|

Related Topics |

|

In our continued efforts to give our readers a broad number of views, opinions and information, we provide readers with Peregrine Treasury Services weekly market wrap below.

|

|

Peregrine Treasury Services Weekly Wrap as at 26 July 2019

With world economies sliding into a gentle holding pattern, as United States (US) quarter two (Q2) earnings season continues to unfold, it’s almost as if, for a brief moment, investors’ eyes have been turned away from the Persian Gulf and US-China trade war tensions. Further north, a new reign has begun under U.K. Prime Minister Boris Johnson, while his task at hand remains resoundingly challenging. Closer to home, South Africa’s future continues to remain unclear, as rifts within the African National Congress become more evident and failing state-owned enterprises somehow win favour over Finance Minister, Tito Mboweni.

GLOBAL DATA AND POLITICS

With the precarious ‘wait and see’ environment shrouding the greater global market, coupled with very little material global data moving the economic needle, in terms of currency markets, most eyes have been turned toward the health of the western equity markets, as (Q2) earnings roll out on US shores. The data has, however, provided the general investor with a comparative basis to make assumptions on global trends and activities across, not only, the hesitant emerging markets, but also the driving developed markets.

Starting off with the mighty United States, most investors still have their focus squarely sighted on the Federal Reserve (Fed) interest rate decision, coming up next week, and more importantly, the depth of the interest rate cut, coupled with the overall tone of the Reserve. This week saw existing home sales undershooting its target, reaching 5.27 million (expected 5.33 million) during June, while the manufacturing index also dropped to the 50 points mark in July from the previous 50.6 points - 50 points being the average of an expanding or contracting manufacturing environment. New home sales for June improved from the previous release, gaining 7% month-on-month. Thursday saw durable goods orders accelerate by 2%, largely outperforming the meager 0.8% that markets anticipated, while initial jobless claims, once again, reflected the resilience of the US employment market, coming in at 206,000 for the week. Today will see the release of the all-important US quarterly gross domestic product figures, with markets expecting growth of 1.9% quarter-on-quarter, for Q2.

The United Kingdom (U.K.) seems to be experiencing a moment of disbelief, as the next Prime Minister of the British Empire is none other than the very controversial Boris Johnson, officially voted in by the conservative party on Tuesday. On Wednesday evening, Theresa May officially stepped down as Prime Minister, while Johnson obtained official approval from the Queen to commence the assembly of a new government. The British pound largely ‘priced in’ the anticipated victory of Johnson in the days leading up to the results, while simultaneously losing significant ground against the US dollar. On Thursday however, the pound recovered some of this lost ground, as markets hoped to finally see the Brexit saga come to an end. Besides the changing of guard, it has been a slow week on the data front for the U.K.

Leading up to end of October, we will see the European Union (EU) and the U.K. battle out terms of an agreement, and more so, whether an agreement of any sort will be reached. The economy of the EU remains embattled, as the greater global growth slowdown continues to add pressure to some of the greatest EU economies. Consumer confidence for the union improved marginally during July, from -7.7 to -6.6, while Markit Composite purchasing managers index (PMI) declined to 51.5 points, undershooting market expectations. Manufacturing PMI also came under pressure in July, dropping to 46.4 from the previous 47.6 points. The European Central Bank (ECB) kept marginal lending facilities rates flat on Thursday, at 0.25%, while interest rates remained unchanged at 0%.The key benchmark rate also remained flat at -0.4%.The ECB remained dovish, with rates likely to remain at current or lower levels. The announcement by the ECB saw the euro hitting a two week low against the dollar as the ECB opened the doors to quantitative easing in the near-and-medium term.

