|

Related Topics |

|

In our continued efforts to give our readers a broad number of views, opinions and information, we provide readers with Peregrine Treasury Services weekly market wrap below.

|

|

Peregrine Treasury Services Weekly Wrap as at 12 July 2019

In a world of contradictions, influential Twitter tweets and market upsets, one should consider keeping in mind that almost anything could happen, no matter how many indicators point toward the complete opposite assumption. This week reinforced the above logic, as Jerome Powell, Chairman of the Federal Reserve (Fed), testified in front of congress, on Wednesday afternoon. Last week Friday, as the US released unexpectedly impressive employment figures, markets geared up for a less-dovish Fed, reducing their bets on an interest rate cut. Soon thereafter however, sending the market into a correctional tailspin, the Fed arrived more dovishly than initially expected. In stark contradiction to the beliefs of a few days ago, it is now ‘all systems go’ for a rate cut at the end of June.

GLOBAL DATA AND POLITICS

As the Fed gears up to decrease interest rates, it seem that President Donald Trump will have his way for the time being, diminishing the likelihood of currency market interventions, in an effort to depreciate the dollar. United States (US) consumer price index (CPI) numbers, released on Thursday, indicated the biggest acceleration in consumer goods prices in 18 months, as tariffs started triggering substantial gains in the prices relating to a series of goods and services. US JOLTs job openings undershot expectations of 7.47 million, coming in at 7.32 million, while initial jobless claims declined to 209,000 for the week. Friday will see the release of producer price index (PPI) numbers. The market is expecting PPI to come in at 1.60% year-on-year for June.

The uncertainty of Brexit, a stronger dollar and weak economic data from the United Kingdom (U.K.) saw the British pound reach two year lows earlier this week, before demonstrating a slight recovery on Wednesday, as the dollar came under pressure. With the ‘Brexit can’ now being kicked too far down the road to be turned around, the only question left is whether a deal between the UK and the European Union will be reached, and if so what that deal would look like. With regard to the U.K., gross domestic product (GDP) remains subdued at 1.50% month-on-month during May, while industrial production remained under pressure, accelerating by a mere 0.90% year-on-year during the same month. Manufacturing production stagnated year-on-year, for the region.

The EU is due to release industrial production figures on Friday, while the European Central Bank policy-makers agreed to start preparing for policy-easing, in order to assist the lagging EU economy. The policy-easing will likely involve the provision of additional monetary stimuli, which could even be followed by an interest rate cut.

China reported stable CPI figures year-on-year for June, accelerating by 2.70%, in line with expectations. PPI undershot expectations coming in at 0.0%, down from the previous 0.6%. China is set to release import and export data, as well as foreign direct investment numbers, on Friday.

A quiet week of data releases was seen on South African shores, with gold, mining and manufacturing production data released on Thursday. Mining production decelerated less than expected, declining by 1.50% year-on-year, while gold production remained under extreme pressure, dropping by 24.40% year-on-year during May. Manufacturing production numbers contracted by 1.50% month-on-month during May, after posting a gain of 2.80% during April.

US EQUITIES

US Equities edged ever so slightly higher this week, mainly having had waited on the edge of their seats for Jerome Powell’s testimony which was finally delivered on Wednesday afternoon. After starting the week off sluggishly, all three indices were seen jumping higher after the Fed’s dovish sentiment was voiced. The moves in the hours following the announcement on Wednesday were as follows:

Facebook (FB), now venturing into their own form of financial services and cryptocurrency venture - called Libra, was heavily questioned and highlighted as a cause-for-concern, as part of the Federal Reserve’s testimony on Wednesday. Considering the privacy issues that FB has been plagued by over the last few years, it makes sense that Libra could be heavily queried going forward. Having said this, FB really stormed through the week, returning investors over four percent since last Friday. Facebook opened up Friday’s trading day at $201.23 per share.

