|

Pioneer Foods (PFG) interim results for the period ending March 2019

Date: 20 May 2019 Category: Stock Market Share price at time of writing: R78.45 We take a look at food producing group Pioneer Food's financial results for the interim period ending March 2019. Pioneer Foods has seen a significant decline in its share price in recent months from a share price that was trading around R140 a share at the beginning of 2018, its now almost half that price trading at R78.45 a share at the time of writing this review of their financial results

|

|

Related Topics |

About Pioneer Foods

Pioneer Foods is one of the largest South African producers and distributors of a range of branded food and beverage products. The Group operates mainly across South Africa, providing wholesale, retail and informal trade customers with products of a consistently high standard. Pioneer Foods exports to more than 60 countries across the globe. The growing international business represents 21% of operating profit.

The Group operates a number of world-class production facilities producing a range of products that includes some of the most recognisable and best loved brand names in South Africa, including the following power brands: Weet-Bix, Liqui-Fruit, Ceres, Sasko, Safari, Spekko and White Star.

The equity-accounted, joint venture investments based in South Africa, Nigeria, Botswana and Namibia do not form part of PFI’s segmental results, but are managed by the International division.

These include:

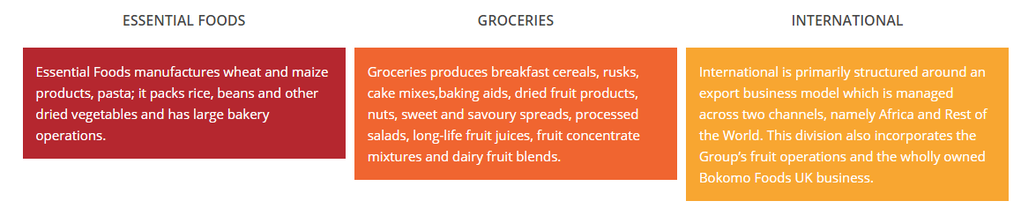

Pioneer Foods was established in 1997 and listed on the Johannesburg Stock Exchange (“JSE”) in 2008. It has three main divisions:

The Group operates a number of world-class production facilities producing a range of products that includes some of the most recognisable and best loved brand names in South Africa, including the following power brands: Weet-Bix, Liqui-Fruit, Ceres, Sasko, Safari, Spekko and White Star.

The equity-accounted, joint venture investments based in South Africa, Nigeria, Botswana and Namibia do not form part of PFI’s segmental results, but are managed by the International division.

These include:

- Alpen Food Company SA (50%)

- Bokomo Botswana (50%)

- Bokomo Namibia (50%)

- Bowman Ingredients South Africa (50%)

- Future Life Health Products (50%)

- Weetabix East Africa (49.89%)

Pioneer Foods was established in 1997 and listed on the Johannesburg Stock Exchange (“JSE”) in 2008. It has three main divisions:

Pioneer Foods Group main divisions

Financial results for period ending March 2019

The following was published on the JSE Security Exchange News Syteme (SENS) system earlier today

- Revenue (+12%) R11 039 million

- Adjusted operating profit (before items of a capital nature)* (-23%) R729 million

- Earnings (-18%) R509 million

- Earnings per share (-18%) 272 cents

- Diluted earnings per share (-14%) 272 cents

- Headline earnings ("HE") (-14%) R509 million

- Headline earnings per share (-14%) 272 cents

- Diluted headline earnings per share (-9%) 272 cents

- Adjusted headline earnings* (-15%) R506 million

- Adjusted headline earnings per share* (-15%) 271 cents

- Net cash profit from operating activities (-19%) R971 million

- Net asset value per share (+4%) 4 508 cents

- Interim gross dividend per listed ordinary share (2018: 105 cents) - 105 cents

- Dividend yield: 2.7%

- Cash and equivalents per share: R2.23 (or 2.8% of the company's share price)

- Cash generated from operations per share: R5.12 a share

- Tobin's Q: 0.995 (values over 1 shows the company's market capital is worth more than its total assets, while values less than 1 shows the company's total assets are worth more than the company's market capital). A potential indicator of value in a company if its Tobin's Q is below or close to 1.

So while revenue growth was pretty strong, earnings, earnings per share and diluted headline earnings per share all showed significant declines during the period. Currently the group trades at roughly 1.7 times its stated Net Asset Value (NAV). This is not uncommon as most operating entities tend to trade at levels around twice their NAV. Cash generation remains strong,

Management commentary on the financial results

Pioneer Foods posted revenue growth of 11.5% to R11.039 billion with volumes 2.7% higher for the six months ended 31 March 2019. Excluding the acquired Wellingtons and Lizi's businesses revenue grew by 7.9% with volumes up by 1.3%. This represents a credible topline performance in the significantly constrained local consumer market with consequent competitive pressures.

