|

Related Topics |

|

We take a look at the financial results for the year ending March 2019 for MultiChoice Group (after its unbundling from Naspers (NPN) earlier in the year. A few weeks ago the group stated they expected a loss of around R8 a share due to exchange rate losses and cost of empowerment transaction.

|

|

Background on MultiChoice

MULTICHOICE

MultiChoice, its subsidiaries, affiliates and associates ("MultiChoice Group") is one of the leading video entertainment operators on the African continent, and one of the fastest growing pay-TV broadcast providers globally, entertaining 13.9 million households (as at 30 September 2018) across 50 countries. Its carefully curated local and international content is distributed across multiple platforms, including digital satellite and terrestrial television, as well as through OTT solutions. The MultiChoice Group is structured around the following three business segments: - South Africa, the MultiChoice Group's division that offers digital satellite television and subscription video-on-demand services to 7.2 million subscribers in South Africa (as at 30 September 2018). Connected Video, which forms part of the South Africa segment from a financial reporting standpoint, delivers online video entertainment services to subscribers; - Rest of Africa, the MultiChoice Group's division which offers digital satellite, online services and digital terrestrial television services to 6.7 million subscribers across Africa (as at 30 September 2018); and - Technology, which includes the MultiChoice Group's leading digital platform and application security division, Irdeto.

MultiChoice, its subsidiaries, affiliates and associates ("MultiChoice Group") is one of the leading video entertainment operators on the African continent, and one of the fastest growing pay-TV broadcast providers globally, entertaining 13.9 million households (as at 30 September 2018) across 50 countries. Its carefully curated local and international content is distributed across multiple platforms, including digital satellite and terrestrial television, as well as through OTT solutions. The MultiChoice Group is structured around the following three business segments: - South Africa, the MultiChoice Group's division that offers digital satellite television and subscription video-on-demand services to 7.2 million subscribers in South Africa (as at 30 September 2018). Connected Video, which forms part of the South Africa segment from a financial reporting standpoint, delivers online video entertainment services to subscribers; - Rest of Africa, the MultiChoice Group's division which offers digital satellite, online services and digital terrestrial television services to 6.7 million subscribers across Africa (as at 30 September 2018); and - Technology, which includes the MultiChoice Group's leading digital platform and application security division, Irdeto.

On 27 February 2019 we had the following to say regarding a potention valuation of MultiChoice shares by the market once it lists.

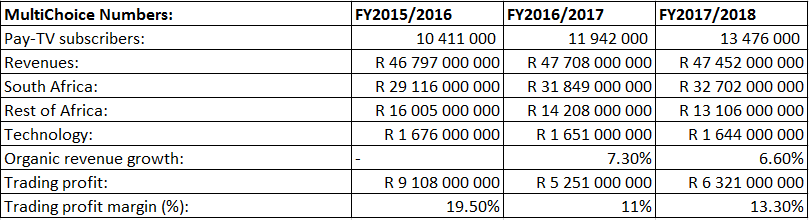

"So while MultiChoice has seen strong subscriber numbers growth over the last three years, infact 29.4%, while revenue over the same period only grew by 1.4%. Their trading profit margins are in decline too. But looking at the number of shares MultiChoice plans on issuing, their trading profits and placing a PE ratio of 15 on MultiChoice shares, it will give the company a valuation of R94.8 billion (which will make MultiChoice the 21st largest firm listed on the JSE) or around R211 a share

Note we do not think that MultiChoice will trade at a PE of 15. We merely used it as a benchmark PE ratio as it is close to the overall market average. We believe in the long run MultiChoice group will trade at a PE of around 8, due to the struggling segment they are operating in. Competition from online pay per view companies such as Netflix eating into their subscriber base. At a PE of 8 we see them trading at around R112 a share.

But dont be surprised if on listing the price surges as large funds tracking the Top 40 (and dont have a lot of exposure in NPN) needs to buy the share to have it in their funds. A gradual decline after the feeding frenzy mayhem of listing will then probably set in and MCG we predict will be trading at a PE of around 7/8 a few months after listing."

So where are MCG shares trading at right now after a few months of trading on the Johannesburg Stock Exchange? The screenshot below, taken from Sharenet shows that its been a pretty positive period for the group since it's listing on the JSE.

