|

Related Topics |

|

In our continued efforts to give our readers a broad number of views, opinions and information, we provide readers with Peregrine Treasury Services weekly market wrap below.

|

|

Peregrine Treasury Services Weekly Wrap as at 7 June 2019

A cold shadow was cast over financial markets this week, as the global environment braces for renewed anxiety linked to the ever-growing growth slump. With India cutting interest rates to their lowest levels in nine years and both the United States (US) and South Africa leaning toward reducing interest rates as soon as July, will other global central Banks follow suit? If so, is this the correct action that global governors should look at taking, in order to achieve some form of economic growth?

GLOBAL DATA AND POLITICS

South African data, once again, disappointed this week, with the most notable release being the highly anticipated gross domestic product (GDP) figure. The local economy contracted 3.20% quarter-on-quarter, massively undershooting expectations of a 1.70% contraction. The underperformance by the economy has largely been attributed to the global trade dynamic, as well as the rolling blackouts (electricity cuts) suffered by the country during the first quarter of the year. The most prominent attributors to the contraction was agriculture (declining by 13.20%), mining (declining by 10.80%) and manufacturing (shedding 8.80%). The effect of global trade tensions was mainly seen in the decline of exports (dropping by 26.40%), while a 4.80% decline in imports can be attributed to the strained local consumer and soft demand. Manufacturing purchasing managers index (PMI) continues to worsen, with the index dropping to 45.4, while total vehicle sales declined by 5.70% in May. The current account deficit constituted 2.90% of GDP during the first quarter (Q1) - up from the previous 2.20%.

Manufacturing PMI from China, released on Monday, remained largely flat at 50.2, marginally beating expectations, while the same index from Russia declined during May, decreasing to 49.8 from the previous 51.8. Both Russia and China also saw a decline in services PMI, coming in at 52.7 and 52.0 respectively.

Crossing over to the US, the Federal Reserve is likely to start decreasing rates by as early as July, as fears of a recession in 2020 looms. Manufacturing PMI declined marginally in May, dipping to 50.5, while total vehicle sales rose to 17.30 million. Factory orders lost some ground, contracting by 0.80% month-on-month in April, in line with expectations. Unit labour cost and non-farm productivity both declined quarter-on-quarter by 1.60% and 0.10% respectively. Initial jobless claims remained flat for the week at 218,000. Non-farm payrolls average hourly earnings and unemployment rates are due for release later today.

The European economy grew by 1.20% year-on-year for Q1 2019, in line with expectations, while their producer price index (PPI) contracted by 2.60% year-on-year in April. The Eurozone’s consumer price index (CPI) numbers saw a decrease year-on-year in May, decelerating to 1.20% from the previous 1.70%, while manufacturing PMI remained subdued at 47.7. The European consumer is seemingly not too keen on engaging in a shopping spree, with retail sales declining by 0.40% month-on-month in April. In the undertow, the European Central Bank (ECB) kept interest rates flat on Thursday afternoon, with the deposit rate remaining at -0.40%. Moving west, the United Kingdom’s (U.K.) manufacturing PMI came under pressure during May, with the index dropping from 53.1 in April to 49.5 in May. Services PMI marginally rose to 51.0, for the region.

US EQUITIES

An overall positive week for US equities this week, with the technology sector (NASDAQ) experiencing a small wobble after an announcement of an anti-trust probe rippled through the markets. In essence, what the probe is trying to address, is the fact that the likes of Facebook, Amazon, Apple, Alphabet (Google) and Netflix are creating an impossible barrier-to-entry within their respective silos, when looking at competition. A small 2.00% drop was seen on the NASDAQ, following this announcement, however the index managed to fight its way back to a net-positive space for the week by, Thursday evening.

Mark Zuckerberg, of Facebook, has recently come under extreme pressure from shareholders asking him to step down as Chairman of the social media company. This, in order to bring someone impartial/independent into the position who hasn’t been involved of the company’s DNA since inception. Ultimately the CEO and Chairman roles need to be separated.

