|

Related Topics |

|

We take a look at the financial stability review, second edition 2019, published by the South African Reserve Bank (SARB), who is ultimately responsible for financial stability in South Africa.

|

|

What is financial stability?

According to the publication by the SARB, the purpose of the financial stability review and the definition of financial stability are discussed below

Purpose of the Financial Stability Review

The primary objective of the South African Reserve Bank (SARB) is to protect the value of the currency in the interest of balanced and sustainable economic growth in South Africa. In addition to this, the SARB’s function and mandate of protecting and enhancing financial stability in the Republic of South Africa is affirmed in the Financial Sector Regulation Act 9 of 2017 (FSR Act).

In pursuit of this objective, and to promote a stable financial system, the SARB publishes a semiannual Financial Stability Review. The publication aims to identify and analyse potential risks to financial system stability, communicate such assessments, and stimulate debate on pertinent issues. The SARB recognises that it is not the sole custodian of financial system stability, but that it contributes significantly towards and coordinates a larger effort involving government, other regulators, self-regulatory agencies, and financial market participants.

Defining ‘financial stability’

Financial stability is not an end in itself but, like price stability, is generally regarded as an important precondition for sustainable economic growth, development, and employment creation. Financial stability refers to a financial system that is resilient to systemic shocks, facilitates efficient financial intermediation, and mitigates the macroeconomic costs of disruptions in such a way that confidence in the system is maintained.

Purpose of the Financial Stability Review

The primary objective of the South African Reserve Bank (SARB) is to protect the value of the currency in the interest of balanced and sustainable economic growth in South Africa. In addition to this, the SARB’s function and mandate of protecting and enhancing financial stability in the Republic of South Africa is affirmed in the Financial Sector Regulation Act 9 of 2017 (FSR Act).

In pursuit of this objective, and to promote a stable financial system, the SARB publishes a semiannual Financial Stability Review. The publication aims to identify and analyse potential risks to financial system stability, communicate such assessments, and stimulate debate on pertinent issues. The SARB recognises that it is not the sole custodian of financial system stability, but that it contributes significantly towards and coordinates a larger effort involving government, other regulators, self-regulatory agencies, and financial market participants.

Defining ‘financial stability’

Financial stability is not an end in itself but, like price stability, is generally regarded as an important precondition for sustainable economic growth, development, and employment creation. Financial stability refers to a financial system that is resilient to systemic shocks, facilitates efficient financial intermediation, and mitigates the macroeconomic costs of disruptions in such a way that confidence in the system is maintained.

Overview

The South African Reserve Bank (SARB) continually assesses risks to the stability of the domestic financial system with a view to mitigating the build-up of vulnerabilities that may become systemic. Overall, the South African financial system remains stable, despite some global and domestic headwinds. Since the release of the previous edition of the Financial Stability Review (FSR), global financial conditions have eased further, premised on expectations of additional monetary policy accommodation in advanced economies. Such accommodative conditions pose a renewed risk of fuelling the build-up of financial vulnerabilities. Domestically, downside risks to financial stability increased during the reporting period as a result of countryspecific risks, such as expectations of a prolonged period of slower domestic economic growth and a deterioration in the fiscal outlook. Higher costs of funding for South African banks, higher levels of volatility in financial markets and asset price losses dominated economic and financial conditions.

The potential threats to financial stability reported in the FSR second edition 2019 include:

(i) the deteriorating domestic fiscal position, which resulted largely from higher government debt, weak domestic economic growth and revenue undercollection, and was further exacerbated by the weak financial positions of stated-owned enterprises and government’s rising contingent liabilities;

(ii) rising cyber dependency and security risks attributed to the increasing digital interconnection of people, systems and organisations, as cyberattacks could have direct material consequences for financial institutions through financial losses as well as indirect costs such as reputational impact;

(iii) weaker global economic growth and spillovers to emerging markets, including South Africa, which mostly emanated from the escalation of trade tensions and the expected spillover to financial sectors, the uncertainty related to Brexit outcomes, weak business confidence, and subdued corporate profitability and investment spending; and

(iv) the low probability but potentially high impact risk of abrupt and unanticipated changes to global financial conditions impacting on emerging markets. Monetary policy adjustments in advanced economies could lead to a rapid repricing of risk, unpredictable swings in capital flows to emerging markets and increased financial market volatility.

The global environment has been impacted by increased uncertainty as trade tensions remain heightened and investors remain concerned about downside risks to the economic growth outlook. Further downside risks to the outlook for global growth may lead to a retreat into investments that are perceived to be safer, such as United States (US) Treasury bills. Large-scale investment flows out of riskier assets, including emerging market assets, could expose financial vulnerabilities that accumulated during the years of low interest rates, disinflationary pressures, Brexit-related uncertainty, and rising geopolitical tensions that have an impact on global risk sentiment. During the reporting period, global risk measures such as the VIX Index (which measures advanced markets’ equity volatility) and the Global Financial Stress Indicator initially increased, but then stabilised as major central banks continued with accommodative monetary policy. As part of its forward-looking assessment, the International Monetary Fund (IMF) Global Financial Stability Report also identified rising corporate debt burdens, increased holdings of riskier and more illiquid securities by institutional investors in a lowfor-longer interest rate scenario, and the increased reliance on external borrowing by emerging and frontier markets as financial vulnerabilities that could exacerbate a next economic downturn.

The potential threats to financial stability reported in the FSR second edition 2019 include:

(i) the deteriorating domestic fiscal position, which resulted largely from higher government debt, weak domestic economic growth and revenue undercollection, and was further exacerbated by the weak financial positions of stated-owned enterprises and government’s rising contingent liabilities;

(ii) rising cyber dependency and security risks attributed to the increasing digital interconnection of people, systems and organisations, as cyberattacks could have direct material consequences for financial institutions through financial losses as well as indirect costs such as reputational impact;

(iii) weaker global economic growth and spillovers to emerging markets, including South Africa, which mostly emanated from the escalation of trade tensions and the expected spillover to financial sectors, the uncertainty related to Brexit outcomes, weak business confidence, and subdued corporate profitability and investment spending; and

(iv) the low probability but potentially high impact risk of abrupt and unanticipated changes to global financial conditions impacting on emerging markets. Monetary policy adjustments in advanced economies could lead to a rapid repricing of risk, unpredictable swings in capital flows to emerging markets and increased financial market volatility.