FAANGs performance, for the last five trading days:

Year-to-date, the Dow Jones is up around 17.08%, the NASDAQ: 23.52% and the S&P 500: 19.67%.

In South African rand-terms, subtract 0.26% against each of these return-figures to see what the South African investor could be up in 2019, with the currency-effect added.

COMMODITIES

Both gold and Brent Crude oil were seen breaking higher this week, as a perfect mix of news was delivered by both the Fed and the Energy Information Administration. US crude oil inventory numbers were seen dropping by 9.40 million barrels last week, compared to an expected 3.08 million barrel drop predicted by analysts. This unexpected drop in oil inventories assisted a, roughly seven percent, move higher for both Brent Crude and West Texas Intermediate (WTI) during the course of the week.

Along with the unexpectedly lower inventory numbers, both Jerome Powell’s Fed guidance (to maintain current economic expansion) as well as evacuations from oil rigs within the Gulf of Mexico being implemented, due to strengthening Tropical Storm Barry, assisted oil on its incredible ramp up this week. It seems unlikely that oil will be able to maintain these levels, once inventory picks up again and Tropical Storm Barry resides. Brent Crude opened Friday’s trading day at $66.98 per barrel, while US West Texas Intermediate (WTI) opened at $60.58.

When looking at the last five trading days, gold actually traded relatively flat, however, it’s move lower in the beginning of the week was quickly whipped back up to levels of around $1,421.15 per ounce, after Jerome Powell alluded to the possibility of a mind-bending 50 basis point cut in rates (which will more than likely not happen). With the likelihood of monetary easing on the horizon for the US, investors have been stocking up on the precious metal amidst the obscure monetary environment. Palladium continues to show its strength, by pushing up and over the $1,600.00 an ounce level during the week. As i note of interest, Goldman Sachs have now mentioned that clients should look at trading palladium with caution in the coming months. It will be interesting to watch this particular precious metal, for the remainder of 2019.

On Friday morning, gold, platinum and palladium were trading at levels of around $1,406.21, $824.57 and $1,554.18 per fine ounce respectively.

SOUTH AFRICAN FUNDAMENTALS

The Economic Freedom Front (EFF) is back to their old habits, disrupting parliament on Thursday, as Pravin Gordhan took the stand to table his budget vote, stating that the party refused to be addressed by a “constitutional delinquent”. Gordhan has been the main focus of the Public Protector, Busisiwe Mkhwebane, leading many to believe that she has been “captured” by the Ace Mageshule faction, in an effort to eradicate all those in strong opposition to the broader state capture and looting of the nation.

While the stand-off between the two factions within the African National Congress (ANC) is far from over, the power struggle continues to play out rather publicly. President Cyril Ramaphosa reaffirmed his power by appointing South African Reserve Bank’s (SARB) governor, Lesetja Kganyago, to serve another term. This move, in an effort to reassure markets of the independence of the SARB and of course his authority as President of the Republic.

The SARB wasn’t the only glimmer of hope for South Africa this week, as Finance Minister, Tito Mboweni, moved to appoint the new Public Investment Corporation (PIC) board, following the state capture scandal that cast a dark cloud over the entity. The board, which includes previous ABSA CEO, Maria Ramos, will be imperative to ensure the protection and performance of state pensions in particular. The PIC have also offered a debt-equity swap to the embattled state owned enterprise, Eskom, as a potential rescue plan – a plan that could lead to the restructuring of Eskom, without turning to the private sector - an option that is highly contested by unions and other political bodies.

The performance of the local currency has largely been driven by the testimony of Jerome Powell. The renewed anticipation of a drop in federal interest rates saw the US dollar tumble once again, causing the rand to gain significant ground, breaking below the R14.00 mark in overnight trade on Wednesday. The potential rescue plan (of Eskom by the PIC) assisted the rand in gaining even more ground during trade on Thursday, maintaining the break below R14.00 and trading as high as R13.88 against the Greenback.