"So while MultiChoice has seen strong subscriber numbers growth over the last three years, infact 29.4%, while revenue over the same period only grew by 1.4%. Their trading profit margins are in decline too. But looking at the number of shares MultiChoice plans on issuing, their trading profits and placing a PE ratio of 15 on MultiChoice shares, it will give the company a valuation of R94.8 billion (which will make MultiChoice the 21st largest firm listed on the JSE) or around R211 a share

Note we do not think that MultiChoice will trade at a PE of 15. We merely used it as a benchmark PE ratio as it is close to the overall market average. We believe in the long run MultiChoice group will trade at a PE of around 8, due to the struggling segment they are operating in. Competition from online pay per view companies such as Netflix eating into their subscriber base. At a PE of 8 we see them trading at around R112 a share.

But dont be surprised if on listing the price surges as large funds tracking the Top 40 (and dont have a lot of exposure in NPN) needs to buy the share to have it in their funds. A gradual decline after the feeding frenzy mayhem of listing will then probably set in and MCG we predict will be trading at a PE of around 7/8 a few months after listing."

So where are MCG shares trading at right now after a few months of trading on the Johannesburg Stock Exchange? The screenshot below, taken from Sharenet shows that its been a pretty positive period for the group since it's listing on the JSE.

The summary below shows the performance of MultiChoice (MCG) shares over various time periods since its listing at the end of February 2019.

- 1 week: 1.11%

- 1 month: 7.71%

- Month to date (MTD): 9.48%

- Year to date (YTD): 25.88%

MultiChoice warning investors about the expected headline loss per share

Earlier in the month MCG released the following trading update in which it warned investors that it will be making around R8 loss per share in their financial results it will be releasing.

Trading statement

Shareholders are advised that the MultiChoice group ("the group") is finalising its consolidated annual financial statements for the twelve months ended 31 March 2019 ("current period"). Core headline earnings per share and trading profit Shareholders are reminded that the board considers core headline earnings per share and trading profit as the two most appropriate indicators of the operating performance of the group, as they adjust for non-recurring and non- operational items.

Compared to the group´s results for the twelve months ended 31 March 2018 ("prior year") included within the pre- listing statement, the group expects core headline earnings per share for the current period to be between 8% (30 ZAR cents) and 12% (45 ZAR cents) higher than the prior year´s reported 374 ZAR cents.

Trading profit is expected to be between 9% (R0.6bn) and 13% (R0.8bn) higher than the prior year´s reported R6,3bn. On an organic basis (i.e. reflecting results on a constant currency basis, excluding any M&A) trading profit is expected to be between 24% (R1.5bn) and 30% (R1.9bn) higher than the prior year’s reported R6,3bn. The improved financial performance expected for the current period is mainly driven by solid subscriber growth and a reduction in losses in the Rest of Africa segment. As explained in the pre-listing statement, core headline earnings per share and organic trading profit constitute pro forma financial information in terms of the JSE Listings Requirements.

The pro forma financial information is the responsibility of the group's directors, has been prepared for illustrative purposes only, and may not fairly present the group’s financial position, changes in equity, cash flows or results of operations. Core headline earnings is calculated by adjusting headline earnings for the following items, net of tax and non-controlling interests: a) amortisation of intangible assets arising from business combinations; b) accounting adjustments stemming from IFRS 3: Business Combinations; c) equity-settled share-based payment compensation; d) unrealised foreign currency gains/losses; e) certain fair-value adjustments under IFRS; and f) non-recurring current and deferred taxation impacts. Organic trading profit is calculated by excluding foreign currency movements and changes in the composition of the group. Loss per share and headline loss per share Compared to the prior year, the group expects loss per share for the current period to be between 673 ZAR cents and 739 ZAR cents lower than the prior year´s reported earnings per share of 332 ZAR cents.

Headline loss per share for the current period is expected to be between 724 ZAR cents and 800 ZAR cents lower than the prior year´s reported headline earnings per share of 410 ZAR cents. The key reasons for the movements above are set out below:

a) As disclosed in annex 7 of the pre-listing statement, the group had to account for the impact of allocating for no consideration a 5% stake in MultiChoice South Africa Holdings (Pty) Ltd to Phuthuma Nathi Investments 1 and Phuthuma Nathi Investments 2 as part of the unbundling process. As a result, loss per share and headline loss per share were impacted significantly by the once-off equity-settled share-based compensation charge recognised on what was an effective disposal of 5% of the group´s interest in MultiChoice South Africa Holdings (Pty) Ltd. While the impact of this transaction is removed from core headline earnings per share and trading profit, it is included in both loss per share and headline loss per share. This is expected to reduce earnings per share and headline earnings per share by 438 ZAR cents.

b) Furthermore, the impact of the depreciation of SA Rand against the US dollar has led to an increase in unrealised foreign exchange losses on translation of the group’s US dollar denominated transponder lease liabilities. This is expected to reduce earnings per share and headline earnings per share by 263 ZAR cents.