The global environment has been impacted by increased uncertainty as trade tensions remain heightened and investors remain concerned about downside risks to the economic growth outlook. Further downside risks to the outlook for global growth may lead to a retreat into investments that are perceived to be safer, such as United States (US) Treasury bills. Large-scale investment flows out of riskier assets, including emerging market assets, could expose financial vulnerabilities that accumulated during the years of low interest rates, disinflationary pressures, Brexit-related uncertainty, and rising geopolitical tensions that have an impact on global risk sentiment. During the reporting period, global risk measures such as the VIX Index (which measures advanced markets’ equity volatility) and the Global Financial Stress Indicator initially increased, but then stabilised as major central banks continued with accommodative monetary policy. As part of its forward-looking assessment, the International Monetary Fund (IMF) Global Financial Stability Report also identified rising corporate debt burdens, increased holdings of riskier and more illiquid securities by institutional investors in a lowfor-longer interest rate scenario, and the increased reliance on external borrowing by emerging and frontier markets as financial vulnerabilities that could exacerbate a next economic downturn.

From a South African perspective, a sustained slowdown in global growth in the longer run could lead to lower external demand for South African manufactured goods and other exports, thus placing a damper on domestic economic growth prospects. This could result in a pick-up in unemployment levels, which could potentially hamper the debt-servicing capacity of borrowers and in turn impact negatively on banks’ asset quality. In general, weak domestic economic and financial fundamentals could weigh on sovereign and corporate credit ratings, and increase the funding costs and credit risk in both the financial and non-financial sectors. Since the previous edition of the FSR, local assets have reflected volatile global market conditions and fluctuated between losses and gains.

Weaker-than-expected economic data releases from advanced economies fuelled renewed expectations of a prolonged stance of accommodative global monetary policy with potential implications for emerging economies. Local asset markets were also impacted by negative sentiment about domestic growth prospects and fiscal deterioration following the announcement of additional government bailouts for some state-owned entities (SOEs). An analysis of the local equity market suggests that the risk premium on South African banks has been increasing, putting upward pressure on bank funding costs. However, the higher funding cost does not yet appear to be spilling over into higher lending rates. Looking ahead, global risk perceptions will be a key driver of asset price performances as South Africa also contends with country-specific risks and the prospect of further credit rating downgrades for the sovereign.

Although a sovereign credit rating downgrade by Moody’s Investors Service (Moody’s) in the medium term has been somewhat priced in by financial markets, high levels of volatility and asset price losses could be expected, especially in an environment where foreign investors have a preference for safer financial assets. During the period under review, the overall trend in the domestic banking sector’s ratio of impaired advances to onbalance-sheet loans remained largely unchanged, following a strong upward trend since the implementation of International Financial Reporting Standard (IFRS) 91 in January 2018. The profitability of smaller banks continued to decline during 2019, but the rate of decline slowed in the second half of the year. Growth in residential mortgages recovered, with a large part of the new business originated at loan-to-value ratios in excess of 100%, perhaps an early indicator of more lenient mortgage financing conditions. There was a modest increase in credit growth during the reporting period, mainly due to increased lending to corporates. Affordability measures for the non-financial corporate sector point to a weakening in the sector’s ability to service its debt.

The current negative feedback loop between business confidence and economic growth is likely to constrain corporate sector investment, spending and earnings. Some industries are facing more severe financial strain than others. However, it seems unlikely that a possible default by some of the weakest institutions will have severe systemic implications for the banking sector, given the banking sector’s limited exposure to these industries. Further significant and/or rapid deterioration in non-financial corporate balance sheets may affect the sector’s debt-servicing capacity and could pose a threat to domestic financial stability. During the period under review, the net wealth of households improved as a result of their total assets exceeding their total financial liabilities by an increasing amount over the past three quarters. However, the sector remains vulnerable to both financial and economic shocks, given slowing disposable income growth, very low savings and higher debt levels. With weak economic growth prospects and some signals of financial distress pointing to vulnerability in the household sector, consumers are becoming increasingly pessimistic.

The economic sub-index of the First National Bank/Bureau for Economic Research (FNB/BER) Consumer Confidence Index declined in the second quarter of 2019, in line with consumers’ expectations for domestic conditions to worsen in the next 12 months. Consumers’ confidence about their financial position worsened, with most consumers rating the current period as unfavourable to purchase durable goods, indicating financial strain. The overall analysis suggests that, although selected risks in the banking sector such as banks’ exposure to highly indebted corporate and household sectors have the potential to lead to vulnerabilities that could amplify shocks, these risks are currently not systemic in nature.

Global trade tensions have placed more pressure on economic growth and some central banks have embarked on a fresh round of liquidity support measures to sustain growth. At present, about a quarter of the bond issuance by governments and other institutions globally is trading at negative yields, resulting in long-term institutional investors (pension funds and insurance companies) being almost obliged to make unprecedented changes to their asset allocation mix and taking on more risk in the process. In addition, institutional investors might be constrained to hold government bonds due to prudential requirements, and this could contribute to a demand surplus and further downward pressure on yields. In South Africa, nominal yields were positive during the accommodative monetary policy stance in the peak and immediate aftermath of the global financial crisis. Since 2007, the benchmark 10-year government bond yield has mostly been above 7%, and the asset composition of the South African pension fund and insurance industry has remained consistent.

Weaker-than-expected economic data releases from advanced economies fuelled renewed expectations of a prolonged stance of accommodative global monetary policy with potential implications for emerging economies. Local asset markets were also impacted by negative sentiment about domestic growth prospects and fiscal deterioration following the announcement of additional government bailouts for some state-owned entities (SOEs). An analysis of the local equity market suggests that the risk premium on South African banks has been increasing, putting upward pressure on bank funding costs. However, the higher funding cost does not yet appear to be spilling over into higher lending rates. Looking ahead, global risk perceptions will be a key driver of asset price performances as South Africa also contends with country-specific risks and the prospect of further credit rating downgrades for the sovereign.

Although a sovereign credit rating downgrade by Moody’s Investors Service (Moody’s) in the medium term has been somewhat priced in by financial markets, high levels of volatility and asset price losses could be expected, especially in an environment where foreign investors have a preference for safer financial assets. During the period under review, the overall trend in the domestic banking sector’s ratio of impaired advances to onbalance-sheet loans remained largely unchanged, following a strong upward trend since the implementation of International Financial Reporting Standard (IFRS) 91 in January 2018. The profitability of smaller banks continued to decline during 2019, but the rate of decline slowed in the second half of the year. Growth in residential mortgages recovered, with a large part of the new business originated at loan-to-value ratios in excess of 100%, perhaps an early indicator of more lenient mortgage financing conditions. There was a modest increase in credit growth during the reporting period, mainly due to increased lending to corporates. Affordability measures for the non-financial corporate sector point to a weakening in the sector’s ability to service its debt.

