|

Related Topics |

|

We take a look at the latest financial results of Invicta Holdings (IVT) for the period ending March 2019. So how has the equipment and engineering group been doing in this tough operating environment?

|

|

About Invicta (IVT)

Invicta Holdings listed on the JSE in 1989 and acquired Invicta Bearings Proprietary Limited in 1991. Bearings quickly became Invicta’s core business and the unrelated companies that initially formed part of the Group were sold. During the nineties various companies were added to the Group, including Autobax, Northmec, and CSE. In July 2000 Invicta acquired Bearing Man and completed a significant share repurchase program over the five years that followed. Invicta’s management continued to grow the Group and in 2013 acquired Kian Ann, a Singaporean company that distributes to over 50 countries. Other notable acquisitions included Equipment Spare Parts, Man-Dirk, HPE and Hyflo. During the 2018 financial year, Invicta disposed of its Building Supply Group (“BSG”) and decided to focus on its core competencies of industrial consumables, and capital equipment and spare parts. Invicta controls and manages assets of over R10 billion and employs over 4 500 people worldwide

Bearing Man Group (“BMG”)

• Engineering consumables including bearings, seals and gaskets, power transmission, material handling, fasteners, geared and electric drives and motors and tools;

• Fluid technology products and solutions including hydraulic, pneumatic, filtration and lubrication; and

• Technical design, on-site installation, maintenance, breakdown, condition monitoring as well as design engineering and failure analysis services Hyflo Group Hydraulic and pneumatic products and engineered solutions. Hansen Transmissions South Africa Industrial gearbox units. Man-Dirk Group (including SA Tool and Sibuyile Industrial Supplies) Tools and equipment, including personal protective equipment, lifting and welding products. OST Vibrator motors, tensioning and suspension systems. Screen Doctor Vibrating equipment and material handling solutions. Autobax Automotive components.

Our business model

Our business model is to invest in distribution businesses with strategic differentiation and competitive advantage in their respective markets. Invicta management works in close cooperation with the management teams of our respective businesses, to maximise growth, improve efficiencies, generate cash and improve returns on capital from our businesses. In addition, the team seeks and secures value enhancing acquisitions for the Group. Our philosophy is to run a small cost-effective head office with divisional management taking responsibility for daily operations. A flat management structure also ensures quick decision-making. We secure adequate and appropriate funding for the Group using the strength of our balance sheet. Capital is allocated to our businesses and projects offering the best returns. Our philosophy is to own the strategic properties from which the Group’s businesses operate. All our businesses seek to secure distribution rights to leading global brands and sources of supply. The businesses in turn add value to our customers by providing them with unrivalled availability of product from the significant inventories we hold and a superior level of technical service and support.

The Group offers a distribution footprint through its various own operations and approved distributors which provides a strategic asset for both investors and suppliers, a unique springboard into southern Africa and Asia. We are continuously looking to grow and diversify our spread of customers, market segments, suppliers and geographies such that risks are mitigated and growth is achieved

Bearing Man Group (“BMG”)

• Engineering consumables including bearings, seals and gaskets, power transmission, material handling, fasteners, geared and electric drives and motors and tools;

• Fluid technology products and solutions including hydraulic, pneumatic, filtration and lubrication; and

• Technical design, on-site installation, maintenance, breakdown, condition monitoring as well as design engineering and failure analysis services Hyflo Group Hydraulic and pneumatic products and engineered solutions. Hansen Transmissions South Africa Industrial gearbox units. Man-Dirk Group (including SA Tool and Sibuyile Industrial Supplies) Tools and equipment, including personal protective equipment, lifting and welding products. OST Vibrator motors, tensioning and suspension systems. Screen Doctor Vibrating equipment and material handling solutions. Autobax Automotive components.

Our business model

Our business model is to invest in distribution businesses with strategic differentiation and competitive advantage in their respective markets. Invicta management works in close cooperation with the management teams of our respective businesses, to maximise growth, improve efficiencies, generate cash and improve returns on capital from our businesses. In addition, the team seeks and secures value enhancing acquisitions for the Group. Our philosophy is to run a small cost-effective head office with divisional management taking responsibility for daily operations. A flat management structure also ensures quick decision-making. We secure adequate and appropriate funding for the Group using the strength of our balance sheet. Capital is allocated to our businesses and projects offering the best returns. Our philosophy is to own the strategic properties from which the Group’s businesses operate. All our businesses seek to secure distribution rights to leading global brands and sources of supply. The businesses in turn add value to our customers by providing them with unrivalled availability of product from the significant inventories we hold and a superior level of technical service and support.

The Group offers a distribution footprint through its various own operations and approved distributors which provides a strategic asset for both investors and suppliers, a unique springboard into southern Africa and Asia. We are continuously looking to grow and diversify our spread of customers, market segments, suppliers and geographies such that risks are mitigated and growth is achieved

Management overview of the results

Below an overview of the results by Invicta's management as contained in the SENS announcement.