Further details will be provided in the consolidated provisional annual results, due to be released on SENS on 18 June 2019. The financial information on which this trading statement is based has not been reviewed and reported on by the Company´s external auditor.

End SENS

Trading statement

Shareholders are advised that the MultiChoice group ("the group") is finalising its consolidated annual financial statements for the twelve months ended 31 March 2019 ("current period"). Core headline earnings per share and trading profit Shareholders are reminded that the board considers core headline earnings per share and trading profit as the two most appropriate indicators of the operating performance of the group, as they adjust for non-recurring and non- operational items.

Compared to the group´s results for the twelve months ended 31 March 2018 ("prior year") included within the pre- listing statement, the group expects core headline earnings per share for the current period to be between 8% (30 ZAR cents) and 12% (45 ZAR cents) higher than the prior year´s reported 374 ZAR cents.

Trading profit is expected to be between 9% (R0.6bn) and 13% (R0.8bn) higher than the prior year´s reported R6,3bn. On an organic basis (i.e. reflecting results on a constant currency basis, excluding any M&A) trading profit is expected to be between 24% (R1.5bn) and 30% (R1.9bn) higher than the prior year’s reported R6,3bn. The improved financial performance expected for the current period is mainly driven by solid subscriber growth and a reduction in losses in the Rest of Africa segment. As explained in the pre-listing statement, core headline earnings per share and organic trading profit constitute pro forma financial information in terms of the JSE Listings Requirements.

The pro forma financial information is the responsibility of the group's directors, has been prepared for illustrative purposes only, and may not fairly present the group’s financial position, changes in equity, cash flows or results of operations. Core headline earnings is calculated by adjusting headline earnings for the following items, net of tax and non-controlling interests: a) amortisation of intangible assets arising from business combinations; b) accounting adjustments stemming from IFRS 3: Business Combinations; c) equity-settled share-based payment compensation; d) unrealised foreign currency gains/losses; e) certain fair-value adjustments under IFRS; and f) non-recurring current and deferred taxation impacts. Organic trading profit is calculated by excluding foreign currency movements and changes in the composition of the group. Loss per share and headline loss per share Compared to the prior year, the group expects loss per share for the current period to be between 673 ZAR cents and 739 ZAR cents lower than the prior year´s reported earnings per share of 332 ZAR cents.

Headline loss per share for the current period is expected to be between 724 ZAR cents and 800 ZAR cents lower than the prior year´s reported headline earnings per share of 410 ZAR cents. The key reasons for the movements above are set out below:

a) As disclosed in annex 7 of the pre-listing statement, the group had to account for the impact of allocating for no consideration a 5% stake in MultiChoice South Africa Holdings (Pty) Ltd to Phuthuma Nathi Investments 1 and Phuthuma Nathi Investments 2 as part of the unbundling process. As a result, loss per share and headline loss per share were impacted significantly by the once-off equity-settled share-based compensation charge recognised on what was an effective disposal of 5% of the group´s interest in MultiChoice South Africa Holdings (Pty) Ltd. While the impact of this transaction is removed from core headline earnings per share and trading profit, it is included in both loss per share and headline loss per share. This is expected to reduce earnings per share and headline earnings per share by 438 ZAR cents.

b) Furthermore, the impact of the depreciation of SA Rand against the US dollar has led to an increase in unrealised foreign exchange losses on translation of the group’s US dollar denominated transponder lease liabilities. This is expected to reduce earnings per share and headline earnings per share by 263 ZAR cents.

Further details will be provided in the consolidated provisional annual results, due to be released on SENS on 18 June 2019. The financial information on which this trading statement is based has not been reviewed and reported on by the Company´s external auditor.