The current negative feedback loop between business confidence and economic growth is likely to constrain corporate sector investment, spending and earnings. Some industries are facing more severe financial strain than others. However, it seems unlikely that a possible default by some of the weakest institutions will have severe systemic implications for the banking sector, given the banking sector’s limited exposure to these industries. Further significant and/or rapid deterioration in non-financial corporate balance sheets may affect the sector’s debt-servicing capacity and could pose a threat to domestic financial stability. During the period under review, the net wealth of households improved as a result of their total assets exceeding their total financial liabilities by an increasing amount over the past three quarters. However, the sector remains vulnerable to both financial and economic shocks, given slowing disposable income growth, very low savings and higher debt levels. With weak economic growth prospects and some signals of financial distress pointing to vulnerability in the household sector, consumers are becoming increasingly pessimistic.

The economic sub-index of the First National Bank/Bureau for Economic Research (FNB/BER) Consumer Confidence Index declined in the second quarter of 2019, in line with consumers’ expectations for domestic conditions to worsen in the next 12 months. Consumers’ confidence about their financial position worsened, with most consumers rating the current period as unfavourable to purchase durable goods, indicating financial strain. The overall analysis suggests that, although selected risks in the banking sector such as banks’ exposure to highly indebted corporate and household sectors have the potential to lead to vulnerabilities that could amplify shocks, these risks are currently not systemic in nature.

Global trade tensions have placed more pressure on economic growth and some central banks have embarked on a fresh round of liquidity support measures to sustain growth. At present, about a quarter of the bond issuance by governments and other institutions globally is trading at negative yields, resulting in long-term institutional investors (pension funds and insurance companies) being almost obliged to make unprecedented changes to their asset allocation mix and taking on more risk in the process. In addition, institutional investors might be constrained to hold government bonds due to prudential requirements, and this could contribute to a demand surplus and further downward pressure on yields. In South Africa, nominal yields were positive during the accommodative monetary policy stance in the peak and immediate aftermath of the global financial crisis. Since 2007, the benchmark 10-year government bond yield has mostly been above 7%, and the asset composition of the South African pension fund and insurance industry has remained consistent.

Government finances remain fragile due to deteriorating debt dynamics and shrinking fiscal space, and debt sustainability remains a concern. Risks to the fiscal outlook remain elevated over the medium term and could potentially pose risks to the stability of the domestic financial system. These include a bleak outlook for government revenue, the poor financial position of major SOEs, and weak economic growth affecting future growth in tax revenues.

Proposed key interventions by government to support fiscal consolidation include a decrease in the public sector wage bill, strengthened governance over fiscal expenditure, and increasing infrastructure investment expenditure. As high net external financing requirements could make a country vulnerable to financial market volatility, countries strengthen or increase their reserve buffers to combat such vulnerability. South Africa’s official gross gold and foreign exchange reserves increased to US$49.95 billion in August 2019 from US$49.36 billion in July. Although the Guidotti ratio, which represents a measure of reserve adequacy for financial stability purposes, decreased further in the second quarter of 2019, it remained above the threshold of 1, suggesting that there is sufficient funding available to service the country’s short-term external debt should the availability of foreign exchange reduce suddenly. During the period under review, a number of legislative and regulatory initiatives were tabled which, once implemented, will enhance the resilience of the South African financial system. These include the enactment of the National Credit Amendment Act, implementation of some aspects of the Financial Intelligence Centre Act 1 of 2017, and draft conduct standards for the banking industry. There were also a number of developments relating to the domestic banking sector and financial markets, including the latest Basel III reforms and their implications for South African banks, and the reform of benchmark rates.

This edition of the FSR also explores the increasingly important role of financial technologies for payment systems. Finally, an overview of international regulatory developments that may impact on the domestic financial sector, such as the post-London Interbank Offered Rate (Libor) transition of benchmark rates and efforts to stymie misconduct risk in financial services, are discussed. The Governor of the SARB, after giving notice to the Financial Sector Oversight Committee, designated six South African banks as systemically important financial institutions (SIFIs). All six banks – Absa Bank Limited, The Standard Bank of South Africa Limited, FirstRand Bank Limited, Nedbank Bank Limited, Investec Bank Limited and Capitec Bank Limited – accepted their designations. Designation as a SIFI does not mean that these banks are seen as relatively riskier institutions but, given their potential systemic impact on the financial system, it is important for the SARB to monitor and regulate their operations and soundness, in addition to the microprudential regulation and supervision conducted by the Prudential Authority (PA) of the SARB. In terms of the Financial Sector Regulation Act 9 of 2017 (FSR Act), the SARB may, after consultation with the PA, impose additional requirements on SIFIs to mitigate the risk that systemic events may occur.

Climate change continues to pose risks for the insurance sector, given its exposures to losses caused by extreme weather events. Owing to the high degree of interconnectedness across sectors within the financial system, the probability of spillover effects between the insurance sector and the rest of the financial system through various transmission channels is becoming increasingly probable, although it is not significant at this stage. However, climate-related risks to the financial system are not limited solely to the insurance sector. Stranded assets and the risk of a significant system-wide re-evaluation of asset prices are considered to pose a more direct risk to financial stability. Disclosures relating to institutions’ exposures to nonsustainable sectors as well as the associated financial risk are currently performed on a voluntary basis in many jurisdictions. As such, investors remain uninformed about the exact extent to which industries are exposed to non-sustainable sectors. In conclusion, since the previous edition of the FSR, risks to financial stability have increased against the backdrop of easy financial conditions, over-valuations in some markets and elevated vulnerabilities.

Aside from being affected by global factors through trade, investment and financial channels, South Africa’s economic and financial system stability is expected to be further impacted by country-specific risks, as reflected in the deterioration of a number of key metrics. Despite these challenges, the South African financial system has continued to efficiently facilitate financial intermediation and mitigate negative spillovers and disruptions. Overall, the financial sector remains strong and stable, despite some headwinds from a challenging low domestic economic growth environment, persistent fiscal challenges and increased global policy uncertainty. The South African financial sector is also characterised by well-regulated, highly capitalised, liquid and profitable financial institutions, supported by a robust regulatory and financial infrastructure.

