|

Related Topics |

|

We take a look at the latest set of financial results from South African clothing retail giant, Mr Price Group. And based on the share share price increase on Friday, the markets liked the results a lot.

|

|

Background and overview of Mr Price Group (MRP)

Mr Price group is a retailer active in the fashion and clothing segment of the market. The retail in apparel, homeware and sportswear and is one of the fastest growing retailers in South Africa. Mr Price's cash sales constitute 82.6% of total sales and the group is focused on remaining a cash-driven retailer. This will continue to differentiate the group from its competitors and produce cash flows that will fund our continued growth and enable an attractive dividend cover.

Their brands include:

Mr Price

Mr Price Sports

Mr Price Home

Sheet Street

Milady's

Mr Price has a very strong foothold in the South African retail clothing market, and this offers a strong value investing proposition for us.

Their brands include:

Mr Price

Mr Price Sports

Mr Price Home

Sheet Street

Milady's

Mr Price has a very strong foothold in the South African retail clothing market, and this offers a strong value investing proposition for us.

Financial review

Management commentary on the results

“We are pleased to be able to deliver solid earnings growth and increase our dividend to shareholders in what has been a very tough year for retail. Despite this, both our apparel and homeware segments outperformed the market and gained market share on an annual basis. For the first time our retail sales exceeded R20bn and profit before tax R4bn,” said CEO Mark Blair.

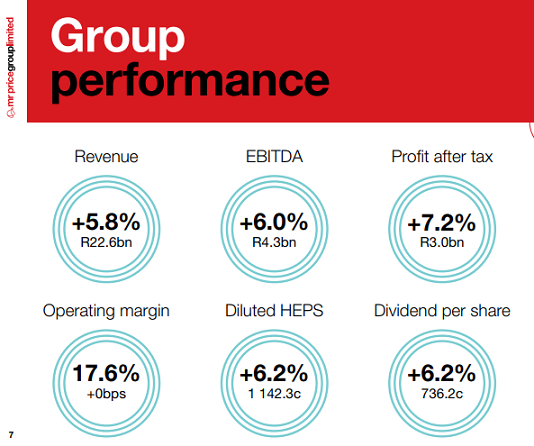

Total revenue grew 5.8% to R22.6bn with retail sales increasing by 4.4% (comparable stores 1.6%) to R20.9bn. Other income grew 24.7% to R1.5bn, mainly from financial services and cellular. Interest earned on cash balances grew by 38.2% to R224m. Cash sales grew by 6.6% and constitute 84.2% of total sales, whilst credit sales including cellular increased by 2.3%. Local store sales were up 3.8% while non-South African store sales grew 12.1%, aided by the acquisition of the Kenyan franchise stores in May 2018.

Retail selling price inflation was 5.1% and 220m units were sold, an increase of 0.2%. By opening 82 new stores and expanding 11, weighted average new space grew 3.1%. After closing 17 stores and reducing the size of 30, total weighted average space was up 1.4%, taking the total number of corporate owned stores to 1 323. The group continues to focus on optimising trading space with trading densities up 3.0%. The group’s gross profit margin declined by 40bps to 42.9%.

All divisions grew merchandise margins except for MRP Apparel whose Q4 markdowns offset prior gains. Merchandise margins on an annual basis contracted 10bps to 43.6%. Cellular margins decreased 150bps to 19.1% due to product mix changes as Cellular kiosks, which are lower margin than MRP Mobile, were rolled out to over 200 stores. Selling and administration expenses were well managed, increasing by 4.0% (excluding Kenya and Poland 2.8%). Profit from operating activities increased by 5.5% to R3.9bn and the operating margin remained flat at 17.6% of retail sales and other income (RSOI).