Apple attended the 2019 Worldwide Developers Conference in San Jose, California, on Monday, where they unveiled both new products and upgrades to their operating systems. Some of the key and more interesting take-aways were:

Apple tend to have a way of breaking their products down into hundreds of smaller pieces and selling them to customers in different ‘parts to a puzzle’ for more money. One wonders when this will start damaging brand loyalty. All-in-all, investors seemed impressed with Apple’s presentation, which was a much needed counter-balance to the anti-trust probe being announced over the weekend.

FAANGs performance, for Thursday’s trading day:

In South African rand-terms, add 4.95% against each of these return-figures to see what the South African investor could be up in 2019, with the currency-effect added.

COMMODITIES

After falling over 6.00% since last Friday, oil prices have now moved into a holding pattern, where they will, with great interest, watch how the Persian Gulf region reacts to the hostility between the west and middle-east. With Trump deploying troops and military equipment, along with imposing sanctions on Iran, growing war-tensions start to mount. Could we see oil prices moving up toward the $90.00 a barrel region if war breaks out?

Brent Crude opened Friday’s trading day at $62.50 per barrel, while US West Texas Intermediate (WTI) opened at $53.25. Precious metals continue to press higher, with gold now coming into its own. Up over 2.00% for the week, one gets the feeling that safe-haven forms of investments are starting to make up larger allocations within the greater investor’s portfolio. Palladium remains in a cooling off phase, following its mighty run in early 2019, while platinum still trying to find any kind of traction at all in a world of manufacturers who find it illogical to switch back to platinum-centric products and machinery components vs a more recently favoured palladium. On Friday morning, gold, platinum and palladium were trading at levels of around $1,332.55, $804.40 and $1,350.73 per fine ounce respectively.

SOUTH AFRICAN POLITICS

Every ounce of ugly contained within the local political landscape was exposed this week as the SARB mandate once again made headlines. On Tuesday, ANC secretary-general Ace Magashule announced that the NEC had made a decision to expand the mandate of the SARB to include economic growth and employment, in addition to the current inflation targeting approach. He continued by stating that quantitative easing will be used to avail funds for development purposes. The statement left financial markets reeling, once again bringing the independence of the SARB into question. But the turmoil did not end there, with the ANC’s economic transformation head, Enoch Godongwana and Finance Minister Tito Mboweni both contradicting the controversial statement, as the spat between top leadership of the governing party became public.

At a time when the country is reeling from poor local economic performance, policy certainty and government stability become crucial fundamental elements to stimulate the economy and create desperately needed jobs. While many speculators have deemed Magashule’s utterances as an act of sabotage against the president’s efforts to restore investor and business confidence, the president himself remains eerily quiet on the matter. During its recent visit to South Africa, the IMF highlighted the risk of embattled SOEs on the economy, with specific focus on Eskom, while highlighting the importance of structural transformation to ensure stronger and more sustainable economic growth. This has been said before and nothing much had changed. Rinse and repeat.

With SA’s economic growth wiped out, and sub 1% now the reality for 2019, the nation will be turning its attention to the State of The Nation Address by President Ramaphosa, set to take place later this month. However, it seems that the greatest battles the president is facing are being fought inside his own party and, regardless of policy promises, resistance from within the ANC ranks can be taken as a certainty. If anything has become clear, it is just how unstable the ruling party remains and that the remnants of the Zuma era continue to tarnish the envisaged “new dawn” South Africans voted for on 8 May. This turmoil saw the rand immediately lose its footing against the dollar, quickly losing 3% against the greenback and topping levels of R14.90 by Thursday afternoon. By Friday morning it was testing the R15.00 level.

SOUTH AFRICAN EQUITY

Still trapped under the sombre veil of the recent elections and reshuffles within the greater parliament, the JSE Top 40 and All Share indices surprisingly clawed back just under 4.00% over the last five trading days. The catch however, was that the primary catalyst for this move was the weaker rand against the US dollar. With over 60.00% of the overall revenue’s generated by JSE listed companies being primarily denominated in US dollars, the weaker rand actually saw the larger dual listed-companies and miners push the indices higher. The drastic sell-off witnessed at the end of May has now started to present fairly attractive levels to re-enter the market again, albeit companies with US dollar exposure taking heavy preference.