Revenue expansion was driven by sound volume growth in key product categories such as bread, wheat, rice, beverages (long life fruit juice), cereals in the UK and sausage rolls in Nigeria. Total basket inflation of 6.6% (ahead of overall SA CPI) was fueled by price inflation in the Essential Foods, International fruit and some smaller Groceries product categories.

Volume declines in maize and cereals constrained further revenue growth. Beverage exports into nearby African countries held its own despite the constrained trading environment with increased credit risk. The Group gained overall market share in South Africa across participating categories during the six months under review (Nielsen's Trade Desk).

FINANCIAL PERFORMANCE

Gross profit increased by 5% to R3.1 billion. The gross margin decreased from 29.6% to 27.9%, mainly as a result of insufficient price inflation to compensate for increased raw material costs and operating cost growth. Increased operating costs were driven by the considered investment in future growth capabilities (e.g. bread production and availability and distribution network expansion) as well as the higher cost of fuel, impacting distribution and energy related cost elements.

Total trade investment required (promotional activity and incentives) to maintain volume momentum and category participation, increased materially on the comparative period. This was caused mainly by intensified retailer competition and demands for promotional support.

Operating profit, before items of a capital nature, adjusted for the Phase I B-BBEE equity transaction ("BEE") share-based payment income/charge and related hedge ("SBP"), decreased by 23% to R729 million. In turn, the adjusted operating profit margin decreased from 9.6% to 6.6%. The Wellingtons business made a loss of R40 million before income tax (2018: R150 million on a 100% interest basis) for the 6 months.The operating profit margin would have been 7.2% if the Wellingtons business is excluded.

Profit for the period, after finance costs of R97.3 million (2018: R88.9 million) and the share of profit of joint ventures and associates of R38.7 million (2018: R21.6 million loss), decreased by 17.7% to R512.1 million. Earnings per share ("EPS") decreased by 18% to 272.3 cents and headline earnings per share ("HEPS") decreased by 14% to 272.4 cents per share. HEPS, adjusted for the BEE SBP net charge/gain, decreased by 15% to 270.9 cents per share. During the period, the strategic shareholder Phase II B-BBEE equity transaction matured and Pioneer Foods repurchased and cancelled 11 563 013 ordinary shares.

Essential Foods

The business, excluding maize, delivered an improved performance on the comparative period, but not enough to counter the material maize shortfall. The recovery in the wheaten value chain performance was led by strong bread volume growth following investments in manufacturing capacity during the past two years augmented by the route-to-market and availability growth strategy. Investment in operating cost to deliver the planned bread volume growth has accelerated, specifically in respect of distribution and manpower. The bread category experienced some price inflation during the reporting period following an extended deflationary cycle since the end of 2016. Sound rice volume and profitability expansion were achieved, with the pasta performance further constrained through competitively priced imports. Bread and rice posted market share gains for the reporting period in the Top End Retail market. The year-on-year regression in the performance of the maize category, off the strong comparative period base, was more than expected given sustained selling price deflation despite raw material cost inflation, and a weaker milling performance. The latter was impacted by weaker milling yields to sustain uncompromised White Star quality despite regression in maize quality and lower overall milling volumes. Although total White Star volumes sold were maintained compared to the comparative period, some share loss is reported given underlying category growth. White Star Instant maize porridge continues to outgrow a fast expanding product category with leading Top End Retail share reported during recent months.

Groceries

The major contributor to the decline in Groceries' profitability was the newly integrated Wellingtons business. Though overall negative profitability in the Wellingtons business is materially better than the comparative period, the performance of the business was impaired mainly by claims and costs associated with third party sales and distribution, which has now been addressed. The integration of the Wellingtons business is completed with key category participation improving through share gains in Top End Retail. The product and brand offerings together with accelerated innovation, portfolio maintenance, improved procurement and further operating performance enhancements, enabled through the Pioneer Foods integration, portends further improvement and upside. Within the rest of Groceries, the beverage business posted a good performance. Regression in cereals (negative product mix and pricing recovery lag) and some smaller categories contributed to the lower year-on-year profit in the business, excluding Wellingtons. Material growth in trade investment to hold volume shares and increased distribution costs contributed negatively, whilst the remainder of operating and conversion costs were well contained. Long life fruit juice delivered an excellent performance given sound volume growth supported by pack format and product innovation and posted share expansion in a growing category.

