|

Related Topics |

|

We take a look at Premier Fishing and Brands financial results for the year ending August 2018 and their dividend announcements as published on the Johannesburg Stock Exchange (JSE) news service earlier today

|

|

About Premier Fishing and Brands

Premier Fishing and Brands Limited through its subsidiaries operates a vertically integrated fishing business which specialises in the harvesting, processing and marketing of fish and fish-related products. The Group holds medium to long-term fishing rights in squid, lobster, small pelagics, hake deep-sea trawl, hake longline, horse mackerel, swordfish and tuna. The Group also owns an abalone farm and invests in organic fertilisers through the "Seagro" range of products. Premier Fishing and Brands was listed on the main board of the Johannesburg Stock Exchange (“JSE”) on 2 March 2017

Their range of brands include:

Their range of brands include:

- South Atlantic Lobster

- Atlantic Abalone

- Sea Diamanond

- Seagro

High level summary of the results

Highlights compared to the prior year:

- Revenue increased by 20% from R411 million to R491 million.

- Operating profit increased by 41% from R65 million to R92 million.

- Profit after tax increased by 40% from R68 million to R95 million.

- The acquisition of a 50.31% shareholding in Talhado Fishing Enterprises Proprietary Limited ("Talhado").

- Cash generated from operations increased by 128% from R40 million to R91 million.

- Gross dividends of 25 cents per share declared to shareholders (2017: 15 cents per share).

Profit after taxes of R95.3million on Revenue of R491million gives a net profit margin of 19.35%, which is extremely strong net profit margins and something the group should be proud of.

They have strong levels of cash and equivalents with the group sitting with R350.6 million in cash and equivalents (or R1.34 per share currently held in cash). Thus at a share price of R3.70 (36% of the share price is made up by cash on the balance sheet). So essentially the active business operations are bought with 64% of the share price, and the rest of the share price is buying cash on the books. They reported a net asset value (NAV) of R3.31 per share, up from R2.96 per share from a year ago. Essentially of they sell all their assets, pay off all their debts, investors will get R3.31 a share. So if the share price tanks and falls to the ground, investors can rest assured that they will get R3.31 a share if the business is liquidated and assets distributed among shareholders. The nice thing about this is that those investors looking to take a punt on the stock, at R3.70, the reported net asset value is not far off from the share price. Thus potential limited down side in the share as it is trading so close to its reported net asset value.

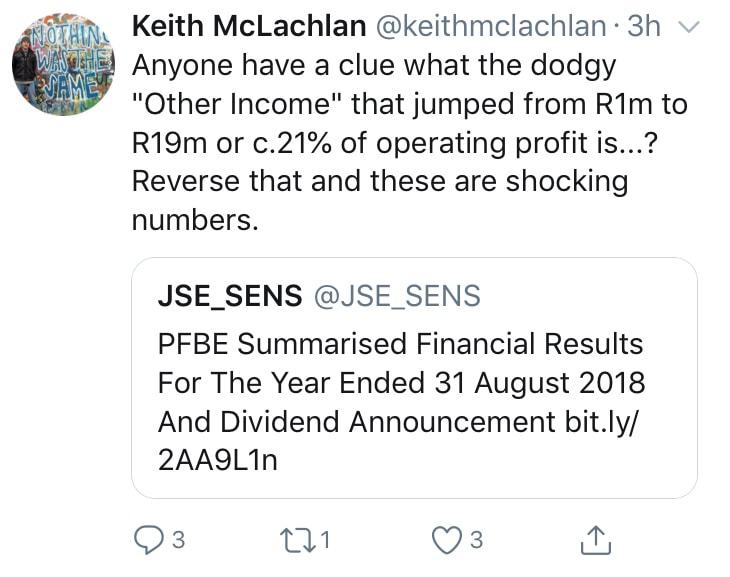

Cash generated from operations at R91million (or 34.6c) a share is very strong too. Headline earnings per share came in at 31.6c, which places the group on a moderate PE of 11.7. And the dividend for the year of 25c per share places them on a very healthy dividend yield of 6.8%. However well known equity analyst Keith Mchachlan from Smallcaps.co.za had a concern regarding their results. And he was referring to the "Other operating income" that jumped from around R1mil to R19mil. See his tweet below.

