite the financial support, Eskom’s balance sheet remains stressed and continues to pose a systemic risk to the country’s economy. For the period under review, there have been a number of legislative and regulatory initiatives that, once implemented, could enhance the resilience of the South African financial system. These include the release, for public comment, of the Conduct of Financial Institutions Bill and the proposed Financial Matters Amendment Bill.1 The review of the National Payment System Act 78 of 1998 to take into account changes in the payment landscape and to align the regulation of the payment system to international best practice is also underway. The national payment system (NPS) plays a critical role in the settlement of domestic and international payment transactions and is key to a stable financial system

In conclusion, since the previous edition of the Financial Stability Review (FSR), global economic growth has slowed, and medium-term risks remain tilted to the downside. More recently, indications of continued less restrictive monetary policy by central banks in advanced economies, against a backdrop of slowing global growth, have led to easier financial conditions which supported global risk sentiment. Aside from being affected by exogenous factors through trade, investment and financial channels, South Africa’s growth prospects will be affected by domestic policy setting and idiosyncratic risks, reflected in the deterioration of a number of key indicators. Despite these challenges, the South African financial system continues to efficiently facilitate financial intermediation and mitigate negative spillovers and disruptions. Overall, the financial sector remains strong and stable, even with some headwinds from increased uncertainty around global economic policy, a challenging low domestic economic growth environment and persistent fiscal risks. The South African financial sector is also characterised by well-regulated, highly-capitalised, liquid and profitable financial institutions, supported by a robust financial infrastructure and strong regulatory and supervisory frameworks.

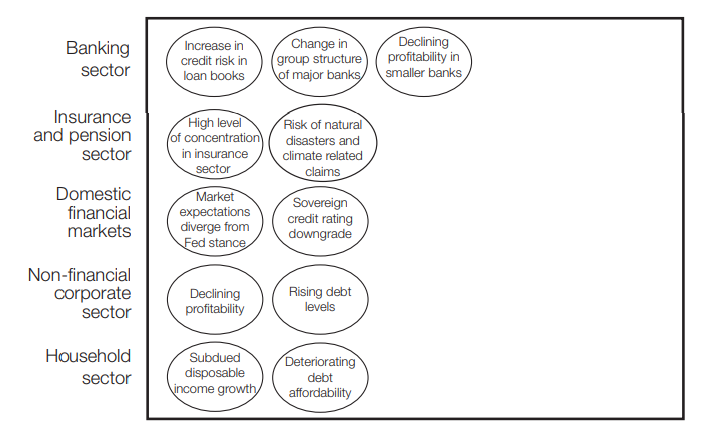

The image below shows the Sectoral Risk Map. Basically the biggest financial stability risks for various sectors of the South African economy.

What follows is a summary of financial stability risks as contained in the Financial Stability Review report.

The SARB regularly assesses the risks to financial stability in the next 12 months, with a view to identifying and mitigating any risks and/or vulnerabilities in the domestic financial system. Potential threats to financial stability are identified and rated according to the likelihood of their occurrence as well as their expected impact on the domestic financial system. Below the Top 5 biggest sources of financial stability risks, which according to SARB has a high likelihood of occurring:

The SARB regularly assesses the risks to financial stability in the next 12 months, with a view to identifying and mitigating any risks and/or vulnerabilities in the domestic financial system. Potential threats to financial stability are identified and rated according to the likelihood of their occurrence as well as their expected impact on the domestic financial system. Below the Top 5 biggest sources of financial stability risks, which according to SARB has a high likelihood of occurring:

- Deteriorating debt dynamics and limited fiscal space

- Weak economic growth and revenue collection outlook

- Fragile financial position of SOEs contributing to rising fiscal risk

- Rising public sector wage bill and cost of debt crowding out investment spending