Proposed key interventions by government to support fiscal consolidation include a decrease in the public sector wage bill, strengthened governance over fiscal expenditure, and increasing infrastructure investment expenditure. As high net external financing requirements could make a country vulnerable to financial market volatility, countries strengthen or increase their reserve buffers to combat such vulnerability. South Africa’s official gross gold and foreign exchange reserves increased to US$49.95 billion in August 2019 from US$49.36 billion in July. Although the Guidotti ratio, which represents a measure of reserve adequacy for financial stability purposes, decreased further in the second quarter of 2019, it remained above the threshold of 1, suggesting that there is sufficient funding available to service the country’s short-term external debt should the availability of foreign exchange reduce suddenly. During the period under review, a number of legislative and regulatory initiatives were tabled which, once implemented, will enhance the resilience of the South African financial system. These include the enactment of the National Credit Amendment Act, implementation of some aspects of the Financial Intelligence Centre Act 1 of 2017, and draft conduct standards for the banking industry. There were also a number of developments relating to the domestic banking sector and financial markets, including the latest Basel III reforms and their implications for South African banks, and the reform of benchmark rates.

This edition of the FSR also explores the increasingly important role of financial technologies for payment systems. Finally, an overview of international regulatory developments that may impact on the domestic financial sector, such as the post-London Interbank Offered Rate (Libor) transition of benchmark rates and efforts to stymie misconduct risk in financial services, are discussed. The Governor of the SARB, after giving notice to the Financial Sector Oversight Committee, designated six South African banks as systemically important financial institutions (SIFIs). All six banks – Absa Bank Limited, The Standard Bank of South Africa Limited, FirstRand Bank Limited, Nedbank Bank Limited, Investec Bank Limited and Capitec Bank Limited – accepted their designations. Designation as a SIFI does not mean that these banks are seen as relatively riskier institutions but, given their potential systemic impact on the financial system, it is important for the SARB to monitor and regulate their operations and soundness, in addition to the microprudential regulation and supervision conducted by the Prudential Authority (PA) of the SARB. In terms of the Financial Sector Regulation Act 9 of 2017 (FSR Act), the SARB may, after consultation with the PA, impose additional requirements on SIFIs to mitigate the risk that systemic events may occur.

Climate change continues to pose risks for the insurance sector, given its exposures to losses caused by extreme weather events. Owing to the high degree of interconnectedness across sectors within the financial system, the probability of spillover effects between the insurance sector and the rest of the financial system through various transmission channels is becoming increasingly probable, although it is not significant at this stage. However, climate-related risks to the financial system are not limited solely to the insurance sector. Stranded assets and the risk of a significant system-wide re-evaluation of asset prices are considered to pose a more direct risk to financial stability. Disclosures relating to institutions’ exposures to nonsustainable sectors as well as the associated financial risk are currently performed on a voluntary basis in many jurisdictions. As such, investors remain uninformed about the exact extent to which industries are exposed to non-sustainable sectors. In conclusion, since the previous edition of the FSR, risks to financial stability have increased against the backdrop of easy financial conditions, over-valuations in some markets and elevated vulnerabilities.

Aside from being affected by global factors through trade, investment and financial channels, South Africa’s economic and financial system stability is expected to be further impacted by country-specific risks, as reflected in the deterioration of a number of key metrics. Despite these challenges, the South African financial system has continued to efficiently facilitate financial intermediation and mitigate negative spillovers and disruptions. Overall, the financial sector remains strong and stable, despite some headwinds from a challenging low domestic economic growth environment, persistent fiscal challenges and increased global policy uncertainty. The South African financial sector is also characterised by well-regulated, highly capitalised, liquid and profitable financial institutions, supported by a robust regulatory and financial infrastructure.

Economic growth outlook and its potential impact on the financial sector:

Without a stable financial system there is no basis for sustainable economic growth. Conversely, developments in the real economy also have an impact on financial stability. Low levels of economic growth could impact on financial stability through various channels, including higher unemployment and a reduced ability to service debt by households and corporates. This, in turn, could lower the profitability of banks and insurers and impact negatively on the quality of banks’ assets. Weakening global economic activity and financial stability. The global environment has been impacted by increased uncertainty related to heightened trade tensions and growing investor concerns about downside risks to the economic growth outlook. Other downside risks to the global growth outlook include rising risk aversion that exposes financial vulnerabilities that have been accumulating after years of low interest rates, Brexit-related uncertainty, and rising geopolitical tensions.

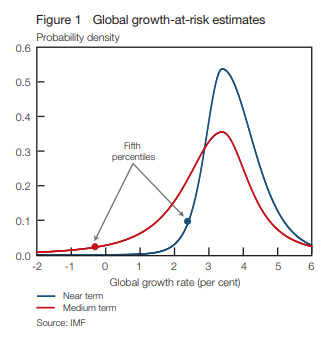

According to the IMF’s Global Financial Stability Report (GFSR), the easing of financial conditions has helped moderate downside risks to global growth and financial stability in the near term. This is despite a decline in the IMF’s baseline growth forecast and a rise in financial vulnerabilities. The GFSR reports that near-term growth-at-risk (GaR) (defined as the 5th percentile of the one-year-ahead forecast distribution) has remained broadly unchanged compared to six months ago, while medium-term risks are skewed to the downside4 (Figure 1 below).

It is, however, suggested that investors might be overly complacent about downside risks. Domestic growth remains vulnerable to global and idiosyncratic developments. The South African economy recorded gross domestic product (GDP) growth of 3.1% in the second quarter of 2019 (quarteron-quarter annualised rates), after a revised contraction of 3.1% in the previous quarter. Despite the rebound in economic activity, the growth outlook remains anaemic, amid poor manufacturing prospects, rising unemployment,5 weak consumer and business confidence, subdued investment levels, slow implementation of domestic structural reforms, and a slowing global economy. The SARB’s November 2019 forecast is for domestic growth of 0.5% for 2019 (down from a previous estimate of 0.6%). The forecast for 2020 is 1.4% (down from 1.5%), rising to 1.7% in 2021 (down from 1.8%). With respect to ‘tail risks’ stemming from the lower end of the growth distribution, near-term GaR has remained relatively unchanged over the past two quarters, while medium-term GaR improved in the second quarter of 2019 after deteriorating markedly in the previous quarter.