International

International delivered an improvement on the comparative period in the face of challenging trading conditions in neighbouring export markets and rand/dollar volatility. Higher export fruit pricing delivered solid revenue and profit growth. As a consequence, the 2019 vine fruit procurement prices experienced double-digit inflation which was further exacerbated by increased local competition. The UK subsidiary delivered an excellent performance driven by the core business, as well as the Lizi's product range that was acquired in the prior year. The Nigerian business performed well with the construction of the new bakery in Lagos progressing to plan.

OUTLOOK

The macro environment is expected to remain challenging and will continue to place pressure on consumer demand with resulting muted spending. Cost inflation in key raw materials and other operational input costs remains present although it is starting to level off. With pricing recovery still constrained by lower consumer demand and retailer competitive intensity, pressure on operating margins is expected to continue. The Group will continue efforts to optimise costs and efficiencies whilst ensuring its brands remain available and relevant to customers and consumers, thus strengthening the base for continued growth.

Revenue expansion was driven by sound volume growth in key product categories such as bread, wheat, rice, beverages (long life fruit juice), cereals in the UK and sausage rolls in Nigeria. Total basket inflation of 6.6% (ahead of overall SA CPI) was fueled by price inflation in the Essential Foods, International fruit and some smaller Groceries product categories.

Volume declines in maize and cereals constrained further revenue growth. Beverage exports into nearby African countries held its own despite the constrained trading environment with increased credit risk. The Group gained overall market share in South Africa across participating categories during the six months under review (Nielsen's Trade Desk).

FINANCIAL PERFORMANCE

Gross profit increased by 5% to R3.1 billion. The gross margin decreased from 29.6% to 27.9%, mainly as a result of insufficient price inflation to compensate for increased raw material costs and operating cost growth. Increased operating costs were driven by the considered investment in future growth capabilities (e.g. bread production and availability and distribution network expansion) as well as the higher cost of fuel, impacting distribution and energy related cost elements.

Total trade investment required (promotional activity and incentives) to maintain volume momentum and category participation, increased materially on the comparative period. This was caused mainly by intensified retailer competition and demands for promotional support.

Operating profit, before items of a capital nature, adjusted for the Phase I B-BBEE equity transaction ("BEE") share-based payment income/charge and related hedge ("SBP"), decreased by 23% to R729 million. In turn, the adjusted operating profit margin decreased from 9.6% to 6.6%. The Wellingtons business made a loss of R40 million before income tax (2018: R150 million on a 100% interest basis) for the 6 months.The operating profit margin would have been 7.2% if the Wellingtons business is excluded.

Profit for the period, after finance costs of R97.3 million (2018: R88.9 million) and the share of profit of joint ventures and associates of R38.7 million (2018: R21.6 million loss), decreased by 17.7% to R512.1 million. Earnings per share ("EPS") decreased by 18% to 272.3 cents and headline earnings per share ("HEPS") decreased by 14% to 272.4 cents per share. HEPS, adjusted for the BEE SBP net charge/gain, decreased by 15% to 270.9 cents per share. During the period, the strategic shareholder Phase II B-BBEE equity transaction matured and Pioneer Foods repurchased and cancelled 11 563 013 ordinary shares.

Essential Foods

The business, excluding maize, delivered an improved performance on the comparative period, but not enough to counter the material maize shortfall. The recovery in the wheaten value chain performance was led by strong bread volume growth following investments in manufacturing capacity during the past two years augmented by the route-to-market and availability growth strategy. Investment in operating cost to deliver the planned bread volume growth has accelerated, specifically in respect of distribution and manpower. The bread category experienced some price inflation during the reporting period following an extended deflationary cycle since the end of 2016. Sound rice volume and profitability expansion were achieved, with the pasta performance further constrained through competitively priced imports. Bread and rice posted market share gains for the reporting period in the Top End Retail market. The year-on-year regression in the performance of the maize category, off the strong comparative period base, was more than expected given sustained selling price deflation despite raw material cost inflation, and a weaker milling performance. The latter was impacted by weaker milling yields to sustain uncompromised White Star quality despite regression in maize quality and lower overall milling volumes. Although total White Star volumes sold were maintained compared to the comparative period, some share loss is reported given underlying category growth. White Star Instant maize porridge continues to outgrow a fast expanding product category with leading Top End Retail share reported during recent months.