- Increasing borrowing requirements

- Deteriorating fiscal position, rising debt levels and increase in taxes

- Lower household and corporate income and investment

- Sovereign credit ratings downgrade triggering capital outflows

- Tighter financial conditions due to negative investor sentiment

- Increase in financing costs

- Protracted period of low economic growth

- Pressure on financial sector profitability

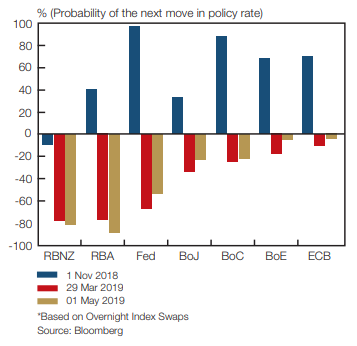

Positive global market sentiment in recent months was driven by expectations of continued accommodative monetary policy from the US and other advanced economy central banks. Since the previous edition of the FSR, global risk sentiment has improved, with risky assets benefitting from the surprise signalling of less restrictive monetary policy by the Fed and some other major central banks (such as the European Central Bank and Bank of Japan), against a backdrop of slowing global economic growth. See the chart below.

The yield on the two-year US Treasury bond, most sensitive to changes in Fed policy, declined by 60 basis points to 2.26%, below the mid-point of the Fed’s target range. The US dollar’s trade weighted index (TWI) traded sideways despite market expectations for interest rates changing to cuts from expectations of a hike. The USD TWI benefited from interest rate and growth differentials among the Group of Ten countries that favoured the USD. Volatility indicators retreated during the review period, with the MOVE Index (measuring advanced markets bond volatility), and the VIX (a proxy for advanced markets equity volatility) trading below their 100-day moving averages. Further, the global financial stress index (GFSI) declined below zero, indicating less financial market stress than normal, and possibly driven by lower hedging activity.

Emerging markets with strong fundamentals have benefited from the positive sentiment in global markets, as reflected in narrower credit default swap (CDS) spreads (Figure 6). Some emerging markets (including South Africa), remain vulnerable to idiosyncratic risks.

The yield on the two-year US Treasury bond, most sensitive to changes in Fed policy, declined by 60 basis points to 2.26%, below the mid-point of the Fed’s target range. The US dollar’s trade weighted index (TWI) traded sideways despite market expectations for interest rates changing to cuts from expectations of a hike. The USD TWI benefited from interest rate and growth differentials among the Group of Ten countries that favoured the USD. Volatility indicators retreated during the review period, with the MOVE Index (measuring advanced markets bond volatility), and the VIX (a proxy for advanced markets equity volatility) trading below their 100-day moving averages. Further, the global financial stress index (GFSI) declined below zero, indicating less financial market stress than normal, and possibly driven by lower hedging activity.

Emerging markets with strong fundamentals have benefited from the positive sentiment in global markets, as reflected in narrower credit default swap (CDS) spreads (Figure 6). Some emerging markets (including South Africa), remain vulnerable to idiosyncratic risks.

Monetary policy expectations for various central banks including the FED, BOJ, ECB and BoE

Idiosyncratic developments limited domestic asset price gains.

Domestic financial asset prices initially increased in line with the general emerging market trend; however, gains were limited by idiosyncratic factors. During the period under review, the exchange rate of the rand, domestic bonds and equities recorded strong performances in line with the general emerging market trend and, after Moody’s Investor Services (Moody’s) refrained from issuing a credit rating review on South Africa (Figure 7). However, the rand reversed some of its 2018 gains on heightened concerns about government’s contingent liabilities and the impact of electricity supply constraints on the country’s growth and sovereign credit rating. South Africa’s fiscal position weakened further, owing to tax revenue underperformance, which necessitated increased borrowing, and funding pressures from Eskom and other financially distressed state-owned companies, leading to a higher public sector borrowing requirement. This could increase the risk of a sovereign credit rating downgrade to sub-investment grade by Moody’s.