End SENS

Financial results of MultiChoice (MCG)

- Revenue: R50.095 billion (up 6% from R47.452 billion in previous period)

- Cost of providing services and sales of goods: R29.203 billion (up % from 27.588 billion in previous period)

- Operating profit: R7.363 billion (up from R6.381 billion in previous period)

- Profit before taxation: R2.497 billion (down from R6.247 billion in the previous year). Due to empowerment transaction expenses and foreign exchange losses as mentioned in the SENS above)

- Profit/Loss for the period: -R1.276 billion (from a profit of R2.538 billion in the previous period)

- Headline loss per share came in at: -R3.53 a share (and not at around R8 as expected). Perhaps the reason the share price has held up so well recently

- Number of shares in issue: 439 million

- Market Capital: R58.387 billion

- Cash and equivalents: R6.723 billion (or R15.31 a share)

- Cash as a percentage of share price: 11.51%

- Net asset value (NAV): R22.31

- Tobin's Q: 1.42 (a value of 1 shows the market capital is equal to the value of the company's total assets. Values above 1 shows that the market capital of the group is more than the total value of the company's assets)

Management commentary on MultiChoice (MCG) results

A total of 1.6m subscribers were added across the continent, representing 12% year-on-year (YoY) growth, taking the overall active subscriber base to 15.1m subscribers. This was achieved despite continued macroeconomic headwinds and consumer affordability pressure, illustrating the resilience of our products. The year also marks the first time that the Rest of Africa (RoA) base of 7.7m subscribers exceeded the 7.4m subscribers in South Africa.

The group generated revenue of R50.1bn, up 6% on last year (6% organic). Subscription revenue amounted to R41.2bn, up 7% on last year (8% organic). This represents an acceleration in growth from previous years driven by the continued success of our value strategy in the RoA and a healthy contribution from South Africa. Group trading profit rose 11% to R7bn (27% organic) benefiting from a R0.9bn reduction in losses in RoA. As part of the group’s cost optimisation programme, a further R1.3bn in costs were removed from the base during the year. This resulted in overall costs being contained to an increase of 5% (2% organic) and achieved the group target of keeping the rate of growth in costs below the rate of growth in revenue. The group continued its investment in local content adding a further 4 600 hours to take the local content library to nearly 50 000 hours. The spend on local general entertainment content as a percentage of total general entertainment content increased from 38% to 40%, in line with the strategy to reach a target of 45%. Core headline earnings, the board’s measure of sustainable business performance, was up 10% on last year at R1.8bn.

Consolidated free cash flow of R3.3bn was up 96% compared to the prior year. This was achieved after an improvement in the trading result from the RoA, the non-recurrence of once-off content prepayments in the prior year and remittances of cash from Angola. Capital expenditure of R1bn was slightly up YoY due to additional investments in information technology infrastructure to improve customer experience as well as the renewal of our digital terrestrial television (DTT) licence in Nigeria. The cash conversion ratio (EBITDA-Capex/EBITDA) remains positive at 90%. As one of the largest taxpayers in Africa, MCG paid direct cash taxes of R3.7bn, in line with the previous year. Net interest paid amounted to R305m, an increase of R152m from the previous year. This was due to an increase in the interest bearing loan funding received from Naspers in the RoA segment which was capitalised as part of the unbundling

The group balance sheet is strong with R9.8bn in net assets, including R6.7bn of cash and cash equivalents and R3.5bn in undrawn facilities providing R10.2bn in financial flexibility to fund our business plan.

Segmental review

South Africa

The South African business delivered subscriber growth of 8% YoY or 0.5m subscribers and generated revenues of R33.7bn, up 3% (4% organic) from the prior year. This was on the back of healthy subscriber growth in the mass market and despite absorbing a 1% increase in value added tax by not passing it on to customers. The Premium segment remained under pressure as consumers were impacted by rising fuel and other costs and we competed for share of wallet. ARPU declined from R335 to R322 due to the ongoing change in subscriber mix towards the mass market. Trading profit was in line with the prior year at R10.2bn, while the trading margin remained relatively stable at 30%. The segment continued to drive product enhancements by expanding the content offering in some of its bouquets and adding JOOX, a music streaming service, to its platform. Sustained efforts to grow the digital offering through Connected Video and position the business for the future, saw good uptake of both the Showmax and DStv Now services. As a result, online subscribers doubled YoY.

Rest of Africa

The Rest of Africa (RoA) business continued to build on the success of its value strategy by growing the subscriber base 17% YoY or 1.1m subscribers. The Fifa World Cup resonated extremely positively with our customers and we used the event to drive uptake of our products on both the satellite and digital terrestrial platforms. The strong subscriber growth translated into revenue growth of 13% (13% organic) to R14.8bn, while trading losses reduced 19% (41% organic) or R0.9bn (R1.9bn organic) to R3.7bn. Encouragingly, average revenue per user (ARPU) in the RoA has stabilised at R159 (FY2018: R160). This is despite the macroeconomic environment that remained challenging with material currency depreciation in the Angolan kwanza (60%), Zambian kwacha (17%) and the Ghanaian cedi (11%). To solidify our position in the Angolan market, we converted the Angolan operation from an agency to a subsidiary, which has been fully consolidated, from 1 February 2019. Cash balances and trade receivables of R298m held in Angola and Zimbabwe that remain exposed to weakening currencies, have reduced 80% compared to last year’s balance. Liquidity constraints in Angola improved considerably in FY2019, leaving a closing cash position of R168m as at 31 March 2019.

