|

Related Topics |

|

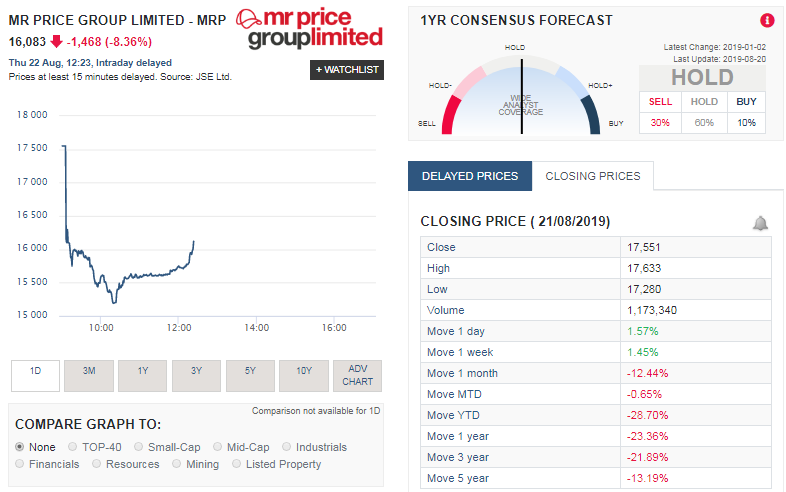

We take a look at the latest trading update from Mr Price and from the looks of it the group is really struggling in South Africa. And Mr Market is punishing the group's share with it being down almost 9% for the trading day so far.

|

|

Background and overview of Mr Price Group (MRP)

Mr Price group is a retailer active in the fashion and clothing segment of the market. The retail in apparel, homeware and sportswear and is one of the fastest growing retailers in South Africa. Mr Price's cash sales constitute 82.6% of total sales and the group is focused on remaining a cash-driven retailer. This will continue to differentiate the group from its competitors and produce cash flows that will fund our continued growth and enable an attractive dividend cover.

Their brands include:

Mr Price

Mr Price Sports

Mr Price Home

Sheet Street

Milady's

Mr Price has a very strong foothold in the South African retail clothing market, and this offers a strong value investing proposition for us.

Their brands include:

Mr Price

Mr Price Sports

Mr Price Home

Sheet Street

Milady's

Mr Price has a very strong foothold in the South African retail clothing market, and this offers a strong value investing proposition for us.

Advertisement (and yes South Africans can buy from Amazon as they ship to SA)

Trading update released on 22 August 2019

During the first four months (18 weeks to 3 August 2019)(the "Period") of the financial year ending 28 March 2020, the group recorded growth in retail sales and other income of 1.1% to R7.5bn over the corresponding period in the prior year ("Corresponding Period"). Total retail sales, including sales to franchisees, of R6.9bn were 0.5% higher than the Corresponding Period, while growths in corporate owned stores were as follows:

Apparel Segment Retail Sales Comparable store sales Units RSP Inflation

Mr Price -2.1% -5.3% -1.6% -0.6%

Mr Price Sport 9.3% 5.9% 4.0% 5.0%

Miladys 3.4% -1.2% 2.1% 1.7%

Total for apparel segment -0.5% -3.9% -1.0% 0.5%

Home Segment Retail Sales Comparable store sales Units RSP Inflation

Mr Price Home 3.2% 1.7% -4.4% 8.0%

Sheet Street 5.4% 2.9% -5.4% 11.4%

Total for Home segment 3.9% 2.1% -4.8% 9.1%

Total for the group Retail Sales Comparable store sales Units RSP Inflation

Group 0.6% -2.5% -1.9% 2.5%

It was communicated at the annual results presentation in May, that the first half of FY2020 was expected to be an extremely challenging trading period.

The continued poor retail environment, and a generally strong performance in the base relative to the rest of the market per Stats SA, contributed to the performance in the Period. In addition, internal factors had an impact and are outlined below. Consumers continue to be constrained, which is affecting propensity to spend. GDP growth, unemployment, inflation and disposable income remain at levels that are not supportive of growth in the retail environment. The corporate store sales performance detailed above reflect some of the external challenges. Despite these factors, group sales excluding Mr Price Apparel were up 4.8%, with these divisions maintaining or improving gross margin percentage. South African retail sales increased 0.6% to R6.4bn. Store sales were up 0.2% and online sales up 31.1% to R109.1m.