It’s been a quiet week on the Chinese front, with only industrial profit year-to-date (YTD), and year-on-year, being released on Friday. The previous YTD figures, indicated a decline of 2.3%. Turkey caught markets off-guard on Thursday, when the new central bank governor oversaw the biggest interest rate cut since 2002, and the first interest rate cut since 2016 - a move that is aimed to please President Erdogan in his bid to lower borrowing costs in the country. The governor cut interest rates by 435 basis points, bringing interest in the region down to 19.75%

US EQUITIES

As US listed equities continue to make their way through Q2 earnings season, the S&P 500 has now seen around 20% of their listed companies having reported earnings, with over 77% of those having beaten analyst expectations. Thus far, the average growth in earnings of these companies has been in the region of around 3.5%. Fueling the rise in US markets this week, alongside the flurry of better-than-expected earnings announcements, congressional leaders in the US put forward a budget deal to the White House which could see the federal government’s debt ceiling raised in the near future. This would assist the government in avoiding future government shutdowns, seen in earlier in 2018 and 2019.

Q2 earnings highlights this week:

Expected earnings releases over the next few trading days: McDonalds, Starbucks, Amazon, Alphabet and Western Digital. At the rate US earnings are presenting themselves, the market seems fairly priced and possibly even ready for the next leg up, should major unreleased earnings continue with this positive trend.

Since Friday last week, US indices seem to have caught some positive momentum. Here’s are some of the movements over the last four trading days.

In South African rand-terms, subtract 1.78% against each of these return-figures to see what the South African investor could be up in 2019, with the currency-effect added.

COMMODITIES

Up around one percent this week, Brent Crude oil has traded in an extremely tight band of between $63.00 and $63.70 per barrel. Once again, it’s worth echoing how quiet the oil and iron ore market has been since US Q2 earnings season commenced. Looking at it now, even the US China trade war has been put on the back-burner. One gets a feeling that US President Trump has put a pause on the Iranian and Chinese tensions in order to give way for US earnings to play out, while the Fed’s dovish stance on interest rates is sure to add some small form of reaction to the global markets, once announced.

US inventory slipped by 10.8 million barrels this week vs analyst expectations of around a four million barrel drop. OPEC even had two of their allies cutting oil production by 500,000 barrels a day. Even with the news of oil inventories and production being managed lower, both the price of US WTI crude and Brent Crude remained tightly bound between their respective 0.50% to 1.10% ranges for the week. Brent Crude opened Friday’s trading day at $63.44 per barrel, while US West Texas Intermediate (WTI) opened at $56.17.

Both gold and platinum seem to be moving in tandem, with palladium finally starting to cool off. When looking at the longer term technical charts, platinum definitely mock-charged the longer-term downward trend this week, in order to test its resistance and strength. Once could possibly start seeing platinum coming into its own again, after being downtrodden for the last ten years. Watch this space. On Friday morning, gold, platinum and palladium were trading at levels of around $1,416.00, $867.12 and $1,529.86 per fine ounce respectively.

SOUTH AFRICAN FUNDAMENTALS

Besides the normal political bickering one has become accustomed to, and the ongoing shock-worthy details being released at the Zondo Commission, it has been quite an eventful week on the South African (SA) front. SA’s public protector has, once again, come under fire, with the Constitutional court finding that Busisiwe Mkhwebane perjured herself, acted with malice and in bad faith (with regard to the ongoing South African Reserve Bank/ABSA saga), while Pravin Gordhan has sought out an interdict against her recommended remedial action, with regard to the South African Revenue Services rogue unit. The recent revelations at the Zondo commission, regarding the Estina dairy farm transactions, has also done little to revive any confidence in Mkhwebane, while the nation now waits to see what action, if any, will be taken against her.

The new approved appropriation bill, tabled in parliament by Finance Minister, Tito Mboweni, also made headlines. The bill will see the allocation of an additional R59 billion to the embattled state-owned enterprise (SOE), Eskom, over the next two years. While the move was made in an effort to ensure Eskom continues to meet its financial obligations, the exact conditions of the appropriation remains murky. While South African citizens are all painfully aware that government is ‘stuck between a rock and a hard place’, when it comes to Eskom, one cannot help but wonder when the much needed structural reform is going to take place and how long one will need to wait before they are presented with a confident restructuring plan for Eskom. The appropriation bill, not only being how the state funds are applied, but also how the SOE will be restructured in an effort to cut down on cost and ensure sustainable electricity supply.

