|

Related Topics |

|

We take a look at South Africa's 1st financial stability for 2020 as reported by the South African Reserve Bank (SARB) . How has the Covid-19 affected South Africa's financial stability

|

|

What is financial stability?

According to the publication by the SARB, the purpose of the financial stability review and the definition of financial stability are discussed below

Purpose of the Financial Stability Review

The primary objective of the South African Reserve Bank (SARB) is to protect the value of the currency in the interest of balanced and sustainable economic growth in South Africa. In addition to this, the SARB’s function and mandate of protecting and enhancing financial stability in the Republic of South Africa is affirmed in the Financial Sector Regulation Act 9 of 2017 (FSR Act).

In pursuit of this objective, and to promote a stable financial system, the SARB publishes a semiannual Financial Stability Review. The publication aims to identify and analyse potential risks to financial system stability, communicate such assessments, and stimulate debate on pertinent issues. The SARB recognises that it is not the sole custodian of financial system stability, but that it contributes significantly towards and coordinates a larger effort involving government, other regulators, self-regulatory agencies, and financial market participants.

Defining ‘financial stability’

Financial stability is not an end in itself but, like price stability, is generally regarded as an important precondition for sustainable economic growth, development, and employment creation. Financial stability refers to a financial system that is resilient to systemic shocks, facilitates efficient financial intermediation, and mitigates the macroeconomic costs of disruptions in such a way that confidence in the system is maintained.

Purpose of the Financial Stability Review

The primary objective of the South African Reserve Bank (SARB) is to protect the value of the currency in the interest of balanced and sustainable economic growth in South Africa. In addition to this, the SARB’s function and mandate of protecting and enhancing financial stability in the Republic of South Africa is affirmed in the Financial Sector Regulation Act 9 of 2017 (FSR Act).

In pursuit of this objective, and to promote a stable financial system, the SARB publishes a semiannual Financial Stability Review. The publication aims to identify and analyse potential risks to financial system stability, communicate such assessments, and stimulate debate on pertinent issues. The SARB recognises that it is not the sole custodian of financial system stability, but that it contributes significantly towards and coordinates a larger effort involving government, other regulators, self-regulatory agencies, and financial market participants.

Defining ‘financial stability’

Financial stability is not an end in itself but, like price stability, is generally regarded as an important precondition for sustainable economic growth, development, and employment creation. Financial stability refers to a financial system that is resilient to systemic shocks, facilitates efficient financial intermediation, and mitigates the macroeconomic costs of disruptions in such a way that confidence in the system is maintained.

Financial stability risks and system resiliance

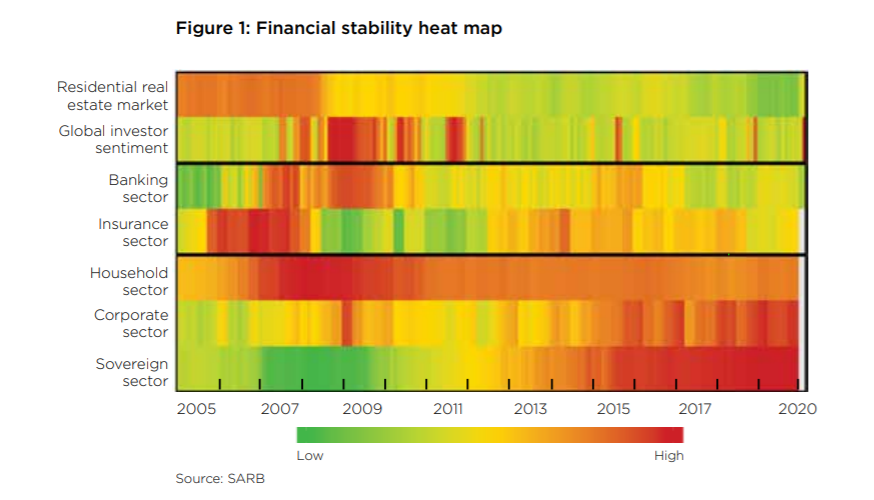

The South African Reserve Bank (SARB) monitors a wide range of sectors, asset markets and financial intermediaries for signs of financial stability risk. No single indicator can provide a comprehensive view of financial stability risk, thus a multitude of quantitative tools is used to support a qualitative assessment of risk. The financial stability heat map (Figure 1) is a visual depiction of various risk indicators. It provides an easy-to-interpret overview of the evolution of risk across different parts of the economy. Box 1 outlines the key elements of the heat map. The data in the heat map are released with a lag, so they do not capture the full effects of COVID-19. Depending on the scale and duration of the economic shock caused by COVID-19, the heat map could change substantially over the coming months. Grey areas in the heat map reflect sections for which data are not yet available

The South African heat map currently consists of seven categories:

The residential real estate market category consists of two indicators: the annual growth rate of the Standard Bank House Price Index, and mortgage loans as a share of total loans.

