|

Related Topics |

|

We take a look at the share price performance of some of the main retailers and wholesalers listed on the JSE and how the market has punished these shares due to poor trading updates released.

We will look at:

|

|

Its been a tough old year for retailers and wholesalers in South Africa

The companies we will be looking at all brought out trading updates in recent days and the market was not impressed with it at all, and it has sent investors in retail stocks running for the exits, as they expect lower profits, dividends and less capital appreciation potential of the shares in the short to medium term.

We will summarize the trading statements that were brought out by each of these companies and then take a look at their share price performance over the last couple of days, months and years.

Shoprite:

The Shoprite Group increased total turnover by 0.03% to approximately R72.9bn billion in the 6 months to December 2018. Including the impact of the Angolan hyperinflation accounting adjustment, the Group's turnover declined by 0.01%. In difficult circumstances, the Group managed to increase the number of customer visits by 1.7% and product volumes by 0.2%.

Massmart:

Massmart’s total sales for the 52-week period of R90.9 billion increased by 2.9%, with comparable store sales increasing by 1.2%, and with product deflation estimated at 0.2%. These figures are compared to the 2017 52-week period excluding Shield (see the IFRS 15 explanation below). Despite a satisfactory sales performance over the Black Friday period, sales growth slowed in all Divisions apart from Massdiscounters in both November and December 2018. The slowdown resulted in total and comparable sales growths in that two-month period being 0.1% and -0.9% respectively.

Woolworths:

Group sales for the 26 weeks ended 23 December 2018 increased by 1.9% (+2.7% in constant currency) compared to the 26 weeks ended 24 December 2017. Sales growth was impacted by one day less of pre-Christmas trade, compared to last year.

Woolworths Fashion, Beauty and Home (‘FBH’) sales declined by 2.0% (comparable stores were 2.4% lower), impacted by a significantly smaller winter clearance sale in the first quarter. Sales in the second quarter of the year have, however, shown positive growth. Price movement was 1.7% for FBH, (and 0.8% for Fashion). Net retail space grew by 0.6%.

Woolworths Food sales increased by 6.3% (and by 7.0% if adjusted for the earlier close), with volume growth driven by low inflation, higher levels of promotions and price investment. Price movement was 1.2%. Comparable store sales increased by 4.2%, with net retail space growth of 1.4%. The

Woolworths Financial Services debtors book reflected positive year-on-year growth of 4.8% as at the end of December 2018. The annualised impairment rate for the six months ended 31 December 2018 was 3.5% (6 months ended 31 December 2017: 5.0%). The Group implemented IFRS 9 with effect from 1 July 2018.

David Jones sales increased by 1.0%, with sales performance weakening in line with the rest of the retail market in the final weeks leading up to Christmas. Comparable store sales grew by 0.9%, with growth from new stores largely offset by sales disruption from the Elizabeth Street store refurbishment. Net retail space grew by 2.7%. Further net space reductions to improve the productivity of the store portfolio are planned. Online sales have grown by 46.1%, and now contribute 7.7% of total sales. Country Road Group sales increased by 2.3%, and by 0.5% in comparable stores. Online sales grew by 20.0% over the period, representing 17.7% of sales. Net retail space contracted by 1.7%.

Mr Price (MRP):

Group retail sales and other income (RSOI) for the nine month period ended 29 December 2018 increased 5.8% over the corresponding period in the prior year (“Corresponding Period”). The Group’s South African retail sales growth exceeded the combined sales growth of Type D and Type E retailers per Stats SA for April to November (the period for which market information is available) indicating continued market share gains. During the third quarter (30 September 2018 to 29 December 2018) of the financial year ending 30 March 2019, RSOI grew 3.5% to R7.1bn. Total retail sales of R6.7bn (including franchise) were 2.0% higher. Corporate owned store performance was as follows:

The corporate store sales performance detailed above was below expectations and analysis thereof should consider: - sales growth of 8.5% in the Corresponding Period, which included a strong performance by the largest division, MRP Apparel, which grew sales 11.3%. - the prevailing poor economic and retail environments in several markets in which the Group trades. In our largest market, South Africa, the following factors have reduced consumer spending power: low GDP growth, rising unemployment and inflation levels, a VAT rate increase, higher average fuel prices and an interest rate increase in November 2018. - The deterioration in South African consumer confidence into Q3. This was in contrast to the optimism experienced in December 2017 post the ANC election outcome and subsequent change in South Africa’s president, which provided temporary support to the retail sector. - November trade being impacted by lower Black Friday sales. - December school holidays commencing a week later than the Corresponding Period. These holidays will return to normal in 2019.

