|

Related Topics |

|

We take a look at struggling food group, Famous Brands latest financial results. And we say struggling food group as their entry into the UK market with the acquisition of Gourmet Burger Kitchen (GBK) has blown up in their face. They have written down a massive chunk of their R2 billion odd investment in GBK. So how did things go for the group for the half year ending 31 August 2019

|

|

About Famous Brands

Famous Brands owns a large number of franchised restaurants, coffee shops and bars. And they have been fueling their growth over the last number of years by way of acquisition. They have been on a tremendous buying spree and they were hoping to replicate their local, South African success in the UK with the acquisition of GBK. However they are finding that it is a lot harder to do this than what they initiall thought. They bought GBK for almost R2billion, and recently announced a significant write off on that acquisition. But we will get to that soon. So which brands belong to the Famous Brands group?

Well they own the following brands (note we only listing a few of their brands below).

Well they own the following brands (note we only listing a few of their brands below).

- Mugg & Bean

- Wimpy

- Fishaways

- Debonairs

- Steers

- Vovo Telo

- Tashas

- Keg

- Mythos

- Turn 'n Tender

- Milky Lane

- Salsa Mexican Grill

- Giramundo

So whats contained in their financial results for the period ending 31 August 2019

Across our trading markets, consumer behaviour continued to be driven by the demand for convenience, value and enhanced brand experiences. This was represented by the following growing trends:

• outperformance of take-away and fast food outlets at the expense of restaurants and coffee shops, reflecting their perceived convenience and value propositions;

• the sustained strong move to online and home delivery (with a related decline in footfall in shopping malls, specifically major centres);

• a heightened focus on differentiated in-store experiences (including enhanced technology aimed at improving service);

• proliferation of bespoke Customer Relationship Management programmes recognising and rewarding individual customers; and

• new store openings targeted at previously underserviced customers (including entry into outlying markets and diversification of convenience-centred formats ranging from drive-through to mobile carts and containers).

SA

Locally, consumer and business confidence remained at low levels throughout the review period. Sustained financial hardship and subdued economic growth were exacerbated by country-specific risk factors which continued to cause general sociopolitical uncertainty and discontent. While competition in the market remained intense, the aggressive and unrealistic pricing evident in recent years has settled to a more rational level, as international newcomers have become part of the established landscape or exited, and independent operators trading on unsustainable margins were rationalised. The impact of deteriorating economic conditions in certain provinces resulted in stark differences in regional performance. Worst affected areas were Limpopo and the North West, while the Western and Eastern Cape were less buoyant than recent trends. Stronger results were reported by Gauteng. Significantly, low food inflation remained a major factor during the review period, restricting opportunities to increase menu pricing in the context of constrained consumer disposable income.

UK

Uncertainty arising from the recent change in political leadership as well as progress regarding Brexit weighed heavily on consumer sentiment during the review period

Group Performance

The business delivered solid results in a challenging environment. Particularly pleasing was the good performance reported in the Brands division. Disappointingly, this improved performance did not pull through to the Supply Chain, which experienced weaker sales and significant margin pressure. Our key strategic focus areas during the review period were to:

• enhance the profitability of our franchise partners and the viability of the franchise model;

• ensure the improvement of returns for stakeholders through refining and implementing our long-term strategy for GBK Restaurants Limited (GBK); and

• optimise allocation of capital in the business.

Good progress was achieved across these focus areas:

• the franchise network is stable, and we continue to monitor and support our partners in a tough environment. To ensure that the total value chain delivers franchisee profitability, we implemented a range of initiatives including re-engineering and optimising menus, reducing costs and improving operational efficiencies, and absorbing margins in the Supply Chain to enable it to remain competitive against peer offerings;

• our strategy to entrench the gold standard in the GBK business continued to deliver benefits, resulting in a more focused and relevant offering and an improvement in costs and efficiencies. Activities included product innovation and renovation and menu design and rationalisation; and

• the goal to ensure investment in areas providing the best returns and exit non-core business was advanced through improved allocation of capital to the appropriate business units in our operations and rationalisation of underperforming brands and stores. Working capital management continues to be a keen focus area to ensure that cash from operations is optimised for future investment.