Previously, Moody’s has warned SA that any deterioration in Eskom, and the fiscal position of the country, could weigh heavily on the company and county’s credit rating moving forward, once again reiterating their stance on Thursday, noting that the additional funding allocated to Eskom is seen as credit-negative by the agency. The rand however, did little in response to this statement, with a downgrade largely being ‘priced in’ over the past couple of months.

The rand traded within a tight range this week, with the next catalyst events that could give direction to the currency, in all likelihood, being the impending interest rate cut by the Fed, following the interest rate announcement by the ECB, due to take place next week. While the rand continues on a stable footing, even after the depreciation of over 1.6% on Thursday, against major currencies in the short term, our projections for the longer term indicates a move toward the R15.00 mark, against the US dollar.

Local consumer price index and producer price index released, during this week, remained largely in-line with market expectations, at 4.5% and 5.8% YoY, during June.

SOUTH AFRICAN EQUITY

Closer to home, local equity markets have largely been directed by the indecisive rand, which has been seen trying to navigate the turbulent oceans shrouded with treacherous siren songs in the form of the public protector saga, the voting-in of Boris Johnson - as U.K.’s next Prime Minister, the surprisingly strong US earnings season and the dragging effect created by the US China trade war, which has seemingly turned stale, in terms of progression or any form of conclusive agreement. With the above challenges veiling the last week, both the All Share index and Top 40 were seen moving fractionally higher, to the tune of around 0.35% respectively, for the last five trading days.

Last Friday, AB Inbev (ANH) agreed to sell their Australian operations, Carlton & United Breweries, to Japan’s Asahi for $11.3 billion. The disposal of ANH’s Australian operations will definitely assist the company in chipping away at its debt pile, albeit at a slower rate than a successful IPO would have achieved. The fact that ANH’s debt burden is now topping the $100 billion mark, coupled with the recent cancellation of its Asian IPO, means that the sale of its Australian business is definitely a step in the right direction. Although one might think that the entire proceeds from the sale would be directed towards alleviating the company’s debt burden, there is a greater possibility of the proceeds being split between repaying its debt and targeting strategic buyouts and expansions within emerging markets, namely the buoyant Asia-Pacific region.

On Tuesday, Kumba Iron Ore (KIO) was seen reporting some extremely good, yet murky sim-month results, which saw the stock actually take a tumble on the day by around 2.93%. Once could say that investor expectations were potentially too high going into earnings. What one saw on the day, was simply the effect of an over-reaction cooling off. Some of their numbers were as follows:

Mondi Ltd (MND) have announced that they will be delisting their local version of the stock, while flipping its primary listing over to their London’s Mondi PLC (MNP) listing. Shareholders holding MND previously will now have their shares converted into the secondary listed MNP on the JSE. On MND’s final day of trading, around R6.7 billion in JSE daily volume was pushed through the stock alone.

If any investor held MND, and is uncertain about the way forward, here’s the conversion timelines advised by the company:

THE WEEK AHEAD

We will be keeping a close eye on the gross domestic price data due from the US, later today, in order to guide us on the expected tone of the Fed next week. The interest cut due to take place has already been ‘priced in’ - the key, however, will be depth of the cut, coupled by the tone of the Fed, especially in light of a seemingly resilient US economy. The week ahead has a relatively material data week in store for the local economy, with key data releases including the unemployment rate (previously peaking at 27.6%), trade balance, manufacturing PMI and vehicle sales, potentially providing direction to the confusing market-moves one has been seeing of late. A cut by the Fed, in excess of 25 basis points, could see the rand gain some momentum once again, potentially retesting the R13.80 mark, and open a new-stronger trading range within the short term, while slowing global growth is due to claim its pound-of-flesh from emerging markets in the longer run. On Friday morning the rand would’ve set the investor back R14.09 per US dollar, R15.72 a euro and R17.54 a British pound.