A downgrade by Moody’s to sub-investment grade (local currency) would result in South Africa’s exclusion from FTSE World Government Bond Index (WGBI) and forced sales of domestic government bonds from those investors whose mandates require them to track the index or prevent them from owning sub-investment grade instruments. The actual net portfolio outflows following a sovereign credit downgrade for countries like Russia, Brazil or Turkey have always been less than estimated. This is because a large portion of selling tends to occur prior to the actual downgrade to sub-investment grade, and investors with sub-investment grade mandates tend to purchase these securities, helping to offset some of the outflows. Fitch Ratings and Standard & Poor’s (S&P) Global Ratings downgraded South Africa’s sovereign credit rating to subinvestment grade in April 2017 and November 2017 respectively, resulting in South Africa exiting both the JPM GBI-EM Global Diversified index and the Barclays Global Aggregate Index. This triggered some forced selling of domestic bonds, which according to market estimates, was between R50 billion and R55 billion.

According to an IMF assessment8 , as at March 2018, remaining investment grade sensitive investors appeared to be only those tracking the WGBI. Overall, the IMF estimated that while in 2016 about 20% of local currency government debt was held by IG-sensitive investors, this share has now fallen to around 2%. Therefore, should a sovereign downgrade by Moody’s occur, it could prompt forced outflows of about US$1.5 billion or 0.5% of GDP. As some outflows have already occurred, this estimate is below the IMF’s 2016 estimate of about 2.5% of GDP. The IMF assessed only the R186 and R2023 holdings by non-residents (constituting about 85% of total holdings), hence, outflows could be marginally higher if total investment is taken into consideration. There are a few mitigating factors that could see South Africa’s financial markets being insulated from a WGBI exit.

South Africa’s equity market valuations continue to trend downwards despite an uneven recovery in some sectors. Following the global equity market correction during the latter part of 2018, equity valuations in a number of advanced and emerging markets reset towards relatively cheap levels by historical standards. Similarly, in South Africa, equities have continued on a downward trend in valuations since the peak reached in March 2016. Different variations of the priceearnings (PE) multiple for the JSE Limited (JSE) Top 40 index declined below their respective long-term averages before rising modestly during the first quarter of 2019 (Figure 8). This has resulted in a lower premium at which South African shares trade relative to emerging economies, as shares in these markets have seen a more modest adjustment in valuations over the same period. The estimate of the equity risk premium, which measures compensation for taking on equity risk over relatively safe bonds, has also been increasing.

Although the global sell-off in equities at the end of 2018 resulted in South African equities posting losses for the year, the JSE All-share Index (Alsi) has generally seen a steady recovery for the year to date. While the Alsi has increased by 12.3% for the year to date9 , retailers and construction shares have been sold off considerably (Figure 9). The construction and materials index currently trades near historic lows, as the industry struggles with weak infrastructure demand from both the private and the public sectors. General retailers have also underperformed the benchmark index, owing to disappointing retail sales, expectations of low profits and constrained household spending. Overall, South Africa’s equities are not overvalued in relative terms and financial stability risks appear to be well contained. Despite the overall positive sentiment towards risky assets, risks remain for the global financial system. US economic growth and inflation could surprise on the upside, convincing the Fed officials to continue with both interest rate and balance sheet normalisation. This would likely result in higher US bond yields, a stronger US dollar and a renewed tightening in financial conditions. Trade tension between the US and China could re-escalate and possibly spread to European countries. The current global economic slowdown could prove deeper and more protracted than the market anticipates. These developments would have negative implications for the performance of emerging market assets, particularly those emerging markets with elevated idiosyncratic risks, including South Africa.

