|

|

Related Topics

|

About Italtile

Italtile limited is a leading retailer and manufacturer of tiles, bathroomware and related products. The Group operates as a national franchisor of its three high profile retail brands, Italtile Retail, CTM and TopT. The retail operations are underpinned by an extensive property portfolio and a vertically integrated supply chain comprising International Tap Distributors (an importer and distributor of brassware and accessories), and Cedar Point, (an importer of shower enclosures, laminated boards, cabinets, sanitaryware, décor and tiling tools). The Group holds controlling interests in both businesses. The Group’s Distribution Centre sources imported products and provides warehousing and distribution facilities to the retail brands. Effective 2 October 2017, the Group acquired controlling stakes in its key suppliers, tile and sanitaryware manufacturer, Ceramic Industries (Pty) Ltd and adhesives and related products manufacturer, Ezee Tile.

Woolworths East London 1948

Financial results overview

Financial results highlighted by Italtile management:

Financial results we are interested in:

- System-wide turnover: R10,0 billion 2018: R8,7 billion (Up 15%)

- Trading profit: R1 797 million 2018: R1 518 million (Up 18%)

- Earnings per share: 102,6 cents 2018: 95,0 cents (Up 8%)

- Headline earnings per share: 101,8 cents 2018: 95,0 cents (Up 7%)

- Ordinary dividend per share: 41,0 cents 2018: 38,0 cents (Up 8%)

- Special dividend per share: 50,0 cents 2018: 30,0 cents (Up 67%)

- Net cash: R1 201 million 2018: R679 million (Up 77%)

- Net asset value per share: 480 cents 2018: 486 cents (Down 1%)

- Store network: 189 2018: 176 (Up 7%)

Financial results we are interested in:

- Gross profit: R2.614 billion (up 12%)

- Net profit: R1.319 billion (up 15%)

- PE ratio: 13.4

- Dividend yield including special dividend: 6.7%

- Cash generated from operations: R2.14 billion

- Cash generated from operations per share: R1.65

- Cash on balance sheet: R1.2 billion

- Cash per share: R0.93 (or 6.9% of the group's share price)

- Price to book value: 2.81 (company trading at 2.81 times its net asset value)

- Inventories: R857 million (up 6.3% from R806 million in the previous period)

- Trade and other receivables: R850 million (down from R942 million). This is a good sign as less money is owed to them for goods and services supplied.

Advertisement (yes South Africans can buy from Amazon as they deliver to SA)

Management commentary on the results

OVERVIEW

Established 50 years ago, in 1969, Italtile Limited is a manufacturer, franchisor and retailer of tiles, bathroomware and other related home-finishing products. The Group's retail brands are CTM, Italtile Retail and TopT, represented through a total network of 189 stores, including five online webstores. The brand offering targets homeowners across the LSM 4 to 10 categories. The retail operation is strategically supported by a vertically integrated supply chain, comprising key manufacturing and import operations, and an extensive property portfolio.

IMPACT OF CERTAIN TRANSACTIONS ON THE GROUP'S RESULTS AND REPORTING REFERENCE TERMS

Comparable disclosure and analysis of the Group's results for the year ended 30 June 2019 ("review period") with the prior corresponding period have been impacted on by the acquisition of Ceramic Industries Proprietary Limited ("Ceramic") ("Acquisition") as set out in the circular to shareholders of Italtile dated 23 August 2016, which became effective on 2 October 2017 and the partially underwritten renounceable rights offer as set out in the circular to shareholders of Italtile dated 6 November 2017 ("Rights Offer"). Shareholders are referred to previous announcements in this regard. RESULTS Notwithstanding the exceptionally difficult trading conditions experienced over the past year, the Group has recorded a creditable performance, achieving our stated goal of delivering improved headline earnings growth for the review period. In line with our guidance, the results for the first half of the year were stronger than the prior comparable period, due to a low-base effect, while the performance for the second half of the year was solid, albeit as forecast, less robust than the prior comparable period.