GLOBAL DATA AND POLITICS

With the precarious ‘wait and see’ environment shrouding the greater global market, coupled with very little material global data moving the economic needle, in terms of currency markets, most eyes have been turned toward the health of the western equity markets, as (Q2) earnings roll out on US shores. The data has, however, provided the general investor with a comparative basis to make assumptions on global trends and activities across, not only, the hesitant emerging markets, but also the driving developed markets.

Starting off with the mighty United States, most investors still have their focus squarely sighted on the Federal Reserve (Fed) interest rate decision, coming up next week, and more importantly, the depth of the interest rate cut, coupled with the overall tone of the Reserve. This week saw existing home sales undershooting its target, reaching 5.27 million (expected 5.33 million) during June, while the manufacturing index also dropped to the 50 points mark in July from the previous 50.6 points - 50 points being the average of an expanding or contracting manufacturing environment. New home sales for June improved from the previous release, gaining 7% month-on-month. Thursday saw durable goods orders accelerate by 2%, largely outperforming the meager 0.8% that markets anticipated, while initial jobless claims, once again, reflected the resilience of the US employment market, coming in at 206,000 for the week. Today will see the release of the all-important US quarterly gross domestic product figures, with markets expecting growth of 1.9% quarter-on-quarter, for Q2.

The United Kingdom (U.K.) seems to be experiencing a moment of disbelief, as the next Prime Minister of the British Empire is none other than the very controversial Boris Johnson, officially voted in by the conservative party on Tuesday. On Wednesday evening, Theresa May officially stepped down as Prime Minister, while Johnson obtained official approval from the Queen to commence the assembly of a new government. The British pound largely ‘priced in’ the anticipated victory of Johnson in the days leading up to the results, while simultaneously losing significant ground against the US dollar. On Thursday however, the pound recovered some of this lost ground, as markets hoped to finally see the Brexit saga come to an end. Besides the changing of guard, it has been a slow week on the data front for the U.K.

Leading up to end of October, we will see the European Union (EU) and the U.K. battle out terms of an agreement, and more so, whether an agreement of any sort will be reached. The economy of the EU remains embattled, as the greater global growth slowdown continues to add pressure to some of the greatest EU economies. Consumer confidence for the union improved marginally during July, from -7.7 to -6.6, while Markit Composite purchasing managers index (PMI) declined to 51.5 points, undershooting market expectations. Manufacturing PMI also came under pressure in July, dropping to 46.4 from the previous 47.6 points. The European Central Bank (ECB) kept marginal lending facilities rates flat on Thursday, at 0.25%, while interest rates remained unchanged at 0%.The key benchmark rate also remained flat at -0.4%.The ECB remained dovish, with rates likely to remain at current or lower levels. The announcement by the ECB saw the euro hitting a two week low against the dollar as the ECB opened the doors to quantitative easing in the near-and-medium term.

It’s been a quiet week on the Chinese front, with only industrial profit year-to-date (YTD), and year-on-year, being released on Friday. The previous YTD figures, indicated a decline of 2.3%. Turkey caught markets off-guard on Thursday, when the new central bank governor oversaw the biggest interest rate cut since 2002, and the first interest rate cut since 2016 - a move that is aimed to please President Erdogan in his bid to lower borrowing costs in the country. The governor cut interest rates by 435 basis points, bringing interest in the region down to 19.75%

US EQUITIES

As US listed equities continue to make their way through Q2 earnings season, the S&P 500 has now seen around 20% of their listed companies having reported earnings, with over 77% of those having beaten analyst expectations. Thus far, the average growth in earnings of these companies has been in the region of around 3.5%. Fueling the rise in US markets this week, alongside the flurry of better-than-expected earnings announcements, congressional leaders in the US put forward a budget deal to the White House which could see the federal government’s debt ceiling raised in the near future. This would assist the government in avoiding future government shutdowns, seen in earlier in 2018 and 2019.