The Monetary Policy Committee is also very likely to reduce local interest rates during their announcement next week. The weakening effect on the rand by a 25 basis-point cut will however be limited, as it is likely to be offset by the positive effect of the US Fed rate cut and its potential to activate some economic activity. The local economy, however, will require more than an interest rate cut to see any significant and sustainable growth.

SOUTH AFRICAN EQUITY

With the local political landscape having had a relatively calm two weeks, all eyes were, once again, focused on the Fed’s testimony which was delivered on Wednesday afternoon. In essence, the ebb and flow of the US dollar, vs the local rand, has been the major driver of South African listed stocks. Where resources had a great run last week, this week saw the precious metal sector cooling off by just over one percent. Most other sectors were seen climbing little more than 0.50% in the last five trading days - an extremely tricky trail to navigate.

ArcelorMittal (ACL) were seen releasing a gloomy six-month trading update on Wednesday which stated that the company had been hampered by rigidly high costs which lie outside of the company’s control, including the likes of raw materials, electricity, and rail and port costs. The company is also likely to face additional headwinds, as it navigates the formal consultation process, which will assess the feasibility and impact of the 2,000 job losses potentially being considered as part of the firm’s cost-cutting strategy. ACL were seen closing 15.80% down on the day of the release of this news, closing at a market price of R2.93 per share on Wednesday. Thursday morning saw the stock touching lows of around R2.71 per share. ACL opened Friday’s trading day at R2.90 per share.

Woolworths (WHL) finally caught a much-needed break after having spent most of 2019 under the R50.00 a share mark, due to unfavourable news coming out from its David Jones clothing business in Australia earlier in the year. Thursday morning saw WHL releasing a surprisingly positive trading update for the 53 weeks ending 30 June 2019. Key figures that influenced Woolworths’ stronger-than-expected performance:

Here’s some of the bigger movers on the JSE for the 2019 year so far, painting a relatively clear picture that investors are tending to lean toward the, historically-defined, safer haven segment:

THE WEEK AHEAD

With the current momentum, the rand is likely to test the R13.80 mark, while local interest rate cuts could see the rand trade toward the upper band of R14.05, provided that the global backdrop remains the same. On Friday morning the rand would’ve set the investor back R13.92 per US dollar, R15.70 a euro and R17.47 a British pound

GLOBAL DATA AND POLITICS

As the Fed gears up to decrease interest rates, it seem that President Donald Trump will have his way for the time being, diminishing the likelihood of currency market interventions, in an effort to depreciate the dollar. United States (US) consumer price index (CPI) numbers, released on Thursday, indicated the biggest acceleration in consumer goods prices in 18 months, as tariffs started triggering substantial gains in the prices relating to a series of goods and services. US JOLTs job openings undershot expectations of 7.47 million, coming in at 7.32 million, while initial jobless claims declined to 209,000 for the week. Friday will see the release of producer price index (PPI) numbers. The market is expecting PPI to come in at 1.60% year-on-year for June.

The uncertainty of Brexit, a stronger dollar and weak economic data from the United Kingdom (U.K.) saw the British pound reach two year lows earlier this week, before demonstrating a slight recovery on Wednesday, as the dollar came under pressure. With the ‘Brexit can’ now being kicked too far down the road to be turned around, the only question left is whether a deal between the UK and the European Union will be reached, and if so what that deal would look like. With regard to the U.K., gross domestic product (GDP) remains subdued at 1.50% month-on-month during May, while industrial production remained under pressure, accelerating by a mere 0.90% year-on-year during the same month. Manufacturing production stagnated year-on-year, for the region.

The EU is due to release industrial production figures on Friday, while the European Central Bank policy-makers agreed to start preparing for policy-easing, in order to assist the lagging EU economy. The policy-easing will likely involve the provision of additional monetary stimuli, which could even be followed by an interest rate cut.

China reported stable CPI figures year-on-year for June, accelerating by 2.70%, in line with expectations. PPI undershot expectations coming in at 0.0%, down from the previous 0.6%. China is set to release import and export data, as well as foreign direct investment numbers, on Friday.