Overview of the year

This has been one of the toughest years on record for the Group. Almost every sector served by the Group in South Africa (from which the Group derives about 76% of its revenue), has been under severe economic pressure. The generally poor economic conditions in South Africa, and months of uncertainty leading up to a general election in May 2019, contributed to a general decline in demand for products across our product range. It is therefore most pleasing to report that revenue for the Group increased by 5% to R10.450 billion. A number of acquisitions were made during the year, which contributed R254 million to revenue.

The challenging trading conditions resulted in a decline in gross margin, whilst overheads increased due to take-on and rationalisation costs of acquisitions and once-off costs of right sizing some existing underperforming businesses. As a result, operating profit declined from R839 million to R690 million. The tax dispute with SARS was settled for R750 million during the year and has been fully provided for in the accounts, of which R550 million was provided in prior years and R200 million in this year. R450 million of the settlement has been paid to SARS to date and the balance is payable over the next 4 years. Group performance

The operations comprise:

- ESG (Engineering Solutions Group) - distributor of engineering products (bearings, belts, tools, electric motors, hydraulics), technical services and solutions.

- CEG (Capital Equipment Group) - distributor of agricultural machinery, construction and earthmoving machinery, forklifts and related parts, including Kian Ann Engineering, which is based in Singapore. Profit for the year grew by 21% to R229 million with basic earnings per share up 62% and headline earnings per share up 93%. The interest received/paid and dividends received from financial investments have reduced substantially in the year under review due to the settlement of financial transactions.

The Group has reassessed the accounting treatment of the repurchase of agency distribution rights agreements within the ESG operations and the amortization of intangible assets primarily related to these rights. This has resulted in the restatement of financial information in the prior periods. The comparative financial information has accordingly been restated and is detailed in the relevant notes to the financial statements. ESG Revenue grew by 15% to R5.238 billion, of which R254 million came from acquisitions during the year.

Trading conditions were challenging, with the significant sectors which are serviced by ESG (mining, manufacturing, agriculture, general industry, construction) all experiencing headwinds during the year. These market conditions presented good acquisition opportunities, which ESG took advantage of. The acquisition of the Forge Industrial Group, which operates mainly in the Tool and Belting sectors of the economy, and the Driveshafts Parts business, operating in South Africa and Poland in the replacement drive shaft parts sectors, were concluded during the year. A total investment of R331 million was made in these businesses. The tool business was amalgamated with ESG's Mandirk (tool) business, but major restructuring was required to turn the business around. The turnaround strategy has, unfortunately, taken longer than expected to implement, but the combined tool business is expected to be profitable during the first quarter of the new financial year. The other core businesses in ESG have grown and the first phase of the consolidation and rationalisation of the logistics operations at BMG World are finally being completed and bedded down. CEG CEG revenue declined by 5% to R4.831 billion largely due to an overall decline in demand.

The sectors serviced by CEG

- agricultural machinery, construction machinery and the forklift sector

- all experienced a significant decline in unit sales and gross margin in South Africa, due to the prevailing market conditions. CEG's focus on annuity type business gave it protection and the improved contribution from Kian Ann Engineering Group (based in Singapore) helped CEG to limit its decline in segment operating profit before interest on financing transactions and foreign exchange movements to 17%. CEG has managed to maintain its market shares in South Africa and has once again managed to contain costs and generate cash. Strategic focus and prospects Trading conditions have settled since the elections in May 2019, but they still remain challenging. Management expects the coming year to be more positive than the year under review, but anticipates a slow return to growth. Management will focus on bedding down acquisitions, prioritising cash generation and return on equity.

Changes to the board and board committees Ms. N Rajmohamed was appointed as the Group Financial Director effective 1 July 2018. Mr. LR Sherrell was appointed to the audit committee on a temporary basis with effect from 16 November 2018. The board is in the process of appointing a new independent non-executive director to serve on the audit committee, which will bring its composition back in line with the recommendations of King IV. Ms. R Naidoo resigned effective 25 September 2018 as an independent non-executive director. There have been no further changes to the board or the membership of its committees. Dividend policy In light of the tax settlement and the resultant higher gearing in the group, the board has resolved not to declare a final dividend. It is anticipated that the normal dividend policy (of a total dividend cover ratio of 3.5 times at interim results adjusted to 2.75 times at year-end) will be resumed once cash flows and gearing permit. Appreciation

The board is once again highly appreciative to the executive management, the respective management teams of our businesses and most importantly all the staff, for the excellent commitment and performance in what can only be described as difficult and uncertain economic times. The board is confident that, with the strengths the Group possesses and the strategic plans, the Group will continue to deliver sustainable value to all stakeholders going forward.