- Revenue increased by 20% from R411 million to R491 million.

- Operating profit increased by 41% from R65 million to R92 million.

- Profit after tax increased by 40% from R68 million to R95 million.

- The acquisition of a 50.31% shareholding in Talhado Fishing Enterprises Proprietary Limited ("Talhado").

- Cash generated from operations increased by 128% from R40 million to R91 million.

- Gross dividends of 25 cents per share declared to shareholders (2017: 15 cents per share).

Profit after taxes of R95.3million on Revenue of R491million gives a net profit margin of 19.35%, which is extremely strong net profit margins and something the group should be proud of.

They have strong levels of cash and equivalents with the group sitting with R350.6 million in cash and equivalents (or R1.34 per share currently held in cash). Thus at a share price of R3.70 (36% of the share price is made up by cash on the balance sheet). So essentially the active business operations are bought with 64% of the share price, and the rest of the share price is buying cash on the books. They reported a net asset value (NAV) of R3.31 per share, up from R2.96 per share from a year ago. Essentially of they sell all their assets, pay off all their debts, investors will get R3.31 a share. So if the share price tanks and falls to the ground, investors can rest assured that they will get R3.31 a share if the business is liquidated and assets distributed among shareholders. The nice thing about this is that those investors looking to take a punt on the stock, at R3.70, the reported net asset value is not far off from the share price. Thus potential limited down side in the share as it is trading so close to its reported net asset value.

Cash generated from operations at R91million (or 34.6c) a share is very strong too. Headline earnings per share came in at 31.6c, which places the group on a moderate PE of 11.7. And the dividend for the year of 25c per share places them on a very healthy dividend yield of 6.8%. However well known equity analyst Keith Mchachlan from Smallcaps.co.za had a concern regarding their results. And he was referring to the "Other operating income" that jumped from around R1mil to R19mil. See his tweet below.

Segmental analysis of profits

The summary below shows the profit before tax that each of Premier fishings main divisions brought in

- Lobster R53 941 000

- Pelagics R16 379 000

- Hake: R8 893 000

- Squid: R58 018 000

- Abalone: R12 175 000

- Horse mackerel: R879 000

- Cold storage: R359 000

- Seagro: R1 193 000

- Processing and marketing: R5 503 000

So what does the management team say about their results?

Lobster

The 2018 total allowable catch ("TAC") for south coast rock lobster ("SCRL") is 335 tons up by 1% from the prior year TAC of 331 tons. The quota which is available to Premier is 135 tons (2017: 133 tons). The 2018 TAC for west coast rock lobster ("WCRL") remained unchanged from the prior year at 1 924 tons however the offshore allocation decreased from 1 204 tons to 995 tons. The quota which is available to Premier is 64 tons (2017: 87 tons). The total WCRL contracted quota acquired for 2018 is 101 tons (2017: 96 tons). WCRL contribution to revenue and profits of the Group is less than 15%. The Group experienced increased landings due to good catch rates for the lobster division as well as bigger size mix for SCRL. The bigger size mix resulted in the Group achieving an increase of 3% in US dollar pricing for SCRL as compared to the prior period. The increased landings also resulted in increased sales volumes for the division as compared to the prior period. The good catch rates, increased market prices and volumes resulted in the division maintaining its margin despite the strengthening of the Rand against the dollar in the first half of the financial year.

Small pelagics

The Group’s 2018 quota allocation for Pilchards is 4 396 tons (2017: 3 383 tons). The catch rates for pilchards was lower than that of the prior year, industry wide resulting in lower landed and sales volumes of Pilchards in the current year. Industrial fish catch rates were the same as those experienced in the prior year. The lower landings and sales volumes for Pilchards resulted in lower revenues and operating profits for the division in the current year.