A downgrade by Moody’s to sub-investment grade (local currency) would result in South Africa’s exclusion from FTSE World Government Bond Index (WGBI) and forced sales of domestic government bonds from those investors whose mandates require them to track the index or prevent them from owning sub-investment grade instruments. The actual net portfolio outflows following a sovereign credit downgrade for countries like Russia, Brazil or Turkey have always been less than estimated. This is because a large portion of selling tends to occur prior to the actual downgrade to sub-investment grade, and investors with sub-investment grade mandates tend to purchase these securities, helping to offset some of the outflows. Fitch Ratings and Standard & Poor’s (S&P) Global Ratings downgraded South Africa’s sovereign credit rating to subinvestment grade in April 2017 and November 2017 respectively, resulting in South Africa exiting both the JPM GBI-EM Global Diversified index and the Barclays Global Aggregate Index. This triggered some forced selling of domestic bonds, which according to market estimates, was between R50 billion and R55 billion.

According to an IMF assessment8 , as at March 2018, remaining investment grade sensitive investors appeared to be only those tracking the WGBI. Overall, the IMF estimated that while in 2016 about 20% of local currency government debt was held by IG-sensitive investors, this share has now fallen to around 2%. Therefore, should a sovereign downgrade by Moody’s occur, it could prompt forced outflows of about US$1.5 billion or 0.5% of GDP. As some outflows have already occurred, this estimate is below the IMF’s 2016 estimate of about 2.5% of GDP. The IMF assessed only the R186 and R2023 holdings by non-residents (constituting about 85% of total holdings), hence, outflows could be marginally higher if total investment is taken into consideration. There are a few mitigating factors that could see South Africa’s financial markets being insulated from a WGBI exit.

South Africa’s equity market valuations continue to trend downwards despite an uneven recovery in some sectors. Following the global equity market correction during the latter part of 2018, equity valuations in a number of advanced and emerging markets reset towards relatively cheap levels by historical standards. Similarly, in South Africa, equities have continued on a downward trend in valuations since the peak reached in March 2016. Different variations of the priceearnings (PE) multiple for the JSE Limited (JSE) Top 40 index declined below their respective long-term averages before rising modestly during the first quarter of 2019 (Figure 8). This has resulted in a lower premium at which South African shares trade relative to emerging economies, as shares in these markets have seen a more modest adjustment in valuations over the same period. The estimate of the equity risk premium, which measures compensation for taking on equity risk over relatively safe bonds, has also been increasing.

Although the global sell-off in equities at the end of 2018 resulted in South African equities posting losses for the year, the JSE All-share Index (Alsi) has generally seen a steady recovery for the year to date. While the Alsi has increased by 12.3% for the year to date9 , retailers and construction shares have been sold off considerably (Figure 9). The construction and materials index currently trades near historic lows, as the industry struggles with weak infrastructure demand from both the private and the public sectors. General retailers have also underperformed the benchmark index, owing to disappointing retail sales, expectations of low profits and constrained household spending. Overall, South Africa’s equities are not overvalued in relative terms and financial stability risks appear to be well contained. Despite the overall positive sentiment towards risky assets, risks remain for the global financial system. US economic growth and inflation could surprise on the upside, convincing the Fed officials to continue with both interest rate and balance sheet normalisation. This would likely result in higher US bond yields, a stronger US dollar and a renewed tightening in financial conditions. Trade tension between the US and China could re-escalate and possibly spread to European countries. The current global economic slowdown could prove deeper and more protracted than the market anticipates. These developments would have negative implications for the performance of emerging market assets, particularly those emerging markets with elevated idiosyncratic risks, including South Africa.

Are banks expecting increased impairments?

The following section covers Financial institutions in South Africa and the impact they have on financial stability as well as the impact financial stability has on them. The report had the following to say.