• outperformance of take-away and fast food outlets at the expense of restaurants and coffee shops, reflecting their perceived convenience and value propositions;

• the sustained strong move to online and home delivery (with a related decline in footfall in shopping malls, specifically major centres);

• a heightened focus on differentiated in-store experiences (including enhanced technology aimed at improving service);

• proliferation of bespoke Customer Relationship Management programmes recognising and rewarding individual customers; and

• new store openings targeted at previously underserviced customers (including entry into outlying markets and diversification of convenience-centred formats ranging from drive-through to mobile carts and containers).

SA

Locally, consumer and business confidence remained at low levels throughout the review period. Sustained financial hardship and subdued economic growth were exacerbated by country-specific risk factors which continued to cause general sociopolitical uncertainty and discontent. While competition in the market remained intense, the aggressive and unrealistic pricing evident in recent years has settled to a more rational level, as international newcomers have become part of the established landscape or exited, and independent operators trading on unsustainable margins were rationalised. The impact of deteriorating economic conditions in certain provinces resulted in stark differences in regional performance. Worst affected areas were Limpopo and the North West, while the Western and Eastern Cape were less buoyant than recent trends. Stronger results were reported by Gauteng. Significantly, low food inflation remained a major factor during the review period, restricting opportunities to increase menu pricing in the context of constrained consumer disposable income.

UK

Uncertainty arising from the recent change in political leadership as well as progress regarding Brexit weighed heavily on consumer sentiment during the review period

Group Performance

The business delivered solid results in a challenging environment. Particularly pleasing was the good performance reported in the Brands division. Disappointingly, this improved performance did not pull through to the Supply Chain, which experienced weaker sales and significant margin pressure. Our key strategic focus areas during the review period were to:

• enhance the profitability of our franchise partners and the viability of the franchise model;

• ensure the improvement of returns for stakeholders through refining and implementing our long-term strategy for GBK Restaurants Limited (GBK); and

• optimise allocation of capital in the business.

Good progress was achieved across these focus areas:

• the franchise network is stable, and we continue to monitor and support our partners in a tough environment. To ensure that the total value chain delivers franchisee profitability, we implemented a range of initiatives including re-engineering and optimising menus, reducing costs and improving operational efficiencies, and absorbing margins in the Supply Chain to enable it to remain competitive against peer offerings;

• our strategy to entrench the gold standard in the GBK business continued to deliver benefits, resulting in a more focused and relevant offering and an improvement in costs and efficiencies. Activities included product innovation and renovation and menu design and rationalisation; and

• the goal to ensure investment in areas providing the best returns and exit non-core business was advanced through improved allocation of capital to the appropriate business units in our operations and rationalisation of underperforming brands and stores. Working capital management continues to be a keen focus area to ensure that cash from operations is optimised for future investment.

Update from Famous Brands on Gourmet Burger Kitchen

In line with management’s projections, the business made good progress, benefiting from the extensive range of operational improvements implemented, together with the Company Voluntary Arrangement (CVA) restructuring programme completed over the past year. Despite the subdued economy and general pressure experienced by the industry, GBK’s like-for-like sales grew, attributable to intensified focus on the quality of the offering (product and experience); a targeted reinvestment in refurbishments; an intensified campaign to upweight online sales; and improved management of efficiencies and costs.

Revenue in Rand terms decreased by 7% to R640.7 million (2018: R691.6 million), while revenue in Sterling was 13% lower. Notably, the business reduced its operating loss by 76% from (R45.4 million) in the prior corresponding period to (R10.7 million). The operating margin improved from (6.6%) in the prior comparable period to (1.7%). The operating loss improvement includes R16.2 million related to the adoption of IFRS 16, which has an impact of 2.5% on the operating margin improvement. System-wide UK sales (Sterling) declined by 12.5% (2018: decrease of 6.8%), due to the closure of 24 stores as part of the CVA process, seven of which were closed during the review period. Significantly, like-for-like sales increased by 8.6% (2018: decrease of 9.7%).

