|

Related Topics |

|

In our continued efforts to give our readers a broad number of views, opinions and information, we provide readers with Peregrine Treasury Services weekly market wrap below.

|

|

Peregrine Treasury Services Weekly Wrap as at 4 October 2019

Data doesn't lie

From contracting manufacturing numbers in the US, to slowing retail sales in Germany and a UK that’s experiencing its fifth consecutive month of slowing construction data, it’s safe to say that the world is finally accepting that the cloak of a slowing global economic climate is seemingly shrouding it. The last five trading days have really stripped away all the noise and shown investors the economic reality, without irrational tweets and too many trade threats being thrown into the mix.

Global economy showing signs of strain

Looking east, the rekindled Hong Kong riots seemed to take centre-stage across most major media headlines this week, while actual economic data releases for China were extremely thin. Caixin Manufacturing purchasing managers index (PMI) numbers came in stronger for September in China, indicating a small hint of life being breathed back into the manufacturing sector. Non-manufacturing PMI numbers came in slightly lower than expected for September, ultimately flat month-on-month.

German retail sales data came in weaker than expected (0.5% vs expected 0.9% for August month-on-month), indicating a slight pinch on citizens’ pockets, while a more fine-tuned awareness of their spending habits seems to be evident. UK construction numbers also came in lower for the fifth consecutive month. In addition, Markit UK Services PMI come in weaker for September at 49.5 vs an expected 50.5 – anything above 50 is expansionary and positive, while anything under 50 points towards a contracting economy.

A quick gander at UK politics and Boris Johnson is still fighting a losing Brexit battle, now aiming to replace the Irish backstop with an all-island regulatory zone. The European Union’s Donald Tusk has absolutely lambasted Johnson and his ideals around this. For the moment, there is not much else to see here… moving on.

Heading west, the US was slapped with a reality-check this week, with most of its economic data releases coming in worse than expected. The US is ultimately showing signs of an economy that’s ready to join a world that’s experiencing a relatively broad-based economic slowdown. Upsets of the week were as follows:

This week has been a relatively calm one on SA shores, with the only notable event coming from Minister of Finance, Tito Mboweni. A passionate Mboweni made a statement at the ANC NEC at the weekend and then partially retracted it. But let’s have a look at what he did say:

Mboweni’s very direct views and suggestions are some of those which the country really needs to consider and potentially adopt. He spoke with common sense and reasonable truth. He understands that South Africa is a battling, yet promising, country that can be reborn, however the political game seems to have silenced him. How long can this go on for? How long until the hard truth can be swallowed and the country’s dire situation be taken seriously? On the data front ABSA’s manufacturing PMI numbers for the country came in lower than expected at 41.6 vs an expected 43. Total vehicle sales came in stronger than expected versus the previous month with 49,190 vehicles being sold during the month.

Rand stronger ... for now

Much of the same is to be expected in the coming week, with more signs of a slowing economy being recognised through economic data releases. For now, patience is key as the greater market slowly reaches a point where conviction needs to be more understandable and directional. After being largely dictated by the US dollar’s rapid strengthening this week, the rand saw some relief on Thursday as the US released weaker-than-expected non-manufacturing data. After flying through two general trading ranges, the rand pulled back into the R15.09 to R15.25 range against the USD. Although the brief relief was well received by the local ZAR, the likelihood of this being long lived is questionable. Risk is currently to the downside (weakness) of the ZAR against major developed market currencies, especially the USD.

The rand started the day trading at R15.13/$, R16.59/€ and R18.67/£.

From contracting manufacturing numbers in the US, to slowing retail sales in Germany and a UK that’s experiencing its fifth consecutive month of slowing construction data, it’s safe to say that the world is finally accepting that the cloak of a slowing global economic climate is seemingly shrouding it. The last five trading days have really stripped away all the noise and shown investors the economic reality, without irrational tweets and too many trade threats being thrown into the mix.

Global economy showing signs of strain

Looking east, the rekindled Hong Kong riots seemed to take centre-stage across most major media headlines this week, while actual economic data releases for China were extremely thin. Caixin Manufacturing purchasing managers index (PMI) numbers came in stronger for September in China, indicating a small hint of life being breathed back into the manufacturing sector. Non-manufacturing PMI numbers came in slightly lower than expected for September, ultimately flat month-on-month.

German retail sales data came in weaker than expected (0.5% vs expected 0.9% for August month-on-month), indicating a slight pinch on citizens’ pockets, while a more fine-tuned awareness of their spending habits seems to be evident. UK construction numbers also came in lower for the fifth consecutive month. In addition, Markit UK Services PMI come in weaker for September at 49.5 vs an expected 50.5 – anything above 50 is expansionary and positive, while anything under 50 points towards a contracting economy.

