|

Related Topics |

|

In our continued efforts to give our readers a broad number of views, opinions and information, we provide readers with Peregrine Treasury Services weekly market wrap below.

|

|

Peregrine Treasury Services Weekly Wrap as at 19 July 2019

As the United States earnings season swings into full bloom, for the second quarter (Q2) of 2019, it’s interesting to note how eerily quiet both the US-China trade war talks and tussle between the US and Iran, in the Middle East, have become. While South African equity markets crept higher this week, due to a stronger rand (weaker US dollar), the Dow Jones, NASDAQ and S&P 500 all slipped into a holding pattern, as all eyes now turn toward Jerome Powell and Federal Reserve’s impending outlook on the health of the US economy.

GLOBAL DATA AND POLITICS

Following a rather quiet few weeks, President Donald Trump once again moved to reignite the trade war. While the long-standing trade tiff between the US and China rages on, President Trump is setting his sights on other regions of the globe, including France and Japan. Earlier this week, Chinese gross domestic product (GDP) numbers gave investors a glimpse of the global slowdown, as the economic powerhouse posted growth of 6.2% year-on-year for Q2. This, the lowest level of growth, for China, recorded since 1992, while retail sales accelerated by 9.8% year-on-year in June, outperforming the market forecast of 8.5%

Locally, South Africa witnessed retail sales outperform expectations, gaining 2.2% year-on-year. When taking the retail sales numbers into consideration, in combination with various other improving economic indicators, Q2 GDP is sure to improve, following a dismal Q1.

The United Kingdom’s (U.K.) average earnings increased marginally to 3.4%, while the unemployment rate remained unchanged at 3.8%. Inflation remained steady at two percent, year-on-year, in June. The Brexit dynamic continues to weigh heavily on the U.K., with threats of a parliamentary shutdown, by Boris Johnson, in an effort to force a hard (no-deal) exit from the European Union (EU).

Consumer price index (CPI) numbers for the EU indicated a slight uptick year-on-year, in June, rising to 1.3% from the previous 1.2%. The European Central Bank (ECB) is reported to be investigating a change in their inflation target, while all indicators point to a potential rate cut, as well as renewed asset purchases in an effort to fight off the headwinds caused by the global slowdown as well as the trade wars.

The US had quite a full economic calendar this week, with monthly retail sales accelerating by 0.4% during June, outperforming market expectations, while the annual increase in retail sales amounted to 3.4%. Housing starts disappointed in June as the figure decelerated to 1.25 million from 1.26 million. Initial jobless claims, released on a weekly basis, rose from 208,000 to 216,000 - in line with analyst consensus. With the expectation of a rate cut by the Fed hanging in the undertow, the US economy remains resilient. A decrease in interest rate by the Fed would be seen as a pro-active approach to combating future headwinds, while the trade spat remains one of the key concerns from the Fed’s perspective.

US EQUITIES

After reaching all-time-highs on Tuesday, the NASDAQ, Dow Jones and S&P 500 lacked any sign of continued upward momentum, as a new wave of company earnings swung into effect. With around just-over seven percent of companies reporting Q2 earnings so far, on the S&P500, the next few weeks of earnings releases are set keep the three major indices in check. Along with this, the delayed resolution of the US-China trade war has also added a small dragging-effect to the overall equity market.

Since Friday last week, one can see that US markets aren’t too interested in making any massive decision on direction at the moment.

Netflix saw its share price plummeting more than 12% on Wednesday after releasing lower than expected growth numbers for quarter two (Q2). Losing around 130,000 subscribers, in the US, to the likes of Hulu, Amazon and Amazon Prime, the streaming service also undershot global expected new subscriber estimates for Q2 (2.7 million vs an expected 5 million new subscribers). Netflix’s CEO, Reed Hastings, boiled it down to both the gentle subscription fee hikes as well as lack of original content being released by Netflix itself. Netflix continue to believe that their expected growth trajectory will fall in place by the end of Q3, with most new future subscribers being based outside of the US. Some of Netflix’s earnings numbers, for Q2, were as follows:

In South African rand-terms, subtract 3.48% against each of these return-figures to see what the South African investor could be up in 2019, with the currency-effect added.