A quiet week of data releases was seen on South African shores, with gold, mining and manufacturing production data released on Thursday. Mining production decelerated less than expected, declining by 1.50% year-on-year, while gold production remained under extreme pressure, dropping by 24.40% year-on-year during May. Manufacturing production numbers contracted by 1.50% month-on-month during May, after posting a gain of 2.80% during April.

US EQUITIES

US Equities edged ever so slightly higher this week, mainly having had waited on the edge of their seats for Jerome Powell’s testimony which was finally delivered on Wednesday afternoon. After starting the week off sluggishly, all three indices were seen jumping higher after the Fed’s dovish sentiment was voiced. The moves in the hours following the announcement on Wednesday were as follows:

- S&P 500: up 1.02%

- NASDAQ: up 1.28%

- Dow Jones: up 0.89%

Facebook (FB), now venturing into their own form of financial services and cryptocurrency venture - called Libra, was heavily questioned and highlighted as a cause-for-concern, as part of the Federal Reserve’s testimony on Wednesday. Considering the privacy issues that FB has been plagued by over the last few years, it makes sense that Libra could be heavily queried going forward. Having said this, FB really stormed through the week, returning investors over four percent since last Friday. Facebook opened up Friday’s trading day at $201.23 per share.

FAANGs performance, for the last five trading days:

- Facebook: up around 3.23%

- Amazon: up around 3.85%

- Apple: down around 0.65%

- Netflix: up around 0.85%

- Alphabet: up around 2.22%

- Viacom: labour cost represents 2% of sales

- Under Armour: 3% of sales

- Seagate Technology PLC: 3% of sales

- Monster Beverage Corporation: 5% of sales

Year-to-date, the Dow Jones is up around 17.08%, the NASDAQ: 23.52% and the S&P 500: 19.67%.

In South African rand-terms, subtract 0.26% against each of these return-figures to see what the South African investor could be up in 2019, with the currency-effect added.

COMMODITIES

Both gold and Brent Crude oil were seen breaking higher this week, as a perfect mix of news was delivered by both the Fed and the Energy Information Administration. US crude oil inventory numbers were seen dropping by 9.40 million barrels last week, compared to an expected 3.08 million barrel drop predicted by analysts. This unexpected drop in oil inventories assisted a, roughly seven percent, move higher for both Brent Crude and West Texas Intermediate (WTI) during the course of the week.

Along with the unexpectedly lower inventory numbers, both Jerome Powell’s Fed guidance (to maintain current economic expansion) as well as evacuations from oil rigs within the Gulf of Mexico being implemented, due to strengthening Tropical Storm Barry, assisted oil on its incredible ramp up this week. It seems unlikely that oil will be able to maintain these levels, once inventory picks up again and Tropical Storm Barry resides. Brent Crude opened Friday’s trading day at $66.98 per barrel, while US West Texas Intermediate (WTI) opened at $60.58.

When looking at the last five trading days, gold actually traded relatively flat, however, it’s move lower in the beginning of the week was quickly whipped back up to levels of around $1,421.15 per ounce, after Jerome Powell alluded to the possibility of a mind-bending 50 basis point cut in rates (which will more than likely not happen). With the likelihood of monetary easing on the horizon for the US, investors have been stocking up on the precious metal amidst the obscure monetary environment. Palladium continues to show its strength, by pushing up and over the $1,600.00 an ounce level during the week. As i note of interest, Goldman Sachs have now mentioned that clients should look at trading palladium with caution in the coming months. It will be interesting to watch this particular precious metal, for the remainder of 2019.

On Friday morning, gold, platinum and palladium were trading at levels of around $1,406.21, $824.57 and $1,554.18 per fine ounce respectively.