Squid

The acquisition of Talhado resulted in the increase in fishing rights and the number of fishing vessels utilised for squid from 4 vessels in the prior year to 22 vessels in the current year. The squid industry experienced exceptional catch rates in the current period. The landed volumes and sales volumes for the division were more than double those of the prior period. The market for South African squid remained stable despite the significant increase in landed volumes and the Euro sales prices achieved by the Group were the same as the prior period. The exceptional catch rates, increased sales volumes and consolidation of Talhado from 9 May resulted in an increase of 431% in operating profits of the division. Revenue of R80 million and profit after tax of R29 million has been consolidated from Talhado for the year ended 31 August 2018.

Hake

The 2018 TAC for hake is 133 119 tons. The quota which is available to the Group is 700 tons. The Group’s hake quota is caught, processed and marketed through a joint operation with Blue Continental Products (Pty) Ltd ("BCP") Hake. The catch rates for the division were similar to those of the prior period and the division also experienced a bigger size mix for its catches. There were unexpected major repairs and maintenance work done to the fishing vessel due to a breakdown which resulted in operating profits for this division being lower than the prior year.

Abalone

The Group commenced with construction of the expansion of the abalone farm. 40 tons of additional animal rearing capacity have been added to date and construction is anticipated to be completed by the end of Quarter 1 in 2019. The division is currently focused on increasing its spat ("Baby Abalone") production and stock holding in preparation for the farm is expansion. Sales volumes for the period were less than those of the prior period as the Group is growing out the animals to a bigger size for the market. Sales volumes are expected to increase once construction at the farm has been completed. The stock value increased by 25% from the prior year and this volume will be realised in the coming financial years. It is the Group’s intention to increase the stock value in line with the abalone expansion plans. Horse Mackerel The Group was awarded a horse mackerel quota of 800 tons during the FRAP2015/2016 process. The Group’s horse mackerel quota is caught, processed and marketed by Desert Diamond Fishing (Pty) Ltd. 100% of the quota was caught during the current period.

Seagro

Seagro is an organic fertiliser produced from Fish Oil which is a by-product of the Fishmeal making process. There was an increased availability of fish Oil in the current period which resulted in production of Seagro and increased sales volumes as compared to the prior period. The increased sales volumes in the current period resulted in increased profitability compared to the prior period.

Processing and marketing

The total WCRL contracted quota acquired for 2018 is 101 tons (2017: 96 tons). The total Wild Abalone contracted quota acquired for 2018 is 31 tons (2017: 30 tons). The quota holders landed their full quota allocations in the current financial year. Revenue and operating profits is lower than that of the prior year due to the strengthening of the Rand against the USD in the first half of the financial year.

The 2018 total allowable catch ("TAC") for south coast rock lobster ("SCRL") is 335 tons up by 1% from the prior year TAC of 331 tons. The quota which is available to Premier is 135 tons (2017: 133 tons). The 2018 TAC for west coast rock lobster ("WCRL") remained unchanged from the prior year at 1 924 tons however the offshore allocation decreased from 1 204 tons to 995 tons. The quota which is available to Premier is 64 tons (2017: 87 tons). The total WCRL contracted quota acquired for 2018 is 101 tons (2017: 96 tons). WCRL contribution to revenue and profits of the Group is less than 15%. The Group experienced increased landings due to good catch rates for the lobster division as well as bigger size mix for SCRL. The bigger size mix resulted in the Group achieving an increase of 3% in US dollar pricing for SCRL as compared to the prior period. The increased landings also resulted in increased sales volumes for the division as compared to the prior period. The good catch rates, increased market prices and volumes resulted in the division maintaining its margin despite the strengthening of the Rand against the dollar in the first half of the financial year.