While dine-in sales declined in line with sector trends, online and delivery sales grew strongly, supported by promotional activity. External benchmarks confirm that the business tracked ahead of the market during the six months, building on the momentum evident in the second half of the prior financial year. Notably, like-for-like sales post the end of the review period have remained positive. Three restaurants underwent full revamps, while 30 other sites received kerbside makeovers in the six months under review. At the close of the reporting period, GBK’s footprint comprised 73 stores.

Revenue in Rand terms decreased by 7% to R640.7 million (2018: R691.6 million), while revenue in Sterling was 13% lower. Notably, the business reduced its operating loss by 76% from (R45.4 million) in the prior corresponding period to (R10.7 million). The operating margin improved from (6.6%) in the prior comparable period to (1.7%). The operating loss improvement includes R16.2 million related to the adoption of IFRS 16, which has an impact of 2.5% on the operating margin improvement. System-wide UK sales (Sterling) declined by 12.5% (2018: decrease of 6.8%), due to the closure of 24 stores as part of the CVA process, seven of which were closed during the review period. Significantly, like-for-like sales increased by 8.6% (2018: decrease of 9.7%).

While dine-in sales declined in line with sector trends, online and delivery sales grew strongly, supported by promotional activity. External benchmarks confirm that the business tracked ahead of the market during the six months, building on the momentum evident in the second half of the prior financial year. Notably, like-for-like sales post the end of the review period have remained positive. Three restaurants underwent full revamps, while 30 other sites received kerbside makeovers in the six months under review. At the close of the reporting period, GBK’s footprint comprised 73 stores.

Outlook for Famous Brands group

Prospects

In the prior comparable period, the strong performance anticipated from our peak trading period failed to materialise in the context of weak consumer sentiment and spend. Management is cautiously optimistic that wide ranging initiatives to provide consumers with ease of access to our brands and to deliver unique customer experiences at every touchpoint will provide the Group with a competitive advantage during the forthcoming holiday season. Notwithstanding macro-economic challenges faced in the Supply Chain, an improved performance in the Brands division should filter through and positively impact on the Manufacturing and Logistics divisions.

Brands

In line with previous years, it is anticipated that Black Friday sales will produce lumpy results leading up to and following what is now one of the biggest trading weekends on the annual calendar. In terms of the holiday season, preparations are well advanced to capture disposable income over the peak December period and into the slower trading environment traditionally experienced in January. Across our markets, the major shift to ”remote convenience” via online ordering and home delivery will afford challenges and opportunities in equal measure for the Group. Our priority will be to make optimal use of technology to improve the experience and service for our customers.

SA and AME

In the forthcoming period, we will continue to strengthen our marketing capability across all channels and leverage our online ordering and home delivery across all the brands; expand our strategic alliance partnerships and roll out new trading formats; and ensure our supply chain and cost drivers provide support for our brands and franchise partners.

UK

In the GBK operation, our focus will remain on leveraging efficiencies achieved over the period and driving profitability and margin growth across the operation. The trading environment is expected to remain challenging for at least the medium term, with a return to profitability anticipated by the end of the 2022 financial year.

Supply Chain

In light of muted demand and anticipated sustained low food inflation, the focus will be on adapting to the competitive landscape and leveraging efficiencies in the business. Cost optimisation across the operation will continue to be prioritised.

Logistics

We will progress the upgrade programme designed to improve capability and capacity of our Logistics operation to accommodate growth over the next decade. The commissioning of the new Free State facility during the review period will substantially improve efficiencies and enhance the service to our franchise partners. The next phase of the programme, comprising the opening of the Western Cape facility, is scheduled for October 2019.