We will summarize the trading statements that were brought out by each of these companies and then take a look at their share price performance over the last couple of days, months and years.

Shoprite:

The Shoprite Group increased total turnover by 0.03% to approximately R72.9bn billion in the 6 months to December 2018. Including the impact of the Angolan hyperinflation accounting adjustment, the Group's turnover declined by 0.01%. In difficult circumstances, the Group managed to increase the number of customer visits by 1.7% and product volumes by 0.2%.

Massmart:

Massmart’s total sales for the 52-week period of R90.9 billion increased by 2.9%, with comparable store sales increasing by 1.2%, and with product deflation estimated at 0.2%. These figures are compared to the 2017 52-week period excluding Shield (see the IFRS 15 explanation below). Despite a satisfactory sales performance over the Black Friday period, sales growth slowed in all Divisions apart from Massdiscounters in both November and December 2018. The slowdown resulted in total and comparable sales growths in that two-month period being 0.1% and -0.9% respectively.

Woolworths:

Group sales for the 26 weeks ended 23 December 2018 increased by 1.9% (+2.7% in constant currency) compared to the 26 weeks ended 24 December 2017. Sales growth was impacted by one day less of pre-Christmas trade, compared to last year.

Woolworths Fashion, Beauty and Home (‘FBH’) sales declined by 2.0% (comparable stores were 2.4% lower), impacted by a significantly smaller winter clearance sale in the first quarter. Sales in the second quarter of the year have, however, shown positive growth. Price movement was 1.7% for FBH, (and 0.8% for Fashion). Net retail space grew by 0.6%.

Woolworths Food sales increased by 6.3% (and by 7.0% if adjusted for the earlier close), with volume growth driven by low inflation, higher levels of promotions and price investment. Price movement was 1.2%. Comparable store sales increased by 4.2%, with net retail space growth of 1.4%. The

Woolworths Financial Services debtors book reflected positive year-on-year growth of 4.8% as at the end of December 2018. The annualised impairment rate for the six months ended 31 December 2018 was 3.5% (6 months ended 31 December 2017: 5.0%). The Group implemented IFRS 9 with effect from 1 July 2018.

David Jones sales increased by 1.0%, with sales performance weakening in line with the rest of the retail market in the final weeks leading up to Christmas. Comparable store sales grew by 0.9%, with growth from new stores largely offset by sales disruption from the Elizabeth Street store refurbishment. Net retail space grew by 2.7%. Further net space reductions to improve the productivity of the store portfolio are planned. Online sales have grown by 46.1%, and now contribute 7.7% of total sales. Country Road Group sales increased by 2.3%, and by 0.5% in comparable stores. Online sales grew by 20.0% over the period, representing 17.7% of sales. Net retail space contracted by 1.7%.

Mr Price (MRP):

Group retail sales and other income (RSOI) for the nine month period ended 29 December 2018 increased 5.8% over the corresponding period in the prior year (“Corresponding Period”). The Group’s South African retail sales growth exceeded the combined sales growth of Type D and Type E retailers per Stats SA for April to November (the period for which market information is available) indicating continued market share gains. During the third quarter (30 September 2018 to 29 December 2018) of the financial year ending 30 March 2019, RSOI grew 3.5% to R7.1bn. Total retail sales of R6.7bn (including franchise) were 2.0% higher. Corporate owned store performance was as follows:

The corporate store sales performance detailed above was below expectations and analysis thereof should consider: - sales growth of 8.5% in the Corresponding Period, which included a strong performance by the largest division, MRP Apparel, which grew sales 11.3%. - the prevailing poor economic and retail environments in several markets in which the Group trades. In our largest market, South Africa, the following factors have reduced consumer spending power: low GDP growth, rising unemployment and inflation levels, a VAT rate increase, higher average fuel prices and an interest rate increase in November 2018. - The deterioration in South African consumer confidence into Q3. This was in contrast to the optimism experienced in December 2017 post the ANC election outcome and subsequent change in South Africa’s president, which provided temporary support to the retail sector. - November trade being impacted by lower Black Friday sales. - December school holidays commencing a week later than the Corresponding Period. These holidays will return to normal in 2019.