Small pelagics

The Group’s 2018 quota allocation for Pilchards is 4 396 tons (2017: 3 383 tons). The catch rates for pilchards was lower than that of the prior year, industry wide resulting in lower landed and sales volumes of Pilchards in the current year. Industrial fish catch rates were the same as those experienced in the prior year. The lower landings and sales volumes for Pilchards resulted in lower revenues and operating profits for the division in the current year.

Squid

The acquisition of Talhado resulted in the increase in fishing rights and the number of fishing vessels utilised for squid from 4 vessels in the prior year to 22 vessels in the current year. The squid industry experienced exceptional catch rates in the current period. The landed volumes and sales volumes for the division were more than double those of the prior period. The market for South African squid remained stable despite the significant increase in landed volumes and the Euro sales prices achieved by the Group were the same as the prior period. The exceptional catch rates, increased sales volumes and consolidation of Talhado from 9 May resulted in an increase of 431% in operating profits of the division. Revenue of R80 million and profit after tax of R29 million has been consolidated from Talhado for the year ended 31 August 2018.

Hake

The 2018 TAC for hake is 133 119 tons. The quota which is available to the Group is 700 tons. The Group’s hake quota is caught, processed and marketed through a joint operation with Blue Continental Products (Pty) Ltd ("BCP") Hake. The catch rates for the division were similar to those of the prior period and the division also experienced a bigger size mix for its catches. There were unexpected major repairs and maintenance work done to the fishing vessel due to a breakdown which resulted in operating profits for this division being lower than the prior year.

Abalone

The Group commenced with construction of the expansion of the abalone farm. 40 tons of additional animal rearing capacity have been added to date and construction is anticipated to be completed by the end of Quarter 1 in 2019. The division is currently focused on increasing its spat ("Baby Abalone") production and stock holding in preparation for the farm is expansion. Sales volumes for the period were less than those of the prior period as the Group is growing out the animals to a bigger size for the market. Sales volumes are expected to increase once construction at the farm has been completed. The stock value increased by 25% from the prior year and this volume will be realised in the coming financial years. It is the Group’s intention to increase the stock value in line with the abalone expansion plans. Horse Mackerel The Group was awarded a horse mackerel quota of 800 tons during the FRAP2015/2016 process. The Group’s horse mackerel quota is caught, processed and marketed by Desert Diamond Fishing (Pty) Ltd. 100% of the quota was caught during the current period.

Seagro

Seagro is an organic fertiliser produced from Fish Oil which is a by-product of the Fishmeal making process. There was an increased availability of fish Oil in the current period which resulted in production of Seagro and increased sales volumes as compared to the prior period. The increased sales volumes in the current period resulted in increased profitability compared to the prior period.

Processing and marketing

The total WCRL contracted quota acquired for 2018 is 101 tons (2017: 96 tons). The total Wild Abalone contracted quota acquired for 2018 is 31 tons (2017: 30 tons). The quota holders landed their full quota allocations in the current financial year. Revenue and operating profits is lower than that of the prior year due to the strengthening of the Rand against the USD in the first half of the financial year.

So should you buy PFB shares?

Its a tough one to answer. They still a relatively new listing, but the results for the full year looks very strong, they trading at a moderate PE ratio, they have a very strong dividend yield, good cash generation and a lot of cash on their balance sheet. In addition to that the share price is close to their net asset value, which limits potential downside in the share price if buying at these levels

Our only worry is the fact that their profits are directly dependent on mother nature and the sea. And this can make their earnings pretty unpredictable and volatile in the long run. In addition to that the government can always withdraw or amend their fishing quotas. So the industry they operate in, while there is strong demand for fish can be a potentially very difficult one of government or mother nature is not in their favour.

Our only worry is the fact that their profits are directly dependent on mother nature and the sea. And this can make their earnings pretty unpredictable and volatile in the long run. In addition to that the government can always withdraw or amend their fishing quotas. So the industry they operate in, while there is strong demand for fish can be a potentially very difficult one of government or mother nature is not in their favour.