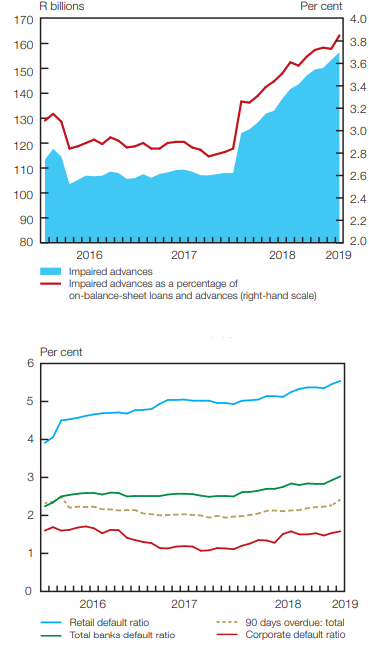

The banking sector’s impaired advances have continued to trend upwards since January 2018 due to a change to expected credit loss accounting as well as increasing credit risk. The banking sector’s impaired advances10 have continued to increase since January 2018, following the implementation of the new expected credit-loss accounting standard (IFRS 9), as reported previously.11 The ratio of impaired advances to on-balance-sheet loans and advances continued to increase from 3.58% in August 2018 to 3.85% in January 2019, having increased from 2.79% in October 2017 (Figure 10). The steady increase in impaired advances is reflective of the implementation of IFRS 9 as well as increasing risk in the sector’s credit portfolios. In order to get a clearer understanding of the rise in impaired advances, other measures of credit risk are analysed in this section of the FSR.

There has been an increase in credit risk in the banking sector, with the highest default ratios reported in the unsecured lending, revolving credit facilities, and vehicle and asset finance categories. Alternative indicators of credit risk are the 90 days overdue ratio12 and default ratios.13 The 90 days overdue ratio for the sector has increased by 48 basis points from a trough of 1.94% in November 2017 to 2.42% in January 2019.

See the two images below as obtained from the report. The top image shows the increase in the value of impaired advances over the last couple of months (on the left hand axis) and the percentage of advances that are being impaired by financial institutions. In 2017 this figure was hovering around 2.8% of advances being impaired, currently it is sitting at almost 4%

The banking sector’s impaired advances have continued to trend upwards since January 2018 due to a change to expected credit loss accounting as well as increasing credit risk. The banking sector’s impaired advances10 have continued to increase since January 2018, following the implementation of the new expected credit-loss accounting standard (IFRS 9), as reported previously.11 The ratio of impaired advances to on-balance-sheet loans and advances continued to increase from 3.58% in August 2018 to 3.85% in January 2019, having increased from 2.79% in October 2017 (Figure 10). The steady increase in impaired advances is reflective of the implementation of IFRS 9 as well as increasing risk in the sector’s credit portfolios. In order to get a clearer understanding of the rise in impaired advances, other measures of credit risk are analysed in this section of the FSR.

There has been an increase in credit risk in the banking sector, with the highest default ratios reported in the unsecured lending, revolving credit facilities, and vehicle and asset finance categories. Alternative indicators of credit risk are the 90 days overdue ratio12 and default ratios.13 The 90 days overdue ratio for the sector has increased by 48 basis points from a trough of 1.94% in November 2017 to 2.42% in January 2019.

See the two images below as obtained from the report. The top image shows the increase in the value of impaired advances over the last couple of months (on the left hand axis) and the percentage of advances that are being impaired by financial institutions. In 2017 this figure was hovering around 2.8% of advances being impaired, currently it is sitting at almost 4%

Not only are more loans being impaired, defaults on loans are starting to increase too. As the bottom image above shows. Defaulters after 90 days is starting to increase. Below is the summary on the defaults as found in the report.

A similar trend is seen in default ratios, with the total default ratio increasing from 2.49% in September 2017 to 3.03% in January 2019. Both retail and corporate default ratios show an upward trend during this period. Of the R26.48 billion (21%) increase in total default exposures since September 2017, R16.23 billion is related to retail exposures (mainly in residential mortgages, unsecured lending and vehicle and asset finance portfolios) and almost R10 billion is related to corporate exposures (both corporate and SME corporate categories increased). The increase in the default ratios suggests that there is increasing credit risk in the banking sector’s loan portfolios among corporate and retail clients – with the highest category default ratios in January 2019 being reported in unsecured lending (13.12%), revolving credit facilities (excluding credit cards) (6.65%) and vehicle and asset finance (6.12%). Although the retail default ratios are higher than the corporate default ratios, the average default size per corporate counterparty is significantly larger than that of the retail counterparties. For example, the average defaulted exposure per counterparty for the total corporate category more than doubled from R2 million in September 2017 to R4.1 million in January 2019. The average retail default exposure per counterparty increased by 12.9% from R18 000 in September 2017 to R20 000 in January 2019, with none of the retail subcategories doubling over the period.