Q2 earnings highlights this week:

- Coca-Cola: adjusted earnings per share (EPS) 63 cents vs expected 61 cents - marginal beat

- Texas Instruments: EPS $1.36 per share vs an expected $1.22 per share - beat

- AT&T: sales up 15% to $45 billion against expected $44.9 billion. Net income to $3.7 billion - beat

- United Technologies: net sales up 17.5% to $19.63 billion vs an expected $19.55 billion. Top-end of earnings guidance for 2019’s full year was adjusted upward by 5 cents a share to $8.05 from $8.00 - beat

- Hasbro: revenue up 9% to $984.5 million vs an expected $956.7 million. Adjusted EPS came in at 78 cents per share vs an expected 50 cents - beat

- VISA: adjusted EPS came in at $1.37 vs an expected $1.33 per share. Revenue up for the quarter year-on-year at $5.8 billion vs $5.2 billion last year - beat

- Chipotle: Revenue beat slightly at $1.43 billion vs an expected $1.41 billion. Adjusted EPS also came in higher than expected at $3.99 per share vs $3.76 – growth in online sales being a main attributor - beat

- SNAP (Snapchat): revenue of $388 million vs an expected $359.7 million. Expected losses also came in lower than expected - beat

- Boeing: $2.9 billion loss for Q2. Largest loss ever reported for the firm. Mainly on the back of the recent faulty 737 MAX airplane issues – material miss

- Caterpillar: Earnings coming in at $2.83 per share vs an expected $3.12 per share. The underwhelming earnings mainly attributed to the US China trade war. Future earnings guidance was also lowered for the construction equipment manufacturer - miss

Expected earnings releases over the next few trading days: McDonalds, Starbucks, Amazon, Alphabet and Western Digital. At the rate US earnings are presenting themselves, the market seems fairly priced and possibly even ready for the next leg up, should major unreleased earnings continue with this positive trend.

Since Friday last week, US indices seem to have caught some positive momentum. Here’s are some of the movements over the last four trading days.

- S&P 500: down 0.36%

- NASDAQ: up 0.50%

- Dow Jones: down -0.11%

- Facebook: up around 0.14%

- Amazon: down around 0.09%

- Apple: up around 0.99%

- Netflix: up around 1.20%

- Alphabet: down around -0.82%

In South African rand-terms, subtract 1.78% against each of these return-figures to see what the South African investor could be up in 2019, with the currency-effect added.

COMMODITIES

Up around one percent this week, Brent Crude oil has traded in an extremely tight band of between $63.00 and $63.70 per barrel. Once again, it’s worth echoing how quiet the oil and iron ore market has been since US Q2 earnings season commenced. Looking at it now, even the US China trade war has been put on the back-burner. One gets a feeling that US President Trump has put a pause on the Iranian and Chinese tensions in order to give way for US earnings to play out, while the Fed’s dovish stance on interest rates is sure to add some small form of reaction to the global markets, once announced.

US inventory slipped by 10.8 million barrels this week vs analyst expectations of around a four million barrel drop. OPEC even had two of their allies cutting oil production by 500,000 barrels a day. Even with the news of oil inventories and production being managed lower, both the price of US WTI crude and Brent Crude remained tightly bound between their respective 0.50% to 1.10% ranges for the week. Brent Crude opened Friday’s trading day at $63.44 per barrel, while US West Texas Intermediate (WTI) opened at $56.17.

Both gold and platinum seem to be moving in tandem, with palladium finally starting to cool off. When looking at the longer term technical charts, platinum definitely mock-charged the longer-term downward trend this week, in order to test its resistance and strength. Once could possibly start seeing platinum coming into its own again, after being downtrodden for the last ten years. Watch this space. On Friday morning, gold, platinum and palladium were trading at levels of around $1,416.00, $867.12 and $1,529.86 per fine ounce respectively.