- The global investor sentiment category consists of the Chicago Board Options Volatility Index (VIX) as a one-sided and double-sided indicator of risk appetite. The VIX is included as a double-sided indicator because both high and low values could point to increased vulnerability. Thus, the two-sided VIX goes red when approaching both 0 and 1, and green as it approaches 0.5.

- The banking sector category consists of five indicators, namely: averages for the sector-wide value of assets to equity, impaired advances to gross loans and advances, the liquidity coverage ratio (LCR), the assets-to-gross-domestic product (GDP) gap, and the credit-to-GDP gap. This category provides a composite measure of the buffers in the banking sector to both solvency risk (the equity buffer) and liquidity risk (the LCR), as well as an indication of the level of credit risk building up in the system.

- The insurance sector category comprises five indicators, all sector-wide, namely: the assets-to-GDP gap, the combined ratio5 (non-life), growth in gross written premiums (life and non-life), the individual lapse ratio (life), and the solvency capital requirement (SCR) (life and non-life). This category provides a composite measure of the degree of risk taking by insurers, the growth in new business, underwriting profits, and buffers in place to absorb an adverse shock.

- The household sector category consists of three indicators: the debt-servicecost-to-disposable-income ratio, the debt-to-disposable-income ratio, and the debt-to-GDP ratio.

- The corporate sector category comprises three indicators for the non-financial corporate (NFC) sector: the debt-to-GDP ratio, the debt-to-net-operating-profit ratio, and the interest coverage ratio.

- The sovereign sector category makes use of a single indicator: the gross government debt-to-GDP ratio.

The heat map is an important input into the SARB’s financial stability monitoring process. Its relative simplicity presents both pros and cons. On the one hand, it provides a broad, consistent view of changes in certain financial variables over time. On the other hand, it only includes a subset of financial variables, and it aggregates these variables without assigning weights to them. Therefore, risk build-up in other areas of the economy, or in only one indicator, might be missed. Also, trend changes in some variables can occur, which may send misleading signals in the heat map (many indicators are assumed to be mean-reverting). It is therefore important to use the heat map alongside various other risk identification tools. The heat map is a ‘living’ indicator and is updated from time to time in line with international best practice

The residential real estate market category consists of two indicators: the annual growth rate of the Standard Bank House Price Index, and mortgage loans as a share of total loans.

- The global investor sentiment category consists of the Chicago Board Options Volatility Index (VIX) as a one-sided and double-sided indicator of risk appetite. The VIX is included as a double-sided indicator because both high and low values could point to increased vulnerability. Thus, the two-sided VIX goes red when approaching both 0 and 1, and green as it approaches 0.5.

- The banking sector category consists of five indicators, namely: averages for the sector-wide value of assets to equity, impaired advances to gross loans and advances, the liquidity coverage ratio (LCR), the assets-to-gross-domestic product (GDP) gap, and the credit-to-GDP gap. This category provides a composite measure of the buffers in the banking sector to both solvency risk (the equity buffer) and liquidity risk (the LCR), as well as an indication of the level of credit risk building up in the system.

- The insurance sector category comprises five indicators, all sector-wide, namely: the assets-to-GDP gap, the combined ratio5 (non-life), growth in gross written premiums (life and non-life), the individual lapse ratio (life), and the solvency capital requirement (SCR) (life and non-life). This category provides a composite measure of the degree of risk taking by insurers, the growth in new business, underwriting profits, and buffers in place to absorb an adverse shock.

- The household sector category consists of three indicators: the debt-servicecost-to-disposable-income ratio, the debt-to-disposable-income ratio, and the debt-to-GDP ratio.

- The corporate sector category comprises three indicators for the non-financial corporate (NFC) sector: the debt-to-GDP ratio, the debt-to-net-operating-profit ratio, and the interest coverage ratio.

- The sovereign sector category makes use of a single indicator: the gross government debt-to-GDP ratio.

The heat map is an important input into the SARB’s financial stability monitoring process. Its relative simplicity presents both pros and cons. On the one hand, it provides a broad, consistent view of changes in certain financial variables over time. On the other hand, it only includes a subset of financial variables, and it aggregates these variables without assigning weights to them. Therefore, risk build-up in other areas of the economy, or in only one indicator, might be missed. Also, trend changes in some variables can occur, which may send misleading signals in the heat map (many indicators are assumed to be mean-reverting). It is therefore important to use the heat map alongside various other risk identification tools. The heat map is a ‘living’ indicator and is updated from time to time in line with international best practice