Without a stable financial system there is no basis for sustainable economic growth. Conversely, developments in the real economy also have an impact on financial stability. Low levels of economic growth could impact on financial stability through various channels, including higher unemployment and a reduced ability to service debt by households and corporates. This, in turn, could lower the profitability of banks and insurers and impact negatively on the quality of banks’ assets. Weakening global economic activity and financial stability. The global environment has been impacted by increased uncertainty related to heightened trade tensions and growing investor concerns about downside risks to the economic growth outlook. Other downside risks to the global growth outlook include rising risk aversion that exposes financial vulnerabilities that have been accumulating after years of low interest rates, Brexit-related uncertainty, and rising geopolitical tensions.

According to the IMF’s Global Financial Stability Report (GFSR), the easing of financial conditions has helped moderate downside risks to global growth and financial stability in the near term. This is despite a decline in the IMF’s baseline growth forecast and a rise in financial vulnerabilities. The GFSR reports that near-term growth-at-risk (GaR) (defined as the 5th percentile of the one-year-ahead forecast distribution) has remained broadly unchanged compared to six months ago, while medium-term risks are skewed to the downside4 (Figure 1 below).

It is, however, suggested that investors might be overly complacent about downside risks. Domestic growth remains vulnerable to global and idiosyncratic developments. The South African economy recorded gross domestic product (GDP) growth of 3.1% in the second quarter of 2019 (quarteron-quarter annualised rates), after a revised contraction of 3.1% in the previous quarter. Despite the rebound in economic activity, the growth outlook remains anaemic, amid poor manufacturing prospects, rising unemployment,5 weak consumer and business confidence, subdued investment levels, slow implementation of domestic structural reforms, and a slowing global economy. The SARB’s November 2019 forecast is for domestic growth of 0.5% for 2019 (down from a previous estimate of 0.6%). The forecast for 2020 is 1.4% (down from 1.5%), rising to 1.7% in 2021 (down from 1.8%). With respect to ‘tail risks’ stemming from the lower end of the growth distribution, near-term GaR has remained relatively unchanged over the past two quarters, while medium-term GaR improved in the second quarter of 2019 after deteriorating markedly in the previous quarter.

Global growth at risk estimates

From a financial stability perspective, a sustained slowdown in global growth in the longer run could lead to lower external demand for South African manufactured goods and other exports, thus placing a damper on domestic economic growth prospects. This could result in a pick-up in unemployment levels, which could hamper debt-servicing capacity and impact negatively on the asset quality of the banking sector. Generally, weak fundamentals could weigh on sovereign and corporate credit ratings, and increase funding costs and the credit risk of financial and non financial sectors. This could also lead to a worsening of the twin deficits (fiscal and current account deficits) as well as capital flow reversal, therefore hindering fiscal consolidation efforts and reinforcing negative feedback loops between growth and the fiscus.

Financial markets

Since the previous edition of the FSR, local assets have tracked volatile global market conditions and fluctuated between losses and gains. The softer-than-expected economic data releases from advanced economies fuelled renewed expectations of a prolonged stance of accommodative global monetary policy. Local assets were also impacted by negative sentiment on expectations of slower domestic growth and fiscal deterioration following the announcement of additional government bailouts of some SOEs. The risk premium on South African banks has been increasing; however, there do not appear to be spillovers to domestic financing conditions.

Looking ahead, global risk perceptions will be a key driver of domestic asset price performances as South Africa also contends with idiosyncratic risks and the prospect of further sovereign rating downgrades in the medium term. Although a possible sovereign credit rating downgrade by Moody’s in the medium term is perceived by most market participants to be somewhat priced in, the possibility of high levels of volatility and asset price losses should not be underestimated, especially against a backdrop of an uncertain global environment. Global market sentiment and asset price performances were mostly driven by global growth concerns and accommodative monetary policy responses from key global central banks. Global risk measures such as the MOVE Index (measuring advanced markets’ bond volatility), the Chicago Board Options Exchange Volatility Index, known as VIX (a proxy for advanced markets’ equity volatility), and foreign exchange rate volatility initially worsened but later stabilised as major central banks continued with accommodative monetary policy action to support economic growth in their respective economies.

The trend was similar for the Global Financial Stress Indicator. Global investors will continue to assess the current global economic fragility against the degree of accommodative policy responses from global central banks such as the United States Federal Reserve (US Fed), European Central Bank (ECB) and People’s Bank of China (PBoC), among others. There are strong expectations among market analysts that the major central banks will continue with monetary policy accommodation measures in the near term to support growth (Figure 4). The US Dollar Index6 was mostly stronger in 2019 and moved in tandem with declining US and global bond yields. In the US, the spread between the US 10-year Treasury yield and 3-month Treasury yield inverted for the first time since 2007, sparking fears of a US recession (Figure 5). According to the Institute of International Finance (IIF), while certain segments of the US yield curve has turned negative since December 2018, inversion has become more widespread, with the majority of the curve being inverted for more than 90 days.

Although it is believed by some market analysts that this could indicate a recession warning, this view is not widely held globally. That being said, the paradigm of ‘lower for longer’ accommodation measures by major central banks is expected to be prolonged, which could benefit risky assets in the short term. However, if looser or easy global financial conditions do not translate into higher economic growth, there could be negative implications for emerging markets, including South Africa. In a ‘lower for longer’ paradigm where investors anticipate low interest rates over a prolonged period, financial stability concerns could arise via a number of channels. For instance, further easing of financial conditions may result in the mispricing of risk and consequently the valuation of risky assets. Very low interest rates could incentivise investors to search for yield and thus take on riskier and more illiquid assets to generate targeted returns.

The accumulation of such assets could be a source of financial market vulnerability should financial conditions tighten abruptly and cause a sharp slowdown or reversal in portfolio flows, particularly among vulnerable emerging markets. Those emerging markets with low economic growth prospects, large macroeconomic imbalances and high external financing needs would become more vulnerable. The IMF8 noted that in a low interest rate environment, there is increased reliance on external debt in emerging market and frontier markets that could trigger a rollover of debt, undermine debt sustainability or increase distress risks. Hence, the IMF recommends that macroprudential policies be constantly reviewed to anticipate the impact of an abrupt end to accommodative monetary policy and the subsequent tightening of market conditions

Looking ahead, global risk perceptions will be a key driver of domestic asset price performances as South Africa also contends with idiosyncratic risks and the prospect of further sovereign rating downgrades in the medium term. Although a possible sovereign credit rating downgrade by Moody’s in the medium term is perceived by most market participants to be somewhat priced in, the possibility of high levels of volatility and asset price losses should not be underestimated, especially against a backdrop of an uncertain global environment. Global market sentiment and asset price performances were mostly driven by global growth concerns and accommodative monetary policy responses from key global central banks. Global risk measures such as the MOVE Index (measuring advanced markets’ bond volatility), the Chicago Board Options Exchange Volatility Index, known as VIX (a proxy for advanced markets’ equity volatility), and foreign exchange rate volatility initially worsened but later stabilised as major central banks continued with accommodative monetary policy action to support economic growth in their respective economies.