SOUTH AFRICAN FUNDAMENTALS

The Economic Freedom Front (EFF) is back to their old habits, disrupting parliament on Thursday, as Pravin Gordhan took the stand to table his budget vote, stating that the party refused to be addressed by a “constitutional delinquent”. Gordhan has been the main focus of the Public Protector, Busisiwe Mkhwebane, leading many to believe that she has been “captured” by the Ace Mageshule faction, in an effort to eradicate all those in strong opposition to the broader state capture and looting of the nation.

While the stand-off between the two factions within the African National Congress (ANC) is far from over, the power struggle continues to play out rather publicly. President Cyril Ramaphosa reaffirmed his power by appointing South African Reserve Bank’s (SARB) governor, Lesetja Kganyago, to serve another term. This move, in an effort to reassure markets of the independence of the SARB and of course his authority as President of the Republic.

The SARB wasn’t the only glimmer of hope for South Africa this week, as Finance Minister, Tito Mboweni, moved to appoint the new Public Investment Corporation (PIC) board, following the state capture scandal that cast a dark cloud over the entity. The board, which includes previous ABSA CEO, Maria Ramos, will be imperative to ensure the protection and performance of state pensions in particular. The PIC have also offered a debt-equity swap to the embattled state owned enterprise, Eskom, as a potential rescue plan – a plan that could lead to the restructuring of Eskom, without turning to the private sector - an option that is highly contested by unions and other political bodies.

The performance of the local currency has largely been driven by the testimony of Jerome Powell. The renewed anticipation of a drop in federal interest rates saw the US dollar tumble once again, causing the rand to gain significant ground, breaking below the R14.00 mark in overnight trade on Wednesday. The potential rescue plan (of Eskom by the PIC) assisted the rand in gaining even more ground during trade on Thursday, maintaining the break below R14.00 and trading as high as R13.88 against the Greenback.

The Monetary Policy Committee is also very likely to reduce local interest rates during their announcement next week. The weakening effect on the rand by a 25 basis-point cut will however be limited, as it is likely to be offset by the positive effect of the US Fed rate cut and its potential to activate some economic activity. The local economy, however, will require more than an interest rate cut to see any significant and sustainable growth.

SOUTH AFRICAN EQUITY

With the local political landscape having had a relatively calm two weeks, all eyes were, once again, focused on the Fed’s testimony which was delivered on Wednesday afternoon. In essence, the ebb and flow of the US dollar, vs the local rand, has been the major driver of South African listed stocks. Where resources had a great run last week, this week saw the precious metal sector cooling off by just over one percent. Most other sectors were seen climbing little more than 0.50% in the last five trading days - an extremely tricky trail to navigate.

ArcelorMittal (ACL) were seen releasing a gloomy six-month trading update on Wednesday which stated that the company had been hampered by rigidly high costs which lie outside of the company’s control, including the likes of raw materials, electricity, and rail and port costs. The company is also likely to face additional headwinds, as it navigates the formal consultation process, which will assess the feasibility and impact of the 2,000 job losses potentially being considered as part of the firm’s cost-cutting strategy. ACL were seen closing 15.80% down on the day of the release of this news, closing at a market price of R2.93 per share on Wednesday. Thursday morning saw the stock touching lows of around R2.71 per share. ACL opened Friday’s trading day at R2.90 per share.

Woolworths (WHL) finally caught a much-needed break after having spent most of 2019 under the R50.00 a share mark, due to unfavourable news coming out from its David Jones clothing business in Australia earlier in the year. Thursday morning saw WHL releasing a surprisingly positive trading update for the 53 weeks ending 30 June 2019. Key figures that influenced Woolworths’ stronger-than-expected performance:

- Sales for the year-ending 30 June: up 5.90%

- Food sales growth: up 9.80%, for the 52 weeks (maybe the firm should focus more on this business? Imagine an even higher-end Whole Foods-like division, to the already-loved WHL fresh fruit, veg and meat selection. With the robust brand they’ve created, would a risk in venturing into a brand new pioneering segment (within South Africa) be fruitless? Definitely something to think about)