Manufacturing

Restoring the profitability of the LBF business will remain a priority, and opportunities to unlock further capacity across all our plants will continue to be explored. The Group’s distribution of licensed retail products to third-party customers has traditionally been outsourced. With effect from 1 October 2019, this business was brought in-house, providing both the Logistics division and the retail Manufacturing businesses with important opportunities to grow capacity.

Dividend

The Board is pleased to declare a dividend payment of 90 cents for the review period. No dividend was declared for the period ended 31 August 2018. The Board will continue to monitor the trading environment, the Group’s future performance, its operating requirements and acquisition opportunities to determine further dividend payments.

In the prior comparable period, the strong performance anticipated from our peak trading period failed to materialise in the context of weak consumer sentiment and spend. Management is cautiously optimistic that wide ranging initiatives to provide consumers with ease of access to our brands and to deliver unique customer experiences at every touchpoint will provide the Group with a competitive advantage during the forthcoming holiday season. Notwithstanding macro-economic challenges faced in the Supply Chain, an improved performance in the Brands division should filter through and positively impact on the Manufacturing and Logistics divisions.

Brands

In line with previous years, it is anticipated that Black Friday sales will produce lumpy results leading up to and following what is now one of the biggest trading weekends on the annual calendar. In terms of the holiday season, preparations are well advanced to capture disposable income over the peak December period and into the slower trading environment traditionally experienced in January. Across our markets, the major shift to ”remote convenience” via online ordering and home delivery will afford challenges and opportunities in equal measure for the Group. Our priority will be to make optimal use of technology to improve the experience and service for our customers.

SA and AME

In the forthcoming period, we will continue to strengthen our marketing capability across all channels and leverage our online ordering and home delivery across all the brands; expand our strategic alliance partnerships and roll out new trading formats; and ensure our supply chain and cost drivers provide support for our brands and franchise partners.

UK

In the GBK operation, our focus will remain on leveraging efficiencies achieved over the period and driving profitability and margin growth across the operation. The trading environment is expected to remain challenging for at least the medium term, with a return to profitability anticipated by the end of the 2022 financial year.

Supply Chain

In light of muted demand and anticipated sustained low food inflation, the focus will be on adapting to the competitive landscape and leveraging efficiencies in the business. Cost optimisation across the operation will continue to be prioritised.

Logistics

We will progress the upgrade programme designed to improve capability and capacity of our Logistics operation to accommodate growth over the next decade. The commissioning of the new Free State facility during the review period will substantially improve efficiencies and enhance the service to our franchise partners. The next phase of the programme, comprising the opening of the Western Cape facility, is scheduled for October 2019.

Manufacturing

Restoring the profitability of the LBF business will remain a priority, and opportunities to unlock further capacity across all our plants will continue to be explored. The Group’s distribution of licensed retail products to third-party customers has traditionally been outsourced. With effect from 1 October 2019, this business was brought in-house, providing both the Logistics division and the retail Manufacturing businesses with important opportunities to grow capacity.

Dividend

The Board is pleased to declare a dividend payment of 90 cents for the review period. No dividend was declared for the period ended 31 August 2018. The Board will continue to monitor the trading environment, the Group’s future performance, its operating requirements and acquisition opportunities to determine further dividend payments.

Fish Aways, one of Famous Brand's fast food and take out brands

Highlights of their interim financial results for the period ending 31 August 2019

So enough of the management commentary and updates already. Lets get to the numbers.