The trend was similar for the Global Financial Stress Indicator. Global investors will continue to assess the current global economic fragility against the degree of accommodative policy responses from global central banks such as the United States Federal Reserve (US Fed), European Central Bank (ECB) and People’s Bank of China (PBoC), among others. There are strong expectations among market analysts that the major central banks will continue with monetary policy accommodation measures in the near term to support growth (Figure 4). The US Dollar Index6 was mostly stronger in 2019 and moved in tandem with declining US and global bond yields. In the US, the spread between the US 10-year Treasury yield and 3-month Treasury yield inverted for the first time since 2007, sparking fears of a US recession (Figure 5). According to the Institute of International Finance (IIF), while certain segments of the US yield curve has turned negative since December 2018, inversion has become more widespread, with the majority of the curve being inverted for more than 90 days.

Although it is believed by some market analysts that this could indicate a recession warning, this view is not widely held globally. That being said, the paradigm of ‘lower for longer’ accommodation measures by major central banks is expected to be prolonged, which could benefit risky assets in the short term. However, if looser or easy global financial conditions do not translate into higher economic growth, there could be negative implications for emerging markets, including South Africa. In a ‘lower for longer’ paradigm where investors anticipate low interest rates over a prolonged period, financial stability concerns could arise via a number of channels. For instance, further easing of financial conditions may result in the mispricing of risk and consequently the valuation of risky assets. Very low interest rates could incentivise investors to search for yield and thus take on riskier and more illiquid assets to generate targeted returns.

The accumulation of such assets could be a source of financial market vulnerability should financial conditions tighten abruptly and cause a sharp slowdown or reversal in portfolio flows, particularly among vulnerable emerging markets. Those emerging markets with low economic growth prospects, large macroeconomic imbalances and high external financing needs would become more vulnerable. The IMF8 noted that in a low interest rate environment, there is increased reliance on external debt in emerging market and frontier markets that could trigger a rollover of debt, undermine debt sustainability or increase distress risks. Hence, the IMF recommends that macroprudential policies be constantly reviewed to anticipate the impact of an abrupt end to accommodative monetary policy and the subsequent tightening of market conditions

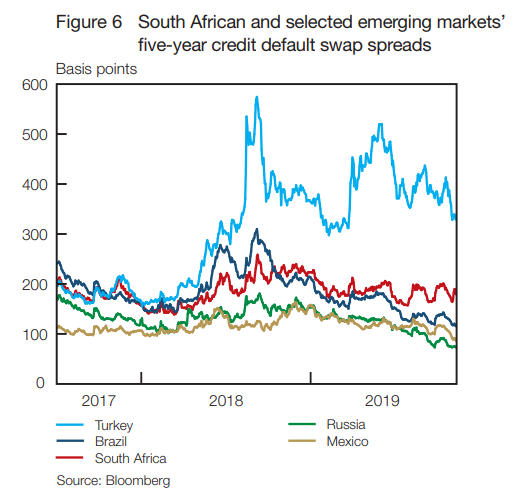

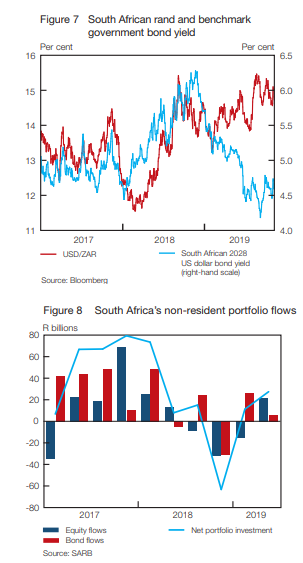

Domestic financial markets tracked volatile global conditions alongside low domestic growth outcomes and fiscal concerns that continued to cloud the country’s sovereign credit rating outlook. A comparison of South Africa’s credit default swap spread relative to B-rated emerging markets (Figure 6) suggests that markets have somewhat priced in further downgrades to the sovereign credit rating, particularly from Moody’s which is the last of the recognised rating agencies that has not downgraded South Africa’s local currency rating to subinvestment grade. Nonetheless, it is important to guard against complacency and not underestimate the possibility of high levels of volatility and asset price losses associated with a Moody’s downgrade decision. During the period under review, the exchange value of the rand was also affected by higher global risk aversion and negative local developments (Figure 7). The exchange value of the rand depreciated by more than 6.0% against the US dollar and traded in a wide range of between R13.81 and R15.50. Domestic bond yields increased on announcements of further bailouts for some of the SOEs as well as implications for the government’s already high debt burden and the sovereign risk rating. However, for the year to date, yields are lower and in line with the global trend. Financial flows to South Africa, which tend to influence the performance of domestic financial assets such as the rand and bonds, have been volatile in recent years. This has largely been due to idiosyncratic factors and changes in global risk appetite. As at the second quarter of 2019, portfolio investments recorded a rise in net inflows. This was due to a sharp reduction in residents’ holdings of foreign portfolio assets and a slight increase in net purchases of local equities by foreigners that offset the impact of continued net sales of local bonds by foreigners and the repayment of a foreign loan by government (Figure 8).

Continued net portfolio flows to the country will be dependent on whether global risk appetite improves and translates into foreign investment in domestic bonds and equities. In addition, a sovereign credit rating downgrade by Moody’s, while priced in by most market participants, could result in liquidations of bonds by foreign investors, thereby reducing the ability of the country to comfortably finance the current account deficit.