Group performance

The results reported for the review period are a good reflection of the Group's:

- robust proudly South African 50-year trading history as the industry trendsetter and style icon;

- strategically structured resilient business model, which provides a total solution through our integrated supply chain;

- competent team with clarity of purpose and clearly defined strategies;

- mutually beneficial partnerships with longstanding franchisees and operators;

- strong cash generative nature, disciplined cash management and cost leadership;

- portfolio of market leading retail brands which are strategically positioned to cater across the demographic and income spectrum, uniquely targeting each segment and supported by a multi-channel offering (in-store, online, social and digital);

-consistent investment in the shopping experience and unwavering efforts to better execute retail excellence principles;

- leading-edge technology employed in the manufacturing operations to produce high quality fashionable products; and

- leveraging growth opportunities in the business through an unrelenting focus on the customer.

OPERATIONAL REVIEW

Most of the key performance metrics improved across the retail brands and the integrated supply chain importers, although the manufacturers did not fare as well. While our stores performed commendably in the weak trading climate, tile sales, specifically, failed to live up to our expectations. This generally softer retail demand and the overstock position of tile wholesalers and retailers in the industry impacted negatively on capacity utilisation at Ceramic's factories. Retail brands Across the brands, retail excellence disciplines improved, reflected by better in-stock levels, enhanced store and merchandise presentation, technological innovation, and better analytical reporting, resulting in an improved customer experience. CTM maintained its market share, while Italtile Retail and TopT continued to make gains in the competitive environment. In total 17 stores were opened across the portfolio during the review period and four stores were closed.

CTM

After a series of disappointing sets of results, CTM started to demonstrate signs of a turnaround, despite the brand's target market remaining under intense financial pressure. Growth was reported across sales, margins, profits and store productivity, while stock turn increased and average store inventory was reduced. This improvement is attributable to a focus on basic retail excellence principles; roll out of the new store format and revamp of older stores; the emphasis on product (cost leadership, differentiation and trendsetting fashion); a brand repositioning campaign which built meaningful equity; and prioritisation of the people pipeline and skills development. During the period, key leadership changes were implemented, including the identification of an equity partner, which should continue to positively impact on CTM's performance. Italtile Retail The brand reported pleasing growth in sales and profitability and improved average stock turn. However, some margin was sacrificed due to an import substitute strategy centred on locally manufactured product. The customer shopping experience was improved with the introduction of innovative webstore and digital initiatives; roll out of the new store format; and an extended range of large format imported tiles and local porcelain tiles. While the Commercial Projects division delivered another strong performance, post year-end there has been a noticeable slowdown in commissioning of new developments, and generally, spend in the upper end of the market has declined as consumers defer investment in the current conditions.

TopT

The brand reported another strong performance, recording double-digit like-on-like sales and profit growth. Stock turn increased and average store inventory reduced. Some margin pressure was experienced in light of cost conscious customers buying down. TopT continued to benefit from successful implementation of the business optimisation programme (BOP); roll out of new stores to underserviced markets and a growing national presence; constant range re-evaluation and responsiveness to customer demand; and introduction of a range of profile building initiatives including a mobile store (Gig Rig), a webstore, community-linked marketing campaigns, and the launch of a dedicated training centre.

U-Light

During the review period, we commenced trialling a new lighting merchandise category which was rolled out to all the TopT stores. To test the scalability and viability of the U-Light offering as a standalone brand, five pilot stores will be opened in Gauteng by the end of August 2019; the five stores will each comprise a slightly different format and target a different market segment. This start-up business will benefit from existing store locations, customer base, business partners and an effective back-office set up.

MANUFACTURERS

Ceramic Industries

The acquisition of Ceramic some 20 months ago continues to deliver the gains envisaged, among them, a stronger combined balance sheet for future expansion, and improved planning and production efficiencies, benefiting both the stores and the factories. Tiles In the South African operation, solid results reported in the first half of the review period were eroded by a weaker performance in the second six months. While market share was gained by Gryphon's large format range, generally demand across the market was sluggish, with many wholesalers and retailers overstocked. In light of slow demand, kilns were shut off at four of Ceramic's factories in the third and fourth quarter of the year; this under-utilisation of capacity impacted negatively on margins and profit for the period and will continue to remain a challenge in the short term. The Australian operation reported improved profitability for the review period, and the investment to increase capacity and product range was completed. Focus will remain on reducing costs and improving yields across the operations.