- Revenue: R3.569 billion (down from R3.583 billion)

- Cost of sales: R1.809 billion (up from R1.667 billion)

- Profit for the period: R192.4 million (up from a loss of almost R600 million due to GBK write offs)

- Headline earnings per share: R1.59 (up from -R5.70 for the same period of the previous year)

- Cash generated from operations: R296.4 million

- Cash generated per share: R2.91

- Cash on balance sheet: R427.6 million

- Cash on balance sheet per share: R4.21 (or 5.4% of share price)

- Net asset value per share: R16.24 (so the group is trading at4.85 times its book value)

- Interim dividend: R0.90 a share

- Dividend yield: 2.28%

- PE ratio: 24.7(which is well above the overall market average PE ratio)

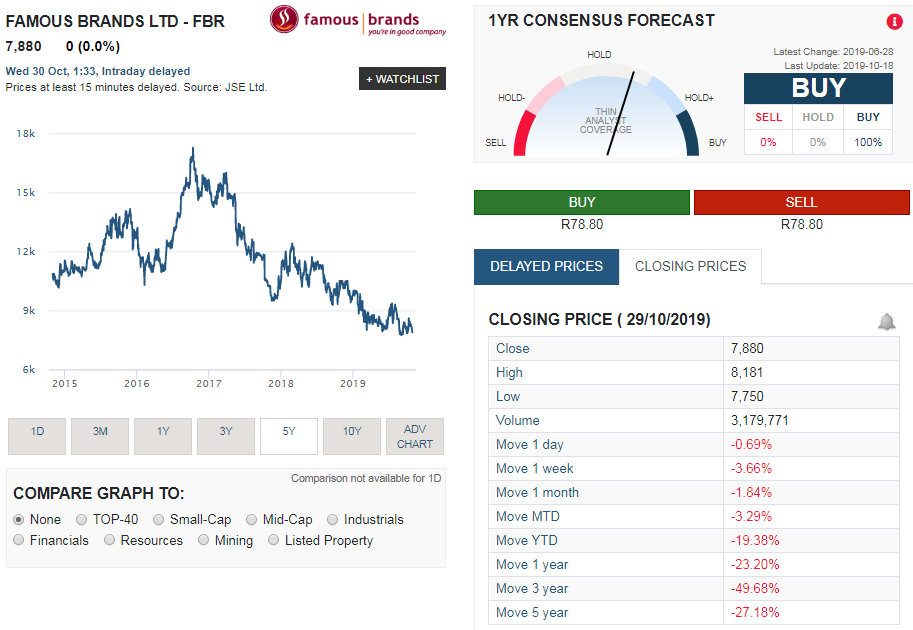

So how has FBR's share price been doing?

The graphic below shows how FBR's share price has been performing in recent years, and as readers can see FBR current share price is a long way off from the highs reached just a few years ago, showing just how tough the going has been for the group. The screenshot was taken from Sharenet

The summary below shows the share price performance of Famous Brands (FBR) over various time periods:

- 1 week: -3.66%

- 1 month: -1.84%

- Year to date: -19.38%

- 1 year: -23.20%

- 3 years: -49.68%

- 5 years: -27.18%

So should you buy FBR shares?

At this point in time, we would not recommend buying into the fast food/ casual dining market. South African consumers are struggling, the Food and Beverages sector has been spinning its wheels in South Africa for a while now, and FBR with their issues in the UK will be focused on trying to get that fixed, which according to us will leave management with less time to focus on South Africa and expanding their business and footprint here, in a market that is already struggling. They not the biggest dividend payer, they trading on a very high PE ratio, but on the positive side they have extremely strong cash generation. But overall we recommend staying away from FBR at this point in time.

But if you really want a benchmark or target price for Famous Brands (FBR), taking all their financials, their brands, their markets and their current issues and obstacles into account, our valuation model places a value of R71.20 per share on FBR (up slightly from our last full year financial results valuation of Famous Brands). Based on Famous Brands' current price feel that they are overvalued and would not recommend investing in them or any other company active in the sector right now

But if you really want a benchmark or target price for Famous Brands (FBR), taking all their financials, their brands, their markets and their current issues and obstacles into account, our valuation model places a value of R71.20 per share on FBR (up slightly from our last full year financial results valuation of Famous Brands). Based on Famous Brands' current price feel that they are overvalued and would not recommend investing in them or any other company active in the sector right now