Groceries

The major contributor to the decline in Groceries' profitability was the newly integrated Wellingtons business. Though overall negative profitability in the Wellingtons business is materially better than the comparative period, the performance of the business was impaired mainly by claims and costs associated with third party sales and distribution, which has now been addressed. The integration of the Wellingtons business is completed with key category participation improving through share gains in Top End Retail. The product and brand offerings together with accelerated innovation, portfolio maintenance, improved procurement and further operating performance enhancements, enabled through the Pioneer Foods integration, portends further improvement and upside. Within the rest of Groceries, the beverage business posted a good performance. Regression in cereals (negative product mix and pricing recovery lag) and some smaller categories contributed to the lower year-on-year profit in the business, excluding Wellingtons. Material growth in trade investment to hold volume shares and increased distribution costs contributed negatively, whilst the remainder of operating and conversion costs were well contained. Long life fruit juice delivered an excellent performance given sound volume growth supported by pack format and product innovation and posted share expansion in a growing category.

International

International delivered an improvement on the comparative period in the face of challenging trading conditions in neighbouring export markets and rand/dollar volatility. Higher export fruit pricing delivered solid revenue and profit growth. As a consequence, the 2019 vine fruit procurement prices experienced double-digit inflation which was further exacerbated by increased local competition. The UK subsidiary delivered an excellent performance driven by the core business, as well as the Lizi's product range that was acquired in the prior year. The Nigerian business performed well with the construction of the new bakery in Lagos progressing to plan.

OUTLOOK

The macro environment is expected to remain challenging and will continue to place pressure on consumer demand with resulting muted spending. Cost inflation in key raw materials and other operational input costs remains present although it is starting to level off. With pricing recovery still constrained by lower consumer demand and retailer competitive intensity, pressure on operating margins is expected to continue. The Group will continue efforts to optimise costs and efficiencies whilst ensuring its brands remain available and relevant to customers and consumers, thus strengthening the base for continued growth.

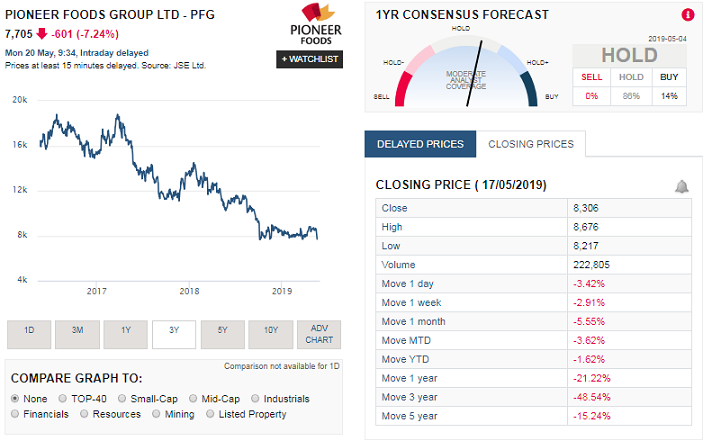

Pioneer Foods Group (PFG) share price performance

The screenshot below taken from Sharenet shows the constant decline in the share price of PFG, and based on the market reaction this morning it seems it is not happy with the financial results the group published today. Down by over 7% for the day.

Pioneer Foods Group (PFG) share price decline over the last 3 years

So based on the image above PFG's shares offered the following retuns over various time periods

- Today (20 May 2019): -7.24%

- 1 week: -2.91%

- 1 month: -5.55%

- Year to Date (YTD): -1.62%

- 1 year: -21.22%

- 3 years: -48.54%

- 5 years: -15.24%

Pioneer Foods Group (PFG) share valuation

So the question is should you buy shares in a company who has lost almost half its share price value since the start of the 2018? Does this represent a great buying opportunity or is there a reason why the market has been punishing the group's share price so hard? We asked the same question in November 2018. And the decline in reported profits and profits per share makes one wonder if Mr Market wasn't right in discounting the group's share price so hard? While there were once off costs associated with BEE transactions the group has stated that the environment they are operating in is difficult and they expect it to remain like this. They make mention of pressures on their operating margins and they expect that pressure to remain, as they struggle to offset increased costs onto consumers (who themselves are struggling).

Based on their current financial results, their prospects, their strong brands and strong balance sheet position, our valuation model places a value of R92.75 per share. We therefore believe at its current price PFG offers excellent long term value for those investors willing to buy and hold and reap the benefits later. Again we will reitirate, this is a long term buy and it might take a few years for margin pressures on the group to ease, in which case they should benefit handsomely, considering their footprint and portfolio of very strong food product brands.