Financial cycle

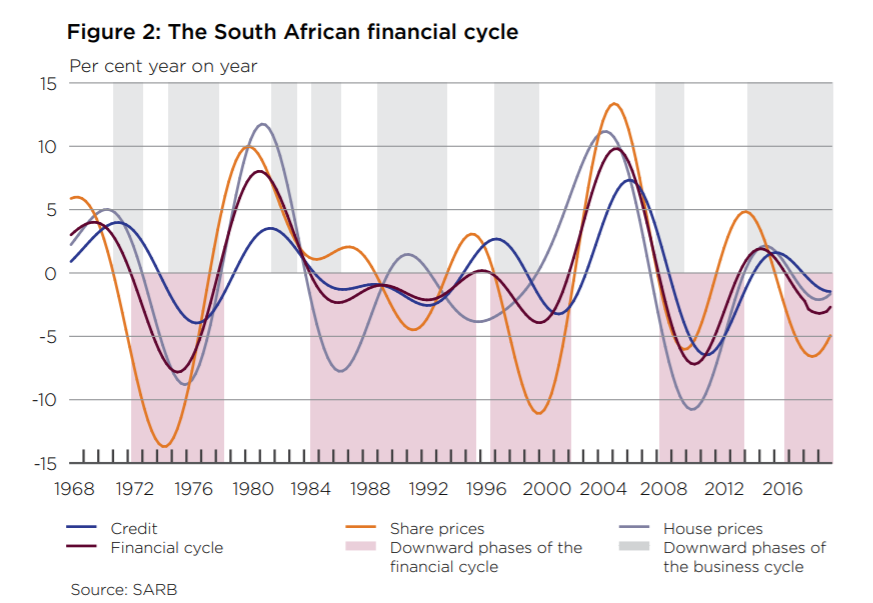

An important indicator of overall risk build-up in the financial system is the financial cycle. The financial cycle is measured by the co-movement of a set of financial variables, including credit growth, real estate price growth and equity price growth. Upward phases of the financial cycle are typically associated with rising financial stability risk. The financial cycle is currently in a downward phase, which began in the fourth quarter of 2016 (see Figure 2).

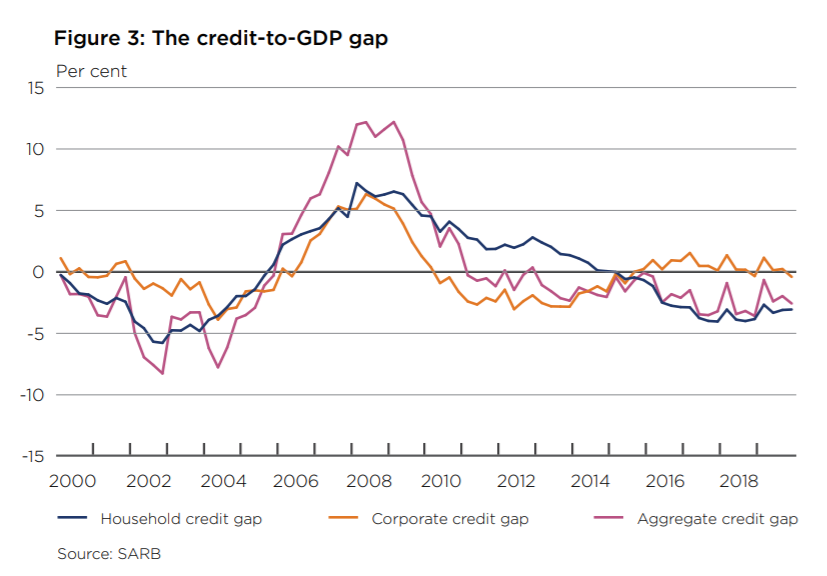

Furthermore, all three subcomponents are in a downward phase. This suggests that the COVID-19 shock has not come at a time of excessive risk taking. An indicator of risk build-up in the private sector is the credit-to-GDP gap.2 This indicator is used as a key input into the Financial Stability Committee’s (FSC) decisions over the use of the countercyclical capital buffer (CCyB). The credit-to-GDP gap is currently slightly negative as credit extension has been below its long-term trend since 2015 (see Figure 3). Disaggregating this measure, one can see that household credit has been growing well below trend, while corporate credit growth has been roughly in line with its historical trend (corresponding to a gap of zero). Private sector credit does not appear to have been excessive in the recent past. However, some household and corporate borrowers are facing elevated debt levels and debt service problems. While certain borrowers are excessively leveraged, the primary challenge faced by the private sector is one of slowing income growth and a weak business environment.