Bathroomware and baths

Both Betta Sanitaryware and Betta Baths reported an improved second six months after a difficult first half. The new warehouse facility should be completed during the next financial year which will improve capacity management and service to customers. As with the tile factories, focus will remain on reducing costs and improving yields.

Ezee Tile

In the first half of the year, the business underperformed management's expectations, delivering disappointing margins and profits. While the remedial actions implemented in the second half have addressed operational inefficiencies and resulted in an improved performance in the latter six months, the business's results for the full year are not in line with targets. Good progress was achieved in upgrading the plant in Mombasa and developing new production facilities in Lusaka and Harare. The business also succeeded in gaining market share in the paint and construction chemicals segments.

SUPPLY CHAIN:

IMPORTERS

Cedar Point Improved sales and profit growth were reported for the year. Key focus areas were range rationalisation, reducing stock levels and improving stock turn. In the year ahead, better implementation of BOP will assist in establishing optimal stockholding and facilitating sell-through. Having successfully outsourced the warehouse function, management's primary focus will henceforth be on improved buying and operational co-ordination.

International Tap Distributors (ITD)

Competition intensified in the brassware category as an increasing number of opportunistic importers entered the market. Aggressive pricing and margin pressure were a constant feature in the review period, and in order to support cash-strapped customers, ITD reduced average selling prices, which further impacted on profits. Some opportunity exists to recover margins should the exchange rate stabilise favourably. Progress was achieved in rationalising the range and enhancing the in-stock position while simultaneously reducing overall stockholding, however, there is further room for improvement in terms of balancing business critical and supplementary stock.

Durban Distribution Centre

In the weak sales environment and given the overstocked position of numerous wholesalers, sales declined marginally although profits improved, based on intensified cost management. Good progress was made on rationalising ranges and reducing stockholding. In light of currency volatility and general margin pressure experienced in the industry, the business continues to investigate new suppliers in new markets.

PROPERTY INVESTMENT

As at 30 June 2019, the portfolio's estimated market value was R3,8 billion, comprising a retail portfolio valued at R3,0 billion (2018: R2,9 billion) and a manufacturing portfolio valued at R0,8 billion (2018: R0,8 billion). During the period capital expenditure of R312 million was incurred on the retail portfolio in respect of an ongoing store upgrade programme and the acquisition of five retail properties, while R189 million was invested across the manufacturing operations on plant, warehouse and equipment upgrades.

ORDINARY CASH DIVIDEND

The Board has declared a final gross ordinary cash dividend of 19,0 cents per share (2018: 21,0 cents per share), which together with the interim gross ordinary cash dividend of 22,0 cents per share (2018: 17,0 cents per share), produces a total gross ordinary cash dividend declared for the year ended 30 June 2019 of 41,0 cents per share (2018: 38,0 cents per share), an increase of 8%. The dividend cover remains at two-and-a-half times.

SPECIAL DIVIDEND

In light of the Group's strong cash generative nature and cash reserves being in excess of operational requirements, the Board has declared a special cash dividend in celebration of 50 years, of 50,0 cents per share (2018: 30,0 cents per share). Italtile is in the process of obtaining the relevant South African Reserve Bank approval in respect of the special dividend, and the Board has reasonably concluded that the Company will satisfy the solvency and liquidity test immediately after distribution thereof and for the next 12 months.

Established 50 years ago, in 1969, Italtile Limited is a manufacturer, franchisor and retailer of tiles, bathroomware and other related home-finishing products. The Group's retail brands are CTM, Italtile Retail and TopT, represented through a total network of 189 stores, including five online webstores. The brand offering targets homeowners across the LSM 4 to 10 categories. The retail operation is strategically supported by a vertically integrated supply chain, comprising key manufacturing and import operations, and an extensive property portfolio.