COMMODITIES

A slight turn in events was seen this week, as US Senator, Rand Paul, agreed to potentially meet up with Iranian Foreign Minister, Javad Zarif, with the sole purpose of trying to cool down the tensions between the US and Iran in the Middle East – this, ultimately pointing toward a potential easing of the US sanctions recently placed on Iran.

Following this announcement, both Brent Crude and West Texas Intermediate (WTI) were seen retreating by more than four percent a piece (Brent, down to lows of around $63.25 and WTI to $56.28 a barrel). The road ahead is still very rocky for oil prices, with oil tanker incidents in the Middle Eastern region generally increasing, while vague trade sanctions still hang in play. The next few weeks will more than likely see a sideways trend being locked-in for oil prices, as easing of sanctions, theoretically, should weaken demand for oil, as supply, coupled with Iranian exports, creeps up.

Brent Crude opened Friday’s trading day at $63.08 per barrel, while US West Texas Intermediate (WTI) opened at $56.10.

For the first time in a while, platinum took center stage this week, as it soared around three percent higher since last Friday, while palladium and gold traded lower and sideways, respectively. According to analysts, life can still be found within the platinum space in 2019, while investors should be weary of the recent palladium bull run. Gold, although taking a breather this week, may be poised to move higher over the coming weeks, with some analysts eyeing the $1,450.00 an ounce mark. On Friday morning, gold, platinum and palladium were trading at levels of around $1,441.90, $855.35 and $1,526.38 per fine ounce respectively.

SOUTH AFRICAN FUNDAMENTALS

All eyes were fixated on the South African Reserve Bank (SARB) on Thursday, as the Governor announced an interest rate cut of 0.25% - the first interest rate cut since March 2018. While inflation has increased slightly, the figure still remains well within the target range of the SARB. The SARB has forecast growth of 0.6% for the year. The subdued forecast is largely driven by the negative economic growth witnessed in Q1 of 2019, while global elements such as slowing growth and the uncertainty caused by ongoing trade wars continues to pose a threat to the local economy.

Local politics, ranging from the disruption of Parliament by the Economic Freedom Front, to the testimony of former president Jacob Zuma at the Zondo commission had no impact on the local market, as the focus remains squarely on the Fed’s interest rate decision and, yet again, the global trade dynamics.

The rand managed to hold its own again this week, trading in a tight range, reaching a high of R13.85 on Wednesday against the US dollar. Continuous carry trade remains one of the most prominent reasons for the resilience of the rand, with the first half of 2019 recording R53 billion of foreign inflows into government bonds - a significant increase from the R16 billion recorded during the same period of 2018.

No new details has emerged with regards to the turnaround plan for Eskom. The lights, however, remain on for the time being, with no threat of loadshedding since pre-election

SOUTH AFRICAN EQUITY

Over the weekend, AB Inbev (ANH) announced the cancellation of their much anticipated Asian IPO on the Hong Kong Stock Exchange. Investors seemed to be worried about the potentially murky state of the company, given the late and unexpected cancellation.

First and foremost, the cancellation of the IPO, will have a small impact on the duration of their expected settlement period, when looking at their debt burden, mainly bought upon by the purchase of SAB in 2016. Although the IPO wasn’t necessarily pivotal in paying off InBev’s debt burden, it certainly would’ve helped. To an immaterial degree, they may have lost shorter-term investor confidence and a potentially increased level of liquidity, with regard to the market price of their share. After stumbling around 3.70% after the announcement, to levels of around R1,210.00 per share, ANH spent the remainder of the week working back its losses and investor confidence. ANH opened Friday’s trading day at R1,234.63 per share

Richemont’s (CFR) Q1 sales numbers came in higher at 12% year-on-year (actual exchange rates) and 9% year-on-year (constant exchange rates). Growth was mainly seen coming out of the Far East countries such as Japan and China. Lower growth figures were seen coming out of the Americas, while Europe, the Middle East and Africa recorded negative growth for the first quarter. While CFR have ventured into the e-commerce business, it’s important to note that margins are a lot tighter within those realms, which could impact operating margins down-the-line. CFR held relatively strong throughout Thursday’s trading day, following the announcement. CFR opened at R120.79 per share on Friday morning.