A further deterioration in domestic macroeconomic conditions

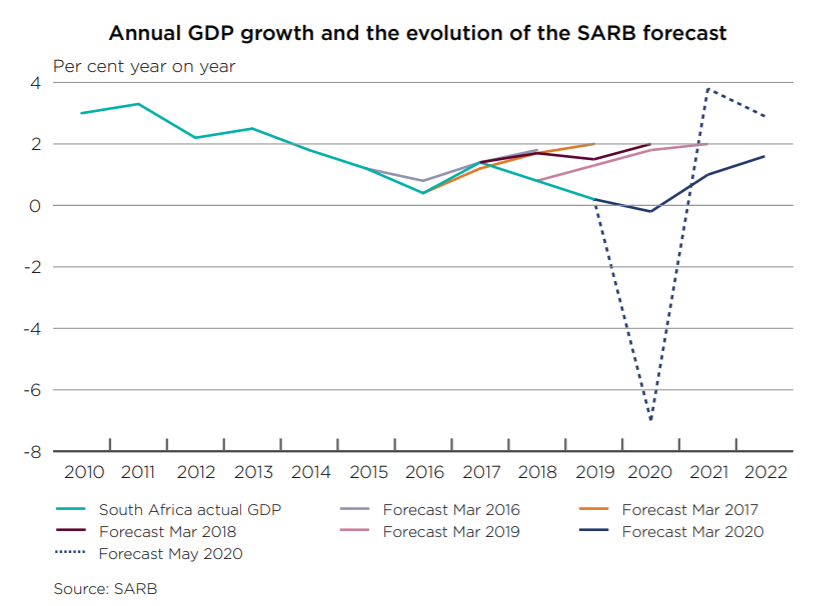

GDP growth in South Africa has persistently surprised to the downside in recent years. Economic activity has underperformed relative to the SARB’s expectations (and those of most analysts), resulting in continuous downward revisions to the growth outlook (see Figure 6). At the end of 2019, the economy was in a technical recession and in the longest business cycle downturn on record. Clearly, the COVID-19 pandemic struck at a time of macroeconomic vulnerability. The SARB expects a GDP contraction of 7% in 2020, the first full-year growth decline since 2009. This represents a substantial shock to the economy, as the worst full-year GDP growth performance in South Africa’s post-World War II history was -2.1% in 1992.

The decline in domestic growth over the past five years is mostly due to structural factors. The SARB’s estimate of the economy’s growth potential has fallen consistently, from approximately 3% for 2014 to 0.6% for 2019. Structural challenges – including skills shortages, infrastructure constraints (particularly in the energy sector) and policy uncertainty – have curbed the capacity of the economy to grow. While the SARB does anticipate an economic recovery after COVID-19 is contained, it is likely to be a relatively muted one due to these structural constraints. GDP is expected to grow by 3.8% in 2021 and 2.9% in 2022. The projection of a sharp contraction in 2020 and a relatively weak recovery implies that the level of real GDP in 2022 is likely be lower than that of 2018. As a result, financial firms could face challenges rebuilding capital buffers if they are worked down over the coming months. Should the economic downturn be deeper or more protracted than currently expected, financial stability risks will escalate

Banking sector-sovereign nexus in South Africa

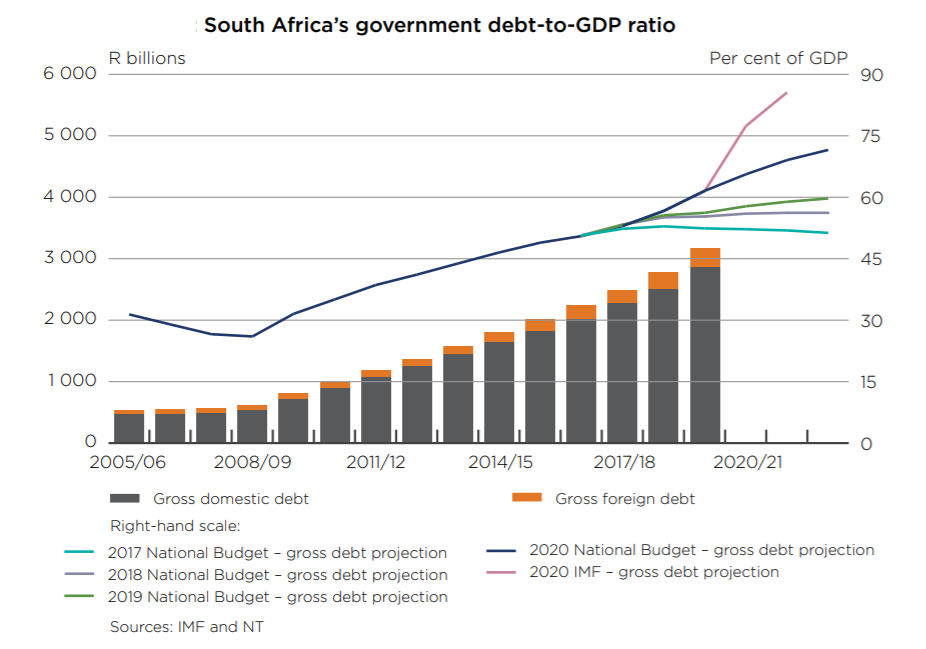

The financial soundness of the banking sector and the sovereign are closely linked. Linkages operate in both directions and include the facts that: government is the single largest debtor of the domestic banking sector, government financing costs influence those of the private sector, the actions of government affect the economy and the performance of the financial sector, and government typically acts as a backstop to the banking sector in the event of a bank failure. The banking sector-sovereign nexus is presently a threat to financial stability due to government’s large and increasing financing requirements. The 2020 National Budget projected a budget deficit of 6.8% of GDP for the current fiscal year, which would have been the largest in South Africa’s postapartheid history. However, since the National Budget was tabled in February, the economic outlook has deteriorated, and government has announced a substantial fiscal stimulus package in response to the COVID-19 outbreak. Therefore, public expenditure is likely to be significantly higher than initially expected and tax revenues are set to underperform.