SOUTH AFRICAN FUNDAMENTALS

Besides the normal political bickering one has become accustomed to, and the ongoing shock-worthy details being released at the Zondo Commission, it has been quite an eventful week on the South African (SA) front. SA’s public protector has, once again, come under fire, with the Constitutional court finding that Busisiwe Mkhwebane perjured herself, acted with malice and in bad faith (with regard to the ongoing South African Reserve Bank/ABSA saga), while Pravin Gordhan has sought out an interdict against her recommended remedial action, with regard to the South African Revenue Services rogue unit. The recent revelations at the Zondo commission, regarding the Estina dairy farm transactions, has also done little to revive any confidence in Mkhwebane, while the nation now waits to see what action, if any, will be taken against her.

The new approved appropriation bill, tabled in parliament by Finance Minister, Tito Mboweni, also made headlines. The bill will see the allocation of an additional R59 billion to the embattled state-owned enterprise (SOE), Eskom, over the next two years. While the move was made in an effort to ensure Eskom continues to meet its financial obligations, the exact conditions of the appropriation remains murky. While South African citizens are all painfully aware that government is ‘stuck between a rock and a hard place’, when it comes to Eskom, one cannot help but wonder when the much needed structural reform is going to take place and how long one will need to wait before they are presented with a confident restructuring plan for Eskom. The appropriation bill, not only being how the state funds are applied, but also how the SOE will be restructured in an effort to cut down on cost and ensure sustainable electricity supply.

Previously, Moody’s has warned SA that any deterioration in Eskom, and the fiscal position of the country, could weigh heavily on the company and county’s credit rating moving forward, once again reiterating their stance on Thursday, noting that the additional funding allocated to Eskom is seen as credit-negative by the agency. The rand however, did little in response to this statement, with a downgrade largely being ‘priced in’ over the past couple of months.

The rand traded within a tight range this week, with the next catalyst events that could give direction to the currency, in all likelihood, being the impending interest rate cut by the Fed, following the interest rate announcement by the ECB, due to take place next week. While the rand continues on a stable footing, even after the depreciation of over 1.6% on Thursday, against major currencies in the short term, our projections for the longer term indicates a move toward the R15.00 mark, against the US dollar.

Local consumer price index and producer price index released, during this week, remained largely in-line with market expectations, at 4.5% and 5.8% YoY, during June.

SOUTH AFRICAN EQUITY

Closer to home, local equity markets have largely been directed by the indecisive rand, which has been seen trying to navigate the turbulent oceans shrouded with treacherous siren songs in the form of the public protector saga, the voting-in of Boris Johnson - as U.K.’s next Prime Minister, the surprisingly strong US earnings season and the dragging effect created by the US China trade war, which has seemingly turned stale, in terms of progression or any form of conclusive agreement. With the above challenges veiling the last week, both the All Share index and Top 40 were seen moving fractionally higher, to the tune of around 0.35% respectively, for the last five trading days.

Last Friday, AB Inbev (ANH) agreed to sell their Australian operations, Carlton & United Breweries, to Japan’s Asahi for $11.3 billion. The disposal of ANH’s Australian operations will definitely assist the company in chipping away at its debt pile, albeit at a slower rate than a successful IPO would have achieved. The fact that ANH’s debt burden is now topping the $100 billion mark, coupled with the recent cancellation of its Asian IPO, means that the sale of its Australian business is definitely a step in the right direction. Although one might think that the entire proceeds from the sale would be directed towards alleviating the company’s debt burden, there is a greater possibility of the proceeds being split between repaying its debt and targeting strategic buyouts and expansions within emerging markets, namely the buoyant Asia-Pacific region.