Here’s some of the bigger movers on the JSE for the 2019 year so far, painting a relatively clear picture that investors are tending to lean toward the, historically-defined, safer haven segment:

THE WEEK AHEAD

Local CPI data is due for release on Wednesday, with markets expecting a 4.6% rise year-on-year for June, while the European Central Bank will announce their interest rate decision on Thursday, followed by the monetary policy statement that will be important to setting the tone for quantitative easing in the region. The rand is expected to remain on a range bound path, and continues to be driven largely by global factors.

On Friday morning the rand would’ve set the investor back R13.85 per US dollar, R15.59 a euro and R17.36 a British pound.

GLOBAL DATA AND POLITICS

Following a rather quiet few weeks, President Donald Trump once again moved to reignite the trade war. While the long-standing trade tiff between the US and China rages on, President Trump is setting his sights on other regions of the globe, including France and Japan. Earlier this week, Chinese gross domestic product (GDP) numbers gave investors a glimpse of the global slowdown, as the economic powerhouse posted growth of 6.2% year-on-year for Q2. This, the lowest level of growth, for China, recorded since 1992, while retail sales accelerated by 9.8% year-on-year in June, outperforming the market forecast of 8.5%

Locally, South Africa witnessed retail sales outperform expectations, gaining 2.2% year-on-year. When taking the retail sales numbers into consideration, in combination with various other improving economic indicators, Q2 GDP is sure to improve, following a dismal Q1.

The United Kingdom’s (U.K.) average earnings increased marginally to 3.4%, while the unemployment rate remained unchanged at 3.8%. Inflation remained steady at two percent, year-on-year, in June. The Brexit dynamic continues to weigh heavily on the U.K., with threats of a parliamentary shutdown, by Boris Johnson, in an effort to force a hard (no-deal) exit from the European Union (EU).

Consumer price index (CPI) numbers for the EU indicated a slight uptick year-on-year, in June, rising to 1.3% from the previous 1.2%. The European Central Bank (ECB) is reported to be investigating a change in their inflation target, while all indicators point to a potential rate cut, as well as renewed asset purchases in an effort to fight off the headwinds caused by the global slowdown as well as the trade wars.

The US had quite a full economic calendar this week, with monthly retail sales accelerating by 0.4% during June, outperforming market expectations, while the annual increase in retail sales amounted to 3.4%. Housing starts disappointed in June as the figure decelerated to 1.25 million from 1.26 million. Initial jobless claims, released on a weekly basis, rose from 208,000 to 216,000 - in line with analyst consensus. With the expectation of a rate cut by the Fed hanging in the undertow, the US economy remains resilient. A decrease in interest rate by the Fed would be seen as a pro-active approach to combating future headwinds, while the trade spat remains one of the key concerns from the Fed’s perspective.

US EQUITIES

After reaching all-time-highs on Tuesday, the NASDAQ, Dow Jones and S&P 500 lacked any sign of continued upward momentum, as a new wave of company earnings swung into effect. With around just-over seven percent of companies reporting Q2 earnings so far, on the S&P500, the next few weeks of earnings releases are set keep the three major indices in check. Along with this, the delayed resolution of the US-China trade war has also added a small dragging-effect to the overall equity market.

Since Friday last week, one can see that US markets aren’t too interested in making any massive decision on direction at the moment.

- S&P 500: down 0.08%

- NASDAQ: up 0.17%

- Dow Jones: up 0.24%

Netflix saw its share price plummeting more than 12% on Wednesday after releasing lower than expected growth numbers for quarter two (Q2). Losing around 130,000 subscribers, in the US, to the likes of Hulu, Amazon and Amazon Prime, the streaming service also undershot global expected new subscriber estimates for Q2 (2.7 million vs an expected 5 million new subscribers). Netflix’s CEO, Reed Hastings, boiled it down to both the gentle subscription fee hikes as well as lack of original content being released by Netflix itself. Netflix continue to believe that their expected growth trajectory will fall in place by the end of Q3, with most new future subscribers being based outside of the US. Some of Netflix’s earnings numbers, for Q2, were as follows:

- Revenue: $4.92 billion vs an expected $4.93 billion (mild miss)

- Earnings per share: 60 cents vs and expected 56 cents per share (beat)

- Global streaming paid memberships: Up 21.9% year-on-year, 151.5 million subscribers

- New US subscribers: A loss of 126,000 US subscribers was seen vs an expected increase for the quarter of 352,000 (large miss)

- New International subscribers: Only up 2.83 million vs analyst expectations of 4.81 million (miss)

- Facebook: up around 0.09%

- Amazon: down around 2.13%

- Apple: up around 1.56%

- Netflix: down around 13.67%

- Alphabet: up around 0.36%

In South African rand-terms, subtract 3.48% against each of these return-figures to see what the South African investor could be up in 2019, with the currency-effect added.