The Mr Price Apparel online channel achieved sales growth of 21.8%, Mr Price Home 40.8% and Mr Price Sport 31.3%. Sales in non-South African corporate owned stores grew 0.3% to R522.3m. Group cash sales increased 1.4%, constituting 83.6% (Corresponding Period: 82.9%) of total sales and credit sales decreased 3.5%. The credit environment continues to be weak as indicated by Transunion in their Q2 2019 Consumer Credit Index report and the group does not believe it is currently appropriate to stimulate growth in this channel. New store openings and expansions resulted in weighted average trading space increasing 3.0%. Ongoing strategic space rationalisation resulted in net weighted average trading space increasing 1.5%. Other income grew 9.4%, to R502.7m. Debtors' interest and fees grew 7.2% to R171.6m. The recent repo rate cut of 25bps will adversely affect interest income for the remainder of the financial year. Insurance revenue of R81.1m decreased 5.2% and cellular and mobile revenue increased 19.4% to R234.6m.

The most significant challenges were faced in Mr Price Apparel, which constitutes 59.5% of group sales. The core elements of our business model and past success, being category dominance and clarity of offer, were compromised by an imbalance in the shape of the assortment. These same issues were present in H2 of the prior financial period and caused excess inventory carry into winter. Higher than desired markdowns were required over the short winter period, diverting customer spend away from full-price merchandise and materially impacting gross margin. The new executive management team has devoted significant time to undertake detailed merchandise process reviews across the business with emphasis on Mr Price Apparel.

Clarity on where corrective action was required has been achieved and remedial action has been taken. As communicated in May, it was not anticipated that the effect of these initiatives would impact winter trading, but they are expected to positively influence performance leading into H2. Group winter inventory was cleared to acceptable levels by the end of the Period. Early signs of a performance recovery into spring and summer have started to emerge. Group retail sales in the last two weeks of the Period grew 3.6% (Mr Price Apparel +0.3%) and in the two weeks after the Period to 17 August grew 6.9%(Mr Price Apparel +4.3%) against a strong performance in the Corresponding Period. Looking ahead, the trading environment is expected to be challenging as global markets remain uncertain and local economic growth is forecast to be muted in 2019.

Despite this, management is optimistic that an extremely talented group of associates, re- focused on entrenching proven disciplines and providing customers with exceptional value, should deliver market share gains, whatever the economic environment. The above-mentioned figures and information contained herein do not constitute an earnings forecast and have not been reviewed and reported on by the company's external auditors.

Durban 22 August 2019

Apparel Segment Retail Sales Comparable store sales Units RSP Inflation

Mr Price -2.1% -5.3% -1.6% -0.6%

Mr Price Sport 9.3% 5.9% 4.0% 5.0%

Miladys 3.4% -1.2% 2.1% 1.7%

Total for apparel segment -0.5% -3.9% -1.0% 0.5%

Home Segment Retail Sales Comparable store sales Units RSP Inflation

Mr Price Home 3.2% 1.7% -4.4% 8.0%

Sheet Street 5.4% 2.9% -5.4% 11.4%

Total for Home segment 3.9% 2.1% -4.8% 9.1%

Total for the group Retail Sales Comparable store sales Units RSP Inflation

Group 0.6% -2.5% -1.9% 2.5%

It was communicated at the annual results presentation in May, that the first half of FY2020 was expected to be an extremely challenging trading period.

The continued poor retail environment, and a generally strong performance in the base relative to the rest of the market per Stats SA, contributed to the performance in the Period. In addition, internal factors had an impact and are outlined below. Consumers continue to be constrained, which is affecting propensity to spend. GDP growth, unemployment, inflation and disposable income remain at levels that are not supportive of growth in the retail environment. The corporate store sales performance detailed above reflect some of the external challenges. Despite these factors, group sales excluding Mr Price Apparel were up 4.8%, with these divisions maintaining or improving gross margin percentage. South African retail sales increased 0.6% to R6.4bn. Store sales were up 0.2% and online sales up 31.1% to R109.1m.