Basic earnings per share increased by 7.0% to 1 156.6 cents. The Apparel segment increased RSOI by 3.8% to R15.6bn. Operating profit increased 3.4% off a strong base and the operating margin declined marginally from 18.1% to 18.0%. Sales in MRP Apparel grew 3.1% (comparable 0.1%) to R12.6bn, and exceeded market growth as reported by Stats SA (Type D) on an annual basis. Online sales grew at 30.2%, with 25.1m visits to mrp.com throughout the year. Miladys grew sales 4.0% (comparable 3.1%). MRP Sport reported strong sales growth of 9.7% (comparable 6.4%), with online sales growing at 43.8%. Despite discretionary spend product being under pressure due to economic challenges, the Home segment performed well, increasing RSOI by 5.9% to R5.3bn.

Operating profit increased 12.3% and the operating margin increased from 15.7% to 16.6%. Both divisions grew market share, outperforming the market on an annual basis as reported by Stats SA (Type D). Sales in MRP Home were up 7.2% (comparable 4.5%) with online sales increasing 34.8%. Sheet Street grew sales by 4.0% (comparable 1.6%). The Financial Services & Cellular segment reported revenue growth of 25.9% to R1.4bn and an operating profit decline of 1.3%. Financial services grew revenue 4.9% to R760m.

A weak credit environment, a lower effective repo rate and a change to IFRS 9 caused growth in interest and fees to slow. The industry has shown a rising number of new accounts in early default. In line with the group’s prudent approach to credit, scorecard adjustments were made. The effect of this was less accounts approved despite growing new account applications. Cellular and mobile revenue grew 62.1% to R677m with Cellular products sold through 216 locations across the group, achieving sales density and operating profit per square metre in line with the other merchandise. The balance sheet remains in a healthy position.

Cash and cash equivalents increased 15.8% to R3.2bn. Net asset value per share increased 16.2% to 3 345 cents. The group’s ROA and ROE were 26.8% and 37.5% respectively, significantly higher than the JSE Top 40 and retail competitors average. Solvency and liquidity ratios remain market leading. Capital expenditure of R424m was incurred primarily relating to store development activities. Inventory levels were up 18.9% due to an increase in goods in transit (GIT) to satisfy the timing of winter merchandise. Excluding GIT, inventory was up 14.2%. Excess stock due to lower than expected trade since the festive period will require promotional activity in the new year. The debtors book remains well managed, with a retail net bad debt to book ratio of 7.3% and an IFRS 9 impairment provision of 8.9%.

The appointment of Mark Blair as CEO effective 1 January 2019, came with him making a few key appointments including newly formed roles of Chief Operating Officer and Chief Retail Officer. The new management team has identified potential opportunities for growth across the business and prioritised key areas of focus which will form part of the process of updating the group strategy. High cash generation, a low cost operating model and strengthening the key fashion-value product offering at everyday low prices will continue to remain central to the business model. The group expects to open 70 new stores in FY2020.

Total revenue grew 5.8% to R22.6bn with retail sales increasing by 4.4% (comparable stores 1.6%) to R20.9bn. Other income grew 24.7% to R1.5bn, mainly from financial services and cellular. Interest earned on cash balances grew by 38.2% to R224m. Cash sales grew by 6.6% and constitute 84.2% of total sales, whilst credit sales including cellular increased by 2.3%. Local store sales were up 3.8% while non-South African store sales grew 12.1%, aided by the acquisition of the Kenyan franchise stores in May 2018.

Retail selling price inflation was 5.1% and 220m units were sold, an increase of 0.2%. By opening 82 new stores and expanding 11, weighted average new space grew 3.1%. After closing 17 stores and reducing the size of 30, total weighted average space was up 1.4%, taking the total number of corporate owned stores to 1 323. The group continues to focus on optimising trading space with trading densities up 3.0%. The group’s gross profit margin declined by 40bps to 42.9%.

