|

Related Topics |

|

We take a look at the latest banking sector information published by the South African Reserve Bank (SARB) and find that gross loans and advances issued by banks have grown significantly over the last year while the impaired advances from banks increased sharply showing consumers are struggling to pay back their outstanding debt

|

|

So how many banks are there in South Africa as at April 2019?

Based on the data from the South African Reserve Bank (SARB) we can say the following about banks in South Africa:

Registered Banks: 19

Mutual Banks: 4

Co-operative Banks: 4

Local branches of foreign Banks: 15

Foreign Banks with approved local representative offices: 30

So what do these banks balance sheets look like and how does it compare to a year ago?

Registered Banks: 19

Mutual Banks: 4

Co-operative Banks: 4

Local branches of foreign Banks: 15

Foreign Banks with approved local representative offices: 30

So what do these banks balance sheets look like and how does it compare to a year ago?

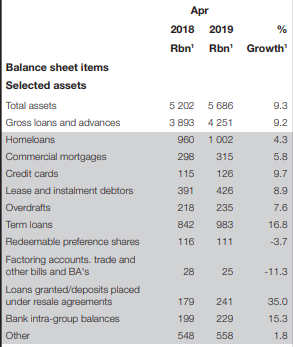

Total assets of banks in South Africa amounted to R5.686 trillion in April 2019 , up from R5.202 trillion in April 2018. This equated to growth of 9.3% in Total assets for banks in South Africa. Gross loans and advances came in at R4.251 trillion in April 2019, up from R3.893 trillion in April 2018, which is growth of 9.2% year on year.

This is pretty strong and aggressive growth in the gross loans and advances. So in which category of gross loans and advances did the strongest growth take place over the last 12 months?

This is pretty strong and aggressive growth in the gross loans and advances. So in which category of gross loans and advances did the strongest growth take place over the last 12 months?

- Home loans: 4.3% growth to R1.002 trillion

- Commercial mortgages: 5.8% growth to R315 billion

- Credit cards: 9.7% growth to R126 billion (jip South Africans owe R126 billion on credit cards)

- Lease and instalment debtors: 8.9% growth to R426 billion

- Overdrafts: 7.6% growth to R235 billion (so South African's are using R235 billion worth of overdraft facilities)

- Term loans: 16.8% growth to R983 billion (mostly short term and personal loans being taken on). This is a massive amount of money and substantial growth being experienced in term loans. A sign for the South African Reserve Bank (SARB) that South African consumers are becoming ever more indebted.

So what about the South African banks profitability? The image below provides various ratios such as return on equity and return on assets for South African Banks

Return on equity of South African banks decline from April 2018 to April 2019 with it falling from 15.93% to 15.5%. Return on assets decline from 1.33% to 1.26%. Cost pressures ar also starting to manifest as the cost t-to-income ration increased from 57.05% to 57.97% from April 2018 to April 2019. Net interest income earned by banks in April 2019 amounted to R167.53 billion.

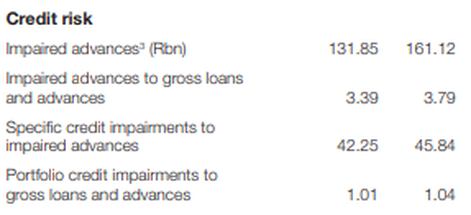

While non interest income of South African banks amounted to R127.92 billion in April 2019. So basically banks earn the bulk of their income from charging interest on loans, with banking and admin and other fees charged by banks making up 43.3% of total income earned while 56.7% of income earned from banks in South Africa comes from interest. But its not only sunshine and roses for South African banks. South African consumers are starting to default more and more on their loans and it shows with the impairments banks are making.

While non interest income of South African banks amounted to R127.92 billion in April 2019. So basically banks earn the bulk of their income from charging interest on loans, with banking and admin and other fees charged by banks making up 43.3% of total income earned while 56.7% of income earned from banks in South Africa comes from interest. But its not only sunshine and roses for South African banks. South African consumers are starting to default more and more on their loans and it shows with the impairments banks are making.

In total South African banks wrote off or impaired loans that have been advanced to the value of R161.12 billion during April 2019. This is an increase of 22% on the R131.85 billion that was impaired by banks during April 2018. Impairments growing a lot faster than the new gross loans and advances that are being issued. And this will affect banks balance sheets and their overall profitability. Currently as at April 2019, 3.79% of all loans and advances made by South African banks are being impaired (or written off). This is up from 3.39% a year ago. If banks, South African's, government of the South African Reserve Bank needed a sign that South African consumers are really struggling this is it. South African's are struggling to pay back and service all their debt. And South Africa needs a more expansionary or accommodating monetary policy, not only to assist ailing South Africa consumers but to give South Africa's economy a boost.