Having said this, the banking sector, as well as retail sector, was seen remaining relatively flat for the week, while the resource sector had a very positive week. The industrial index rose more than 4.00%, off the back of robust moves from dual-listed stocks such as Naspers, Richemont, British American Tobacco and MTN.

A cautionary announcement was released by Spur Corporation on Monday evening pointing toward the possibility of Grand Parade Investments (GPI) continuing to sell down on their 17.50% ownership stake in Spur. This follows GPI’s disastrous venture into two dessert chain stores, namely Dunkin’ Donut’s and Baskin Robbins. The initial American fast-food brand-hype ultimately proved short-lived, due to poor local adoption by consumers. In addition, the arrival of both brands, on South African shores, saw relatively expensive franchise fees impacting GPI’s cash flow negatively.

The Burger King business, on the other hand, has proved to be a home run for GPI. It roughly owns the rights to 91.10% of the burger chain’s South African dealings. The rapid roll out of roughly 69 stores and the positive buy-in from the South African public has resulted in reasonable success for GPI. The high-speed growth of the business has increased its role as a competitor to Spur. Burger King’s expanding business is beginning to bring up questions of possible ‘conflicts of interest’, when comparing GPI’s investment position in both companies.

The negative impact of the confectionary businesses, coupled with the potential to expand Burger King even more, has given GPI the perfect opportunity to either trim or sell down entirely on its holdings in Spur, in order to create a source of strategic cash flow for the business - be it settling debts or focusing on other strategic investments. The likelihood of a full withdrawal isn’t high, but one could reasonably expect GPI to trim its ownership in Spur down to initial investment levels of around 10.00%. At that sort of level it would still provide Spur with the benefit of the BEE partnership with Grand Parade Investments. Spur opened up Friday’s trading day at R22.20 per share

Although bitter-sweet, Sibanye Gold saw their share price rising by more than 10.00% following news that their restructuring process would only see around 3,450 jobs being lost versus an initially expected 5,870. Due to various mining operations within the firm operating as loss making entities since 2017, a carefully designed restructuring plan was needed – one that would create as little impact as possible on employment numbers. Opening the week around levels of R13.37, Sibanye opened Friday’s trading day at Rxxx per share.

Here’s some of the bigger movers on the JSE for the 2019 year so far, as at Friday morning:

THE WEEK AHEAD

While all emerging markets remain under pressure, the rand is certainly bearing the biggest brunt, underlining that the weakness witnessed over the past 2-3 days has been mostly driven by local politics. With the rand frankly ignoring technical levels and purely focusing on the fundaments at play, it is safe to assume that the week ahead will be a hard one to anticipate as the market’s fate now lies at the feet of our politicians. The rand has a weakening bias, but further downside risks would come from:

On Friday morning the rand was trading at R15.06/$, R16.97/€ and R19.14/£. The next resistance level is at R15.10 and support is at R14.90

GLOBAL DATA AND POLITICS

South African data, once again, disappointed this week, with the most notable release being the highly anticipated gross domestic product (GDP) figure. The local economy contracted 3.20% quarter-on-quarter, massively undershooting expectations of a 1.70% contraction. The underperformance by the economy has largely been attributed to the global trade dynamic, as well as the rolling blackouts (electricity cuts) suffered by the country during the first quarter of the year. The most prominent attributors to the contraction was agriculture (declining by 13.20%), mining (declining by 10.80%) and manufacturing (shedding 8.80%). The effect of global trade tensions was mainly seen in the decline of exports (dropping by 26.40%), while a 4.80% decline in imports can be attributed to the strained local consumer and soft demand. Manufacturing purchasing managers index (PMI) continues to worsen, with the index dropping to 45.4, while total vehicle sales declined by 5.70% in May. The current account deficit constituted 2.90% of GDP during the first quarter (Q1) - up from the previous 2.20%.

Manufacturing PMI from China, released on Monday, remained largely flat at 50.2, marginally beating expectations, while the same index from Russia declined during May, decreasing to 49.8 from the previous 51.8. Both Russia and China also saw a decline in services PMI, coming in at 52.7 and 52.0 respectively.