- General sales prices were up by 1.80% for the year

- Clothing segment, David Jones, continued to add its adverse drag: one percent increase in local (Australian) sales, for the period

Here’s some of the bigger movers on the JSE for the 2019 year so far, painting a relatively clear picture that investors are tending to lean toward the, historically-defined, safer haven segment:

- Impala Platinum: up 102.29%

- Kumba Iron Ore: up 66.57%

- Sibanye Gold: up 66.67%

- Rebosis Property Fund: down 71.75%

- Omnia: down 64.50%

- Brait: down 39.33%

THE WEEK AHEAD

With the current momentum, the rand is likely to test the R13.80 mark, while local interest rate cuts could see the rand trade toward the upper band of R14.05, provided that the global backdrop remains the same. On Friday morning the rand would’ve set the investor back R13.92 per US dollar, R15.70 a euro and R17.47 a British pound

Our highlight for the week:

Our highlight of the week comes from the latest customs data released for May 2019 by the South African Revenue Service (SARS). We take a look at the South African imports from the United States of America and the exports from South Africa to the United States for 2019 so far.

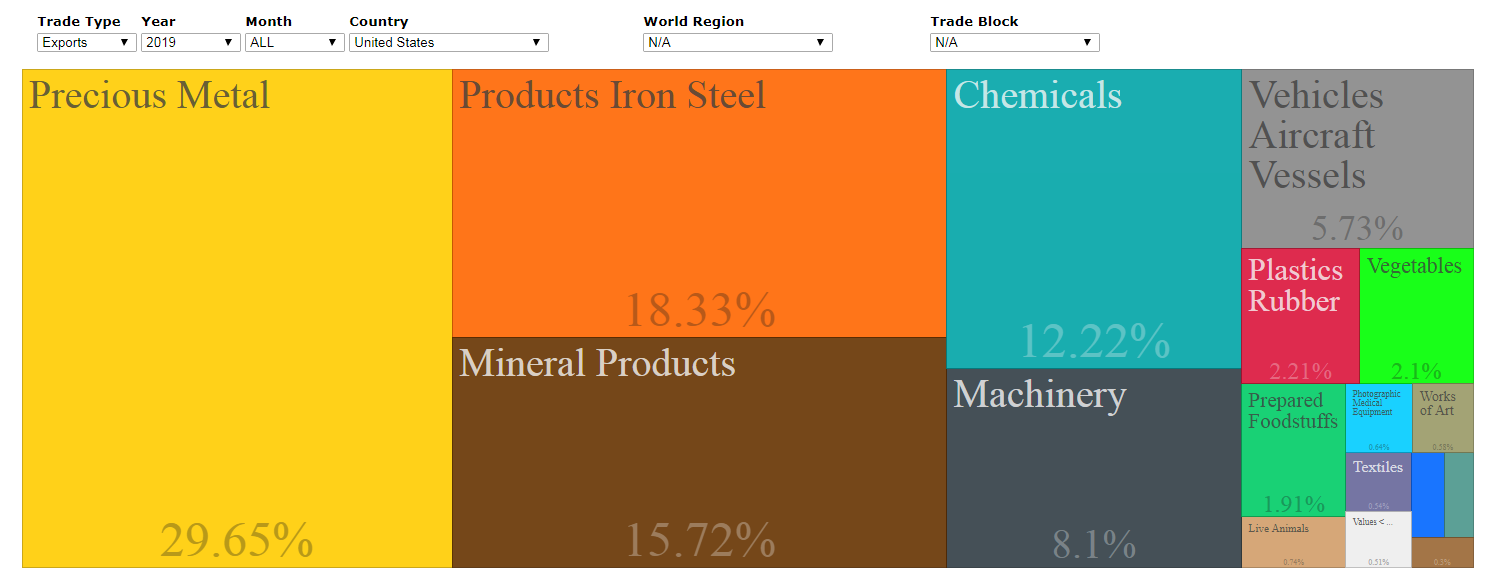

The treemap below shows the main product category exports from South Africa to the United States for 2019 so far (covering the months January 2019 to May 2019). As the image shows the bulk of South African exports to the United States falls under Precious Metals, with it making up just under 30% of South Africa's total exports to the USA so far during 2019. This category includes gold, platinum and diamonds.