So lets take a look at the share price performance of the above mentioned shares

The standard for the graphic above shows the share price if Massmart for the last month. Readers can select the time frame under the Zoom category, or type in their own dates they want to look at (within the last 2 years). As soon as you click on one of the other shares in the top left hand corner of the graphic, the graphic will recalculate the graph and show the share price returns of each share selected for the time period selected at the top of the graphic.

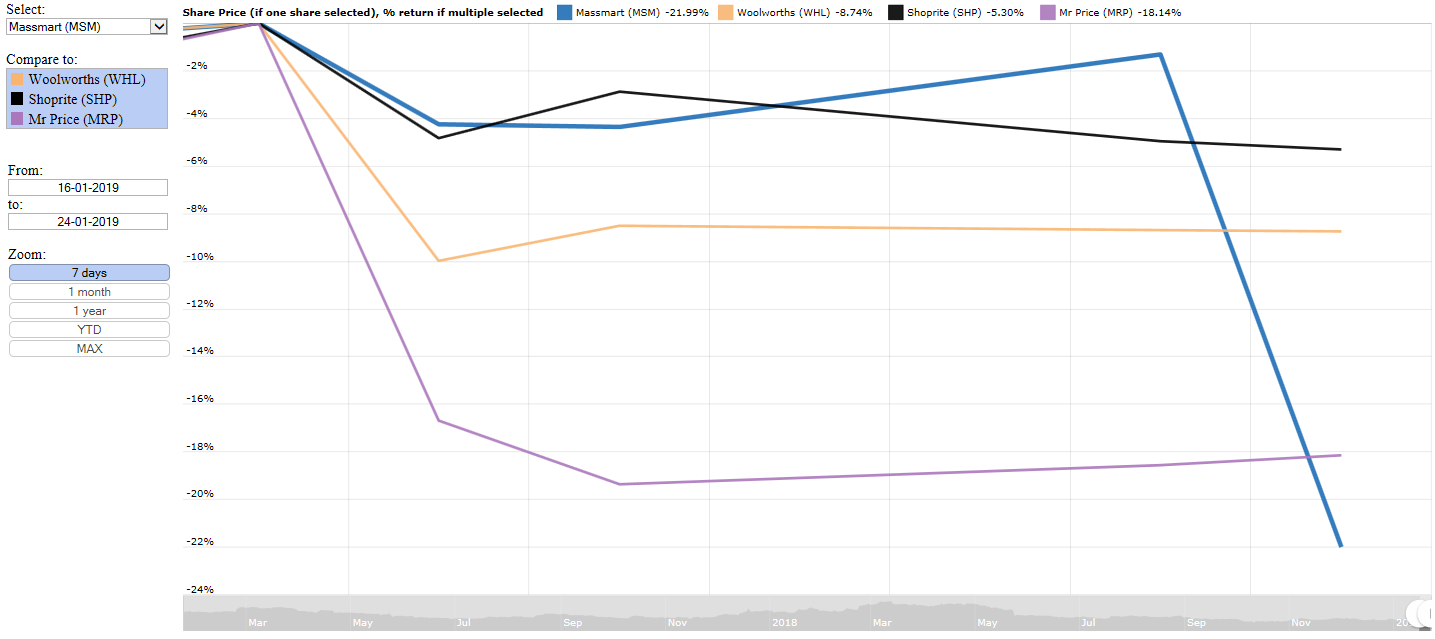

The image below shows the share price returns of all 4 shares mentioned at the start of the article for the last 7 days.

The image below shows the share price returns of all 4 shares mentioned at the start of the article for the last 7 days.

Share price performance over the last 7 days (ranked from poorest performer to best performer):