IMPACT OF CERTAIN TRANSACTIONS ON THE GROUP'S RESULTS AND REPORTING REFERENCE TERMS

Comparable disclosure and analysis of the Group's results for the year ended 30 June 2019 ("review period") with the prior corresponding period have been impacted on by the acquisition of Ceramic Industries Proprietary Limited ("Ceramic") ("Acquisition") as set out in the circular to shareholders of Italtile dated 23 August 2016, which became effective on 2 October 2017 and the partially underwritten renounceable rights offer as set out in the circular to shareholders of Italtile dated 6 November 2017 ("Rights Offer"). Shareholders are referred to previous announcements in this regard. RESULTS Notwithstanding the exceptionally difficult trading conditions experienced over the past year, the Group has recorded a creditable performance, achieving our stated goal of delivering improved headline earnings growth for the review period. In line with our guidance, the results for the first half of the year were stronger than the prior comparable period, due to a low-base effect, while the performance for the second half of the year was solid, albeit as forecast, less robust than the prior comparable period.

Group performance

The results reported for the review period are a good reflection of the Group's:

- robust proudly South African 50-year trading history as the industry trendsetter and style icon;

- strategically structured resilient business model, which provides a total solution through our integrated supply chain;

- competent team with clarity of purpose and clearly defined strategies;

- mutually beneficial partnerships with longstanding franchisees and operators;

- strong cash generative nature, disciplined cash management and cost leadership;

- portfolio of market leading retail brands which are strategically positioned to cater across the demographic and income spectrum, uniquely targeting each segment and supported by a multi-channel offering (in-store, online, social and digital);

-consistent investment in the shopping experience and unwavering efforts to better execute retail excellence principles;

- leading-edge technology employed in the manufacturing operations to produce high quality fashionable products; and

- leveraging growth opportunities in the business through an unrelenting focus on the customer.

OPERATIONAL REVIEW

Most of the key performance metrics improved across the retail brands and the integrated supply chain importers, although the manufacturers did not fare as well. While our stores performed commendably in the weak trading climate, tile sales, specifically, failed to live up to our expectations. This generally softer retail demand and the overstock position of tile wholesalers and retailers in the industry impacted negatively on capacity utilisation at Ceramic's factories. Retail brands Across the brands, retail excellence disciplines improved, reflected by better in-stock levels, enhanced store and merchandise presentation, technological innovation, and better analytical reporting, resulting in an improved customer experience. CTM maintained its market share, while Italtile Retail and TopT continued to make gains in the competitive environment. In total 17 stores were opened across the portfolio during the review period and four stores were closed.

CTM

After a series of disappointing sets of results, CTM started to demonstrate signs of a turnaround, despite the brand's target market remaining under intense financial pressure. Growth was reported across sales, margins, profits and store productivity, while stock turn increased and average store inventory was reduced. This improvement is attributable to a focus on basic retail excellence principles; roll out of the new store format and revamp of older stores; the emphasis on product (cost leadership, differentiation and trendsetting fashion); a brand repositioning campaign which built meaningful equity; and prioritisation of the people pipeline and skills development. During the period, key leadership changes were implemented, including the identification of an equity partner, which should continue to positively impact on CTM's performance. Italtile Retail The brand reported pleasing growth in sales and profitability and improved average stock turn. However, some margin was sacrificed due to an import substitute strategy centred on locally manufactured product. The customer shopping experience was improved with the introduction of innovative webstore and digital initiatives; roll out of the new store format; and an extended range of large format imported tiles and local porcelain tiles. While the Commercial Projects division delivered another strong performance, post year-end there has been a noticeable slowdown in commissioning of new developments, and generally, spend in the upper end of the market has declined as consumers defer investment in the current conditions.