The treemap below shows the main product category exports from South Africa to the United States for 2019 so far (covering the months January 2019 to May 2019). As the image shows the bulk of South African exports to the United States falls under Precious Metals, with it making up just under 30% of South Africa's total exports to the USA so far during 2019. This category includes gold, platinum and diamonds.

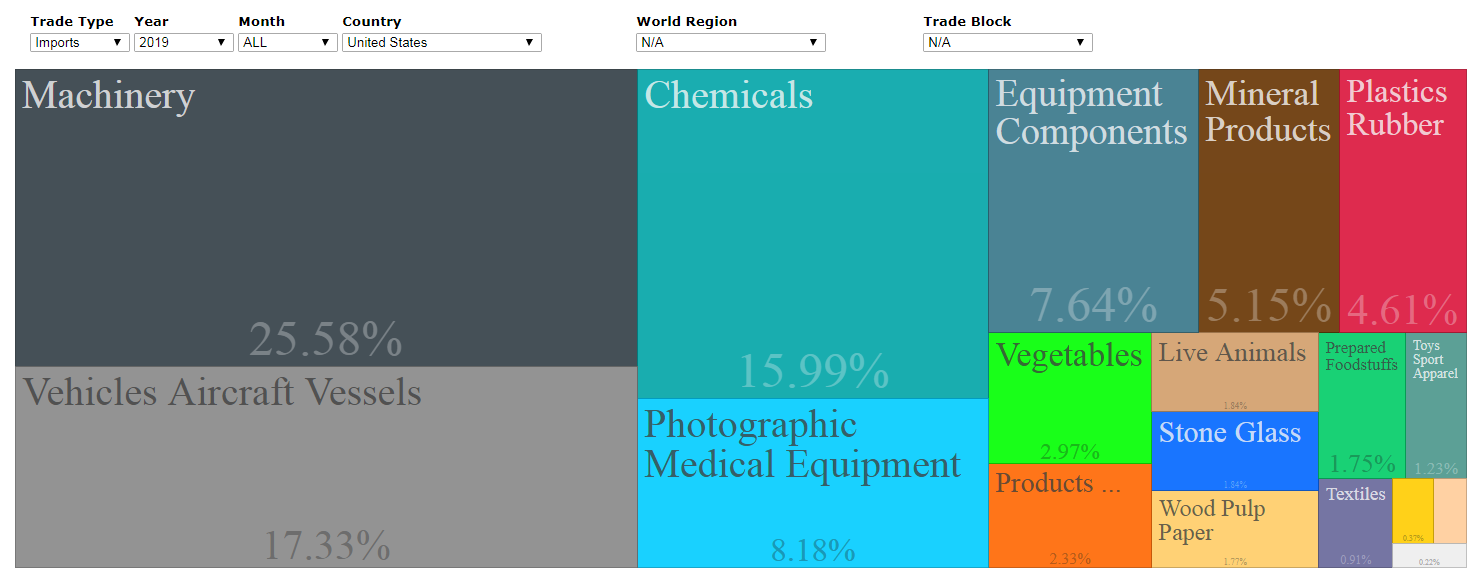

As the treemap of South Africa's imports from the USA below shows, the main product categories imported by South Africa from the USA is not the primary type goods or commodities (like we export to them) but goods that entailed a lot more manufacturing and processing). The main product category imported by South Africa from the United States is Machinery, with it making up more than a quarter of South Africa''s imports from the USA. The second biggest import category being vehicles, aircrafts and vehicles with it making up 17% of the total imports by South Africa from the USA. Mostly American built vehicles being imported into South Africa