All divisions grew merchandise margins except for MRP Apparel whose Q4 markdowns offset prior gains. Merchandise margins on an annual basis contracted 10bps to 43.6%. Cellular margins decreased 150bps to 19.1% due to product mix changes as Cellular kiosks, which are lower margin than MRP Mobile, were rolled out to over 200 stores. Selling and administration expenses were well managed, increasing by 4.0% (excluding Kenya and Poland 2.8%). Profit from operating activities increased by 5.5% to R3.9bn and the operating margin remained flat at 17.6% of retail sales and other income (RSOI).

Basic earnings per share increased by 7.0% to 1 156.6 cents. The Apparel segment increased RSOI by 3.8% to R15.6bn. Operating profit increased 3.4% off a strong base and the operating margin declined marginally from 18.1% to 18.0%. Sales in MRP Apparel grew 3.1% (comparable 0.1%) to R12.6bn, and exceeded market growth as reported by Stats SA (Type D) on an annual basis. Online sales grew at 30.2%, with 25.1m visits to mrp.com throughout the year. Miladys grew sales 4.0% (comparable 3.1%). MRP Sport reported strong sales growth of 9.7% (comparable 6.4%), with online sales growing at 43.8%. Despite discretionary spend product being under pressure due to economic challenges, the Home segment performed well, increasing RSOI by 5.9% to R5.3bn.

Operating profit increased 12.3% and the operating margin increased from 15.7% to 16.6%. Both divisions grew market share, outperforming the market on an annual basis as reported by Stats SA (Type D). Sales in MRP Home were up 7.2% (comparable 4.5%) with online sales increasing 34.8%. Sheet Street grew sales by 4.0% (comparable 1.6%). The Financial Services & Cellular segment reported revenue growth of 25.9% to R1.4bn and an operating profit decline of 1.3%. Financial services grew revenue 4.9% to R760m.

A weak credit environment, a lower effective repo rate and a change to IFRS 9 caused growth in interest and fees to slow. The industry has shown a rising number of new accounts in early default. In line with the group’s prudent approach to credit, scorecard adjustments were made. The effect of this was less accounts approved despite growing new account applications. Cellular and mobile revenue grew 62.1% to R677m with Cellular products sold through 216 locations across the group, achieving sales density and operating profit per square metre in line with the other merchandise. The balance sheet remains in a healthy position.

Cash and cash equivalents increased 15.8% to R3.2bn. Net asset value per share increased 16.2% to 3 345 cents. The group’s ROA and ROE were 26.8% and 37.5% respectively, significantly higher than the JSE Top 40 and retail competitors average. Solvency and liquidity ratios remain market leading. Capital expenditure of R424m was incurred primarily relating to store development activities. Inventory levels were up 18.9% due to an increase in goods in transit (GIT) to satisfy the timing of winter merchandise. Excluding GIT, inventory was up 14.2%. Excess stock due to lower than expected trade since the festive period will require promotional activity in the new year. The debtors book remains well managed, with a retail net bad debt to book ratio of 7.3% and an IFRS 9 impairment provision of 8.9%.

The appointment of Mark Blair as CEO effective 1 January 2019, came with him making a few key appointments including newly formed roles of Chief Operating Officer and Chief Retail Officer. The new management team has identified potential opportunities for growth across the business and prioritised key areas of focus which will form part of the process of updating the group strategy. High cash generation, a low cost operating model and strengthening the key fashion-value product offering at everyday low prices will continue to remain central to the business model. The group expects to open 70 new stores in FY2020.

Financial highlights

- Revenue: R22.6 billion (up 5.8%)

- Profit after tax: R3 billion (up 7.2%)

- Operating margin: 17.6%

- Headline Earnings per share (HEPS): R11.68

- Diluted Headline Earnings per Share: (DHEPS): R11.42

- PE ratio: 17.25 (close to the overall market average PE ratio)

- Dividend per share: R7.36

- Dividend yield: 3.7%

- Cash and equivilents: R3.15 billion (or R12.20 per share). Thus cash makes up 6.2% of the company's share price

- Cash generated per share: R11 a share

- Net asset value: R33.45

- Tobin's Q: 4.55

- Inventories: R2.692 billion (up R477 million).