A quick gander at UK politics and Boris Johnson is still fighting a losing Brexit battle, now aiming to replace the Irish backstop with an all-island regulatory zone. The European Union’s Donald Tusk has absolutely lambasted Johnson and his ideals around this. For the moment, there is not much else to see here… moving on.

Heading west, the US was slapped with a reality-check this week, with most of its economic data releases coming in worse than expected. The US is ultimately showing signs of an economy that’s ready to join a world that’s experiencing a relatively broad-based economic slowdown. Upsets of the week were as follows:

- ISM manufacturing PMI: 47.8 vs an expected 50.1

- ISM non-manufacturing PMI: 52.6 vs an expected 55.5

- Initial jobless claims of 219,000 vs last week’s 215,000

- 10% tariffs to be added onto Airbus planes manufactured in Europe

- 25% duties on single-malt whiskies from Scotland and Ireland

- 25% tariffs on coffee and certain machinery from Germany

- 25% tariffs on certain pork and dairy products from the UK, Spain and Germany.

This week has been a relatively calm one on SA shores, with the only notable event coming from Minister of Finance, Tito Mboweni. A passionate Mboweni made a statement at the ANC NEC at the weekend and then partially retracted it. But let’s have a look at what he did say:

- Weak economic growth, mainly borne from ongoing poor management of state-owned enterprises by the Government. Mr. Mboweni sees it fit to share the load with the public sector, which most investor’s probably agree on.

- Curbing collective bargaining. In essence, Mboweni would like to see exemptions being given to smaller enterprises versus larger ones in South Africa. Again, something the general citizen would tend to agree on.

- High-skilled immigration support.

- More support to private competitors to the likes of Eskom and Transnet.

- More focus on tourism within South Africa and the agricultural sector.

Mboweni’s very direct views and suggestions are some of those which the country really needs to consider and potentially adopt. He spoke with common sense and reasonable truth. He understands that South Africa is a battling, yet promising, country that can be reborn, however the political game seems to have silenced him. How long can this go on for? How long until the hard truth can be swallowed and the country’s dire situation be taken seriously? On the data front ABSA’s manufacturing PMI numbers for the country came in lower than expected at 41.6 vs an expected 43. Total vehicle sales came in stronger than expected versus the previous month with 49,190 vehicles being sold during the month.

Rand stronger ... for now

Much of the same is to be expected in the coming week, with more signs of a slowing economy being recognised through economic data releases. For now, patience is key as the greater market slowly reaches a point where conviction needs to be more understandable and directional. After being largely dictated by the US dollar’s rapid strengthening this week, the rand saw some relief on Thursday as the US released weaker-than-expected non-manufacturing data. After flying through two general trading ranges, the rand pulled back into the R15.09 to R15.25 range against the USD. Although the brief relief was well received by the local ZAR, the likelihood of this being long lived is questionable. Risk is currently to the downside (weakness) of the ZAR against major developed market currencies, especially the USD.

The rand started the day trading at R15.13/$, R16.59/€ and R18.67/£.

Advertisement (and yes South Africans can buy from Amazon as they deliver to SA)

Our highlight for the week:

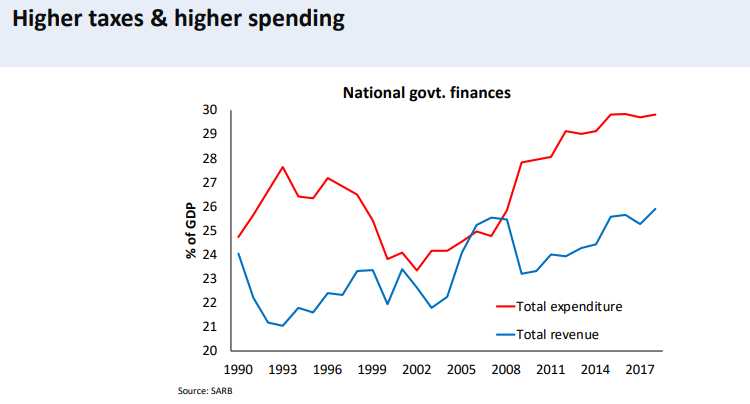

Our highlight of the week is the latest Monetary Policy Review article we did. The South African Reserve Bank published a number of very interesting graphics in this review. And one showed in just how much trouble the South African government's finances are.