As a result, the International Monetary Fund (IMF) has projected that South Africa’s government budget deficit will reach 13.3% of GDP in 2020 and 12.7% of GDP in 2021. Given these large deficits, the IMF expects a rapid increase in gross government debt to 85.6% of GDP in 2021.6 If this forecast does transpire, government debt as a share of GDP will have trebled over a 12-year period. South Africa’s sovereign credit ratings have all been lowered to sub-investment grade. In March 2020, Moody’s Investors Service (Moody’s) became the last major credit rating agency to reduce South Africa’s local and foreign currency credit rating to sub-investment grade. As a result, South Africa’s government bonds were excluded from the FTSE World Government Bond Index (WGBI) on 1 May 2020. This is an index passively tracked by a large number of investors globally. Moreover, many international bond funds are mandated to invest only in securities with a credit rating above investment grade. Consequently, the credit rating downgrade is expected to reduce the potential pool of investors into South Africa’s government bonds, with negative implications for government’s long-term cost of borrowing. At the same time that sovereign creditworthiness has deteriorated, banking sector exposures to the sovereign have increased. Sovereign exposures account for more than 15% of total banking sector assets, having roughly doubled over the past 12 years.7 Therefore, deteriorating fiscal metrics appear to have translated into adverse investor perceptions of the banking sector’s creditworthiness.

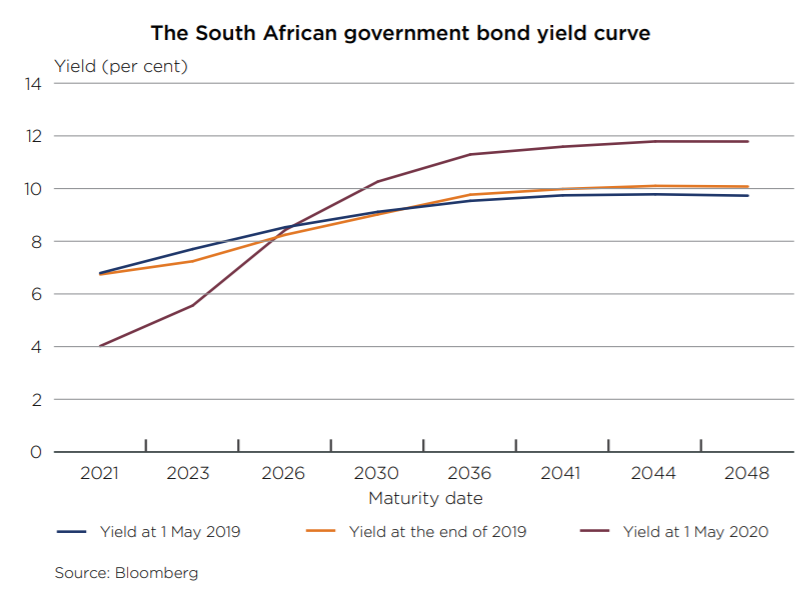

Government’s borrowing costs have increased in response to mounting fiscal risk.

The sharp increase in government’s funding requirements alongside heightened risk aversion across financial markets has resulted in substantially higher government bond yields, particularly for longer-duration debt. As a result, the spread between short- and long-term borrowing costs is at a historically elevated level. Should longer-term bond yields remain elevated, government may be forced to adjust its fiscal stance.

The financial stability implications of COVID-19

COVID-19 is not only a public health risk, but also a significant financial stability threat. This section outlines the potential channels through which

the virus may lead to financial instability. Possible mitigants and amplifiers to these channels of transmission are also discussed. Three main financial stability channels of transmission for the virus have been identified. These are: the direct effects on human health, the impact of disruptions to economic activity, and financial market-related risks.

The human health aspect of the virus could threaten operating capacity in the financial sector. Should COVID-19 spread widely, financial infrastructure and service providers could struggle to operate in an environment of high absenteeism. Given the interconnectedness of the financial system and the reliance on certain firms to provide key services, financial stability may be disrupted by the disease itself. The degree to which most financial institutions have adopted technology is a partial mitigant against this risk. However, skilled staff remain an important part of financial service provision. The absence of staff can also make a firm more vulnerable to other risks, such as cyberattacks and fraud.

The health impact could also have adverse effects on the insurance industry. Various lines of insurance could be affected by the virus, including life insurance as well as disability, business interruption and credit life insurance. The insurance industry is adequately capitalised to absorb higher than-expected claim levels. However, certain firms with high exposure to these business lines could come under stress. The SARB is closely engaged with the industry on this issue.

