|

South Africa's money supply growth remains sluggish, in keeping with poor economic growth

Date: 16 April 2019 Category: Economics |

Related Topics |

|

We take a look at he growth rate in the broad definition of a country's money supply, M3, which is all notes and coins in circulation as well as short term deposit holdings at financial institutions.

With money supply growing slowly, it cannot be argued that increased money supply is a driver of inflation in South Africa. |

|

M3 money supply growth continue to slow

So the velocity theory of money is that the more money is in circulation the greater the inflation rate will be, as excess money is spent on goods and services, which fuels demand, which in turn fuels inflation. This type of inflation is called demand pull inflation, where greater demand for goods leads to retailers and wholesalers pushing up prices in order to maximise profits while there is strong demand for goods and services. But with the growth in money supply declining it cannot be argued that excess money is driving inflation. So lets take a look at the growth in South Africa's money supply in recent years and what the South African Reserve Bank (SARB) says about it.

The following was taken from the latest SARB quarterly bulletin "Growth in the broadly defined money supply (M3) remained roughly at the same subdued level in 2018 as in 2017 and aligned with the moderate growth in nominal GDP. Muted growth in the deposit holdings of the corporate sector during 2018 reflected subdued financial company deposits in the first half of the year and a deceleration in non-financial company deposits towards year-end amid subdued economic conditions. Slower wage growth contributed to a further deceleration in households’ deposit holdings, which became more noticeable towards the end of 2018. The quarter-to-quarter seasonally adjusted and annualised growth in M3 decelerated from 9.3% in the third quarter of 2018 to 4.4% in the fourth quarter. The income velocity of circulation of M3 remained unchanged at 1.42 in the fourth quarter of 2018, as the quarterly expansion in M3 matched that in nominal GDP".

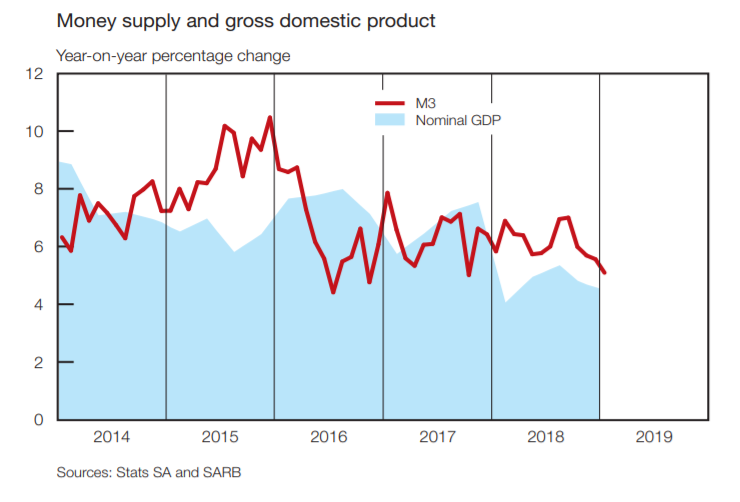

The image below shows the annual growth int the M3 money supply as well as the annual growth in nominal GDP (GDP not adjusted for the effects of inflation)

The image below shows the annual growth int the M3 money supply as well as the annual growth in nominal GDP (GDP not adjusted for the effects of inflation)

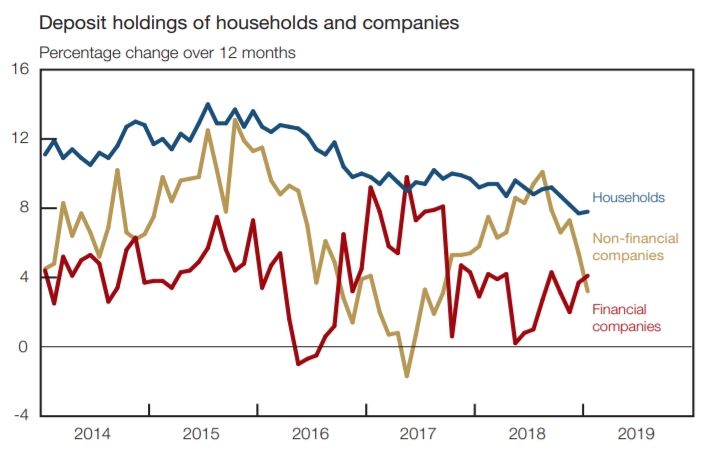

The image shows that the trends between M3 and nominal GDP is fairly similar, and currently both continuing to show declines in annual growth rates as sluggish economic conditions in South Africa persists. SARB also released numbers regarding depost holdings of individuals ad companies and had the following to say. "Year-on-year growth in M3, which had initially fluctuated higher from 5.8% in January 2018 to 7.0% in August, subsequently moderated to 5.6% by year-end. Growth in the deposit holdings of the corporate sector averaged 4.8% in 2018 and slowed from 5.9% in August to 3.7% in January 2019. "

"Weak growth in the deposit holdings of financial companies in the first half of 2018 recovered from less than 1.0% in May and June to 3.7% in December and 4.1% in January 2019. By contrast, growth in the deposit holdings of non-financial companies slowed from a recent high of 10.1% in August 2018 to 5.4% in December and 3.2% in January 2019 following a rebound from -1.7% in May 2017. Growth in the deposit holdings of the household sector slowed from an average of 9.7% in 2017 to 8.9% in 2018 following a recent deceleration from 9.2% in September to 7.8% in January 2019 alongside relatively constrained household income growth."

So as we mentioned in an earlier article, household debt is on the increase and on the flip side deposit holdings from households are on the decline, so taking on more debt and saving less is the basic theme of households. This is not an economy that is in good shape.

So as we mentioned in an earlier article, household debt is on the increase and on the flip side deposit holdings from households are on the decline, so taking on more debt and saving less is the basic theme of households. This is not an economy that is in good shape.