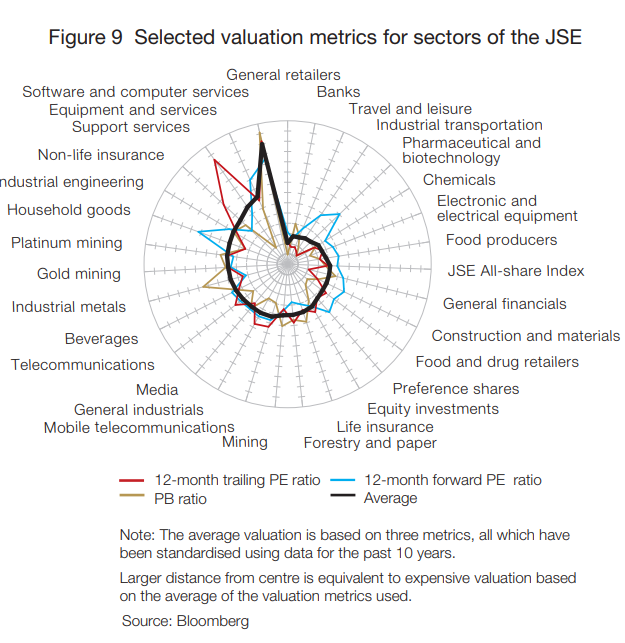

The domestic equity market, proxied by the JSE Limited (JSE) All-share Index, maintained its gains for the year, but exhibited a relatively higher degree of volatility. This was in line with a global trend where risky assets had to contend with risk-off sentiment amid increasing downside risks to global growth. The broader search for yield among global investors is prompting higher asset price valuations, thus creating vulnerabilities in the global financial system, particularly because of growing threats to corporate earnings that, in some regions, are already being revised downwards. This dynamic is likely to worsen financial imbalances as equity valuations are propped up by expectations of further monetary policy easing rather than a response to improving fundamentals. By contrast, valuations on domestic equities have, on average, declined, partly because the domestic equity market did not necessarily benefit greatly from foreign portfolio investments due to downside risks to growth and weak confidence. This has led to a correction of valuations in sectors such as mining, retail, and financial services, among others (see figure 9 below)

. The performances of retail and bank stocks have been under pressure on the JSE so far this year. Since the beginning of 2019, the JSE All-share Index has gained over 5%, while retailers and banks have declined by about 18% and 5% respectively. The underperformance of banks appears to be a global phenomenon, largely attributed to profitability concerns. However, the context within which this is happening abroad is slightly different from South Africa.

. The performances of retail and bank stocks have been under pressure on the JSE so far this year. Since the beginning of 2019, the JSE All-share Index has gained over 5%, while retailers and banks have declined by about 18% and 5% respectively. The underperformance of banks appears to be a global phenomenon, largely attributed to profitability concerns. However, the context within which this is happening abroad is slightly different from South Africa.

For example, low profitability of banks in Europe and Japan is partly driven by low interest rates and flatter yield curves, which are compressing interest margins for banks. These developments are leading to concerns that banks may now venture into inherently risky (or riskier) assets in search for higher yields – a trend that might introduce more vulnerabilities into the global financial system. While South African banks have underperformed and the risk premium for banks is rising, they remain profitable and the composition of their risk-weighted assets does not suggest an unusual take-up of risk onto bank balance sheets. The increase in the risk premium, measured using an average of the major banks’ credit default swap spreads over the sovereign has, however, been persistent. Despite the increase in the risk premium, which could be read as a sign of domestic banks coming under pressure, there are no signs of negative spillovers to financing conditions for banks. Wholesale deposit funding costs for banks remain stable and have been oscillating within a narrow range around the policy rate (Figure 10). In the domestic interbank market, funding spreads have also been relatively stable. The utilisation of standing facilities within the SARB as well as bidding behaviour in the SARB’s main repurchase (repo) auction is also not suggesting any existence of abnormal behaviour that may indicate stress.

Loans and advances and impairments

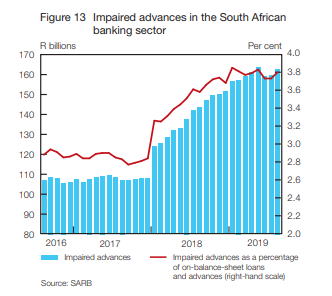

The banking sector’s impaired advances have moderated since January 2019 after trending upwards in the previous year. The banking sector’s impaired advances as a percentage of loans and advances11 have moderated since peaking at 3.85% in January 2019 (Figure 13).12 This was largely due to slower growth in impaired advances of 4% from January 2019 to August 2019, compared to an increase in on-balance-sheet loans and advances of 5% (over the same period). There has been an increase in mortgage loans granted with loan-to-value ratios in excess of 100%. As at August 2019, gross credit exposure to residential mortgages constituted 18.2%, relatively unchanged over the past year. The average LTV ratios for the residential mortgages portfolio have been relatively stable since 2016, with around two thirds in the less than 80% LTV band, between 26% and 28% in the greater than 80% but less than 100% LTV band, and approximately 6% in the greater than 100% LTV band. Almost a quarter of new mortgage loans that originated during 2019 was granted with LTVs in excess of 100%, compared to 17% in 2016. On average, there has been a slight decrease in new mortgage loans granted with LTVs of greater than 80% but less than 100%, suggesting that households have reduced capacity to put down a deposit on residential mortgages compared to four years ago.

For financial stability, it is important to analyse credit risk to identify vulnerabilities in the financial system that could have the effect of amplifying a shock to the system. The next section provides an analysis of credit risk in the South African banking sector. The sector’s credit sentiment has tightened towards business enterprises, but there is increased credit appetite for household credit cards and overdrafts. In its recent bank lending survey, the Centre of Excellence in Financial Services (COEFS) noted that banks had tightened their credit stance in the build-up to the sixth general election held in May 2019, as lending sentiment had deteriorated, mainly as a result of ongoing financial distress in SOEs, low confidence levels in certain state institutions and uncertainty relating to land expropriation.13 The draft National Credit Amendment Bill also impacted negatively across all classes of household lending in the lower-income categories, with lending in excess of one year and developmental credit being most affected. The COEFS noted that banks’ credit appetite towards middleand upper-income households was more favourable towards credit cards and overdrafts; however, there was negative sentiment towards motor vehicle finance. There was increased competition in residential mortgages compared to the previous six months. There was also a positive credit stance towards unsecured credit to households, although the perception of risk towards this asset class became negative following concerns of consumer creditworthiness and deteriorating economic activity. Banks’ credit sentiment towards business enterprises turned negative across all categories, except mining and quarrying. The most significant declines in sentiment were towards SOEs, manufacturing and construction.