Crossing over to the US, the Federal Reserve is likely to start decreasing rates by as early as July, as fears of a recession in 2020 looms. Manufacturing PMI declined marginally in May, dipping to 50.5, while total vehicle sales rose to 17.30 million. Factory orders lost some ground, contracting by 0.80% month-on-month in April, in line with expectations. Unit labour cost and non-farm productivity both declined quarter-on-quarter by 1.60% and 0.10% respectively. Initial jobless claims remained flat for the week at 218,000. Non-farm payrolls average hourly earnings and unemployment rates are due for release later today.

The European economy grew by 1.20% year-on-year for Q1 2019, in line with expectations, while their producer price index (PPI) contracted by 2.60% year-on-year in April. The Eurozone’s consumer price index (CPI) numbers saw a decrease year-on-year in May, decelerating to 1.20% from the previous 1.70%, while manufacturing PMI remained subdued at 47.7. The European consumer is seemingly not too keen on engaging in a shopping spree, with retail sales declining by 0.40% month-on-month in April. In the undertow, the European Central Bank (ECB) kept interest rates flat on Thursday afternoon, with the deposit rate remaining at -0.40%. Moving west, the United Kingdom’s (U.K.) manufacturing PMI came under pressure during May, with the index dropping from 53.1 in April to 49.5 in May. Services PMI marginally rose to 51.0, for the region.

US EQUITIES

An overall positive week for US equities this week, with the technology sector (NASDAQ) experiencing a small wobble after an announcement of an anti-trust probe rippled through the markets. In essence, what the probe is trying to address, is the fact that the likes of Facebook, Amazon, Apple, Alphabet (Google) and Netflix are creating an impossible barrier-to-entry within their respective silos, when looking at competition. A small 2.00% drop was seen on the NASDAQ, following this announcement, however the index managed to fight its way back to a net-positive space for the week by, Thursday evening.

Mark Zuckerberg, of Facebook, has recently come under extreme pressure from shareholders asking him to step down as Chairman of the social media company. This, in order to bring someone impartial/independent into the position who hasn’t been involved of the company’s DNA since inception. Ultimately the CEO and Chairman roles need to be separated.

Apple attended the 2019 Worldwide Developers Conference in San Jose, California, on Monday, where they unveiled both new products and upgrades to their operating systems. Some of the key and more interesting take-aways were:

- Itunes now being split into three stand-alone applications (Music, Podcasts and Video)

- The new iOS 13 operating system.

- The new Mac Pro computer, starting at $6,000.00 (R87,000.00)

- “The Pro Stand” A $1,000.00 computer stand.

Apple tend to have a way of breaking their products down into hundreds of smaller pieces and selling them to customers in different ‘parts to a puzzle’ for more money. One wonders when this will start damaging brand loyalty. All-in-all, investors seemed impressed with Apple’s presentation, which was a much needed counter-balance to the anti-trust probe being announced over the weekend.

FAANGs performance, for Thursday’s trading day:

- Facebook: down around 5.53%

- Amazon: down around 2.35%

- Apple: up around 3.89% (following new product release announcements)

- Netflix: up around 2.50%

- Alphabet: down around 5.56%

In South African rand-terms, add 4.95% against each of these return-figures to see what the South African investor could be up in 2019, with the currency-effect added.

COMMODITIES

After falling over 6.00% since last Friday, oil prices have now moved into a holding pattern, where they will, with great interest, watch how the Persian Gulf region reacts to the hostility between the west and middle-east. With Trump deploying troops and military equipment, along with imposing sanctions on Iran, growing war-tensions start to mount. Could we see oil prices moving up toward the $90.00 a barrel region if war breaks out?

Brent Crude opened Friday’s trading day at $62.50 per barrel, while US West Texas Intermediate (WTI) opened at $53.25. Precious metals continue to press higher, with gold now coming into its own. Up over 2.00% for the week, one gets the feeling that safe-haven forms of investments are starting to make up larger allocations within the greater investor’s portfolio. Palladium remains in a cooling off phase, following its mighty run in early 2019, while platinum still trying to find any kind of traction at all in a world of manufacturers who find it illogical to switch back to platinum-centric products and machinery components vs a more recently favoured palladium. On Friday morning, gold, platinum and palladium were trading at levels of around $1,332.55, $804.40 and $1,350.73 per fine ounce respectively.