TopT

The brand reported another strong performance, recording double-digit like-on-like sales and profit growth. Stock turn increased and average store inventory reduced. Some margin pressure was experienced in light of cost conscious customers buying down. TopT continued to benefit from successful implementation of the business optimisation programme (BOP); roll out of new stores to underserviced markets and a growing national presence; constant range re-evaluation and responsiveness to customer demand; and introduction of a range of profile building initiatives including a mobile store (Gig Rig), a webstore, community-linked marketing campaigns, and the launch of a dedicated training centre.

U-Light

During the review period, we commenced trialling a new lighting merchandise category which was rolled out to all the TopT stores. To test the scalability and viability of the U-Light offering as a standalone brand, five pilot stores will be opened in Gauteng by the end of August 2019; the five stores will each comprise a slightly different format and target a different market segment. This start-up business will benefit from existing store locations, customer base, business partners and an effective back-office set up.

MANUFACTURERS

Ceramic Industries

The acquisition of Ceramic some 20 months ago continues to deliver the gains envisaged, among them, a stronger combined balance sheet for future expansion, and improved planning and production efficiencies, benefiting both the stores and the factories. Tiles In the South African operation, solid results reported in the first half of the review period were eroded by a weaker performance in the second six months. While market share was gained by Gryphon's large format range, generally demand across the market was sluggish, with many wholesalers and retailers overstocked. In light of slow demand, kilns were shut off at four of Ceramic's factories in the third and fourth quarter of the year; this under-utilisation of capacity impacted negatively on margins and profit for the period and will continue to remain a challenge in the short term. The Australian operation reported improved profitability for the review period, and the investment to increase capacity and product range was completed. Focus will remain on reducing costs and improving yields across the operations.

Bathroomware and baths

Both Betta Sanitaryware and Betta Baths reported an improved second six months after a difficult first half. The new warehouse facility should be completed during the next financial year which will improve capacity management and service to customers. As with the tile factories, focus will remain on reducing costs and improving yields.

Ezee Tile

In the first half of the year, the business underperformed management's expectations, delivering disappointing margins and profits. While the remedial actions implemented in the second half have addressed operational inefficiencies and resulted in an improved performance in the latter six months, the business's results for the full year are not in line with targets. Good progress was achieved in upgrading the plant in Mombasa and developing new production facilities in Lusaka and Harare. The business also succeeded in gaining market share in the paint and construction chemicals segments.

SUPPLY CHAIN:

IMPORTERS

Cedar Point Improved sales and profit growth were reported for the year. Key focus areas were range rationalisation, reducing stock levels and improving stock turn. In the year ahead, better implementation of BOP will assist in establishing optimal stockholding and facilitating sell-through. Having successfully outsourced the warehouse function, management's primary focus will henceforth be on improved buying and operational co-ordination.

International Tap Distributors (ITD)

Competition intensified in the brassware category as an increasing number of opportunistic importers entered the market. Aggressive pricing and margin pressure were a constant feature in the review period, and in order to support cash-strapped customers, ITD reduced average selling prices, which further impacted on profits. Some opportunity exists to recover margins should the exchange rate stabilise favourably. Progress was achieved in rationalising the range and enhancing the in-stock position while simultaneously reducing overall stockholding, however, there is further room for improvement in terms of balancing business critical and supplementary stock.

Durban Distribution Centre

In the weak sales environment and given the overstocked position of numerous wholesalers, sales declined marginally although profits improved, based on intensified cost management. Good progress was made on rationalising ranges and reducing stockholding. In light of currency volatility and general margin pressure experienced in the industry, the business continues to investigate new suppliers in new markets.

PROPERTY INVESTMENT

As at 30 June 2019, the portfolio's estimated market value was R3,8 billion, comprising a retail portfolio valued at R3,0 billion (2018: R2,9 billion) and a manufacturing portfolio valued at R0,8 billion (2018: R0,8 billion). During the period capital expenditure of R312 million was incurred on the retail portfolio in respect of an ongoing store upgrade programme and the acquisition of five retail properties, while R189 million was invested across the manufacturing operations on plant, warehouse and equipment upgrades.