The following section is related to the cyclical dimension of systemic risk, focusing on the build-up of risk over time.14 The analysis focuses on credit risk indicators such as the growth rate of lending asset classes and indicators of the quality of that lending (such as the 90 days overdue ratio). However, it must be pointed out that indicators are not a substitute for judgement, but rather a guide to offset inaction bias. The gap between on- and off-balance-sheet lending has increased, which could indicate an increase in new facilities or the increased repayment of existing facilities. The growth rate in off-balance-sheet facilities15 has exceeded that of on-balance-sheet loans and advances since April 2018 The increased growth in off-balance-sheet facilities is largely due to increased credit facilities to corporates and, to a lesser extent, retail revolving credit (including credit cards and revolving personal facilities). Although off-balance-sheet facilities for residential mortgages have increased, on average, by 5% since April 2018, there was a higher rate of growth in the period from August 2016 to April 2018. An increase in the growth of off-balance-sheet facilities compared to on-balancesheet loans and advances could be indicative of an increase in lending facilities or a repayment of loans.

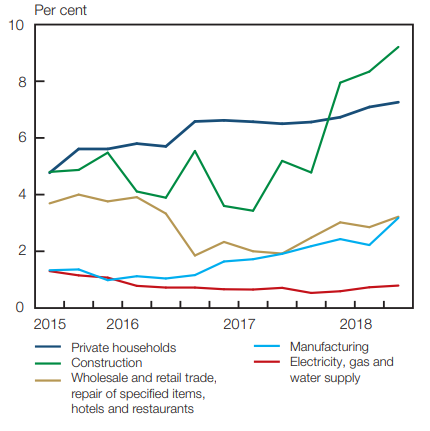

The banking sector has increased lending to the corporate sector compared to a year ago, with the highest sectoral growth rates being to the community, social and personal services; electricity, gas and water supply; and the financial intermediation and insurance sectors. The year-on-year growth of the total corporate and retail asset categories (8.3% and 6.2% respectively) exceeded that of the total sector16 (5.5%) in August 2019 (Figure 15). The corporate and retail credit categories constituted almost 73% of the sector’s total credit exposure as at August 2019. Growth in credit to public sector entities became positive in August 2019 (0.3%) following eight months of contraction, on a year-on-year basis. Growth in corporate credit exposure has been the largest contributor to the sector’s credit growth. The corporate asset class consists of corporate exposure (69%), small- and medium-sized enterprise (SME) corporate exposure (14%) and specialised lending exposure (17%). The sector’s credit growth trended upwards from a trough in February 2017 to a peak of 8.6% in May 2019, and has been mostly driven by increased lending to corporates.

The following section is related to the cyclical dimension of systemic risk, focusing on the build-up of risk over time.14 The analysis focuses on credit risk indicators such as the growth rate of lending asset classes and indicators of the quality of that lending (such as the 90 days overdue ratio). However, it must be pointed out that indicators are not a substitute for judgement, but rather a guide to offset inaction bias. The gap between on- and off-balance-sheet lending has increased, which could indicate an increase in new facilities or the increased repayment of existing facilities. The growth rate in off-balance-sheet facilities15 has exceeded that of on-balance-sheet loans and advances since April 2018 The increased growth in off-balance-sheet facilities is largely due to increased credit facilities to corporates and, to a lesser extent, retail revolving credit (including credit cards and revolving personal facilities). Although off-balance-sheet facilities for residential mortgages have increased, on average, by 5% since April 2018, there was a higher rate of growth in the period from August 2016 to April 2018. An increase in the growth of off-balance-sheet facilities compared to on-balancesheet loans and advances could be indicative of an increase in lending facilities or a repayment of loans.

The banking sector has increased lending to the corporate sector compared to a year ago, with the highest sectoral growth rates being to the community, social and personal services; electricity, gas and water supply; and the financial intermediation and insurance sectors. The year-on-year growth of the total corporate and retail asset categories (8.3% and 6.2% respectively) exceeded that of the total sector16 (5.5%) in August 2019 (Figure 15). The corporate and retail credit categories constituted almost 73% of the sector’s total credit exposure as at August 2019. Growth in credit to public sector entities became positive in August 2019 (0.3%) following eight months of contraction, on a year-on-year basis. Growth in corporate credit exposure has been the largest contributor to the sector’s credit growth. The corporate asset class consists of corporate exposure (69%), small- and medium-sized enterprise (SME) corporate exposure (14%) and specialised lending exposure (17%). The sector’s credit growth trended upwards from a trough in February 2017 to a peak of 8.6% in May 2019, and has been mostly driven by increased lending to corporates.

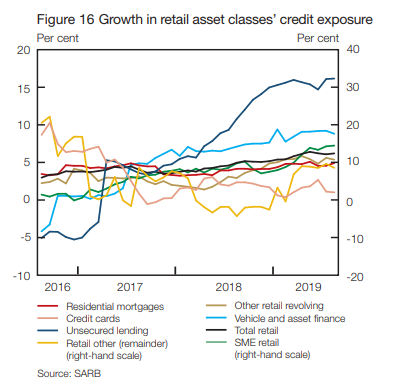

The three asset classes that grew at a higher rate than total retail credit growth of 6.2% (as at August 2019) are unsecured term lending (16.2%), vehicle and asset finance (8.8%), and credit cards (7.2%) (Figure 16). Over half of the sector’s retail lending is for residential mortgages (53%), with other significant subcategories being vehicle and asset finance (13%), credit cards (10%), SME retail (10%) and unsecured term lending (8%). For the period from August 2016 to October 2017, the sector’s total retail credit growth was consistently less than growth in the largest subcategory – residential mortgages. However, since October 2017, the sector’s total retail credit growth has consistently exceeded that of residential mortgages, with the growth differential averaging 1.4% from April to August 2019. This suggests that the sector has increased credit lending to other asset classes, in particular, unsecured lending as well as vehicle and asset finance. The growth differential between the sector’s total retail credit exposure and unsecured term lending has, for the most part, been negative since April 2017, and the differential between vehicle and asset finance has been negative since July 2017. This indicates that the sector has been increasing the credit exposure to these asset classes for at least the past two years. To conclude on credit risk, there has been a modest increase in the banking sector’s credit growth, mainly due to increased lending to corporates. The growth in off-balance-sheet facilities has consistently exceeded the growth in total credit, which could be indicative of new facilities being granted or the repayments of existing on-balance-sheet loans being continued. Credit sentiment to business entities appears to have turned negative, particularly towards public sector entities. However, there is increased credit appetite for household lending, specifically credit cards and overdrafts supplied to middle- to upper-income households.