SOUTH AFRICAN POLITICS

Every ounce of ugly contained within the local political landscape was exposed this week as the SARB mandate once again made headlines. On Tuesday, ANC secretary-general Ace Magashule announced that the NEC had made a decision to expand the mandate of the SARB to include economic growth and employment, in addition to the current inflation targeting approach. He continued by stating that quantitative easing will be used to avail funds for development purposes. The statement left financial markets reeling, once again bringing the independence of the SARB into question. But the turmoil did not end there, with the ANC’s economic transformation head, Enoch Godongwana and Finance Minister Tito Mboweni both contradicting the controversial statement, as the spat between top leadership of the governing party became public.

At a time when the country is reeling from poor local economic performance, policy certainty and government stability become crucial fundamental elements to stimulate the economy and create desperately needed jobs. While many speculators have deemed Magashule’s utterances as an act of sabotage against the president’s efforts to restore investor and business confidence, the president himself remains eerily quiet on the matter. During its recent visit to South Africa, the IMF highlighted the risk of embattled SOEs on the economy, with specific focus on Eskom, while highlighting the importance of structural transformation to ensure stronger and more sustainable economic growth. This has been said before and nothing much had changed. Rinse and repeat.

With SA’s economic growth wiped out, and sub 1% now the reality for 2019, the nation will be turning its attention to the State of The Nation Address by President Ramaphosa, set to take place later this month. However, it seems that the greatest battles the president is facing are being fought inside his own party and, regardless of policy promises, resistance from within the ANC ranks can be taken as a certainty. If anything has become clear, it is just how unstable the ruling party remains and that the remnants of the Zuma era continue to tarnish the envisaged “new dawn” South Africans voted for on 8 May. This turmoil saw the rand immediately lose its footing against the dollar, quickly losing 3% against the greenback and topping levels of R14.90 by Thursday afternoon. By Friday morning it was testing the R15.00 level.

SOUTH AFRICAN EQUITY

Still trapped under the sombre veil of the recent elections and reshuffles within the greater parliament, the JSE Top 40 and All Share indices surprisingly clawed back just under 4.00% over the last five trading days. The catch however, was that the primary catalyst for this move was the weaker rand against the US dollar. With over 60.00% of the overall revenue’s generated by JSE listed companies being primarily denominated in US dollars, the weaker rand actually saw the larger dual listed-companies and miners push the indices higher. The drastic sell-off witnessed at the end of May has now started to present fairly attractive levels to re-enter the market again, albeit companies with US dollar exposure taking heavy preference.

Having said this, the banking sector, as well as retail sector, was seen remaining relatively flat for the week, while the resource sector had a very positive week. The industrial index rose more than 4.00%, off the back of robust moves from dual-listed stocks such as Naspers, Richemont, British American Tobacco and MTN.

A cautionary announcement was released by Spur Corporation on Monday evening pointing toward the possibility of Grand Parade Investments (GPI) continuing to sell down on their 17.50% ownership stake in Spur. This follows GPI’s disastrous venture into two dessert chain stores, namely Dunkin’ Donut’s and Baskin Robbins. The initial American fast-food brand-hype ultimately proved short-lived, due to poor local adoption by consumers. In addition, the arrival of both brands, on South African shores, saw relatively expensive franchise fees impacting GPI’s cash flow negatively.

The Burger King business, on the other hand, has proved to be a home run for GPI. It roughly owns the rights to 91.10% of the burger chain’s South African dealings. The rapid roll out of roughly 69 stores and the positive buy-in from the South African public has resulted in reasonable success for GPI. The high-speed growth of the business has increased its role as a competitor to Spur. Burger King’s expanding business is beginning to bring up questions of possible ‘conflicts of interest’, when comparing GPI’s investment position in both companies.