Technology segment

The Technology segment delivered steady results and contributed R1.6bn in revenues and R0.6bn in trading profit. Despite the impact of non-recurring projects, which generated revenues in the prior year, tight cost controls resulted in trading profits increasing 18% (21% organic) YoY.

Irdeto had some key customer wins in FY2019, including Tata Sky and Bharti Airtel in India. It continues to invest in connected industries, a market which is showing great promise, and that should start contributing more meaningfully to group revenues in the medium term.

Empowerment transaction

The group remains fully committed to broad-based black economic empowerment and transformation. To reinforce this, on 4 March 2019, the date of the group unbundling from Naspers Limited, the group allocated, for no consideration, an additional 5% stake in the MultiChoice South Africa group to Phuthuma Nathi, our black economic empowerment scheme. The value of this 5% has been calculated at R1.9bn, after the impact of the non-controlling interest, which has an adverse impact on earnings and headline earnings per share of 438 SA cents.

Prospects

In the year ahead, the group will continue scaling its video-entertainment services across the continent, mainly in the middle and mass markets. Top-line volume growth combined with inflationary price increases and a focus on cost containment is expected to deliver a continued reduction in trading losses in the RoA and stable margins in South Africa and the Technology segment. Innovation is core to our future, and we will continue to drive the adoption of online products (particularly in South Africa).

Dividend

As set out in the pre-listing statement no dividend is being declared for FY2019. The group remains on track to declare a dividend of R2.5bn, or 569 SA cents per share, for FY2020. This puts the group on a forward dividend yield of 4.2%

The group generated revenue of R50.1bn, up 6% on last year (6% organic). Subscription revenue amounted to R41.2bn, up 7% on last year (8% organic). This represents an acceleration in growth from previous years driven by the continued success of our value strategy in the RoA and a healthy contribution from South Africa. Group trading profit rose 11% to R7bn (27% organic) benefiting from a R0.9bn reduction in losses in RoA. As part of the group’s cost optimisation programme, a further R1.3bn in costs were removed from the base during the year. This resulted in overall costs being contained to an increase of 5% (2% organic) and achieved the group target of keeping the rate of growth in costs below the rate of growth in revenue. The group continued its investment in local content adding a further 4 600 hours to take the local content library to nearly 50 000 hours. The spend on local general entertainment content as a percentage of total general entertainment content increased from 38% to 40%, in line with the strategy to reach a target of 45%. Core headline earnings, the board’s measure of sustainable business performance, was up 10% on last year at R1.8bn.

Consolidated free cash flow of R3.3bn was up 96% compared to the prior year. This was achieved after an improvement in the trading result from the RoA, the non-recurrence of once-off content prepayments in the prior year and remittances of cash from Angola. Capital expenditure of R1bn was slightly up YoY due to additional investments in information technology infrastructure to improve customer experience as well as the renewal of our digital terrestrial television (DTT) licence in Nigeria. The cash conversion ratio (EBITDA-Capex/EBITDA) remains positive at 90%. As one of the largest taxpayers in Africa, MCG paid direct cash taxes of R3.7bn, in line with the previous year. Net interest paid amounted to R305m, an increase of R152m from the previous year. This was due to an increase in the interest bearing loan funding received from Naspers in the RoA segment which was capitalised as part of the unbundling

The group balance sheet is strong with R9.8bn in net assets, including R6.7bn of cash and cash equivalents and R3.5bn in undrawn facilities providing R10.2bn in financial flexibility to fund our business plan.

Segmental review

South Africa

The South African business delivered subscriber growth of 8% YoY or 0.5m subscribers and generated revenues of R33.7bn, up 3% (4% organic) from the prior year. This was on the back of healthy subscriber growth in the mass market and despite absorbing a 1% increase in value added tax by not passing it on to customers. The Premium segment remained under pressure as consumers were impacted by rising fuel and other costs and we competed for share of wallet. ARPU declined from R335 to R322 due to the ongoing change in subscriber mix towards the mass market. Trading profit was in line with the prior year at R10.2bn, while the trading margin remained relatively stable at 30%. The segment continued to drive product enhancements by expanding the content offering in some of its bouquets and adding JOOX, a music streaming service, to its platform. Sustained efforts to grow the digital offering through Connected Video and position the business for the future, saw good uptake of both the Showmax and DStv Now services. As a result, online subscribers doubled YoY.