The macroeconomic impact of the virus and the precautions taken against it are projected to be very significant for South Africa. The resilience of the economy is hampered by a lack of fiscal space, which has constrained government’s ability to provide stimulus in response to the challenging economic outlook. COVID-19 also comes at a time of relative fragility for many borrowers. Weaker new business growth is expected for financial firms in 2020. However, the main negative impact on the sector is likely to occur through a rise in non-performing loans (NPLs). The deterioration in loan performance is expected to come through with a lag. As such, the full effect may only become apparent in late 2020 or early 2021. The economic effects of COVID-19 are being felt disproportionately across the economy, with certain sectors (such as hospitality and retail) being affected more than others

the virus may lead to financial instability. Possible mitigants and amplifiers to these channels of transmission are also discussed. Three main financial stability channels of transmission for the virus have been identified. These are: the direct effects on human health, the impact of disruptions to economic activity, and financial market-related risks.

The human health aspect of the virus could threaten operating capacity in the financial sector. Should COVID-19 spread widely, financial infrastructure and service providers could struggle to operate in an environment of high absenteeism. Given the interconnectedness of the financial system and the reliance on certain firms to provide key services, financial stability may be disrupted by the disease itself. The degree to which most financial institutions have adopted technology is a partial mitigant against this risk. However, skilled staff remain an important part of financial service provision. The absence of staff can also make a firm more vulnerable to other risks, such as cyberattacks and fraud.

The health impact could also have adverse effects on the insurance industry. Various lines of insurance could be affected by the virus, including life insurance as well as disability, business interruption and credit life insurance. The insurance industry is adequately capitalised to absorb higher than-expected claim levels. However, certain firms with high exposure to these business lines could come under stress. The SARB is closely engaged with the industry on this issue.

The macroeconomic impact of the virus and the precautions taken against it are projected to be very significant for South Africa. The resilience of the economy is hampered by a lack of fiscal space, which has constrained government’s ability to provide stimulus in response to the challenging economic outlook. COVID-19 also comes at a time of relative fragility for many borrowers. Weaker new business growth is expected for financial firms in 2020. However, the main negative impact on the sector is likely to occur through a rise in non-performing loans (NPLs). The deterioration in loan performance is expected to come through with a lag. As such, the full effect may only become apparent in late 2020 or early 2021. The economic effects of COVID-19 are being felt disproportionately across the economy, with certain sectors (such as hospitality and retail) being affected more than others

The duration of the constraints on economic activity will determine the longer-term risks. A key risk for the economy is that large-scale business closures and job losses may ensue during the period of COVID-19-related disruption. If this becomes the case, the economy may not recover to its previous level of potential output once the virus has been contained. This could limit the future earnings prospects, and debt service capacity, of both households and firms. Furthermore, the possibility of slower medium-term growth increases if financially weak firms remain afloat but are not profitable enough to invest in new capacity or productivity-enhancing processes.

Banks and insurers are generally well positioned to absorb this shock. Capital and solvency buffers provide space for financial firms to continue operating even as business conditions deteriorate. However, should economic activity remain weak after the immediate health emergency is over, the financial sector may face challenges in rebuilding buffers.

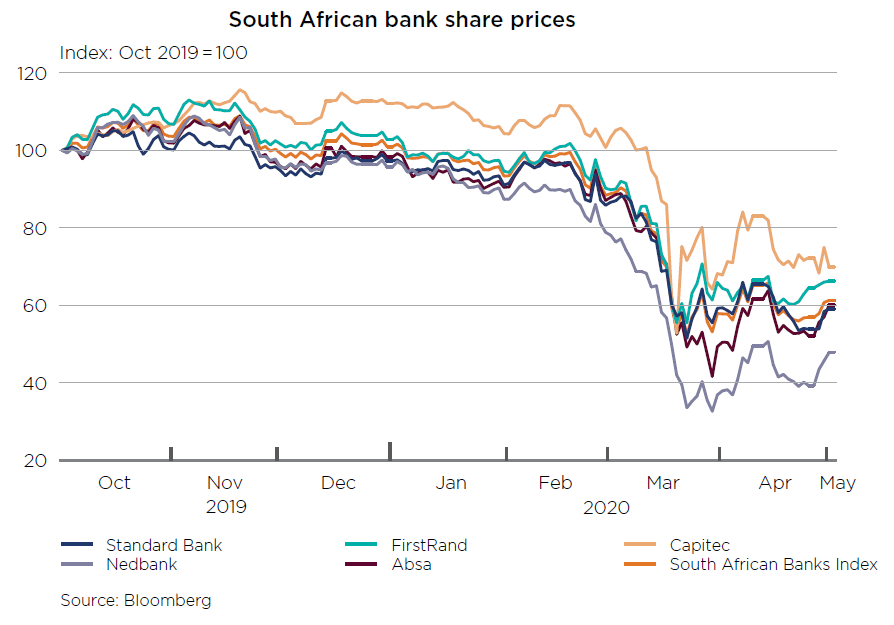

Non-resident portfolio flows into South Africa have contracted sharply. As risk aversion towards emerging markets has spread, a new record for nonresident portfolio outflows from South Africa in a single month was recorded in March 2020. Approximately R90 billion in foreign capital flowed out of the bond and equity markets during that month. Further non-resident outflows occurred in April, but the magnitude was significantly smaller at just over R24 billion. Non-resident outflows have been concentrated in the bond market, suggesting that foreigners were responding to South Africa’s sovereign credit rating downgrade and rising fiscal risk. The foreign selling of local assets has put significant downward pressure on the prices of these assets and has contributed to reduced liquidity in various financial markets.