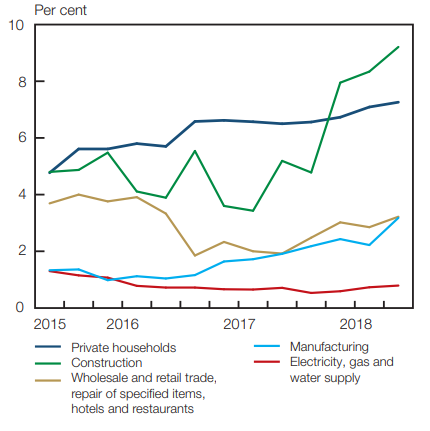

The sectors that showed the highest growth in default ratios since September 2017 were the construction, manufacturing, wholesale and retail trade as well as private household sectors (see the image below). As of December 2018, the private household sector’s defaulted exposures constituted the largest proportion of total defaulted exposures (almost 73%) with wholesale and retail trade (5%), real estate (5%) and manufacturing sector defaults (4%) contributing significantly. The credit rating of the sector’s on-balance-sheet loan portfolios has also deteriorated since December 2015 (Table 2). In December 2015, more than 83% of the onbalance-sheet loans were rated investment grade or higher. In December 2018, just over 35% of the on-balance-sheet loans held the same credit rating. There was a significant ratings migration of the on-balance-sheet loans from investment grade to sub-investment grade, when 30% of the on-balancesheet loans were downgraded between December 2016 and December 2017, and a further 19% was downgraded between December 2017 and December 2018.

A similar trend is seen in default ratios, with the total default ratio increasing from 2.49% in September 2017 to 3.03% in January 2019. Both retail and corporate default ratios show an upward trend during this period. Of the R26.48 billion (21%) increase in total default exposures since September 2017, R16.23 billion is related to retail exposures (mainly in residential mortgages, unsecured lending and vehicle and asset finance portfolios) and almost R10 billion is related to corporate exposures (both corporate and SME corporate categories increased). The increase in the default ratios suggests that there is increasing credit risk in the banking sector’s loan portfolios among corporate and retail clients – with the highest category default ratios in January 2019 being reported in unsecured lending (13.12%), revolving credit facilities (excluding credit cards) (6.65%) and vehicle and asset finance (6.12%). Although the retail default ratios are higher than the corporate default ratios, the average default size per corporate counterparty is significantly larger than that of the retail counterparties. For example, the average defaulted exposure per counterparty for the total corporate category more than doubled from R2 million in September 2017 to R4.1 million in January 2019. The average retail default exposure per counterparty increased by 12.9% from R18 000 in September 2017 to R20 000 in January 2019, with none of the retail subcategories doubling over the period.

The sectors that showed the highest growth in default ratios since September 2017 were the construction, manufacturing, wholesale and retail trade as well as private household sectors (see the image below). As of December 2018, the private household sector’s defaulted exposures constituted the largest proportion of total defaulted exposures (almost 73%) with wholesale and retail trade (5%), real estate (5%) and manufacturing sector defaults (4%) contributing significantly. The credit rating of the sector’s on-balance-sheet loan portfolios has also deteriorated since December 2015 (Table 2). In December 2015, more than 83% of the onbalance-sheet loans were rated investment grade or higher. In December 2018, just over 35% of the on-balance-sheet loans held the same credit rating. There was a significant ratings migration of the on-balance-sheet loans from investment grade to sub-investment grade, when 30% of the on-balancesheet loans were downgraded between December 2016 and December 2017, and a further 19% was downgraded between December 2017 and December 2018.