COMMODITIES

A slight turn in events was seen this week, as US Senator, Rand Paul, agreed to potentially meet up with Iranian Foreign Minister, Javad Zarif, with the sole purpose of trying to cool down the tensions between the US and Iran in the Middle East – this, ultimately pointing toward a potential easing of the US sanctions recently placed on Iran.

Following this announcement, both Brent Crude and West Texas Intermediate (WTI) were seen retreating by more than four percent a piece (Brent, down to lows of around $63.25 and WTI to $56.28 a barrel). The road ahead is still very rocky for oil prices, with oil tanker incidents in the Middle Eastern region generally increasing, while vague trade sanctions still hang in play. The next few weeks will more than likely see a sideways trend being locked-in for oil prices, as easing of sanctions, theoretically, should weaken demand for oil, as supply, coupled with Iranian exports, creeps up.

Brent Crude opened Friday’s trading day at $63.08 per barrel, while US West Texas Intermediate (WTI) opened at $56.10.

For the first time in a while, platinum took center stage this week, as it soared around three percent higher since last Friday, while palladium and gold traded lower and sideways, respectively. According to analysts, life can still be found within the platinum space in 2019, while investors should be weary of the recent palladium bull run. Gold, although taking a breather this week, may be poised to move higher over the coming weeks, with some analysts eyeing the $1,450.00 an ounce mark. On Friday morning, gold, platinum and palladium were trading at levels of around $1,441.90, $855.35 and $1,526.38 per fine ounce respectively.

SOUTH AFRICAN FUNDAMENTALS

All eyes were fixated on the South African Reserve Bank (SARB) on Thursday, as the Governor announced an interest rate cut of 0.25% - the first interest rate cut since March 2018. While inflation has increased slightly, the figure still remains well within the target range of the SARB. The SARB has forecast growth of 0.6% for the year. The subdued forecast is largely driven by the negative economic growth witnessed in Q1 of 2019, while global elements such as slowing growth and the uncertainty caused by ongoing trade wars continues to pose a threat to the local economy.

Local politics, ranging from the disruption of Parliament by the Economic Freedom Front, to the testimony of former president Jacob Zuma at the Zondo commission had no impact on the local market, as the focus remains squarely on the Fed’s interest rate decision and, yet again, the global trade dynamics.

The rand managed to hold its own again this week, trading in a tight range, reaching a high of R13.85 on Wednesday against the US dollar. Continuous carry trade remains one of the most prominent reasons for the resilience of the rand, with the first half of 2019 recording R53 billion of foreign inflows into government bonds - a significant increase from the R16 billion recorded during the same period of 2018.

No new details has emerged with regards to the turnaround plan for Eskom. The lights, however, remain on for the time being, with no threat of loadshedding since pre-election

SOUTH AFRICAN EQUITY

Over the weekend, AB Inbev (ANH) announced the cancellation of their much anticipated Asian IPO on the Hong Kong Stock Exchange. Investors seemed to be worried about the potentially murky state of the company, given the late and unexpected cancellation.

First and foremost, the cancellation of the IPO, will have a small impact on the duration of their expected settlement period, when looking at their debt burden, mainly bought upon by the purchase of SAB in 2016. Although the IPO wasn’t necessarily pivotal in paying off InBev’s debt burden, it certainly would’ve helped. To an immaterial degree, they may have lost shorter-term investor confidence and a potentially increased level of liquidity, with regard to the market price of their share. After stumbling around 3.70% after the announcement, to levels of around R1,210.00 per share, ANH spent the remainder of the week working back its losses and investor confidence. ANH opened Friday’s trading day at R1,234.63 per share

Richemont’s (CFR) Q1 sales numbers came in higher at 12% year-on-year (actual exchange rates) and 9% year-on-year (constant exchange rates). Growth was mainly seen coming out of the Far East countries such as Japan and China. Lower growth figures were seen coming out of the Americas, while Europe, the Middle East and Africa recorded negative growth for the first quarter. While CFR have ventured into the e-commerce business, it’s important to note that margins are a lot tighter within those realms, which could impact operating margins down-the-line. CFR held relatively strong throughout Thursday’s trading day, following the announcement. CFR opened at R120.79 per share on Friday morning.