The negative impact of the confectionary businesses, coupled with the potential to expand Burger King even more, has given GPI the perfect opportunity to either trim or sell down entirely on its holdings in Spur, in order to create a source of strategic cash flow for the business - be it settling debts or focusing on other strategic investments. The likelihood of a full withdrawal isn’t high, but one could reasonably expect GPI to trim its ownership in Spur down to initial investment levels of around 10.00%. At that sort of level it would still provide Spur with the benefit of the BEE partnership with Grand Parade Investments. Spur opened up Friday’s trading day at R22.20 per share

Although bitter-sweet, Sibanye Gold saw their share price rising by more than 10.00% following news that their restructuring process would only see around 3,450 jobs being lost versus an initially expected 5,870. Due to various mining operations within the firm operating as loss making entities since 2017, a carefully designed restructuring plan was needed – one that would create as little impact as possible on employment numbers. Opening the week around levels of R13.37, Sibanye opened Friday’s trading day at Rxxx per share.

Here’s some of the bigger movers on the JSE for the 2019 year so far, as at Friday morning:

- Impala Platinum: up 68.62%

- Kumba Iron Ore: up 55.13%

- Lonmin: up 75.33% (up over 15.00% in the last week)

- Tongaat Hulett: down 71.66%

- Rebosis Property Fund: down 68.03%

- Delta Property Fund: down 53.33%

THE WEEK AHEAD

While all emerging markets remain under pressure, the rand is certainly bearing the biggest brunt, underlining that the weakness witnessed over the past 2-3 days has been mostly driven by local politics. With the rand frankly ignoring technical levels and purely focusing on the fundaments at play, it is safe to assume that the week ahead will be a hard one to anticipate as the market’s fate now lies at the feet of our politicians. The rand has a weakening bias, but further downside risks would come from:

- A downgrade by Moody’s

- Increased global trade tension

- Anticipated decrease in interest rates by the SARB

- Continuous policy uncertainty from local government

- Expectations that the Fed will decrease interest rates

- President Ramaphosa addressing the SARB mandate issue head on and provide some clarity and certainty

- Decrease in global trade tensions

On Friday morning the rand was trading at R15.06/$, R16.97/€ and R19.14/£. The next resistance level is at R15.10 and support is at R14.90

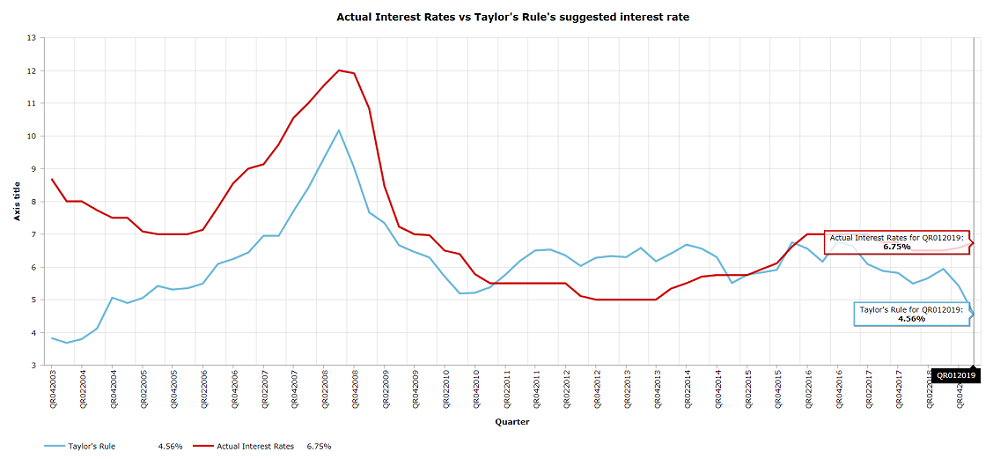

After the very poor GDP numbers released on Tuesday, we revisited our estimate of Taylor's rule which is a formula to estimate where a country's interest rates should be at. And with all the news swirling around the South African Reserve Bank and potential changes to their mandate to include employment and growth, we ask if the Reserve Bank is actually fulfilling its mandate or does it have a blind fixation on inflation targeting only? The results from Taylor's Rule is clear. Based on it South African interest rates are at least 200 basis points to high. See the image below for the latest estimate of Taylor's rule.

Read the full article here

Read the full article here

South Africa's interest rates vs Taylor's Rule suggested interest rate