The Mr Price Apparel online channel achieved sales growth of 21.8%, Mr Price Home 40.8% and Mr Price Sport 31.3%. Sales in non-South African corporate owned stores grew 0.3% to R522.3m. Group cash sales increased 1.4%, constituting 83.6% (Corresponding Period: 82.9%) of total sales and credit sales decreased 3.5%. The credit environment continues to be weak as indicated by Transunion in their Q2 2019 Consumer Credit Index report and the group does not believe it is currently appropriate to stimulate growth in this channel. New store openings and expansions resulted in weighted average trading space increasing 3.0%. Ongoing strategic space rationalisation resulted in net weighted average trading space increasing 1.5%. Other income grew 9.4%, to R502.7m. Debtors' interest and fees grew 7.2% to R171.6m. The recent repo rate cut of 25bps will adversely affect interest income for the remainder of the financial year. Insurance revenue of R81.1m decreased 5.2% and cellular and mobile revenue increased 19.4% to R234.6m.

The most significant challenges were faced in Mr Price Apparel, which constitutes 59.5% of group sales. The core elements of our business model and past success, being category dominance and clarity of offer, were compromised by an imbalance in the shape of the assortment. These same issues were present in H2 of the prior financial period and caused excess inventory carry into winter. Higher than desired markdowns were required over the short winter period, diverting customer spend away from full-price merchandise and materially impacting gross margin. The new executive management team has devoted significant time to undertake detailed merchandise process reviews across the business with emphasis on Mr Price Apparel.

Clarity on where corrective action was required has been achieved and remedial action has been taken. As communicated in May, it was not anticipated that the effect of these initiatives would impact winter trading, but they are expected to positively influence performance leading into H2. Group winter inventory was cleared to acceptable levels by the end of the Period. Early signs of a performance recovery into spring and summer have started to emerge. Group retail sales in the last two weeks of the Period grew 3.6% (Mr Price Apparel +0.3%) and in the two weeks after the Period to 17 August grew 6.9%(Mr Price Apparel +4.3%) against a strong performance in the Corresponding Period. Looking ahead, the trading environment is expected to be challenging as global markets remain uncertain and local economic growth is forecast to be muted in 2019.

Despite this, management is optimistic that an extremely talented group of associates, re- focused on entrenching proven disciplines and providing customers with exceptional value, should deliver market share gains, whatever the economic environment. The above-mentioned figures and information contained herein do not constitute an earnings forecast and have not been reviewed and reported on by the company's external auditors.

Durban 22 August 2019

Mr Price Share Price history

The image below, taken from Sharenet shows the MRP share price history for the last 5 years, and as the chart shows, MRP has been moving largely sideways over the last 5 years,with little share price gains to show over the period. It's share price reflective of the tough operating environment it finds itself in.

MRP share price history

The summary below shows the share price performance of the group over different periods of time:

- 1 week: 1.45%

- 1 month: -12.44%

- Year to date (YTD): -28.7%

- 1 year: -23.36%

- 3 years: -21.89%

- 5 years: -13.19%

Mr Price (MRP) share valuation as at June 2019

So based on MRP's latest financial results, is it a good time to buy there shares? Or did the massive jump in the share price on Friday take away any potential gains for investors looking to buy undervalued quality stocks? While the numbers reported were good, one has to remember it is coming off a lower base, and that the South African economy is growing very slowly and the competition in the sectors they operate in is very tough. The group's inventories increased sharply, possibly due to new stock coming in before change of seasons, or the more sinister answer could be the group is struggling to move stock so inventories are building up?

Based on their current financial results, their profit margins, their revenue growth, their strong balance sheet and cash generating capacity we value the group's shares at R203.60 a share. So at their current price we feel that Mr Price shares are close to being fully valued

Based on their current financial results, their profit margins, their revenue growth, their strong balance sheet and cash generating capacity we value the group's shares at R203.60 a share. So at their current price we feel that Mr Price shares are close to being fully valued