On Tuesday, Kumba Iron Ore (KIO) was seen reporting some extremely good, yet murky sim-month results, which saw the stock actually take a tumble on the day by around 2.93%. Once could say that investor expectations were potentially too high going into earnings. What one saw on the day, was simply the effect of an over-reaction cooling off. Some of their numbers were as follows:

- EBITDA margin up to 58%

- Headline EPS was up 239% vs an expected 160% increase (due to iron ore’s 57% run in 2019)

- Interim dividend of R30.79 per share

- Revenue numbers up 77% for the period

Mondi Ltd (MND) have announced that they will be delisting their local version of the stock, while flipping its primary listing over to their London’s Mondi PLC (MNP) listing. Shareholders holding MND previously will now have their shares converted into the secondary listed MNP on the JSE. On MND’s final day of trading, around R6.7 billion in JSE daily volume was pushed through the stock alone.

If any investor held MND, and is uncertain about the way forward, here’s the conversion timelines advised by the company:

- Last day to trade in MND: Tuesday, 23 July

- Listing of MND suspended from: Wednesday, 24 July

- Response deadline for elections: Wednesday, 24 July

- Scheme record date: Friday, 26 July

- Scheme pay date: Monday, 29 July

- Listing of MND terminated on: Monday, 29 July

- Impala Platinum: up 102.07%

- Kumba Iron Ore: up 68.78%

- Sibanye Gold: up 85.03%

- Rebosis Property Fund: down 78.07%

- Omnia: down 59.61%

- Brait: down 48.30%

THE WEEK AHEAD

We will be keeping a close eye on the gross domestic price data due from the US, later today, in order to guide us on the expected tone of the Fed next week. The interest cut due to take place has already been ‘priced in’ - the key, however, will be depth of the cut, coupled by the tone of the Fed, especially in light of a seemingly resilient US economy. The week ahead has a relatively material data week in store for the local economy, with key data releases including the unemployment rate (previously peaking at 27.6%), trade balance, manufacturing PMI and vehicle sales, potentially providing direction to the confusing market-moves one has been seeing of late. A cut by the Fed, in excess of 25 basis points, could see the rand gain some momentum once again, potentially retesting the R13.80 mark, and open a new-stronger trading range within the short term, while slowing global growth is due to claim its pound-of-flesh from emerging markets in the longer run. On Friday morning the rand would’ve set the investor back R14.09 per US dollar, R15.72 a euro and R17.54 a British pound.

Our highlight for the week:

Growing seaborne trade

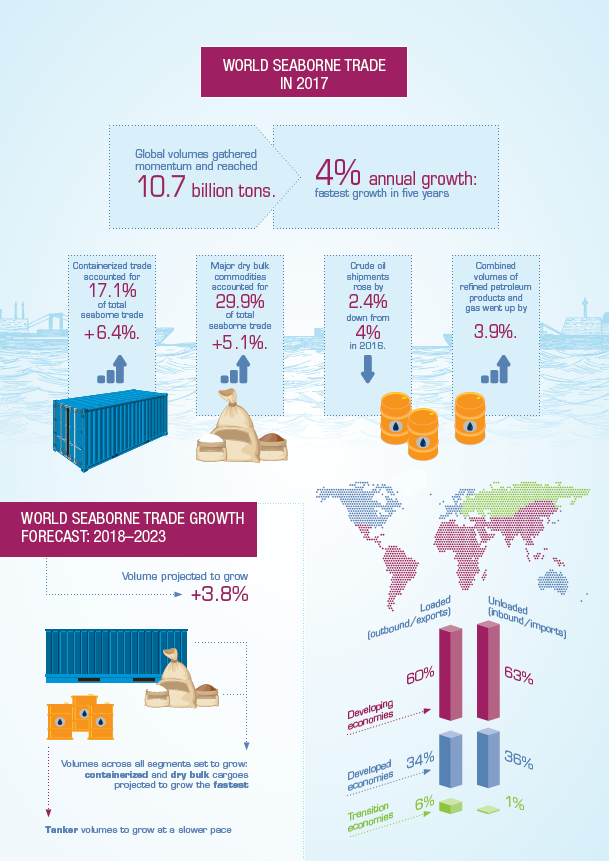

Global seaborne trade is doing well, supported by the 2017 upswing in the world economy. Expanding at 4 percent, the fastest growth in five years, global maritime trade gathered momentum and raised sentiment in the shipping industry. Total volumes reached 10.7 billion tons, reflecting an additional 411 million tons, nearly half of which were made of dry bulk commodities. Global containerized trade increased by 6.4 per cent, following the historical lows of the two previous years. Dry bulk cargo increased by 4.0 per cent, up from 1.7 per cent in 2016, while growth in crude oil shipments decelerated to 2.4 per cent. Reduced shipments from exporters of the Organization of Petroleum Exporting Countries were offset by increased trade flows originating from the Atlantic basin and moving eastward towards Asia. This new trend has reshaped crude oil trade patterns, which became less concentrated on usual suppliers from Western Asia. Supported by the growing global refining capacity – especially in Asia – and the appeal of gas as a cleaner energy source, refined petroleum products and gas increased by a combined 3.9 per cent in 2017. Prospects for seaborne trade are positive; UNCTAD projects volume increases of 4 per cent in 2018, a rate equivalent to that of 2017. Contingent on continued favourable trends in the global economy, UNCTAD is forecasting a 3.8 per cent compound annual growth rate between 2018 and 2023. Volumes across all segments are set to grow, with containerized and dry bulk commodities expected to record the fastest growth at the expense of tanker volumes. UNCTAD projections for overall seaborne trade are consistent with historical trends, whereby seaborne trade increased at an annual average rate of 3.5 per cent between 2005 and 2017. Projections of rapid growth in dry cargo are in line with a five-decade-long pattern that saw the share of tanker volumes being displaced by dry cargoes, dropping from over 50 per cent in 1970 to less than 33 per cent in 2017

Global seaborne trade is doing well, supported by the 2017 upswing in the world economy. Expanding at 4 percent, the fastest growth in five years, global maritime trade gathered momentum and raised sentiment in the shipping industry. Total volumes reached 10.7 billion tons, reflecting an additional 411 million tons, nearly half of which were made of dry bulk commodities. Global containerized trade increased by 6.4 per cent, following the historical lows of the two previous years. Dry bulk cargo increased by 4.0 per cent, up from 1.7 per cent in 2016, while growth in crude oil shipments decelerated to 2.4 per cent. Reduced shipments from exporters of the Organization of Petroleum Exporting Countries were offset by increased trade flows originating from the Atlantic basin and moving eastward towards Asia. This new trend has reshaped crude oil trade patterns, which became less concentrated on usual suppliers from Western Asia. Supported by the growing global refining capacity – especially in Asia – and the appeal of gas as a cleaner energy source, refined petroleum products and gas increased by a combined 3.9 per cent in 2017. Prospects for seaborne trade are positive; UNCTAD projects volume increases of 4 per cent in 2018, a rate equivalent to that of 2017. Contingent on continued favourable trends in the global economy, UNCTAD is forecasting a 3.8 per cent compound annual growth rate between 2018 and 2023. Volumes across all segments are set to grow, with containerized and dry bulk commodities expected to record the fastest growth at the expense of tanker volumes. UNCTAD projections for overall seaborne trade are consistent with historical trends, whereby seaborne trade increased at an annual average rate of 3.5 per cent between 2005 and 2017. Projections of rapid growth in dry cargo are in line with a five-decade-long pattern that saw the share of tanker volumes being displaced by dry cargoes, dropping from over 50 per cent in 1970 to less than 33 per cent in 2017

As the treemap of South Africa's imports from the USA below shows, the main product categories imported by South Africa from the USA is not the primary type goods or commodities (like we export to them) but goods that entailed a lot more manufacturing and processing). The main product category imported by South Africa from the United States is Machinery, with it making up more than a quarter of South Africa''s imports from the USA. The second biggest import category being vehicles, aircrafts and vehicles with it making up 17% of the total imports by South Africa from the USA. Mostly American built vehicles being imported into South Africa