Here’s some of the bigger movers on the JSE for the 2019 year so far, painting a relatively clear picture that investors are tending to lean toward the, historically-defined, safer haven segment:

- Impala Platinum: up 99.15%

- Kumba Iron Ore: up 70.75%

- Sibanye Gold: up 74.75%

- Rebosis Property Fund: down 76.58%

- Omnia: down 61.24%

- Brait: down 43.17%

THE WEEK AHEAD

Local CPI data is due for release on Wednesday, with markets expecting a 4.6% rise year-on-year for June, while the European Central Bank will announce their interest rate decision on Thursday, followed by the monetary policy statement that will be important to setting the tone for quantitative easing in the region. The rand is expected to remain on a range bound path, and continues to be driven largely by global factors.

On Friday morning the rand would’ve set the investor back R13.85 per US dollar, R15.59 a euro and R17.36 a British pound.

Our highlight for the week:

Our highlight of the week comes from the latest customs data released for May 2019 by the South African Revenue Service (SARS). We take a look at the South African imports from the United States of America and the exports from South Africa to the United States for 2019 so far.

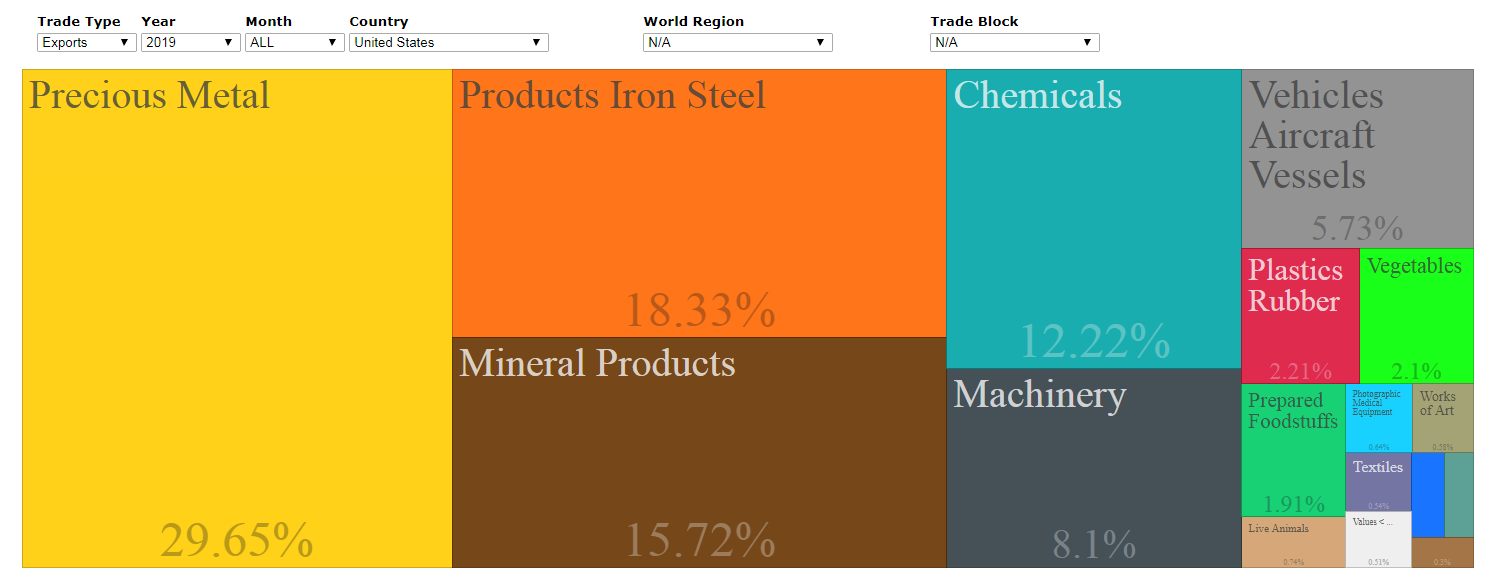