Most of the sector’s on-balance-sheet loans are to counterparties domiciled in South Africa (approximately 93% in December 2018) and to the rest of Africa (approximately 2.57% as of December 2018). Default ratios for South African counterparties increased from 3.14% in September 2017 to 3.65% in December 2018, whereas default ratios for the rest of Africa declined from 1.27% to 0.93% over the same period. The increase in impaired advances for the sector appears to be due to a combination of both the implementation of the new expected credit loss accounting standard, IFRS 9, as well as a deterioration in the credit quality of selected corporate and retail loan categories. In a low economic growth environment, credit risk is exacerbated by increasing financial stress in corporates and SMEs, as well as households affected by both job losses and/or deteriorating disposable income.

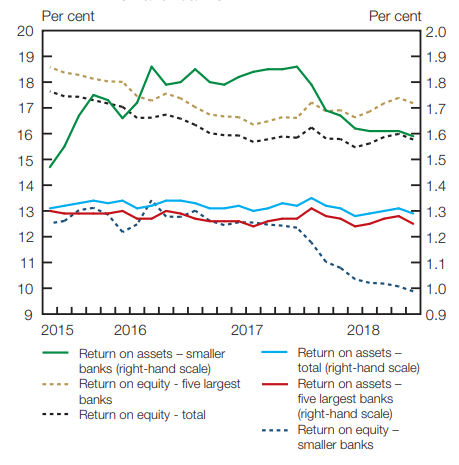

The resilience of the sector to these risks generally depends on the extent of its provisioning and collateral held, as well as the size of the capital buffers available to absorb losses. The profitability of smaller banks has declined since mid-2018. The return on equity (ROE) and return on assets (ROA) for the sector is usually a reflection of the trend movement in the ROE and ROA for the five largest banks. The profitability of the smaller banks (i.e. banks other than the five largest in the sector) is not always reflective in the trend of the sector. During periods of economic stress, the profitability of the largest banks is more resilient given, their diversified income streams. Smaller banks can be more vulnerable to economic stress as a result of their business models, for example, mono-line banking models that offer limited product types to one sector or to limited sectors. Since May 2018, the ROE and ROA of smaller banks has been declining (see image below).

The resilience of the sector to these risks generally depends on the extent of its provisioning and collateral held, as well as the size of the capital buffers available to absorb losses. The profitability of smaller banks has declined since mid-2018. The return on equity (ROE) and return on assets (ROA) for the sector is usually a reflection of the trend movement in the ROE and ROA for the five largest banks. The profitability of the smaller banks (i.e. banks other than the five largest in the sector) is not always reflective in the trend of the sector. During periods of economic stress, the profitability of the largest banks is more resilient given, their diversified income streams. Smaller banks can be more vulnerable to economic stress as a result of their business models, for example, mono-line banking models that offer limited product types to one sector or to limited sectors. Since May 2018, the ROE and ROA of smaller banks has been declining (see image below).

In contrast, the ROE and ROA of the five largest banks has remained largely unchanged over the same period. Smaller banks’ profitability declined by 12% year on year between May 2018 and January 2019. The decline in profitability reported by the smaller banks has been due to a 0.1% reduction in non-interest income (due to foreign exchange and debt securities trading losses, as well as accounting for fair value losses), a 12% increase in credit losses and a 9% increase in operating expenses (mainly due to increased fees and insurance, as well as office equipment and consumables expense). A number of large banks in the sector have implemented changes to their organisational structures. There is a high degree of concentration in the banking sector as well as between financial intermediaries in South Africa. As a result, significant changes to one or more participants that contribute to this high degree of concentration and/or interconnectedness could have implications for the whole system (see Box 2 for the methodology used by South Africa to determine which banks are systemically important). There are currently two major banking groups that have announced or are undergoing significant changes to their organisational structures. At present, and based on available information, there is no reasonable expectation for adverse effects on the financial system or economic activity to occur as a result of these changes.