|

Related Topics |

|

We take a look at the latest gross nominal savings rate of South Africans as calculated and published by the South African Reserve Bank (SARB). Do we as South African households, South African companies or the South African government save enough? In fact do we save at all? We know South Africa's government spends way more than it collects in taxes so what about South African companies and households?

|

|

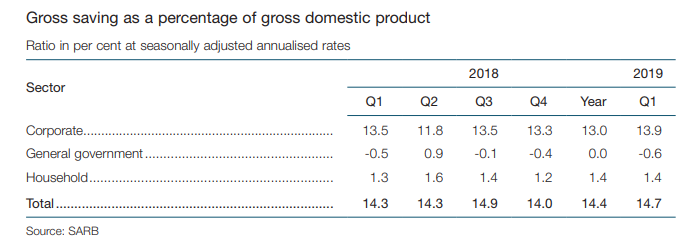

Gross nominal savings by households, companies and government

The South African Reserve Bank (SARB) had the following to say regarding South Africa's gross nominal savings.

South Africa’s national saving rate improved from 14.0% in the fourth quarter of 2018 to 14.7% in the first quarter of 2019. Higher saving by incorporated business enterprises and by households outweighed larger dissaving by general government. The foreign financing ratio, which represents the shortfall in domestic saving to finance capital formation, increased to 16.5% in the first quarter of 2019, from 13.6% in the previous quarter. Gross saving by the corporate sector as a percentage of GDP increased from 13.3% in the fourth quarter of 2018 to 13.9% in the first quarter of 2019, as the decrease in corporate tax payments outweighed the decline in operating surpluses.

South Africa’s national saving rate improved from 14.0% in the fourth quarter of 2018 to 14.7% in the first quarter of 2019. Higher saving by incorporated business enterprises and by households outweighed larger dissaving by general government. The foreign financing ratio, which represents the shortfall in domestic saving to finance capital formation, increased to 16.5% in the first quarter of 2019, from 13.6% in the previous quarter. Gross saving by the corporate sector as a percentage of GDP increased from 13.3% in the fourth quarter of 2018 to 13.9% in the first quarter of 2019, as the decrease in corporate tax payments outweighed the decline in operating surpluses.

Gross dissaving by general government as a percentage of GDP increased to 0.6% in the first quarter of 2019, from 0.4% in the fourth quarter of 2018. The slow pace of increase in government revenue, particularly taxes on production and imports, together with an increase in government expenditure, exacerbated dissaving by general government. Gross saving by the household sector as a percentage of GDP rose marginally to 1.4% in the first quarter of 2019. The increase in nominal disposable income marginally outweighed the increase in nominal consumption expenditure in the first quarter of 2019. Both household income and expenditure were constrained by slower growth in the compensation of employees and increased tax payments

We have to admit we are not surprised by dissaving taking place in the general government sector, as we show regularly on our Fiscal Policy page that the South African government spends far more than what it is collecting in terms of taxes, making it impossible for them to save. What we are rather surprised about is the continued high level of saving by the corporate sector. For a country that is looking to stimulate economic growth surely government should put policies in place in order to lure corporate sector into spending a but more of their saving. While savings is a good thing, we do need growth and perhaps providing incentives for corporates to spend some of their savings on employment, training and job creation projects is a way to kick start the South African economy. The table below shows the gross savings as percentage of GDP for corporate, general government and household sectors of South Africa

Seeing the low savings rate of the household sector is not really a surprise either considering the mountains of debt being taken on in South Africa each months. Earlier today we covered the latest banking sector information which showed that gross loans and advances in April 2019 increased by over 9% compared to April 2018. Especially strong growth was experienced by term loans (mostly unsecured short term personal loans). Below an extract from the article earlier today touching on the amount of bad debt South African banks are starting to right off/impair due to defaults on payments or total non payment of debt obligations.

In total South African banks wrote off or impaired loans that have been advanced to the value of R161.12 billion during April 2019. This is an increase of 22% on the R131.85 billion that was impaired by banks during April 2018. Impairments growing a lot faster than the new gross loans and advances that are being issued. And this will affect banks balance sheets and their overall profitability. Currently as at April 2019, 3.79% of all loans and advances made by South African banks are being impaired (or written off). This is up from 3.39% a year ago. If banks, South African's, government of the South African Reserve Bank needed a sign that South African consumers are really struggling this is it. South African's are struggling to pay back and service all their debt. And South Africa needs a more expansionary or accommodating monetary policy, not only to assist ailing South Africa consumers but to give South Africa's economy a boost.

In total South African banks wrote off or impaired loans that have been advanced to the value of R161.12 billion during April 2019. This is an increase of 22% on the R131.85 billion that was impaired by banks during April 2018. Impairments growing a lot faster than the new gross loans and advances that are being issued. And this will affect banks balance sheets and their overall profitability. Currently as at April 2019, 3.79% of all loans and advances made by South African banks are being impaired (or written off). This is up from 3.39% a year ago. If banks, South African's, government of the South African Reserve Bank needed a sign that South African consumers are really struggling this is it. South African's are struggling to pay back and service all their debt. And South Africa needs a more expansionary or accommodating monetary policy, not only to assist ailing South Africa consumers but to give South Africa's economy a boost.