The treemap below shows the main product category exports from South Africa to the United States for 2019 so far (covering the months January 2019 to May 2019). As the image shows the bulk of South African exports to the United States falls under Precious Metals, with it making up just under 30% of South Africa's total exports to the USA so far during 2019. This category includes gold, platinum and diamonds.

The treemap below shows the main product category exports from South Africa to the United States for 2019 so far (covering the months January 2019 to May 2019). As the image shows the bulk of South African exports to the United States falls under Precious Metals, with it making up just under 30% of South Africa's total exports to the USA so far during 2019. This category includes gold, platinum and diamonds.

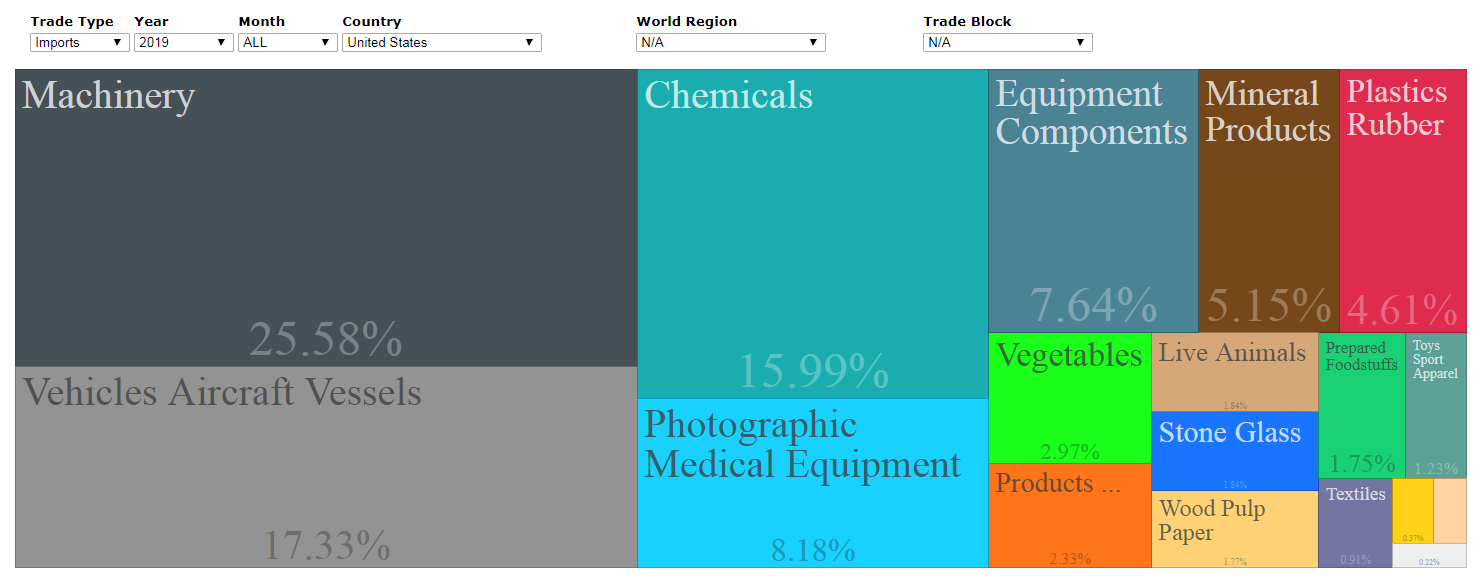

As the treemap of South Africa's imports from the USA below shows, the main product categories imported by South Africa from the USA is not the primary type goods or commodities (like we export to them) but goods that entailed a lot more manufacturing and processing). The main product category imported by South Africa from the United States is Machinery, with it making up more than a quarter of South Africa''s imports from the USA. The second biggest import category being vehicles, aircrafts and vehicles with it making up 17% of the total imports by South Africa from the USA. Mostly American built vehicles being imported into South Africa