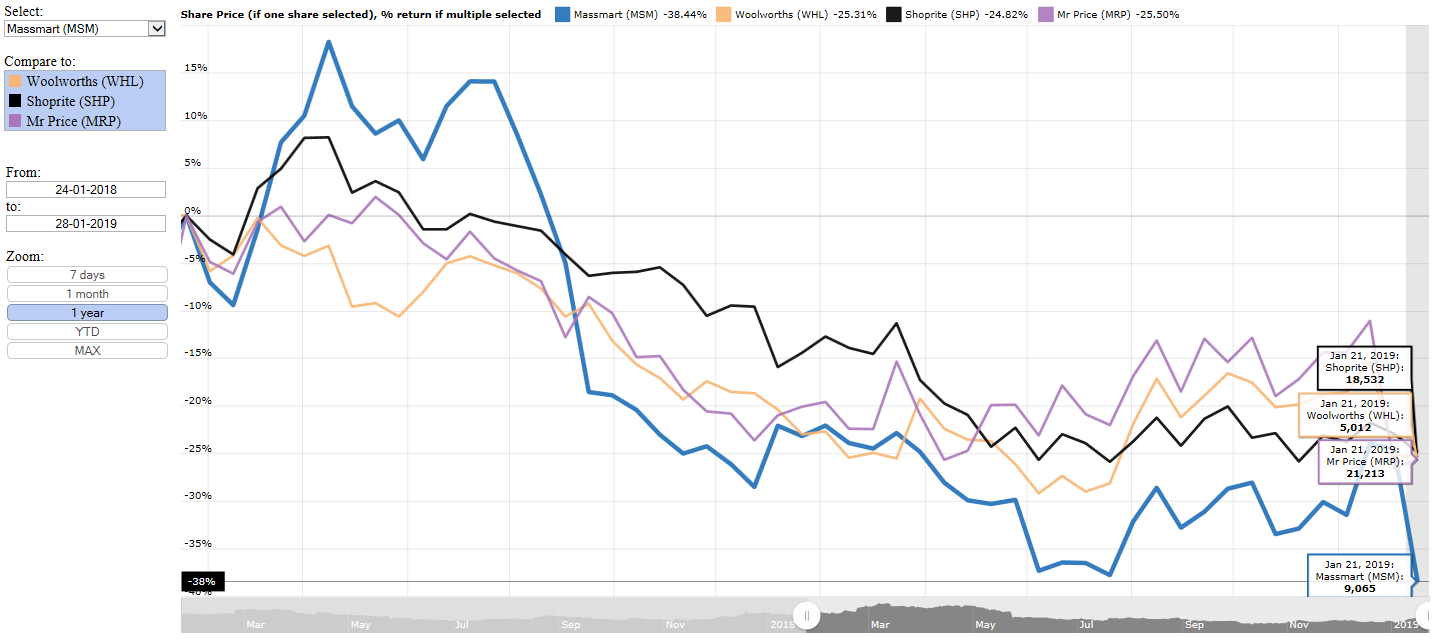

So they have all had a pretty tough time in the last 7 trading days. So what does their share price performance look like over a slightly longer period of time such as 1 year? The image below shows the 1 year share price performance of all the shares mentioned at the start of the article.

- Massmart (MSM): -21.99%

- Mr Price (MRP): -18.14%

- Woolworths (WHL): -8.74%

- Shoprite (SHP): - 5.3%

So they have all had a pretty tough time in the last 7 trading days. So what does their share price performance look like over a slightly longer period of time such as 1 year? The image below shows the 1 year share price performance of all the shares mentioned at the start of the article.

Share price performance over the last year (ranked from poorest performer to best performer):

So all of the shares mentioned lost at least quarter of its value over the last 12 months on the JSE. That is serious punishment being dished out by the market on listed retailers and wholesalers. By far the hardest hit is Massmart (owner of popular wholesaler MAKRO) with it losing 38.4% of its value in the last 12 months. Most investors, be they actual stock buyers or investors in unit trusts will feel this decline in retailers in their portfolios, as they make up a large chunk of most funds core holdings.

The JSE All Share total market capital has lost around R3 trillion in value in the last 12 months. Nowhere to run or hide for active or passive investors in the market right now.

- Massmart (MSM): -38.44%

- Mr Price (MRP): -25.50%

- Woolworths (WHL): -25.31%

- Shoprite (SHP): - 24.82%

So all of the shares mentioned lost at least quarter of its value over the last 12 months on the JSE. That is serious punishment being dished out by the market on listed retailers and wholesalers. By far the hardest hit is Massmart (owner of popular wholesaler MAKRO) with it losing 38.4% of its value in the last 12 months. Most investors, be they actual stock buyers or investors in unit trusts will feel this decline in retailers in their portfolios, as they make up a large chunk of most funds core holdings.

The JSE All Share total market capital has lost around R3 trillion in value in the last 12 months. Nowhere to run or hide for active or passive investors in the market right now.