Substantial financial market losses pose risks to both financial institutions and their customers. Financial institutions have recorded mark-to-market

losses on some trading portfolios as a result of the sharp asset price declines recorded since February 2020. Margin calls have also become more common in this environment of heightened volatility. Aside from the direct trading losses experienced by certain financial firms, lower asset prices affect the value of underlying collateral under credit agreements (such as home loans) and reduce the net wealth of borrowers, increasing their credit risk.

Banks and insurers are generally well positioned to absorb this shock. Capital and solvency buffers provide space for financial firms to continue operating even as business conditions deteriorate. However, should economic activity remain weak after the immediate health emergency is over, the financial sector may face challenges in rebuilding buffers.

Non-resident portfolio flows into South Africa have contracted sharply. As risk aversion towards emerging markets has spread, a new record for nonresident portfolio outflows from South Africa in a single month was recorded in March 2020. Approximately R90 billion in foreign capital flowed out of the bond and equity markets during that month. Further non-resident outflows occurred in April, but the magnitude was significantly smaller at just over R24 billion. Non-resident outflows have been concentrated in the bond market, suggesting that foreigners were responding to South Africa’s sovereign credit rating downgrade and rising fiscal risk. The foreign selling of local assets has put significant downward pressure on the prices of these assets and has contributed to reduced liquidity in various financial markets.

Substantial financial market losses pose risks to both financial institutions and their customers. Financial institutions have recorded mark-to-market

losses on some trading portfolios as a result of the sharp asset price declines recorded since February 2020. Margin calls have also become more common in this environment of heightened volatility. Aside from the direct trading losses experienced by certain financial firms, lower asset prices affect the value of underlying collateral under credit agreements (such as home loans) and reduce the net wealth of borrowers, increasing their credit risk.

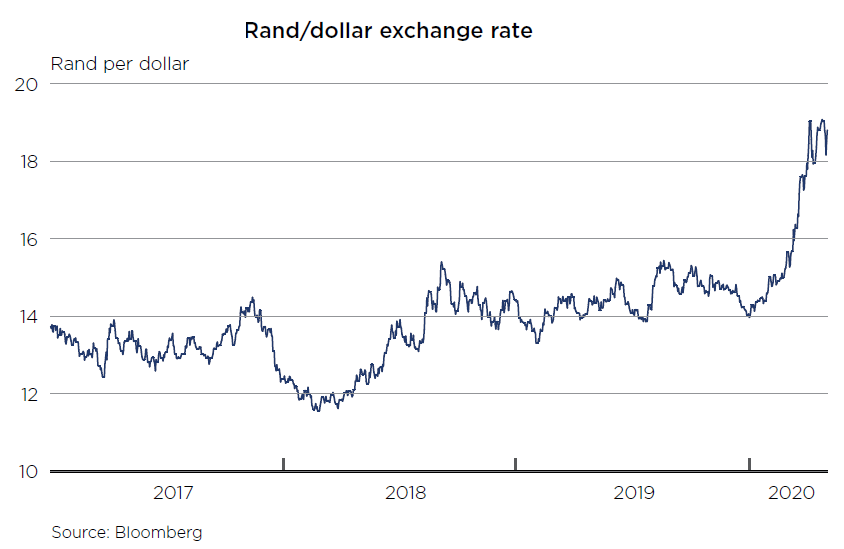

Weaker exchange is affecting foreign currency denominated debt

Foreign currency-denominated borrowing and capital repayment costs have increased in line with the depreciation of the rand against advanced economy currencies. In South Africa, regulations prohibit banks from having unhedged foreign currency exposures in excess of 10% of net qualifying capital and reserve funds. At the sector level, banks’ foreign currency loans and foreign currency liabilities are of a similar size (see the image below). Thus, the aggregate impact of the recent exchange rate depreciation on the financial position of banks has been relatively limited. Differences across firms in terms of the currency and maturity profile of the balance sheet imply, however, that exchange rate effects will be more significant for certain institutions.