Overview of the year

This has been one of the toughest years on record for the Group. Almost every sector served by the Group in South Africa (from which the Group derives about 76% of its revenue), has been under severe economic pressure. The generally poor economic conditions in South Africa, and months of uncertainty leading up to a general election in May 2019, contributed to a general decline in demand for products across our product range. It is therefore most pleasing to report that revenue for the Group increased by 5% to R10.450 billion. A number of acquisitions were made during the year, which contributed R254 million to revenue.

The challenging trading conditions resulted in a decline in gross margin, whilst overheads increased due to take-on and rationalisation costs of acquisitions and once-off costs of right sizing some existing underperforming businesses. As a result, operating profit declined from R839 million to R690 million. The tax dispute with SARS was settled for R750 million during the year and has been fully provided for in the accounts, of which R550 million was provided in prior years and R200 million in this year. R450 million of the settlement has been paid to SARS to date and the balance is payable over the next 4 years. Group performance

The operations comprise:

- ESG (Engineering Solutions Group) - distributor of engineering products (bearings, belts, tools, electric motors, hydraulics), technical services and solutions.

- CEG (Capital Equipment Group) - distributor of agricultural machinery, construction and earthmoving machinery, forklifts and related parts, including Kian Ann Engineering, which is based in Singapore. Profit for the year grew by 21% to R229 million with basic earnings per share up 62% and headline earnings per share up 93%. The interest received/paid and dividends received from financial investments have reduced substantially in the year under review due to the settlement of financial transactions.

The Group has reassessed the accounting treatment of the repurchase of agency distribution rights agreements within the ESG operations and the amortization of intangible assets primarily related to these rights. This has resulted in the restatement of financial information in the prior periods. The comparative financial information has accordingly been restated and is detailed in the relevant notes to the financial statements. ESG Revenue grew by 15% to R5.238 billion, of which R254 million came from acquisitions during the year.

Trading conditions were challenging, with the significant sectors which are serviced by ESG (mining, manufacturing, agriculture, general industry, construction) all experiencing headwinds during the year. These market conditions presented good acquisition opportunities, which ESG took advantage of. The acquisition of the Forge Industrial Group, which operates mainly in the Tool and Belting sectors of the economy, and the Driveshafts Parts business, operating in South Africa and Poland in the replacement drive shaft parts sectors, were concluded during the year. A total investment of R331 million was made in these businesses. The tool business was amalgamated with ESG's Mandirk (tool) business, but major restructuring was required to turn the business around. The turnaround strategy has, unfortunately, taken longer than expected to implement, but the combined tool business is expected to be profitable during the first quarter of the new financial year. The other core businesses in ESG have grown and the first phase of the consolidation and rationalisation of the logistics operations at BMG World are finally being completed and bedded down. CEG CEG revenue declined by 5% to R4.831 billion largely due to an overall decline in demand.

The sectors serviced by CEG

- agricultural machinery, construction machinery and the forklift sector

- all experienced a significant decline in unit sales and gross margin in South Africa, due to the prevailing market conditions. CEG's focus on annuity type business gave it protection and the improved contribution from Kian Ann Engineering Group (based in Singapore) helped CEG to limit its decline in segment operating profit before interest on financing transactions and foreign exchange movements to 17%. CEG has managed to maintain its market shares in South Africa and has once again managed to contain costs and generate cash. Strategic focus and prospects Trading conditions have settled since the elections in May 2019, but they still remain challenging. Management expects the coming year to be more positive than the year under review, but anticipates a slow return to growth. Management will focus on bedding down acquisitions, prioritising cash generation and return on equity.

Changes to the board and board committees Ms. N Rajmohamed was appointed as the Group Financial Director effective 1 July 2018. Mr. LR Sherrell was appointed to the audit committee on a temporary basis with effect from 16 November 2018. The board is in the process of appointing a new independent non-executive director to serve on the audit committee, which will bring its composition back in line with the recommendations of King IV. Ms. R Naidoo resigned effective 25 September 2018 as an independent non-executive director. There have been no further changes to the board or the membership of its committees. Dividend policy In light of the tax settlement and the resultant higher gearing in the group, the board has resolved not to declare a final dividend. It is anticipated that the normal dividend policy (of a total dividend cover ratio of 3.5 times at interim results adjusted to 2.75 times at year-end) will be resumed once cash flows and gearing permit. Appreciation

The board is once again highly appreciative to the executive management, the respective management teams of our businesses and most importantly all the staff, for the excellent commitment and performance in what can only be described as difficult and uncertain economic times. The board is confident that, with the strengths the Group possesses and the strategic plans, the Group will continue to deliver sustainable value to all stakeholders going forward.

Financial overview of Invicta for period ending March 2019

So enough of the management commentary and updates already. Lets get to the numbers.