- Trade and other receivables: R2.179 billion

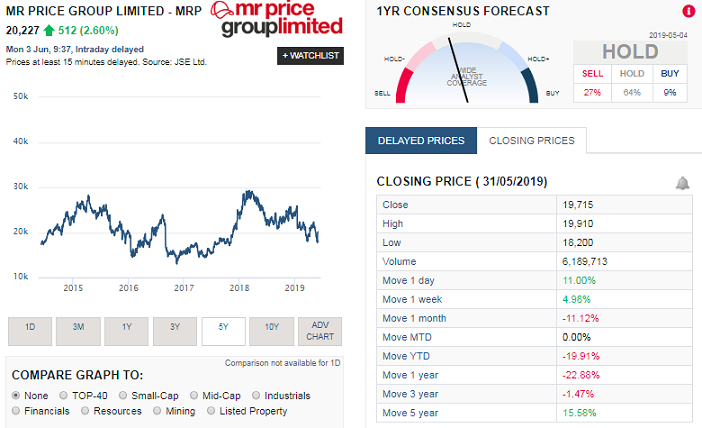

Mr Price Share Price history

The image below, taken from Sharenet shows the MRP share price history for the last 5 years, and as the chart shows, MRP has been moving largely sideways over the last 5 years,with little share price gains to show over the period. It's share price reflective of the tough operating environment it finds itself in.

MRP share price history

The summary below shows the share price performance of the group over different periods of time:

- 1 week: 4.96%

- 1 month: -11.12%

- Year to date (YTD): -19.91%

- 1 year: -22.88%

- 3 years: -1.47%

- 5 years: 15.58%

Outlook

Mr Price group had the following to say regarding their outlook for the current period.

"The retail environment in South Africa is likely to remain under pressure in the short term as flat real wage growth and low levels of disposable income continue to challenge the consumers’ ability to spend. The national elections delivered a positive outcome which we hope will lead to reformed economic policies that will encourage business growth and job creation. Blair commented “Hopefully this could be the start of an upward swing in the retail cycle, but any improvements are expected to be gradual and we are therefore anticipating a very tough first half of the new financial year. The second half should see an improvement due to the base effect and impact of internal initiatives coming through. Increased focus is being applied to our key differentiators to ensure that we continue to gain market share and deliver above market related returns for our shareholders.”

"The retail environment in South Africa is likely to remain under pressure in the short term as flat real wage growth and low levels of disposable income continue to challenge the consumers’ ability to spend. The national elections delivered a positive outcome which we hope will lead to reformed economic policies that will encourage business growth and job creation. Blair commented “Hopefully this could be the start of an upward swing in the retail cycle, but any improvements are expected to be gradual and we are therefore anticipating a very tough first half of the new financial year. The second half should see an improvement due to the base effect and impact of internal initiatives coming through. Increased focus is being applied to our key differentiators to ensure that we continue to gain market share and deliver above market related returns for our shareholders.”

Mr Price (MRP) share valuation

So based on MRP's latest financial results, is it a good time to buy there shares? Or did the massive jump in the share price on Friday take away any potential gains for investors looking to buy undervalued quality stocks? While the numbers reported were good, one has to remember it is coming off a lower base, and that the South African economy is growing very slowly and the competition in the sectors they operate in is very tough. The group's inventories increased sharply, possibly due to new stock coming in before change of seasons, or the more sinister answer could be the group is struggling to move stock so inventories are building up?

Based on their current financial results, their profit margins, their revenue growth, their strong balance sheet and cash generating capacity we value the group's shares at R203.60 a share. So at their current price we feel that Mr Price shares are close to being fully valued

Based on their current financial results, their profit margins, their revenue growth, their strong balance sheet and cash generating capacity we value the group's shares at R203.60 a share. So at their current price we feel that Mr Price shares are close to being fully valued