Financial market pricing has become volatile, with signs of illiquidity having emerged. Liquidity in certain segments of South Africa’s financial markets has declined. This has occurred even in typically well-traded markets. For example, in late March 2020, bid-offer spreads (an indicator of market liquidity) for government bonds (which are among the most actively traded securities) reached levels approximately seven times larger than their historical average. Following the SARB’s interventions in the government bond market,these spreads have narrowed, but they remain wider than usual. Bid-offer spreads in the market for negotiable certificates of deposit (NCDs), which are short-term debt instruments issued by commercial banks, have increased significantly as well. Recent financial market pressures have also resulted in reduced corporate bond issuance.

Financial market pricing has become volatile, with signs of illiquidity having emerged. Liquidity in certain segments of South Africa’s financial markets has declined. This has occurred even in typically well-traded markets. For example, in late March 2020, bid-offer spreads (an indicator of market liquidity) for government bonds (which are among the most actively traded securities) reached levels approximately seven times larger than their historical average. Following the SARB’s interventions in the government bond market,these spreads have narrowed, but they remain wider than usual. Bid-offer spreads in the market for negotiable certificates of deposit (NCDs), which are short-term debt instruments issued by commercial banks, have increased significantly as well. Recent financial market pressures have also resulted in reduced corporate bond issuance.

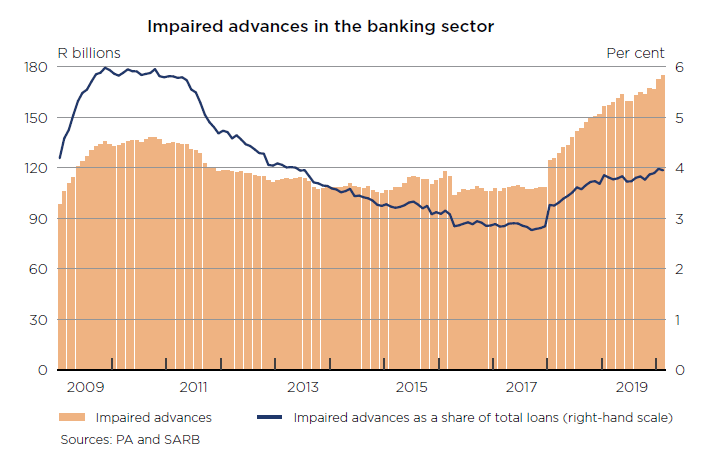

Impaired advances in the banking sector

The repayment capacity of borrowers is under pressure, resulting in higher levels of NPLs. The 90-days-overdue ratio for most of the sector’s loan portfolios has increased since early 2018. The loan portfolios showing the highest stress (in terms of this ratio) are retail unsecured term loans, retail revolving credit (consisting mainly of overdrafts and unsecured loans with a revolving component), and loans to public sector enterprises. The ratio of impaired advances to on-balance sheet loans and advances (a separate indicator of credit risk in the sector) has also increased since 2018 (see image below).

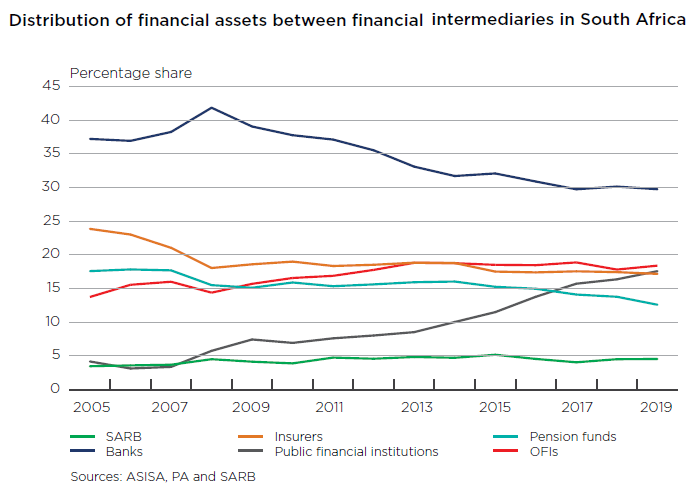

Non-bank financial intermediation

The share of non-banks in total financial intermediation has increased from less than 60% in 2008 to approximately 70% in September 2019. Non-bank financial intermediation (NBFI)44 is conducted by a combination of insurers, pension funds, the SARB, public financial institutions and other financial institutions (OFIs).45 The shift in the distribution of financial assets across intermediaries has occurred largely due to a rise in the share of assets held by public financial institutions and a decline in the share of banking sector assets

OFIs remain a key intermediary in the domestic financial system. OFIs are closely connected, both with one another and with the rest of the financial

sector. Banks and OFIs, for example, have funding channels operating in both directions. Bank funding from OFIs is substantial, ranging between 12% and 14% of total bank financial assets in recent years. Money market funds (MMFs) in particular provide an important share of bank funding. Banks, in return, provide OFIs with liquid assets.

sector. Banks and OFIs, for example, have funding channels operating in both directions. Bank funding from OFIs is substantial, ranging between 12% and 14% of total bank financial assets in recent years. Money market funds (MMFs) in particular provide an important share of bank funding. Banks, in return, provide OFIs with liquid assets.