Rest of Africa

The Rest of Africa (RoA) business continued to build on the success of its value strategy by growing the subscriber base 17% YoY or 1.1m subscribers. The Fifa World Cup resonated extremely positively with our customers and we used the event to drive uptake of our products on both the satellite and digital terrestrial platforms. The strong subscriber growth translated into revenue growth of 13% (13% organic) to R14.8bn, while trading losses reduced 19% (41% organic) or R0.9bn (R1.9bn organic) to R3.7bn. Encouragingly, average revenue per user (ARPU) in the RoA has stabilised at R159 (FY2018: R160). This is despite the macroeconomic environment that remained challenging with material currency depreciation in the Angolan kwanza (60%), Zambian kwacha (17%) and the Ghanaian cedi (11%). To solidify our position in the Angolan market, we converted the Angolan operation from an agency to a subsidiary, which has been fully consolidated, from 1 February 2019. Cash balances and trade receivables of R298m held in Angola and Zimbabwe that remain exposed to weakening currencies, have reduced 80% compared to last year’s balance. Liquidity constraints in Angola improved considerably in FY2019, leaving a closing cash position of R168m as at 31 March 2019.

Technology segment

The Technology segment delivered steady results and contributed R1.6bn in revenues and R0.6bn in trading profit. Despite the impact of non-recurring projects, which generated revenues in the prior year, tight cost controls resulted in trading profits increasing 18% (21% organic) YoY.

Irdeto had some key customer wins in FY2019, including Tata Sky and Bharti Airtel in India. It continues to invest in connected industries, a market which is showing great promise, and that should start contributing more meaningfully to group revenues in the medium term.

Empowerment transaction

The group remains fully committed to broad-based black economic empowerment and transformation. To reinforce this, on 4 March 2019, the date of the group unbundling from Naspers Limited, the group allocated, for no consideration, an additional 5% stake in the MultiChoice South Africa group to Phuthuma Nathi, our black economic empowerment scheme. The value of this 5% has been calculated at R1.9bn, after the impact of the non-controlling interest, which has an adverse impact on earnings and headline earnings per share of 438 SA cents.

Prospects

In the year ahead, the group will continue scaling its video-entertainment services across the continent, mainly in the middle and mass markets. Top-line volume growth combined with inflationary price increases and a focus on cost containment is expected to deliver a continued reduction in trading losses in the RoA and stable margins in South Africa and the Technology segment. Innovation is core to our future, and we will continue to drive the adoption of online products (particularly in South Africa).

Dividend

As set out in the pre-listing statement no dividend is being declared for FY2019. The group remains on track to declare a dividend of R2.5bn, or 569 SA cents per share, for FY2020. This puts the group on a forward dividend yield of 4.2%

Should you buy MultiChoice shares?

Well you might be wondering why buy a share when they made a loss. In the group's defence if you strip out the exchange rate losses and the empowerment transaction fees the group would have made a profit of R2.78 billion (or earnings per share of R6.33 a share), which would place the group on PE ratio of 21 and a forward dividend yield of 4.2%. While the PE is well above the market average PE ratio the dividend yield is fairly strong. And as we mentioned in an earlier update on MultiChoice group three big asset management firms in South Africa owns over 20% of the group alone. They are:

- Allan Gray: 10%

- Prudential Asset Management: 5.37%

- Coronation: 5.1%

MultiChoice (MCG) stock valuation

So looking past the loss they made in this financial year and focusing on their future and prospects and the underlying results after removing the exchange rate losses and the empowerment transaction cost, what are MultiChoice shares actually worth? Looking at their strong balance sheet and expected dividends to be paid in future, we value the shares at R111.30 a share. We therefore feel the shares are overvalued and we don't share the sentiment and love that some of South Africa's biggest asset managers have for MultiChoice. We just believe that their future is riddled with difficulties from a more ever connected and streamed world. We took this opinion of ours into account when valuing their future cash flows as we believe it will not grow at a particularly fast rate in the next few years and this has affected our valuation. At our current valuation the group will trade at a forward PE of 17.6 (which is more inline with the overall All Share PE ratio and a forward dividend yield of 4.7%. We therefore feel R111.30 is a fair valuation for MultiChoice shares.