ORDINARY CASH DIVIDEND

The Board has declared a final gross ordinary cash dividend of 19,0 cents per share (2018: 21,0 cents per share), which together with the interim gross ordinary cash dividend of 22,0 cents per share (2018: 17,0 cents per share), produces a total gross ordinary cash dividend declared for the year ended 30 June 2019 of 41,0 cents per share (2018: 38,0 cents per share), an increase of 8%. The dividend cover remains at two-and-a-half times.

SPECIAL DIVIDEND

In light of the Group's strong cash generative nature and cash reserves being in excess of operational requirements, the Board has declared a special cash dividend in celebration of 50 years, of 50,0 cents per share (2018: 30,0 cents per share). Italtile is in the process of obtaining the relevant South African Reserve Bank approval in respect of the special dividend, and the Board has reasonably concluded that the Company will satisfy the solvency and liquidity test immediately after distribution thereof and for the next 12 months.

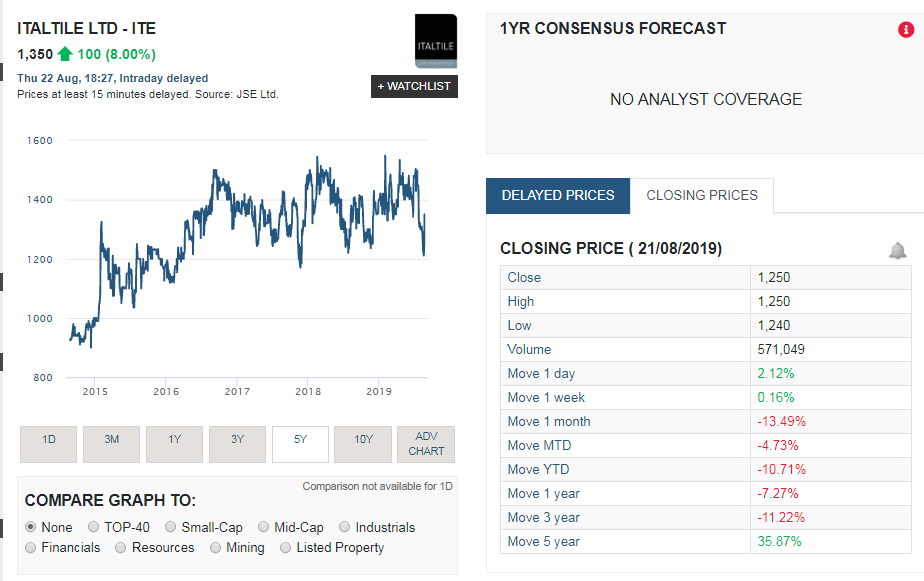

Italtile (ITE) share price performance over last 5 years

The image below, taken from Sharenet shows Italtile's share price performance over the last 5 years. and we must say the share price has held up pretty well considering the industry they operate in.

The summary below shows the share price returns of Italtile over various time periods:

The above shows that over the very short term Italtile has been struggling but when taking a long term view such as the last 5 years, the group actually provided shareholders with pretty decent returns. It should be noted that it is not the most liquid stock around so it doesn't change hands to often, and this might have been providing some protection for the group's share price over the years.

- 1 week: 0.16%

- 1 month: -13.49%

- Year to date (YTD): -10.71%

- 1 year: 7.27%

- 3 years: -11.22%

- 5 years: 45.87%

The above shows that over the very short term Italtile has been struggling but when taking a long term view such as the last 5 years, the group actually provided shareholders with pretty decent returns. It should be noted that it is not the most liquid stock around so it doesn't change hands to often, and this might have been providing some protection for the group's share price over the years.

Italtile stock valuation

Based on the group's financial results, their strong balance sheet and cash position and cash generating ability and the fact that inventories are well managed and trade and other receivables have been coming down and the group is paying a solid dividend and a special dividend we value the company's shares at R17.90 a share. Investors should note the stock is very illiquid and does not trade often so buying and selling it might become problematic.