- Revenue : R10.45 billion (up 5% from R9.99 billion)

- Gross profit: R2.987 billion (down 1.8% from R3.041 billion)

- Net profit: R228.6 million (up 21% from R188 million in prior period)

- Headline earnings per share: R1.12 (up from 58c the previous period)

- PE ratio: 20.8

- No dividend has been declared since the group has a massive tax bill it needs to settle which ate into all available cash and increased the group's gearing. The group had the following to say regarding the dividend. "In light of the tax settlement and the resultant higher gearing in the group, the board has resolved not to declare a final dividend. It is anticipated that the normal dividend policy (of a total dividend cover ratio of 3.5 times at interim results adjusted to 2.75 times at year-end) will be resumed once cash flows and gearing permit.

- Net asset value (NAV): R40.85 up 7.4% from R38.05 in the prior year

- Cash generated by operations: R836 million

- Cash generated per share: R7.81

- Tobin's Q: 0.22. Thus the group's market capital is just 22% of the value of their total assets (note this refers to total assets not net assets after paying all debts). A Tobin's Q below one is usually an indication of a undervalued stock.

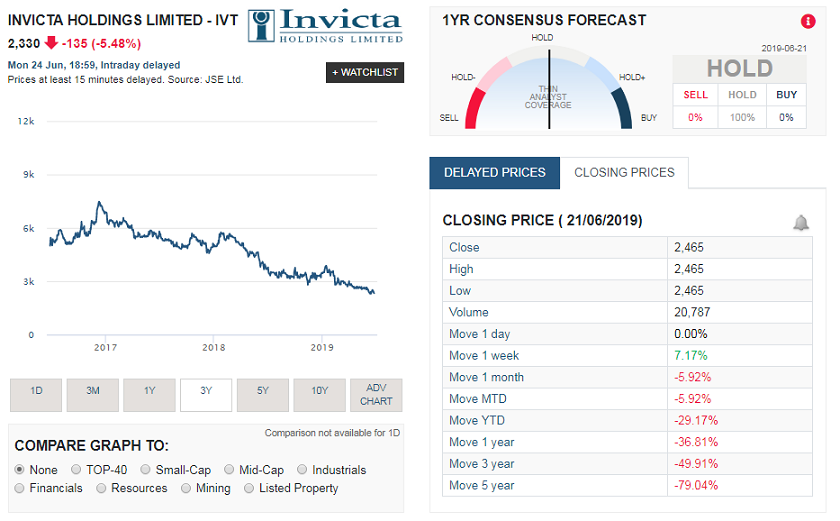

So how has the Invicta (IVT) share price been doing?

The graphic below shows how IVT share price has been performing in recent years, and as readers can see Invicta's current share price is in a long term downward trend in the last number of years considering the highs reached in 2017, showing just how tough the going has been for the group. The screenshot was taken from Sharenet

The summary below shows the share price performance of Famous Brands (FBR) over various time periods:

- 1 week: 7.2%

- 1 month: -5.92%

- Year to date: -29.2%

- 1 year: -36.81%

- 3 years: -49.91%

So should you buy IVT shares?

You must be very brave and have a lot of patience if you looking to buy Invicta right now to make money off it. While the saying goes its always darkest before dawn, the group has been struggling in recent years and their massive tax settlement amount set the group back substantially So much so that they stopped paying a dividend until their cash situation improves again.

They have a strong balance, generate a lot of cash per share, they are trading well below their stated net asset value and Tobin's Q suggests that the stock is undervalued. But we would caution investors against buying the stock right now unless you have money to lose over the short run or have a lot of time and patience to wait out the difficult times for the group. They do have a strong business and the underlying companies they own are profitable, but it will take time for the group's wounds to heal fully. Based on their current financials we valued the group at a R33.50 a share. But this is once the market looks past its current tax settlement problems. So if you really want to risk it and wait it out with Invicta, we believe they offer VERY long term value. But due to the illiquid nature of the stock it might not trade regularly so buying or selling the share might become a problem as the spread between buyers and sellers will in all likelihood be pretty wide.

They have a strong balance, generate a lot of cash per share, they are trading well below their stated net asset value and Tobin's Q suggests that the stock is undervalued. But we would caution investors against buying the stock right now unless you have money to lose over the short run or have a lot of time and patience to wait out the difficult times for the group. They do have a strong business and the underlying companies they own are profitable, but it will take time for the group's wounds to heal fully. Based on their current financials we valued the group at a R33.50 a share. But this is once the market looks past its current tax settlement problems. So if you really want to risk it and wait it out with Invicta, we believe they offer VERY long term value. But due to the illiquid nature of the stock it might not trade regularly so buying or selling the share might become a problem as the spread between buyers and sellers will in all likelihood be pretty wide.